USA Cardiovascular Ultrasound Market Outlook to 2030

Region:North America

Author(s):Vijay Kumar

Product Code:KROD9816

November 2024

81

About the Report

USA Cardiovascular Ultrasound Market Overview

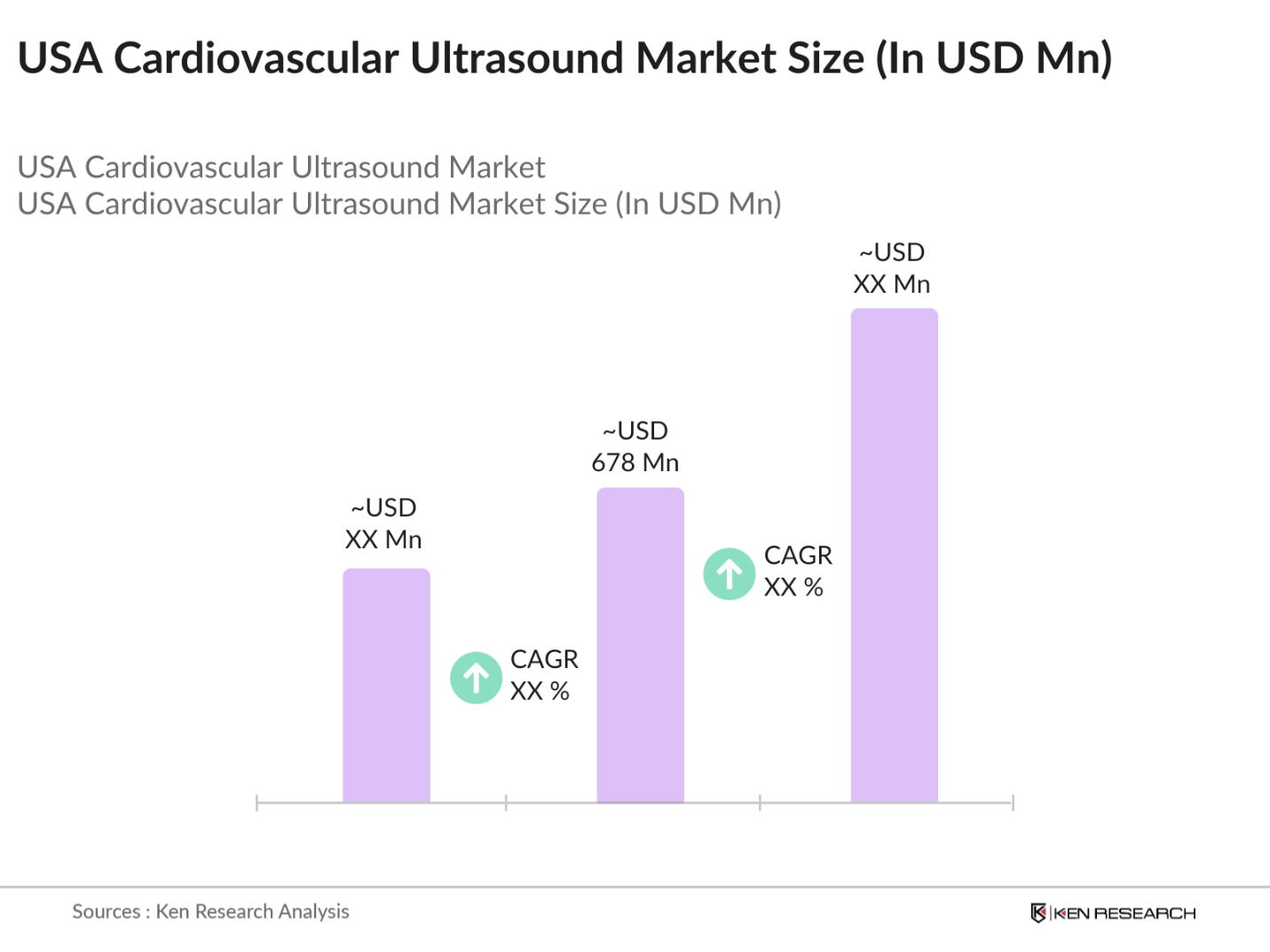

- The USA cardiovascular ultrasound market is valued at USD 678 million, based on a five-year historical analysis. This market is primarily driven by the increasing prevalence of cardiovascular diseases, which necessitates effective and non-invasive diagnostic tools. Technological advancements, particularly in 3D and portable ultrasound devices, enhance diagnostic accuracy and patient experience. Additionally, the focus on preventive healthcare and early diagnosis significantly fuels demand for cardiovascular ultrasound systems, making them vital in contemporary medical practice.

