USA Champagne Market Outlook to 2030

Region:North America

Author(s):Meenakshi Bisht

Product Code:KROD9840

Region:North America

Author(s):Meenakshi Bisht

Product Code:KROD9840

December 2024

98

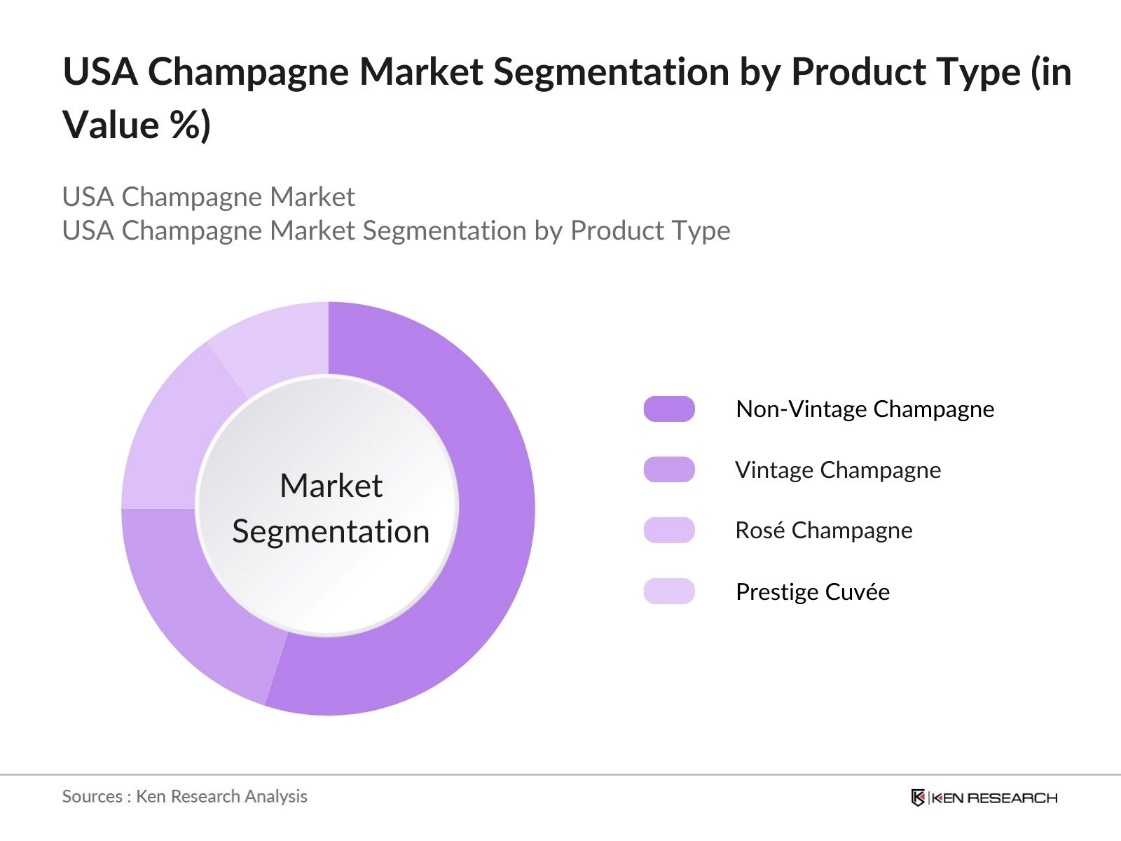

By Product Type: The USA Champagne market is segmented by product type into Vintage Champagne, Non-Vintage Champagne, Ros Champagne, and Prestige Cuve. Recently, Non-Vintage Champagne has emerged as the dominant sub-segment. Its dominance is largely due to its affordability compared to vintage varieties, making it more accessible to a broader range of consumers. Non-vintage champagnes are produced annually, using a blend of several vintages, which ensures consistency in quality and supply, a critical factor for meeting consumer demand in the USA, where buyers often prioritize quality and value.

