USA Bone Graft and Substitutes Market Outlook to 2030

Region:North America

Author(s):Meenakshi

Product Code:KROD2180

Region:North America

Author(s):Meenakshi

Product Code:KROD2180

November 2024

84

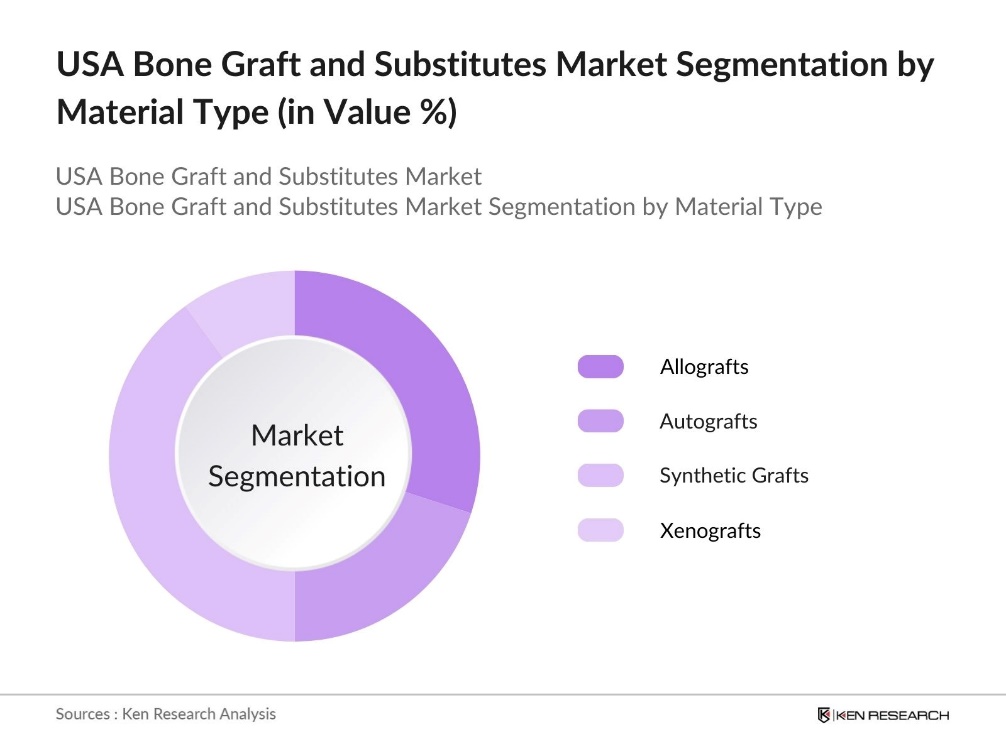

By Material Type: The USA bone graft and substitutes market is segmented by material type into allografts, autografts, synthetic grafts, and xenografts. Synthetic grafts, such as hydroxyapatite and tricalcium phosphate, are currently dominating the market due to their biocompatibility and the ease of availability. Synthetic grafts offer a lower risk of disease transmission compared to allografts and xenografts and can be customized for specific clinical needs. Their increasing use in spinal fusion surgeries and the development of bioresorbable materials have further solidified their leading position in the market.

