USA Bottled Water Market Outlook to 2030

Region:North America

Author(s):Shubham

Product Code:KROD3743

October 2024

97

About the Report

USA Bottled Water Market Overview

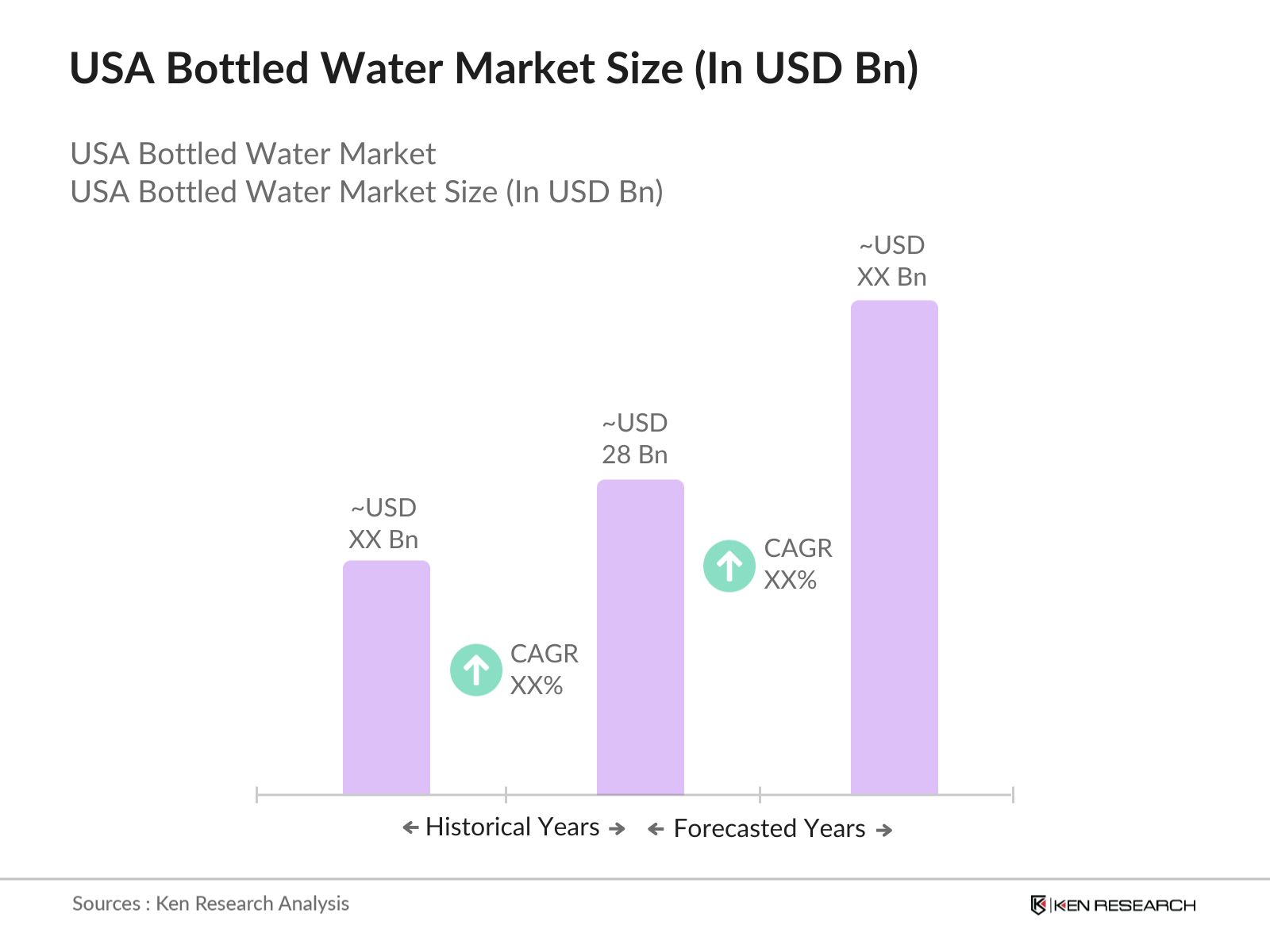

- Based on a five-year historical analysis, the USA Bottled Water market is valued at USD 28 billion, driven by increasing consumer demand for healthier beverage options, convenience, and the growing concerns around water contamination. The market has witnessed steady growth due to rising health consciousness, particularly among urban populations, and the increased consumption of bottled water as a substitute for sugary beverages.