- Key cities like New York, Los Angeles, and Chicago lead the market due to their high concentration of advanced healthcare facilities and specialized cardiovascular centers. These regions also benefit from substantial investment in healthcare infrastructure and advanced imaging technologies, making them central hubs for cardiovascular diagnostics. The dominance of these areas is further supported by a strong presence of prominent healthcare companies and research institutions focusing on cardiovascular health.

- The FDA has streamlined approval processes for cardiovascular imaging devices, enabling quicker market access. Revised guidelines simplify compliance for new entrants in the imaging market, supporting a more competitive landscape. This regulatory support is intended to foster innovation, allowing healthcare providers faster access to advanced diagnostic tools.

USA Cardiovascular Ultrasound Market Segmentation

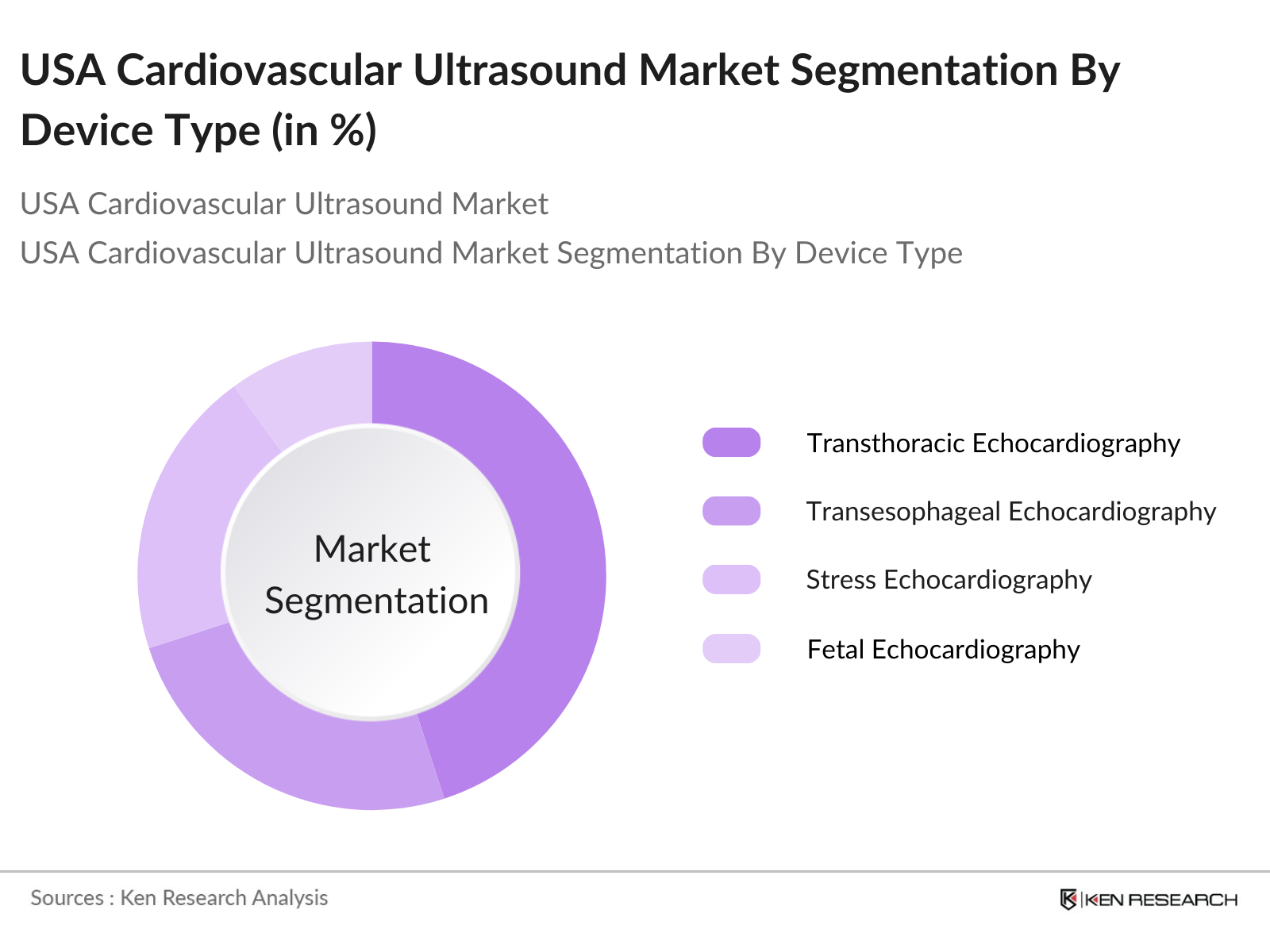

By Device Type: The market is segmented by device type into transthoracic echocardiography, transesophageal echocardiography, stress echocardiography, and fetal echocardiography. Recently, transthoracic echocardiography has maintained a dominant market share under device type segmentation, largely due to its non-invasive nature and high accuracy in diagnosing heart-related issues. This segment is widely used across hospitals and outpatient diagnostic centers, benefiting from a strong adoption rate due to its relatively lower cost and ease of use, which enhances patient throughput in busy healthcare environments.