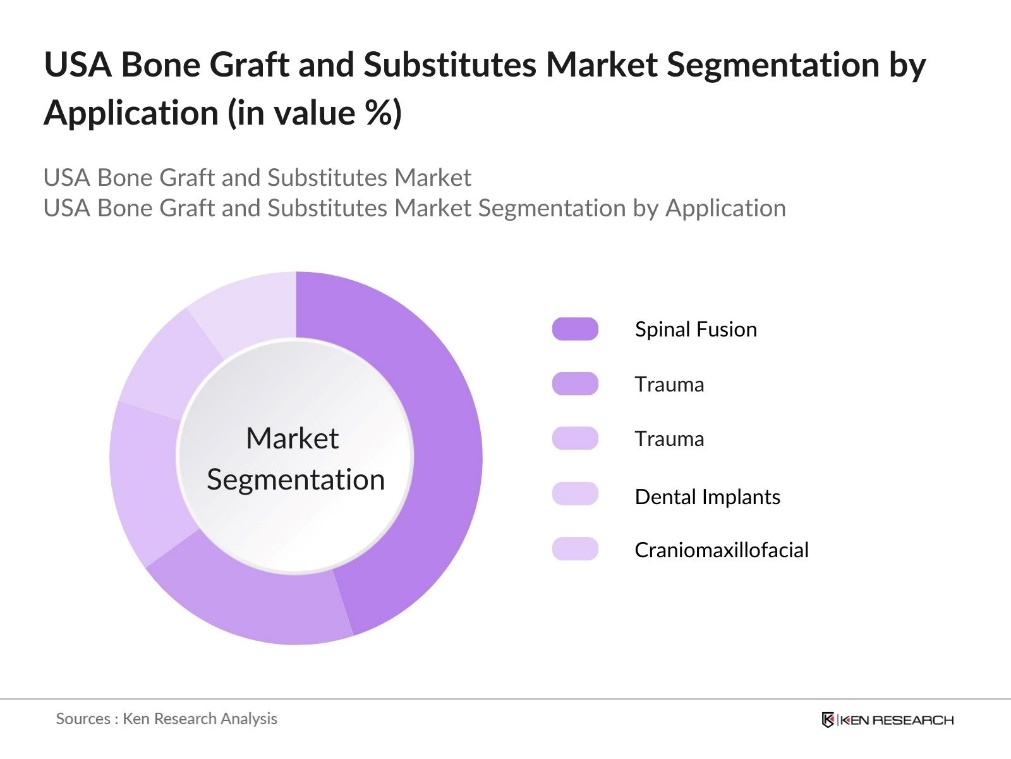

By Application: The USA bone graft and substitutes market is segmented by application into spinal fusion, trauma, joint reconstruction, dental implants, and craniomaxillofacial procedures. Spinal fusion procedures hold the largest share of the market due to the rising incidence of spinal disorders and the increasing demand for minimally invasive surgeries. In particular, the aging population in the U.S. is driving demand for these procedures, as conditions like degenerative disc disease become more prevalent. Spinal fusion surgeries are expected to continue dominating as advanced bone graft substitutes, such as those based on 3D printing and biologics, gain traction.

The USA bone graft and substitutes market is dominated by a few key players, including major medical device companies and specialists in biomaterials. The landscape is highly competitive, with players engaging in strategic mergers and acquisitions, collaborations, and constant innovation to maintain market dominance. For example, companies like Medtronic and Stryker lead the market due to their broad product portfolios, global reach, and commitment to R&D in orthopedic solutions.

|

Company Name |

Establishment Year |

Headquarters |

Product Portfolio |

Revenue (2023, USD Mn) |

FDA Approvals |

R&D Investment |

Number of Employees |

Global Presence |

|

Medtronic |

1949 |

Dublin, Ireland |

||||||

|

Stryker Corporation |

1941 |

Michigan, USA |

||||||

|

Zimmer Biomet |

1927 |

Warsaw, Indiana, USA |

||||||

|

NuVasive, Inc. |

1997 |

California, USA |

||||||

|

DePuy Synthes (J&J) |

1895 |

New Jersey, USA |

Over the next few years, the USA bone graft and substitutes market is expected to witness significant growth driven by technological advancements in graft materials, the rising number of orthopedic and spinal surgeries, and the increasing aging population. The development of personalized medicine, including custom graft materials through 3D printing and stem cell therapies, will likely create new opportunities in the market. In addition, the trend toward minimally invasive surgical techniques is expected to further boost the demand for bone graft substitutes, especially in urban centers with advanced healthcare infrastructure.

|

Material Type |

Allografts Autografts Synthetic Grafts (Hydroxyapatite, Calcium sulfate, etc.) Xenografts |

|

Application |

Spinal Fusion Trauma Joint Reconstruction Dental Implants Craniomaxillofacial |

|

End User |

Hospitals Ambulatory Surgical Centers Specialty Clinics Research & Academic Institutes |

|

Region |

Northeast Midwest South West |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Annual growth rate, CAGR)