- Major metropolitan areas such as New York, Los Angeles, and Chicago are key drivers of this market, benefiting from the high concentration of retail outlets, convenience stores, and a growing preference for premium and flavored bottled water. In rural areas, the demand for bottled water is bolstered by concerns over water quality and limited access to safe drinking water, further driving growth in these regions.

- The U.S. Food and Drug Administration (FDA) plays a crucial regulatory role in ensuring the safety and quality of bottled water. Recent efforts by the FDA to strengthen regulations on water safety, labeling, and environmental sustainability have influenced market dynamics, prompting bottled water companies to invest in cleaner production processes and sustainable packaging solutions.

USA Bottled Water Market Segmentation

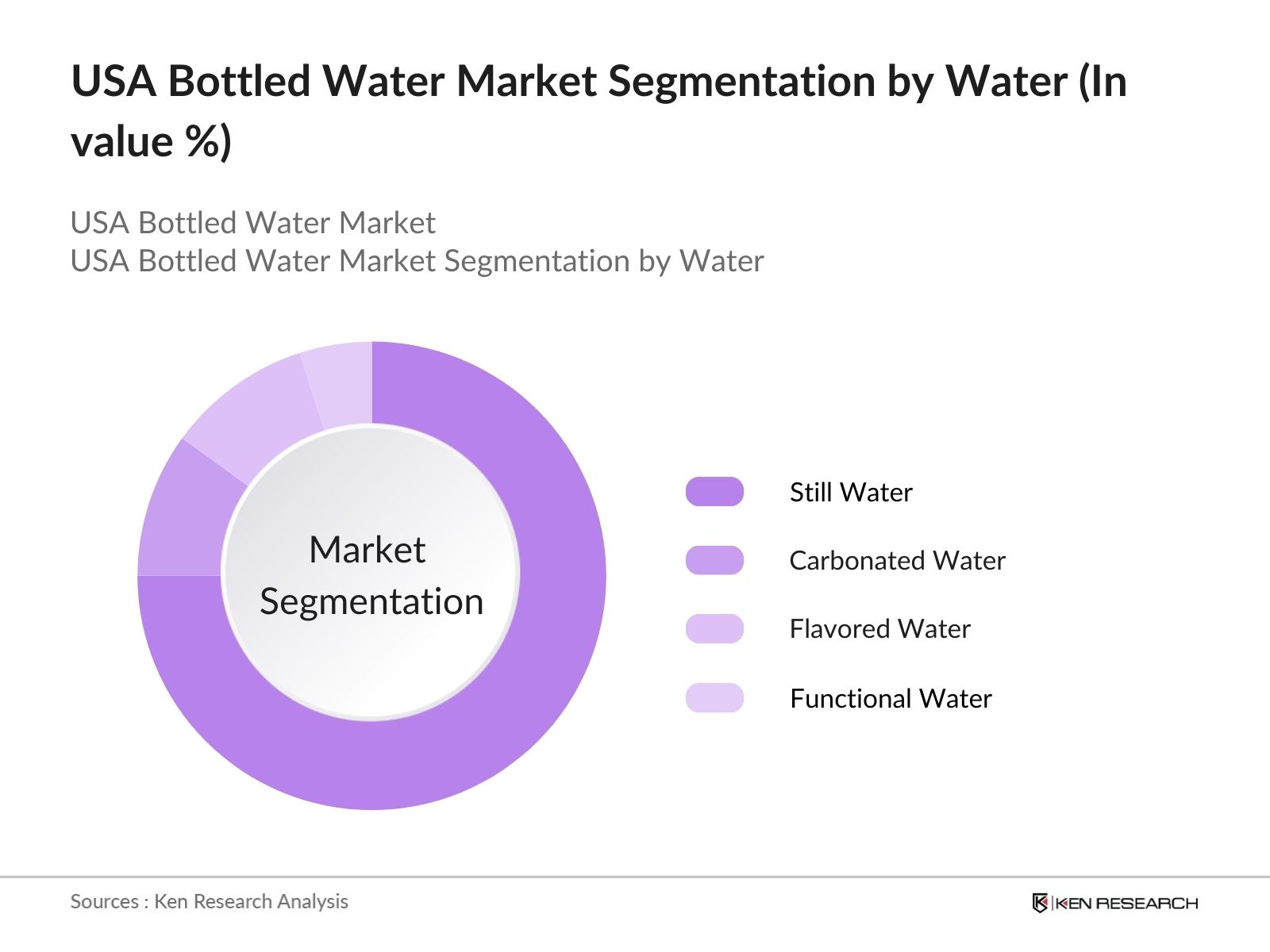

- By Type of Water: The market is segmented into still water, sparkling water, flavored water, and functional water. Still water dominates the market, driven by its widespread availability and affordability. However, sparkling water and flavored water are gaining market share due to their perceived health benefits and increasing demand among health-conscious consumers. Functional water, which includes added vitamins and minerals, is also seeing growth as consumers seek out enhanced hydration options.

- By Distribution Channel: The market is segmented by distribution channel into supermarkets & hypermarkets, convenience stores, online retail, and others. Supermarkets and hypermarkets hold the largest market share due to the convenience and variety they offer to consumers. Online retail is experiencing rapid growth, especially post-pandemic, as more consumers prefer the convenience of home delivery services for bulky water purchases.

USA Bottled Water Market Competitive Landscape