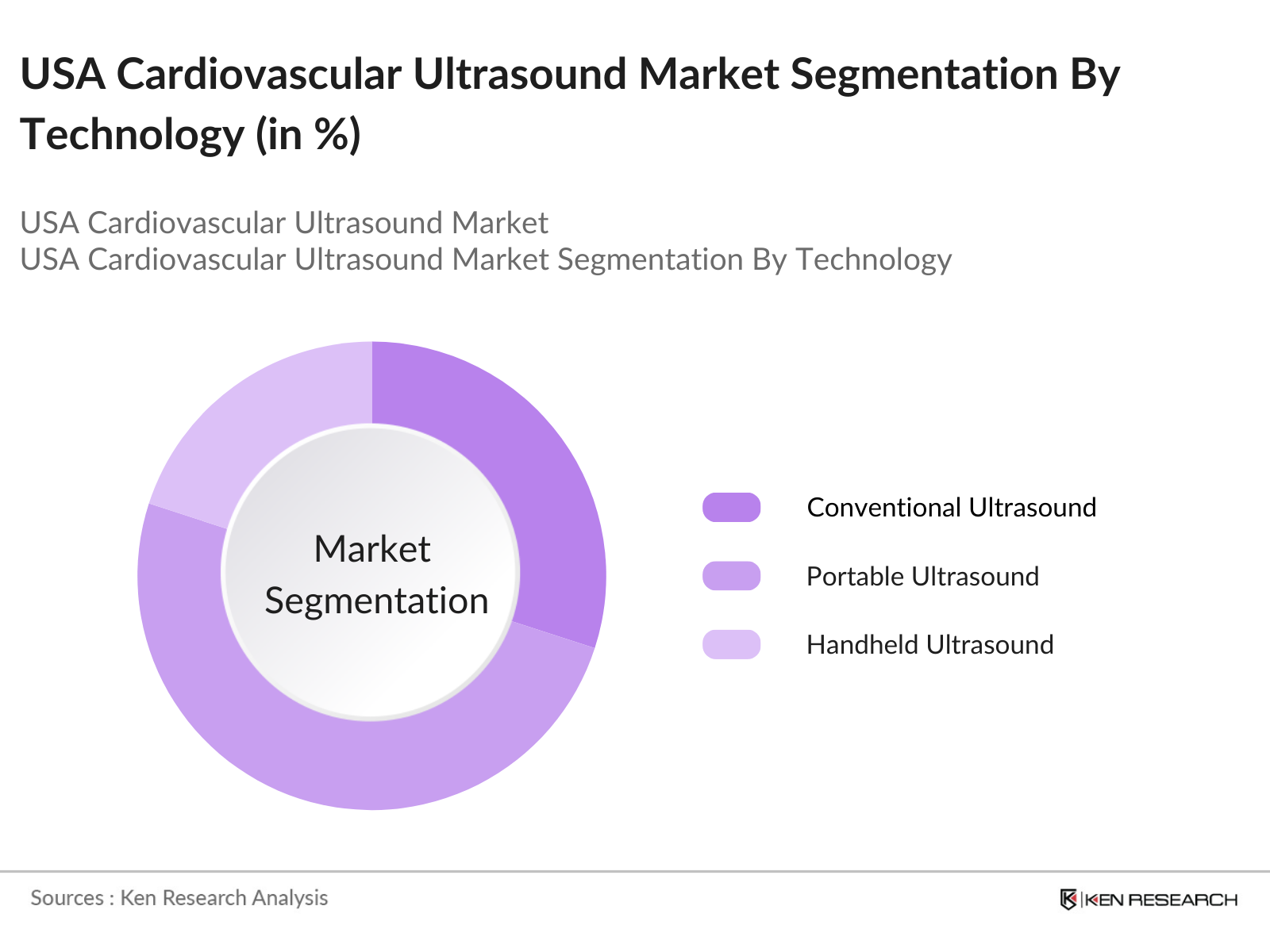

By Technology: The market is segmented by technology into conventional ultrasound, portable ultrasound, and handheld ultrasound. Portable ultrasound systems hold the dominant share in the technology segment, driven by the demand for flexibility in diagnostic procedures, particularly in emergency settings and outpatient care. These devices are increasingly preferred due to advancements in portability and image quality, making them ideal for point-of-care diagnostics and facilitating faster diagnosis without the need for dedicated imaging rooms.

USA Cardiovascular Ultrasound Market Competitive Landscape

The USA cardiovascular ultrasound market is characterized by a few key players dominating the field, leveraging their strong presence in advanced imaging technologies and extensive distribution networks. This consolidation emphasizes the influence of industry leaders who continuously innovate and expand their product portfolios to meet rising healthcare demands.

USA Cardiovascular Ultrasound Industry Analysis

Growth Drivers

- Prevalence of Cardiovascular Diseases: Cardiovascular disease (CVD) remains the top cause of mortality in the United States, with over 702,880 deaths recorded in 2022. One person dies approximately every 33 seconds due to CVD-related causes. Coronary artery disease (CAD), which affects around 5% of adults over age 20, is the most common CVD type, while almost 805,000 people experience a heart attack annually. These figures underscore the need for advanced diagnostic tools, including ultrasound, to support early diagnosis and management, especially as CVD incidence remains high among key demographic groups.

