USA Car Subscription Market Outlook to 2030

Region:North America

Author(s):Samanyu

Product Code:KROD4623

November 2024

93

About the Report

USA Car Subscription Market Overview

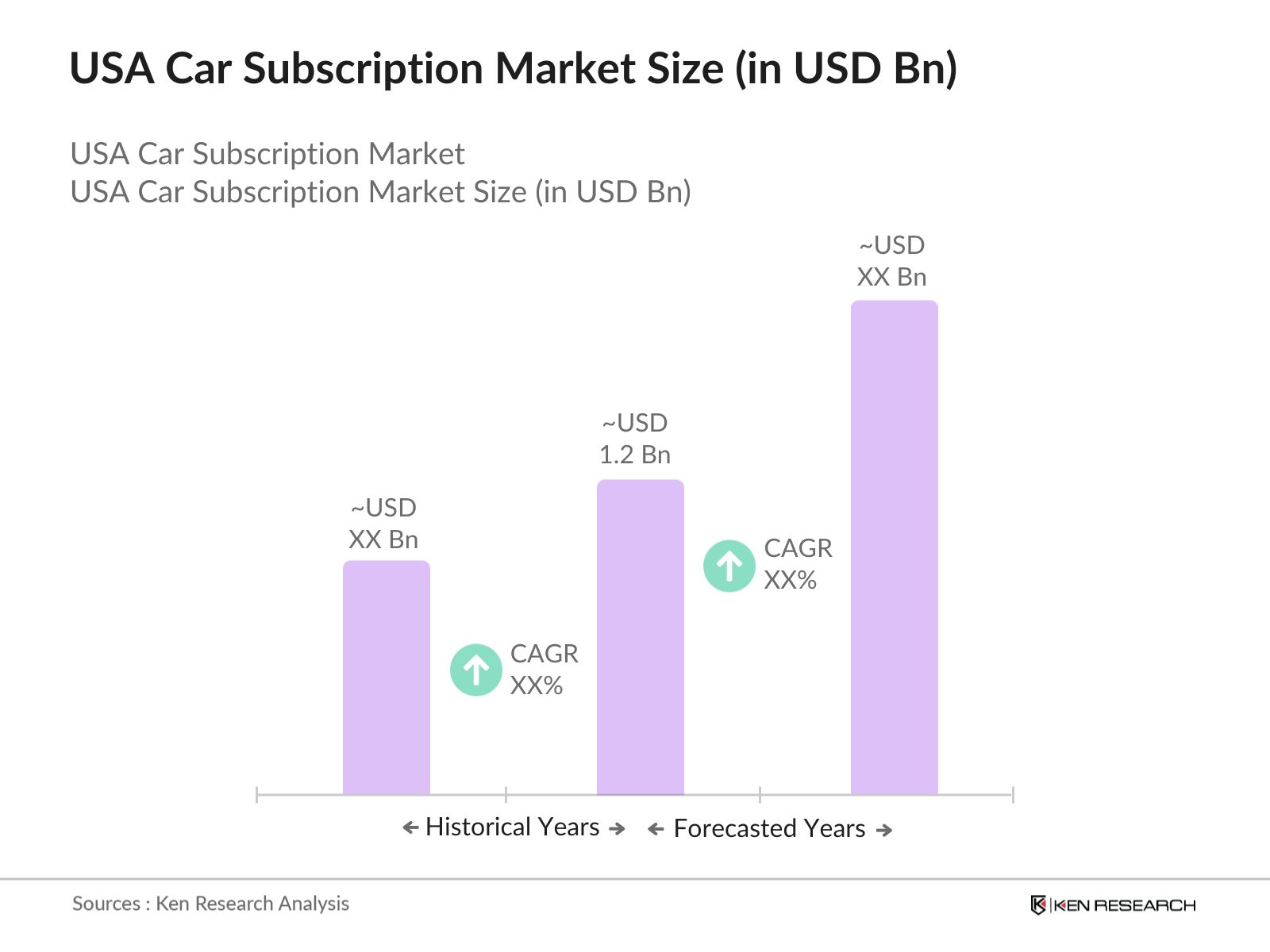

- The USA Car Subscription market is valued at USD 1.2 Bn, based on a five-year historical analysis. This market has been growing steadily over the past five years. This growth is primarily driven by the increasing consumer preference for flexible mobility solutions, the declining interest in traditional car ownership, and the rise of digital platforms that make car subscriptions easier to access. In 2024, the market is expected to maintain its upward trajectory, supported by further innovations in mobility solutions and integration with technology-driven subscription platforms.

- Cities like New York, Los Angeles, and San Francisco dominate the USA car subscription market due to high urbanization, technological infrastructure, and a shift towards flexible, pay-as-you-go models of vehicle access. These cities have seen rapid adoption of car subscription services, especially among younger consumers and businesses looking for more sustainable and cost-effective transportation solutions. The availability of electric vehicles (EVs) under subscription models is also driving growth in these regions.

- Mobile platform integration is becoming a standard feature for car subscription services, allowing users to manage their subscriptions through apps. With 94.7% of Americans using smartphones in 2024 (World Bank), companies are focusing on developing user-friendly mobile apps that offer seamless access to subscription features. These platforms enable users to track their vehicles, make payments, and switch between cars with ease. The rise of digital wallets, with over 180 million users in the U.S. (Statista), further simplifies payment processes and enhances the overall user experience.