The USA Bottled Water market is highly competitive, with several key players continuously innovating and expanding their product offerings. Major players include Nestl Waters North America, The Coca-Cola Company (Dasani), PepsiCo (Aquafina), and Danone (Evian). These companies are investing in product differentiation, sustainable packaging, and expanding their distribution networks to maintain a competitive edge.

|

Company Name |

Establishment Year |

Headquarters |

No. of Employees |

Revenue (USD) |

Key Products |

Sustainability Initiatives |

Geographical Reach |

Technology Adoption |

Partnerships |

|

Nestl Waters North America |

1976 |

Stamford, CT |

|||||||

|

The Coca-Cola Company |

1892 |

Atlanta, GA |

|||||||

|

PepsiCo (Aquafina) |

1965 |

Purchase, NY |

|||||||

|

Danone (Evian) |

1919 |

Paris, France |

|||||||

|

Keurig Dr Pepper |

1919 |

Paris, France |

USA Bottled Water Industry Analysis

Growth Drivers

- Increasing Health Consciousness: The USA's growing health awareness trend has driven consumers to prefer bottled water over sugary beverages. As of 2023, the U.S. witnessed a rise in obesity and related diseases, with nearly 42% of adults classified as obese according to the CDC. The bottled water market benefits from this trend, as more consumers opt for healthier hydration choices. Additionally, the USDA notes that water intake has increased, with an average American consuming over 36 gallons of bottled water annually, driven by the perceived purity and health benefits of bottled water.

- Rising Demand for Convenient, On-the-Go Hydration: As of 2023, the U.S. Department of Transportation reported an increase in daily commuting distances, with Americans traveling an average of 42 miles per day. This increase in commuting time has contributed to the rising demand for convenient hydration solutions like bottled water. According to the Bureau of Labor Statistics data cited in one of the results, in 2021, over 44 billion bottles of water were consumed in the U.S., with about 13 gallons of bottled water consumed per person. The busy lifestyle of U.S. consumers continues to drive demand for bottled water as a convenient hydration source.