- Advancements in Imaging Technology: The integration of artificial intelligence (AI) in cardiovascular ultrasound is significantly improving image resolution and diagnostic accuracy, driving its adoption in both clinical and outpatient settings. AI-driven imaging technology enhances workflow by reducing scan times and automating diagnostic assessments. By 2024, approximately 43% of radiology departments are projected to utilize AI-enabled systems in diagnostics, particularly benefiting complex cardiovascular cases. This tech shift reflects an increasing need for sophisticated imaging in the healthcare sector to keep up with rising demand for reliable cardiovascular assessments.

- Increased Awareness and Early Diagnosis: Public awareness campaigns have led to an increase in early diagnosis rates for cardiovascular conditions. Data from CDC initiatives reveal that programs like Million Hearts, which target early diagnosis, have bolstered screening participation among adults, resulting in a 15% increase in diagnostic visits across at-risk populations between 2021 and 2023. This uptick in preventive screenings drives demand for cardiovascular ultrasound as an essential, non-invasive diagnostic tool that complements increased healthcare awareness.

Market Challenges

- High Cost of Advanced Imaging Systems: The costs associated with implementing and maintaining high-end cardiovascular ultrasound systems remain a barrier, especially for smaller healthcare facilities. These expenses often exceed $50,000 for AI-enabled imaging units, limiting their adoption across rural and less-funded urban clinics. The high cost of these systems could deter facilities from upgrading, despite the growing demand for high-resolution imaging and more comprehensive diagnostic capabilities in cardiovascular care.