1.4. Market Segmentation Overview

2.1. Historical Market Size (Market value in $USD)

2.2. Year-On-Year Growth Analysis (YOY market performance)

2.3. Key Market Developments and Milestones (Notable FDA approvals, partnerships, product launches)

3.1. Growth Drivers

3.1.1. Rising incidence of orthopedic conditions (osteoporosis, spinal fusion surgeries)

3.1.2. Increasing adoption of minimally invasive surgeries

3.1.3. Technological advancements (3D printing, bioactive graft materials)

3.1.4. Favorable reimbursement policies (Medicare/Medicaid coverage)

3.2. Market Challenges

3.2.1. High costs associated with bone graft procedures

3.2.2. Risk of complications (immune rejection, infection in allografts)

3.2.3. Lack of skilled professionals in rural areas

3.3. Opportunities

3.3.1. Increased R&D funding for synthetic and bio-composite grafts

3.3.2. Growth in outpatient and ambulatory surgical centers

3.3.3. Expansion in personalized medicine and custom implants

3.4. Trends

3.4.1. Shift toward synthetic bone graft substitutes

3.4.2. Integration of nanotechnology and biomaterials

3.4.3. Growing focus on patient-specific solutions through AI and 3D modeling

3.5. Government Regulation

3.5.1. FDA Regulatory Pathways (510(k) clearances, PMAs)

3.5.2. Compliance with medical device standards (ISO 13485)

3.5.3. HIPAA and data security regulations for clinical trials

3.6. SWOT Analysis

3.6.1. Strengths

3.6.2. Weaknesses

3.6.3. Opportunities

3.6.4. Threats

3.7. Stake Ecosystem (Manufacturers, distributors, healthcare providers)

3.8. Porters Five Forces

3.8.1. Bargaining Power of Suppliers

3.8.2. Bargaining Power of Buyers

3.8.3. Threat of New Entrants

3.8.4. Threat of Substitutes

3.8.5. Competitive Rivalry

3.9. Competition Ecosystem (Industry dynamics, market share, innovation strategy)

4.1. By Material Type (In Value %)

4.1.1. Allografts (Demineralized bone matrix (DBM), others)

4.1.2. Autografts

4.1.3. Synthetic Grafts (Hydroxyapatite, Calcium sulfate, others)

4.1.4. Xenografts

4.2. By Application (In Value %)

4.2.1. Spinal Fusion

4.2.2. Trauma

4.2.3. Joint Reconstruction

4.2.4. Dental Implants

4.2.5. Craniomaxillofacial

4.3. By End User (In Value %)

4.3.1. Hospitals

4.3.2. Ambulatory Surgical Centers (ASCs)

4.3.3. Specialty Clinics

4.3.4. Research and Academic Institutes

4.4. By Region (In Value %)

4.4.1. Northeast

4.4.2. Midwest

4.4.3. South

4.4.4. West

5.1. Detailed Profiles of Major Competitors

5.1.1. Medtronic

5.1.2. Stryker Corporation

5.1.3. Zimmer Biomet

5.1.4. Johnson & Johnson (DePuy Synthes)

5.1.5. NuVasive, Inc.

5.1.6. Orthofix Medical Inc.

5.1.7. Baxter International

5.1.8. AlloSource

5.1.9. Bioventus

5.1.10. Integra LifeSciences Holdings Corporation

5.1.11. SeaSpine Holdings Corporation

5.1.12. RTI Surgical

5.1.13. Osiris Therapeutics

5.1.14. Wright Medical Group

5.1.15. Xtant Medical

5.2. Cross Comparison Parameters (Revenue, product portfolio, R&D investment, market presence, product recalls, FDA approvals, strategic alliances)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Product innovations, collaborations, geographical expansions)

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Capital investments, partnerships)

5.7. Government Grants and Incentives

5.8. Private Equity and Venture Capital Investments

6.1. FDA Approval Process

6.2. ISO and CE Marking Requirements

6.3. Compliance with HIPAA for Data Security

6.4. Medicare and Medicaid Reimbursement Policies

7.1. Future Market Size Projections (Forecasts based on trends in technology, population aging, surgery volumes)

7.2. Key Factors Driving Future Market Growth (R&D breakthroughs, clinical outcomes, policy changes)

8.1. By Material Type (In Value %)

8.2. By Application (In Value %)

8.3. By End User (In Value %)

8.4. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial phase involves mapping out the entire ecosystem within the USA bone graft and substitutes market. Through extensive desk research, including proprietary databases and publicly available government data, we identified critical variables such as the volume of surgeries, product adoption rates, and reimbursement scenarios.