- Expanding Consumer Preference for Premium and Functional Water: The demand for premium and functional water products, such as electrolyte-infused or alkaline water, has surged in the U.S. Functional water consumption rose by 15% in the past three years, as per the USDA, reflecting an increasing consumer shift toward enhanced hydration products. Furthermore, premium bottled water brands targeting affluent consumers have also seen a spike in sales, supported by rising disposable incomes. The U.S. Census Bureau reported a median household income of USD 80,610 in 2023, boosting consumer willingness to spend on premium bottled water alternatives.

Market Challenges

- Regulatory Pressure on Plastic Use: The bottled water industry in the USA faces increasing regulatory scrutiny over plastic usage. The U.S. Food and Drug Administration (FDA) enforces strict guidelines on bottled water packaging to ensure safety and environmental compliance. The EPA also regulates the environmental impact of plastic, with new mandates requiring companies to reduce plastic bottle usage by 2025. These stringent regulations force bottled water manufacturers to innovate sustainable packaging solutions, potentially increasing operational costs as they transition to alternatives like rPET or biodegradable materials.

- Water Scarcity Issues: Water scarcity has become a critical challenge for the bottled water industry, especially in regions like California and Texas. According to the U.S. Geological Survey (USGS), several states faced groundwater depletion in 2023, with a reduction in water reserves substantially. Bottled water manufacturers face sourcing challenges, as increased regulation limits access to natural water sources. The strain on water resources and stricter water sourcing regulations imposed by state governments further complicate production and supply chain processes for bottled water companies.

USA Bottled Water Market Future Outlook

The USA Bottled Water market is expected to grow steadily over the next five years, driven by increasing consumer demand for healthier beverages, sustainable packaging solutions, and technological advancements in production. With a growing focus on environmental sustainability, bottled water companies will need to invest in eco-friendly practices and continue innovating to stay competitive in this dynamic market.

Future Market Opportunities

- Growth in Functional and Flavored Water Segments: The functional and flavored water segments have seen rapid growth, fueled by consumer interest in health benefits and variety. As of 2023, functional water sales increased remarkably, according to USDA figures, driven by a growing preference for enhanced hydration options. Flavored water products have gained popularity as alternatives to sugary drinks, attracting consumers looking for healthy, low-calorie options. The health-conscious trend, combined with the push for functional ingredients such as vitamins, minerals, and antioxidants, presents a significant opportunity for further market expansion in the coming years.

- Expansion of Online and Direct-to-Consumer Sales Channels

E-commerce has emerged as a vital sales channel for the bottled water industry in the U.S. According to data from the U.S. Census Bureau, online sales for consumer goods grew by over 12% in 2023. Direct-to-consumer (D2C) models are gaining traction, offering consumers the convenience of home delivery subscriptions. This shift to online channels provides bottled water companies with an opportunity to target tech-savvy consumers and expand their market reach. The trend is particularly pronounced among younger demographics, who prioritize convenience and customization in their purchases.

Scope of the Report

|

By Type of Water |

Still Water Sparkling Water Flavored Water Functional Water |

|

By Distribution Channel |

Supermarkets and Hypermarkets Convenience Stores Online Retail Others (Vending machines, direct-to-consumer) |