USA Car Subscription Market Segmentation

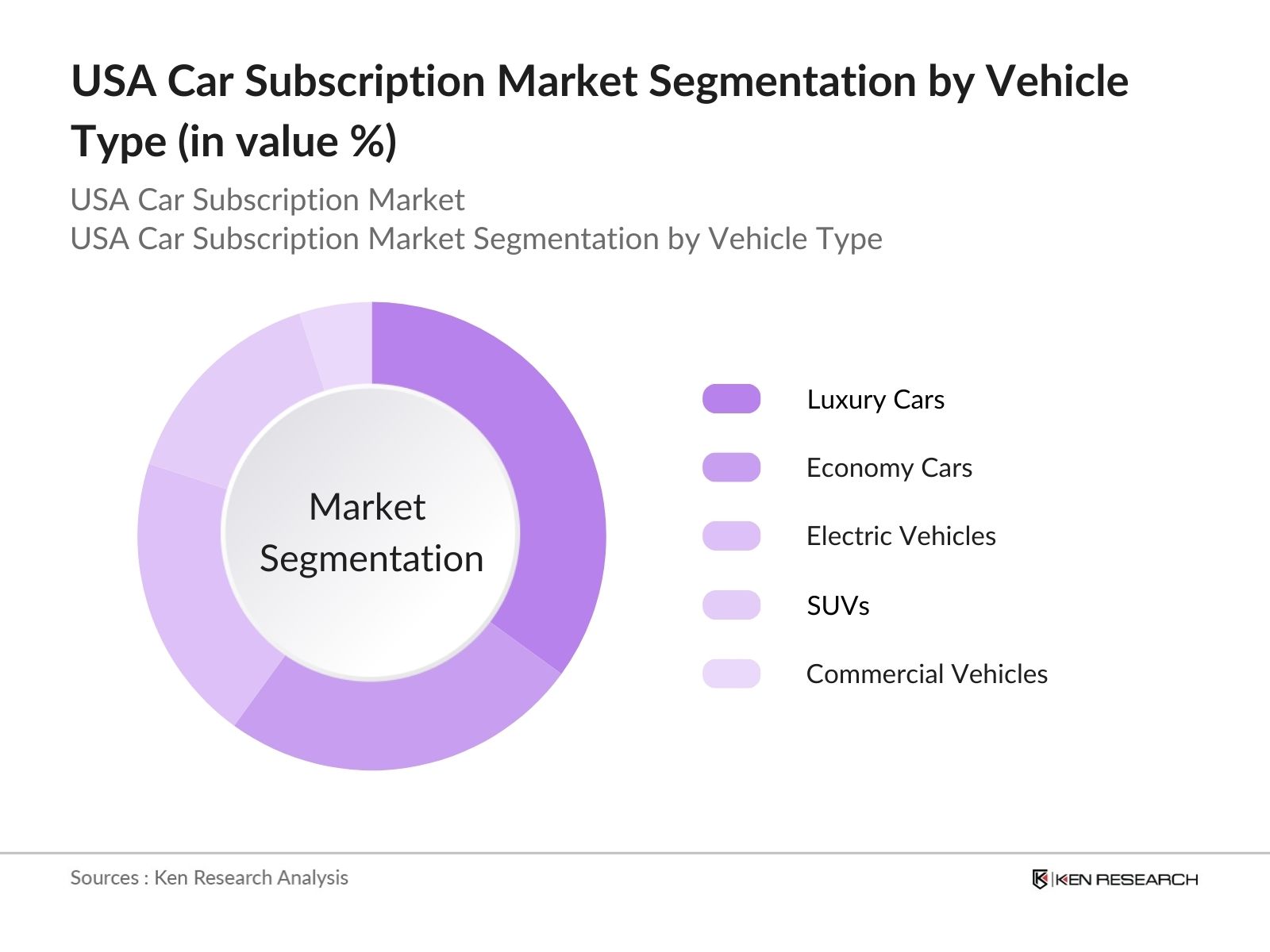

By Vehicle Type: The market is segmented by vehicle type into luxury cars, economy cars, electric vehicles (EVs), SUVs, and commercial vehicles. Luxury cars have recently captured a dominant market share, largely due to the rising demand for high-end, flexible ownership models among affluent consumers. Brands such as Porsche and BMW offer premium subscription plans that allow users to switch between various luxury models, catering to those who prefer access over ownership.