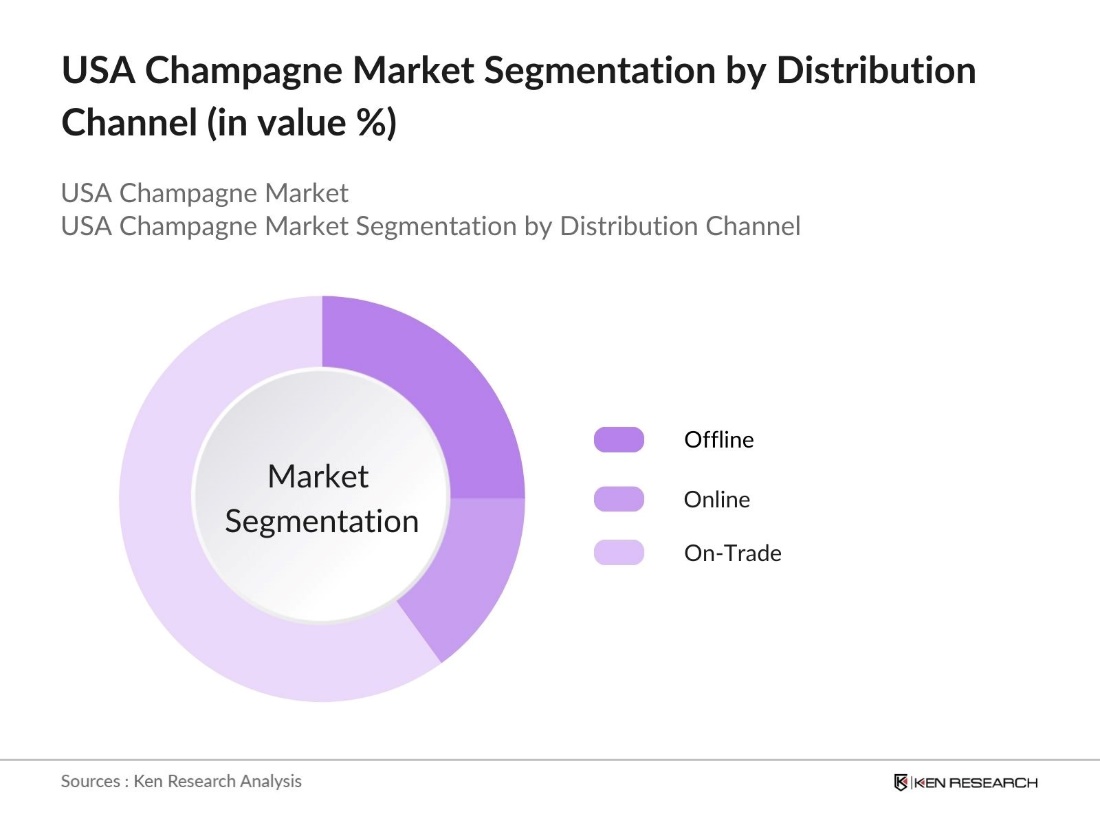

By Distribution Channel: The USA Champagne market is segmented by distribution channel into Offline (Retail Stores, Supermarkets, Liquor Stores), Online (E-Commerce Platforms, Direct-to-Consumer), and On-Trade (Restaurants, Bars, Hotels). On-Trade distribution leads in terms of market share due to the strong association of champagne with dining and special event experiences. Consumers often purchase champagne during fine dining experiences or at celebratory events like weddings and corporate functions. Restaurants and bars also create exclusive opportunities for showcasing high-end champagne products, contributing to the dominance of this segment.

The USA Champagne market is dominated by a mix of international and local brands, with global giants leading the market in terms of brand recognition, product quality, and distribution networks. These companies invest heavily in marketing, and many have well-established relationships with luxury venues and events, ensuring their continued dominance.

|

Company Name |

Established Year |

Headquarters |

Production Capacity |

E-Commerce Integration |

Sustainability Initiatives |

Brand Endorsements |

New Product Introductions |

Global vs. Local Distribution |

|

Mot & Chandon |

1743 |

pernay, France |

||||||

|

Veuve Clicquot |

1772 |

Reims, France |

||||||

|

Louis Roederer |

1776 |

Reims, France |

||||||

|

Laurent-Perrier |

1812 |

Tours-sur-Marne, France |

||||||

|

Dom Prignon |

1668 |

pernay, France |

Over the next five years, the USA Champagne market is expected to show consistent growth driven by an increasing affinity for luxury products, especially in urban areas. The market is likely to benefit from the continued expansion of e-commerce platforms, enabling broader consumer access to premium champagne offerings. Additionally, innovations in champagne production, including more sustainable practices and new flavor profiles, will cater to evolving consumer preferences for eco-friendly and diverse products.

|

Product Type |

Vintage Champagne Non-Vintage Champagne Ros Champagne Prestige Cuve |

|

Distribution Channel |

Offline (Retail Stores, Supermarkets, Liquor Stores) Online (E-Commerce Platforms, Direct-to-Consumer) On-Trade (Restaurants, Bars, Hotels) |

|

Price Range |

Economy Mid-Range Premium Luxury |

|

End-User |

Individual Consumers Corporate Consumers Event-Based Consumers (Weddings, Celebrations) |

|

Region |

Northeast Midwest South West |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Consumer Disposable Income (Disposable Income, Purchasing Power)