|

By Packaging |

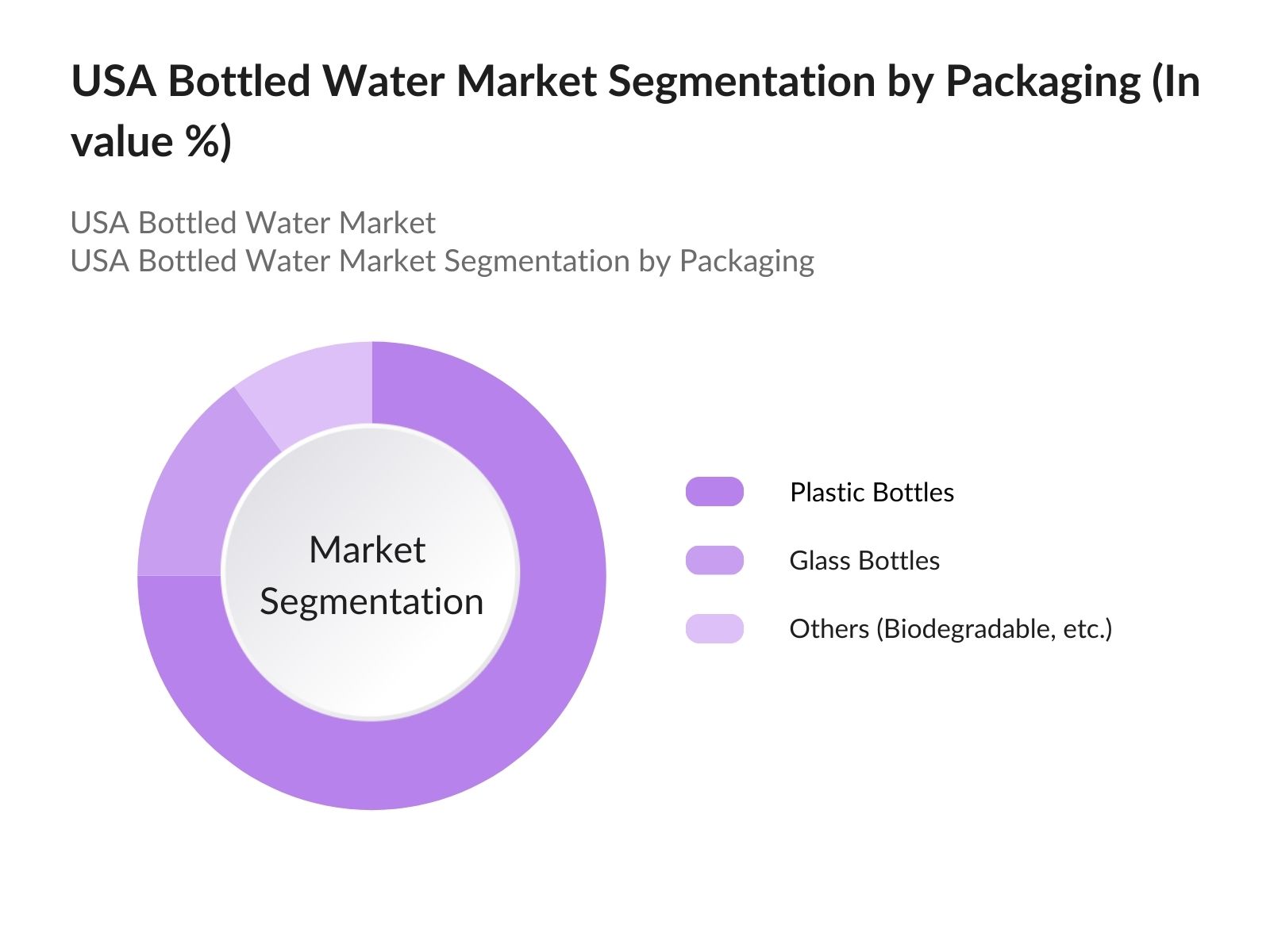

Plastic Bottles Glass Bottles Others (Biodegradable, Aluminum cans) |

|

By Size of Bottles |

Small Bottles (Up to 1 liter) Medium Bottles (12.5 liters) Large Bottles (More than 2.5 liters) |

|

By Region |

Northeast Midwest South West |

Products

Key Target Audience

Bottled Water Manufacturers

Bottled Water Packaging Companies

Retail Chains (Supermarkets, Hypermarkets, Convenience Stores)