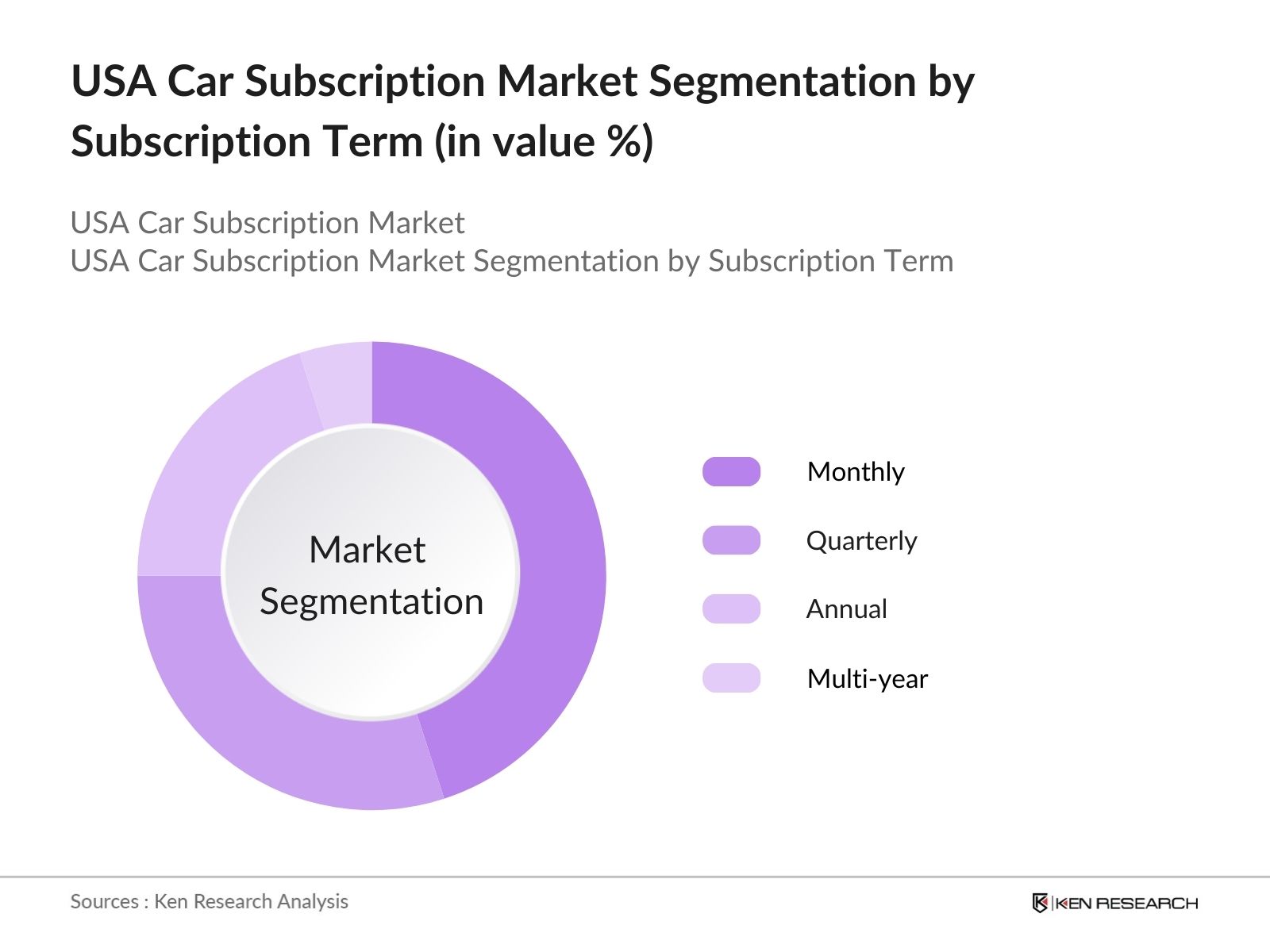

By Subscription Term: The market is also segmented by subscription term into monthly, quarterly, annual, and multi-year plans. Monthly subscriptions are currently the dominant segment, as they offer the highest degree of flexibility. Many users, particularly in urban areas, prefer short-term options that allow them to switch vehicles frequently or even pause subscriptions as needed. This is especially appealing to younger demographics and those in temporary work situations, where flexibility in transportation is crucial.

USA Car Subscription Market Competitive Landscape

The USA car subscription market is dominated by several key players, including established car rental companies, OEMs (Original Equipment Manufacturers), and new subscription-based service providers. These companies have established significant influence through strategic partnerships, advanced technological platforms, and the expansion of their service offerings.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (2023) |

Employees |

Fleet Size |

EV Subscription |

Key Clients |

Service Network |

|

Hertz |

1918 |

Estero, FL |

||||||

|

Avis |

1946 |

Parsippany, NJ |

||||||

|

Sixt |

1912 |

Pullach, Germany |

||||||

|

Fair |

2016 |

Santa Monica, CA |

||||||

|

Care by Volvo |

2017 |

Gothenburg, Sweden |

USA Car Subscription Industry Analysis

Growth Drivers

- Shift towards flexible mobility solutions: In 2024, consumer demand for flexible mobility solutions has surged, fueled by rapid urbanization and increased traffic congestion. The U.S. urban population reached over 270 million in 2023, leading to demand for more versatile transportation options. Car subscriptions offer flexibility, avoiding the long-term commitment of car ownership while meeting the needs of city dwellers who travel less frequently. The U.S. Bureau of Transportation Statistics reports that the average household vehicle ownership dropped from 2.28 cars per household in 2010 to 1.9 cars in 2024, showing an inclination towards shared, flexible mobility.