- Lack of Skilled Sonographers: A shortage of trained sonographers affects the healthcare industry, as fewer than 0.3 trained sonographers are available per 1,000 population, especially outside metropolitan areas. As CVD diagnoses increase, the demand for skilled technicians grows, creating a workforce gap. This shortage places a strain on healthcare providers, limiting the timely deployment of ultrasound services essential for early cardiovascular detection.

USA Cardiovascular Ultrasound Market Future Outlook

The USA cardiovascular ultrasound market is expected to continue its growth trajectory, driven by rising incidences of cardiovascular diseases, ongoing technological advancements, and the increased adoption of portable and handheld ultrasound devices. As healthcare providers emphasize early diagnosis and preventive care, the demand for efficient, cost-effective diagnostic tools like cardiovascular ultrasound is anticipated to surge.

Market Opportunities

- Expansion in Outpatient Diagnostic Centers: Outpatient diagnostic centers are expanding rapidly, catering to a growing patient base seeking accessible cardiovascular diagnostics. Data indicates a 20% increase in diagnostic facilities offering ultrasound services since 2022, driven by higher outpatient demand for specialized services outside hospital settings. This expansion presents an opportunity to decentralize cardiovascular care, especially for preventive diagnostics among aging and at-risk populations.

- Rising Adoption of Portable Devices: The market is experiencing a surge in portable ultrasound device adoption, now comprising approximately 30% of cardiovascular ultrasound applications. Portable devices, valued for their cost-efficiency and mobility, allow clinicians to perform diagnostics outside traditional hospital settings. These systems are particularly beneficial in urgent care, mobile clinics, and rural outreach programs, addressing accessibility issues while supporting immediate diagnostic needs.

Scope of the Report

|

By Device Type |

Transthoracic Echocardiography Transesophageal Echocardiography Stress Echocardiography Fetal Echocardiography |

|

By Display Mode |

2D Imaging 3D and 4D Imaging Doppler Imaging |

|

By End User |

Hospitals Diagnostic Centers Ambulatory Surgery Centers (ASCs) |

|

By Technology |

Conventional Ultrasound Portable Ultrasound Handheld Ultrasound |

|

Region |

Northeast Midwest South West |

Products

Key Target Audience

Hospitals and Diagnostic Centers

Ambulatory Surgery Centers (ASCs)

Cardiology Practices

Government and Regulatory Bodies (FDA, CMS)

Healthcare Insurance Providers

Investments and Venture Capitalist Firms

Medical Device Distributors

Outpatient Care Facilities

Companies

Players Mentioned in the Report

Philips Healthcare

GE Healthcare

Siemens Healthineers

Canon Medical Systems

Fujifilm Holdings Corporation

Samsung Medison

Mindray Medical International

Hitachi Medical Corporation

Chison Medical Imaging

Hologic, Inc.

Table of Contents

1. USA Cardiovascular Ultrasound Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Echocardiography Utilization %)

1.4. Market Segmentation Overview

2. USA Cardiovascular Ultrasound Market Size (in USD)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis (Growth in Diagnostic Utilization %)