In this phase, historical data on the adoption of bone graft substitutes in orthopedic and dental surgeries were analyzed. We compiled data on market penetration and constructed revenue estimates by considering sales volumes and pricing from industry reports and government sources.

Interviews were conducted with industry experts, including medical professionals, product managers, and regulatory specialists, to validate key hypotheses. The expert insights provided clarity on the market dynamics and verified trends in technology adoption and material preference.

In this final stage, our research was cross-verified through engagement with leading medical device manufacturers, ensuring that the statistics and insights reflected real-world market conditions. The synthesis of primary and secondary research enabled the construction of a robust analysis of the USA bone graft and substitutes market.

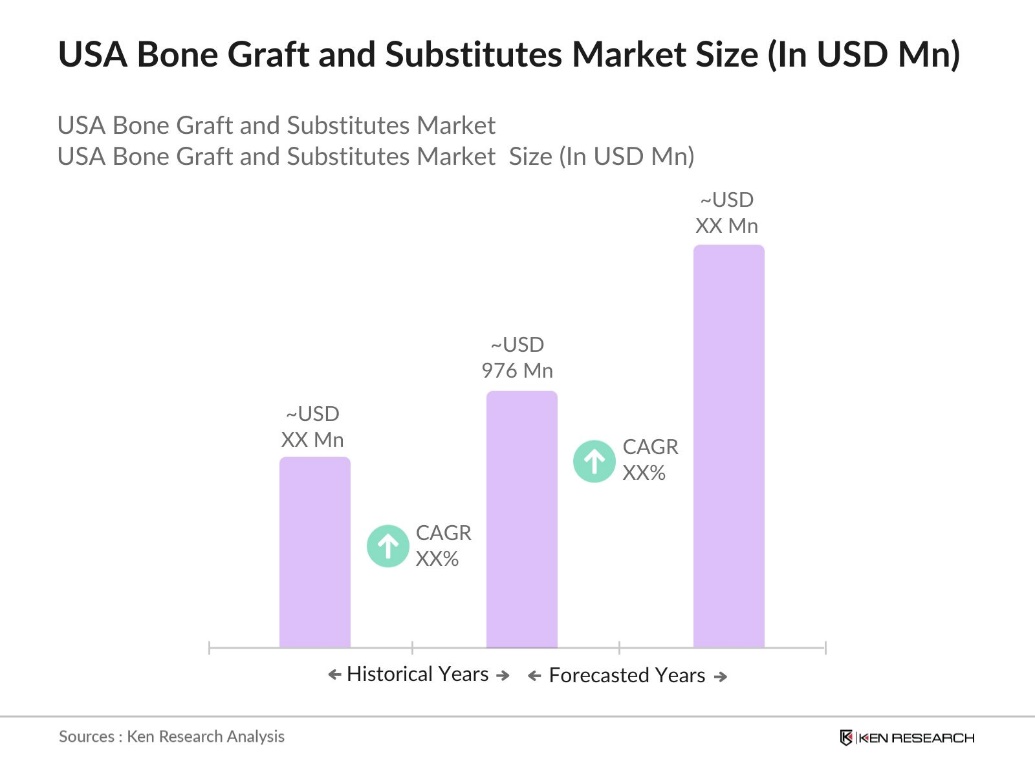

The USA bone graft and substitutes market is valued at USD 976 million, driven by technological advancements in synthetic grafts and the growing number of orthopedic surgeries.

Challenges in the USA bone graft and substitutes market include high costs of advanced graft materials, risk of post-surgical complications, and regulatory hurdles associated with FDA approvals and clinical trials.

Key players in USA bone graft and substitutes market include Medtronic, Stryker Corporation, Zimmer Biomet, NuVasive, and DePuy Synthes (J&J). These companies dominate due to their extensive product portfolios and strong presence in both the spinal and joint reconstruction sectors.

The USA bone graft and substitutes market is driven by increasing orthopedic and dental surgeries, the growing aging population, advancements in bioactive graft materials, and a shift towards minimally invasive surgical techniques.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.