- Increasing preference for on-demand services: The proliferation of on-demand services reflects a broader trend in the service economy, with consumers increasingly valuing convenience and immediacy. The U.S. tech industry has experienced a significant rise, with internet penetration standing at 94.7% in 2024, enabling seamless digital interactions. This tech-savvy population is more likely to opt for car subscription services that integrate with on-demand platforms. With over 185 million smartphone users in the U.S. in 2024, the subscription model aligns with preferences for app-based mobility solutions.

- Rise of electric vehicles (EVs): Electric vehicles are becoming a focal point of car subscription services due to growing interest in sustainable mobility. In 2024, EV registrations reached 2.3 million units in the U.S., according to the U.S. Department of Energy, bolstered by strong government incentives. The Biden administrations continued push for carbon neutrality by 2050 supports the growth of EV subscriptions, with tax rebates up to USD 7,500 for EV buyers. Subscription services offering EVs are aligning with this trend, providing environmentally conscious consumers access to EVs without the financial burden of ownership.

Market Challenges

- Regulatory challenges: The car subscription market in the U.S. faces complex regulatory challenges due to state-specific laws governing vehicle leasing, taxation, and insurance. For instance, states like California and New York have stringent consumer protection laws, while others like Florida are more relaxed. In 2024, there are no unified federal regulations on car subscriptions, making it difficult for companies to scale across states. The U.S. Department of Transportation highlights that discrepancies in taxation and vehicle registration laws across states are causing delays in subscription services' growth, as companies have to tailor services to different state laws.

- Limited market awareness: Despite growing interest in flexible mobility solutions, a large portion of the U.S. population remains unaware of car subscription services. According to a 2024 report by the U.S. Department of Transportation, approximately 48% of Americans are still unfamiliar with car subscription models. This lack of awareness is compounded by the fact that traditional leasing and ownership models dominate, with nearly 90 million vehicles owned outright in the U.S. (Bureau of Transportation Statistics). Without widespread consumer education and marketing, subscription services struggle to gain traction, especially among older generations.

USA Car Subscription Market Future Outlook

Over the next five years, the USA car subscription market is expected to see significant growth driven by the increasing popularity of electric vehicles, ongoing advancements in mobility technologies, and growing consumer demand for flexible transportation solutions. The push towards sustainable mobility, especially in urban areas, will also encourage a greater shift towards car subscriptions, particularly those offering electric and hybrid vehicles.

Subscription services that offer flexibility in vehicle selection, subscription length, and additional services like insurance and maintenance are likely to be the most successful. The integration of AI and IoT for vehicle tracking, personalization, and better service delivery will also be key drivers of market growth.

Future Market Opportunities

- Expansion of electric vehicle subscriptions: With the growing emphasis on green mobility, there is significant potential for expansion in EV subscription services. In 2024, the U.S. government continues to incentivize EV adoption, including subsidies, rebates, and tax breaks for both consumers and companies. According to the U.S. Department of Energy, over 300,000 public EV charging stations are expected to be operational by 2024, up from 118,000 in 2020. This infrastructure growth, combined with increased government support, positions EV subscription services to capitalize on the green mobility wave and cater to environmentally conscious consumers.

- Subscription as a service for corporate fleets: Corporate fleet management represents a lucrative opportunity for car subscription services. In 2024, the U.S. corporate vehicle fleet market stands at over 13 million vehicles (Bureau of Transportation Statistics), with growing interest in flexible, subscription-based fleet management. Large corporations are seeking alternatives to traditional fleet leasing, driven by the need to reduce upfront costs and optimize fleet usage. Subscription models, which bundle maintenance, insurance, and vehicle management, offer businesses a more efficient way to manage their fleets, with lower financial risk and greater flexibility.