Online Retailers

Government and Regulatory Bodies (FDA, EPA)

Venture Capital Firms and Private Equity Investors

Hospitality and Foodservice Industry (Hotels, Restaurants, Gyms)

Beverage Distributors and Wholesalers

Banks and Financial Institutions

Companies

Major Players in the USA Bottled Water Market

-

Nestl Waters North America

The Coca-Cola Company (Dasani)

PepsiCo (Aquafina)

Danone (Evian)

Keurig Dr Pepper (Bai Brands)

Fiji Water

Niagara Bottling

VOSS Water

Boxed Water Is Better

Essentia Water

Perfect Hydration (pH)

Life WTR

JUST Water

Icelandic Glacial

Flow Water

Table of Contents

1. USA Bottled Water Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate (CAGR, USD)

1.4 Market Segmentation Overview

2. USA Bottled Water Market Size (In USD Billion)

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. USA Bottled Water Market Analysis

3.1 Growth Drivers

3.1.1 Increasing Health Consciousness

3.1.2 Rising Demand for Convenient, On-the-Go Hydration

3.1.3 Expanding Consumer Preference for Premium and Functional Water

3.1.4 Environmental Concerns and Sustainability Initiatives (Plastic reduction, 100% rPET bottles)

3.2 Market Challenges

3.2.1 Regulatory Pressure on Plastic Use (FDA & EPA regulations)

3.2.2 Water Scarcity Issues (Sourcing challenges)

3.2.3 Market Fragmentation and Competition from Local Brands

3.3 Opportunities

3.3.1 Growth in Functional and Flavored Water Segments

3.3.2 Expansion of Online and Direct-to-Consumer Sales Channels

3.3.3 Sustainable Packaging and Circular Economy Initiatives

3.4 Trends

3.4.1 Demand for Sustainable Packaging (Glass, biodegradable bottles)

3.4.2 Technological Advancements in Smart Water Bottles

3.4.3 Increasing Focus on Water Quality and Filtration Technologies

3.5 Government Regulations

3.5.1 FDA Regulations on Bottled Water Standards (Purity and safety standards)

3.5.2 Environmental Impact Regulations (Plastic waste reduction initiatives)

3.5.3 National and State-Level Water Sourcing Regulations

3.6 SWOT Analysis

3.6.1 Strengths (Strong consumer demand, health trends)

3.6.2 Weaknesses (Environmental impact, reliance on plastic)

3.6.3 Opportunities (Sustainable innovation, new segments)

3.6.4 Threats (Regulatory restrictions, water scarcity)

3.7 Stakeholder Ecosystem (Bottled Water Companies, Suppliers, Retailers, Environmental Agencies)

3.8 Porters Five Forces

3.8.1 Bargaining Power of Suppliers

3.8.2 Bargaining Power of Buyers

3.8.3 Threat of New Entrants

3.8.4 Threat of Substitutes

3.8.5 Industry Rivalry

3.9 Competition Ecosystem

3.9.1 Market Consolidation and Key Players

3.9.2 Strategic Alliances and Joint Ventures

4. USA Bottled Water Market Segmentation

4.1 By Type of Water (In Value %)

4.1.1 Still Water

4.1.2 Sparkling Water

4.1.3 Flavored Water

4.1.4 Functional Water

4.2 By Distribution Channel (In Value %)

4.2.1 Supermarkets and Hypermarkets

4.2.2 Convenience Stores

4.2.3 Online Retail

4.2.4 Others (Vending machines, direct-to-consumer)

4.3 By Packaging Type (In Value %)

4.3.1 Plastic Bottles

4.3.2 Glass Bottles

4.3.3 Others (Biodegradable, Aluminum cans)

4.4 By Size of Bottles (In Value %)

4.4.1 Small Bottles (Up to 1 liter)

4.4.2 Medium Bottles (12.5 liters)

4.4.3 Large Bottles (More than 2.5 liters)

4.5 By End-User (In Value %)

4.5.1 Households

4.5.2 Institutional (Schools, Hospitals)

4.5.3 Commercial (Restaurants, Hotels, Gyms)

5. USA Bottled Water Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Nestl Waters North America

5.1.2 The Coca-Cola Company (Dasani)

5.1.3 PepsiCo (Aquafina)

5.1.4 Danone (Evian)

5.1.5 Keurig Dr Pepper (Bai Brands)

5.1.6 Niagara Bottling

5.1.7 VOSS Water

5.1.8 Fiji Water

5.1.9 Boxed Water Is Better

5.1.10 Essentia Water

5.1.11 Perfect Hydration (pH)