2.3. Key Market Developments and Milestones

3. USA Cardiovascular Ultrasound Market Analysis

3.1. Growth Drivers

3.1.1. Prevalence of Cardiovascular Diseases (Incidence Rate %)

3.1.2. Advancements in Imaging Technology (Technological Penetration %)

3.1.3. Increased Awareness and Early Diagnosis (Diagnosis Rate %)

3.1.4. Favorable Reimbursement Policies

3.2. Market Challenges

3.2.1. High Cost of Advanced Imaging Systems

3.2.2. Lack of Skilled Sonographers (Workforce Gap %)

3.2.3. Limited Accessibility in Rural Areas

3.3. Opportunities

3.3.1. Expansion in Outpatient Diagnostic Centers

3.3.2. Rising Adoption of Portable Devices (Market Share % in Portable Systems)

3.3.3. Research and Development in AI-driven Diagnostics

3.4. Trends

3.4.1. Adoption of AI and Machine Learning in Imaging Analysis

3.4.2. Miniaturization and Portability of Devices

3.4.3. Focus on Point-of-Care Diagnostics (Adoption Rate %)

3.5. Government Regulation

3.5.1. FDA Regulations on Cardiovascular Imaging Devices

3.5.2. Medicare and Medicaid Reimbursement Policies

3.5.3. Compliance with ISO Standards for Medical Devices

3.5.4. Support for Innovation in Medical Imaging

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape Overview

4. USA Cardiovascular Ultrasound Market Segmentation

4.1. By Device Type (in Value %)

4.1.1. Transthoracic Echocardiography

4.1.2. Transesophageal Echocardiography

4.1.3. Stress Echocardiography

4.1.4. Fetal Echocardiography

4.2. By Display Mode (in Value %)

4.2.1. 2D Imaging

4.2.2. 3D and 4D Imaging

4.2.3. Doppler Imaging

4.3. By End User (in Value %)

4.3.1. Hospitals

4.3.2. Diagnostic Centers

4.3.3. Ambulatory Surgery Centers (ASCs)

4.4. By Technology (in Value %)

4.4.1. Conventional Ultrasound

4.4.2. Portable Ultrasound

4.4.3. Handheld Ultrasound

4.5. By Region (in Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

5. USA Cardiovascular Ultrasound Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Philips Healthcare

5.1.2. GE Healthcare

5.1.3. Siemens Healthineers

5.1.4. Canon Medical Systems

5.1.5. Fujifilm Holdings Corporation

5.1.6. Samsung Medison Co., Ltd.

5.1.7. Mindray Medical International Ltd.

5.1.8. Esaote SpA

5.1.9. Hitachi Medical Corporation

5.1.10. Chison Medical Imaging

5.1.11. Hologic, Inc.

5.1.12. Shantou Institute of Ultrasonic Instruments Co., Ltd.

5.1.13. Mobisante Inc.

5.1.14. Trivitron Healthcare

5.1.15. BMV Technology Co., Ltd.

5.2. Cross Comparison Parameters (Revenue, Headquarters, Number of Employees, Key Products, Regional Presence, Annual R&D Investment %, Regulatory Compliance)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. USA Cardiovascular Ultrasound Market Regulatory Framework

6.1. FDA Approval Processes

6.2. Compliance with Medical Device Standards

6.3. Reimbursement Codes and Policies

7. USA Cardiovascular Ultrasound Future Market Size (in USD)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Cardiovascular Ultrasound Market Segmentation

8.1. By Device Type (in Value %)

8.2. By Display Mode (in Value %)

8.3. By End User (in Value %)

8.4. By Technology (in Value %)

8.5. By Region (in Value %)

9. USA Cardiovascular Ultrasound Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research begins by constructing an ecosystem map, identifying all relevant stakeholders within the USA Cardiovascular Ultrasound Market. Extensive desk research and proprietary database access ensure comprehensive data collection on industry-level dynamics, helping to define key market variables.

Step 2: Market Analysis and Construction

The next phase involves compiling and analyzing historical data on market penetration, technology adoption, and regional diagnostic needs. The data evaluation emphasizes accuracy in revenue estimates through cross-analysis of primary and secondary sources.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are refined through expert consultations and computer-assisted telephone interviews (CATIs) with industry professionals, validating our data and adding insights into market trends and operational challenges.

Step 4: Research Synthesis and Final Output

In the final step, we engage with device manufacturers and healthcare providers to gain insights into specific product segments, sales trends, and market preferences, verifying data accuracy and solidifying our comprehensive view of the USA Cardiovascular Ultrasound market.

Frequently Asked Questions

1. How big is the USA Cardiovascular Ultrasound Market?

The USA cardiovascular ultrasound market is valued at USD 678 million, based on a five-year historical analysis. This market is primarily driven by the increasing prevalence of cardiovascular diseases, which necessitates effective and non-invasive diagnostic tools.

2. What are the major growth drivers in the USA Cardiovascular Ultrasound Market?

Key growth drivers include increased incidences of cardiovascular conditions, the demand for non-invasive diagnostics, and advancements in portable ultrasound technology.

3. Who are the major players in the USA Cardiovascular Ultrasound Market?

Leading players include Philips Healthcare, GE Healthcare, Siemens Healthineers, Canon Medical Systems, and Fujifilm, who dominate due to their advanced product offerings and robust market presence.

4. What challenges does the USA Cardiovascular Ultrasound Market face?

Challenges include the high costs associated with advanced ultrasound systems, a shortage of skilled ultrasound technicians, and limited access in rural areas.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.