Scope of the Report

|

By Vehicle Type |

Luxury Cars Economy Cars Electric Vehicles SUVs and Crossovers Commercial Vehicles |

|

By Customer Type |

Individual Corporate Small Businesses Freelancers/Contractors |

|

By Subscription Term |

Monthly Quarterly Annual Multi-year |

|

By End-User |

Ride-sharing and Rental Platforms Corporate Fleets Personal Use Real Estate Hospitality Services |

|

By Region |

Northeast Midwest South West Coast Rural/Non-urban Regions |

Products

Key Target Audience

Automotive OEMs

Car rental and leasing companies

Subscription-based service providers

Technology solution providers (Telematics, IoT platforms)

Corporate fleet management firms

Investors and venture capitalist firms

Government and regulatory bodies (Department of Transportation, Environmental Protection Agency)

Electric vehicle manufacturers

Companies

Major Players

Hertz

Avis

Sixt

Fair

Flexdrive

Care by Volvo

Clutch Technologies

Porsche Passport

BMW Access

Mercedes-Benz Collection

Borrow

Hyundais Mocean

CarmaCar

Autonomy

Enterprise CarShare

Table of Contents

1. USA Car Subscription Market Overview

1.1. Definition and Scope (Types of car subscription models, ownership vs subscription, rental vs lease)

1.2. Market Taxonomy (Car segment: luxury, economy, electric; Subscription terms: monthly, annual)

1.3. Market Growth Rate (CAGR for USA car subscription services, Market growth in urban regions)

1.4. Market Segmentation Overview (Vehicle type, Customer type, Service providers, End-user industry)

2. USA Car Subscription Market Size (In USD Bn)

2.1. Historical Market Size (Prevalence and growth of car subscription services in key regions)

2.2. Year-On-Year Growth Analysis (Tracking growth patterns in car subscriptions across different user demographics)

2.3. Key Market Developments and Milestones (Notable mergers, partnerships, and expansions by subscription service providers)

3. USA Car Subscription Market Analysis

3.1. Growth Drivers

3.1.1. Shift towards flexible mobility solutions

3.1.2. Increasing preference for on-demand services (consumer preferences, tech penetration)

3.1.3. Rise of electric vehicles (Impact on subscription models for EVs)

3.1.4. Decline in traditional car ownership (Millennials and Gen Z behavioral shifts)

3.2. Restraints

3.2.1. High monthly costs (Cost comparison with leasing and ownership)

3.2.2. Regulatory challenges (Legal frameworks for car subscriptions across states)

3.2.3. Limited market awareness (Lack of consumer understanding of subscription models)

3.3. Opportunities

3.3.1. Technological advancements (AI and IoT integration in subscription management)

3.3.2. Expansion of electric vehicle subscriptions (Growth potential in green mobility)

3.3.3. Subscription as a service for corporate fleets (B2B market)

3.3.4. Cross-industry partnerships (Opportunities with ride-hailing and insurance companies)

3.4. Trends

3.4.1. Increased demand for flexible, pay-as-you-go solutions (Short-term contracts)

3.4.2. Integration of mobile platforms (Apps for managing subscriptions)

3.4.3. EV dominance in subscription models (Impact of electric vehicles on the future of car subscriptions)

3.4.4. Subscription personalization (Data-driven approaches to customize services)

3.5. Regulatory Framework

3.5.1. State-specific regulations (Impact of varying state laws on subscription services)

3.5.2. Insurance and liability concerns (Coverage models, subscription packages)

3.5.3. Emission and environmental policies (Government incentives for EV subscriptions)

3.5.4. Tax implications (Taxation on subscription services vs. ownership)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Service providers, automotive manufacturers, software solution providers)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem (New entrants, market fragmentation)