5.1.12 Life WTR

5.1.13 JUST Water

5.1.14 Icelandic Glacial

5.1.15 Flow Water

5.2 Cross Comparison Parameters (Revenue, Bottling Capacity, Market Share, Product Portfolio, Sustainability Initiatives, Technology Adoption, Geographical Reach, No. of Employees)

5.3 Market Share Analysis

5.4 Strategic Initiatives (New Product Launches, Brand Positioning)

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. USA Bottled Water Market Regulatory Framework

6.1 Environmental Standards (EPA, local regulations on plastic usage)

6.2 Compliance Requirements (FDA certifications, labeling standards)

6.3 Certification Processes (Water quality certifications, sustainable packaging certifications)

7. USA Bottled Water Future Market Size (In USD Billion)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth (Consumer preferences, environmental concerns)

8. USA Bottled Water Future Market Segmentation

8.1 By Type of Water (Still, Sparkling, Flavored, Functional)

8.2 By Distribution Channel (Supermarkets, Convenience Stores, Online Retail, Others)

8.3 By Packaging Type (Plastic, Glass, Others)

8.4 By Size of Bottles (Small, Medium, Large)

8.5 By End-User (Households, Institutional, Commercial)

9. USA Bottled Water Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives (Sustainability-focused branding, health-conscious consumer targeting)

9.4 White Space Opportunity Analysis (New geographical markets, innovative packaging)

Research Methodology

Step 1: Identification of Key Variables

The first step involved creating a comprehensive ecosystem map that includes all major stakeholders in the USA Bottled Water Market. This was done using extensive desk research with the help of secondary and proprietary databases, aiming to identify the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

This step focused on analyzing historical data pertaining to the USA Bottled Water Market, including market penetration, product preferences, and sales channels. Additionally, the analysis covered the revenue generation patterns and the impact of product innovations on market trends.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were developed and validated through consultations with industry experts, including interviews and discussions with senior executives from leading bottled water companies. This ensured the market insights and data were accurate and reflected real-world dynamics.

Step 4: Research Synthesis and Final Output

The final stage involved consolidating data from various sources, including industry reports and interviews with market players. The insights gathered were synthesized into a comprehensive and validated analysis, covering all major aspects of the USA Bottled Water market.

Frequently Asked Questions

01. How big is the USA Bottled Water Market?

The USA Bottled Water Market is valued at USD 28 billion, driven by increasing health awareness, convenience, and environmental concerns among consumers.

02. What are the challenges in the USA Bottled Water Market?

Challenges in the USA Bottled Water Market include environmental concerns regarding plastic waste, regulatory pressures, and increasing competition from local brands offering eco-friendly packaging alternatives.

03. Who are the major players in the USA Bottled Water Market?

Major players in the USA Bottled Water Market include Nestl Waters North America, The Coca-Cola Company (Dasani), PepsiCo (Aquafina), Danone (Evian), and Keurig Dr Pepper.

04. What are the growth drivers of the USA Bottled Water Market?

Growth drivers in the USA Bottled Water Market include increasing health consciousness, rising demand for premium and functional water products, and advancements in sustainable packaging solutions.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.