4. USA Car Subscription Market Segmentation

4.1. By Vehicle Type (In Value %)

4.1.1. Luxury Cars

4.1.2. Economy Cars

4.1.3. Electric Vehicles

4.1.4. SUVs and Crossovers

4.1.5. Commercial Vehicles

4.2. By Customer Type (In Value %)

4.2.1. Individual

4.2.2. Corporate

4.2.3. Small Businesses

4.2.4. Freelancers/Contractors

4.3. By Subscription Term (In Value %)

4.3.1. Monthly

4.3.2. Quarterly

4.3.3. Annual

4.3.4. Multi-year

4.4. By End-User Industry (In Value %)

4.4.1. Ride-sharing and Rental Platforms

4.4.2. Corporate Fleets

4.4.3. Personal Use

4.4.4. Real Estate and Hospitality Services (Concierge services)

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West Coast

4.5.5. Rural/Non-urban Regions

5. USA Car Subscription Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Hertz

5.1.2. Avis

5.1.3. Sixt

5.1.4. Enterprise CarShare

5.1.5. Fair

5.1.6. Flexdrive

5.1.7. Clutch Technologies

5.1.8. Care by Volvo

5.1.9. CarmaCar

5.1.10. Porsche Passport

5.1.11. BMW Access

5.1.12. Mercedes-Benz Collection

5.1.13. Borrow

5.1.14. Hyundais Mocean

5.1.15. Autonomy

5.2. Cross Comparison Parameters (Subscription Plan Features, Geographic Coverage, Pricing Strategy, Fleet Size, No. of Dealerships, Service Levels, Technology Integration)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Business Expansion, Product Launches)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. USA Car Subscription Market Regulatory Framework

6.1. State and Federal Regulations (Impact on subscription models)

6.2. Compliance Requirements (Licensing, service regulations)

6.3. Certification Processes (Service providers' certification for quality and safety)

7. USA Car Subscription Future Market Size (In USD Bn)

7.1. Future Market Size Projections (Long-term projections of market growth)

7.2. Key Factors Driving Future Market Growth (Technological, demographic, and environmental drivers)

8. USA Car Subscription Future Market Segmentation

8.1. By Vehicle Type (In Value %)

8.2. By Customer Type (In Value %)

8.3. By Subscription Term (In Value %)

8.4. By End-User Industry (In Value %)

8.5. By Region (In Value %)

9. USA Car Subscription Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis (Segmentation by demographics and subscription preferences)

9.3. Marketing Initiatives (Key marketing strategies for service providers)

9.4. White Space Opportunity Analysis (Potential areas of growth within the market)

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map that includes all major stakeholders within the USA car subscription market. Extensive desk research was conducted to gather data from proprietary databases, as well as publicly available industry reports, to identify key market drivers and variables influencing market growth.

Step 2: Market Analysis and Construction

In this phase, historical data pertaining to the USA car subscription market was compiled and analyzed. Key metrics such as market penetration, vehicle utilization rates, and subscription-based revenue generation were evaluated. Market forecasts were constructed based on this analysis, focusing on the future growth trajectory of the market.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses regarding market growth, pricing models, and consumer preferences were validated through interviews with industry experts, car subscription service providers, and technology solution vendors. These insights were used to refine the market models and forecast future trends.

Step 4: Research Synthesis and Final Output

The final phase involved synthesizing the research data, validating the market forecasts, and refining the reports conclusions. This included direct engagement with car subscription companies to ensure the accuracy of data regarding vehicle types, subscription durations, and consumer demographics.

Frequently Asked Questions

01. How big is the USA Car Subscription Market?

The USA car subscription market, valued at USD 1.2 billion in 2023, has been growing steadily due to the increasing demand for flexible transportation solutions and the rise of electric vehicles under subscription models.

02. What are the challenges in the USA Car Subscription Market?

Challenges in USA car subscription market include high costs of subscriptions compared to leasing, limited consumer awareness, and state-specific regulatory hurdles that affect service offerings across different regions.

03. Who are the major players in the USA Car Subscription Market?

Key players in USA car subscription market include Hertz, Avis, Sixt, Fair, and Care by Volvo. These companies dominate the market due to their extensive service networks, large vehicle fleets, and partnerships with OEMs.

04. What are the growth drivers of the USA Car Subscription Market?

The growth of USA car subscription market is driven by consumer preference for flexible ownership models, the rise of electric vehicles, and technological advancements in mobility platforms and vehicle management systems.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.