3.1.2. Increasing Demand for Premium Products (Premiumization)

3.1.3. Influence of Celebratory Culture (Event and Occasions Spending)

3.1.4. Rising E-Commerce and Online Distribution (E-commerce Penetration)

3.2. Market Challenges

3.2.1. Stringent Regulatory Framework (FDA and TTB Regulations)

3.2.2. Fluctuations in Production due to Climate Change (Weather Impact, Crop Yields)

3.2.3. High Competition from Sparkling Wine Alternatives (Substitution by Prosecco, Cava)

3.3. Opportunities

3.3.1. Rising Popularity of Non-Alcoholic Champagne (Health Consciousness, Non-Alcoholic Beverages Market)

3.3.2. Expansion in New Distribution Channels (Direct-to-Consumer, E-Retailing)

3.3.3. Growth in Small and Independent Wineries (Craft and Boutique Producers)

3.4. Trends

3.4.1. Increasing Focus on Sustainability (Sustainable Viticulture, Eco-Friendly Packaging)

3.4.2. Innovations in Flavors and Packaging (Flavor Diversity, Customizable Bottles)

3.4.3. Celebrity Endorsements and Partnerships (Brand Collaborations with Influencers)

3.5. Government Regulation

3.5.1. Champagne Labeling Requirements (AOC Regulations, Origin Certification)

3.5.2. Import Tariffs and Trade Policies (Impact of Tariffs, International Trade Policies)

3.5.3. Marketing Restrictions for Alcoholic Beverages (Advertising Rules, Age Restrictions)

3.6. SWOT Analysis

3.6.1. Strengths (Premium Perception, Heritage and Luxury Positioning)

3.6.2. Weaknesses (Limited Supply, Seasonality)

3.6.3. Opportunities (Emerging Markets, E-Commerce Growth)

3.6.4. Threats (Economic Downturns, Competition from Sparkling Wines)

3.7. Stake Ecosystem

3.7.1. Producers (Vineyard Owners, Winemakers)

3.7.2. Distributors (Retailers, E-Commerce Platforms)

3.7.3. End-Consumers (Luxury Consumers, Event-Based Purchasers)

3.8. Porters Five Forces

3.8.1. Threat of New Entrants (Barriers to Entry, Capital Investment)

3.8.2. Bargaining Power of Suppliers (Raw Material Costs, Viticulture Dependencies)

3.8.3. Bargaining Power of Buyers (Consumer Preferences, Market Competition)

3.8.4. Threat of Substitutes (Sparkling Wines, Non-Alcoholic Alternatives)

3.8.5. Industry Rivalry (Brand Competitiveness, Product Differentiation)

3.9. Competition Ecosystem (Competitors, Market Shares, Competitive Strategies)

4.1. By Product Type (In Value %)

4.1.1. Vintage Champagne

4.1.2. Non-Vintage Champagne

4.1.3. Ros Champagne

4.1.4. Prestige Cuve

4.2. By Distribution Channel (In Value %)

4.2.1. Offline (Retail Stores, Supermarkets, Liquor Stores)

4.2.2. Online (E-Commerce Platforms, Direct-to-Consumer)

4.2.3. On-Trade (Restaurants, Bars, Hotels)

4.3. By Price Range (In Value %)

4.3.1. Economy

4.3.2. Mid-Range

4.3.3. Premium

4.3.4. Luxury

4.4. By End-User (In Value %)

4.4.1. Individual Consumers

4.4.2. Corporate Consumers

4.4.3. Event-Based Consumers (Weddings, Celebrations)

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

5.1 Detailed Profiles of Major Companies

5.1.1. Mot & Chandon

5.1.2. Veuve Clicquot

5.1.3. Dom Prignon

5.1.4. Louis Roederer

5.1.5. Laurent-Perrier

5.1.6. Perrier-Jout

5.1.7. Pol Roger

5.1.8. Taittinger

5.1.9. Krug

5.1.10. Bollinger

5.1.11. G.H. Mumm

5.1.12. Ruinart

5.1.13. Piper-Heidsieck

5.1.14. Nicolas Feuillatte

5.1.15. Charles Heidsieck

5.2 Cross Comparison Parameters (Headquarters, Production Capacity, Vintage vs. Non-Vintage Sales, Global vs. Local Distribution, Sustainability Practices, E-Commerce Integration, Marketing Expenditure, New Product Introductions)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. FDA and TTB Compliance

6.2. Alcohol Distribution Laws

6.3. Environmental Sustainability Certifications

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By Price Range (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Cohort Analysis

9.3. White Space Opportunity Analysis

Disclaimer Contact UsThis stage involved identifying all key stakeholders in the USA Champagne market, including producers, distributors, retailers, and consumers. Extensive desk research was conducted, utilizing proprietary databases and industry reports to pinpoint the most influential market factors, such as consumer behavior trends, regulatory frameworks, and distribution channels.

In this phase, historical market data from various sources was compiled and analyzed. This included evaluating the production levels of champagne, consumer purchasing patterns, and the impact of marketing campaigns by key brands. Special emphasis was placed on identifying revenue generated through various distribution channels and product segments.

To validate the collected data, consultations with industry experts, including champagne producers and retail managers, were conducted. These expert interviews provided valuable insights into the operational and financial dynamics of the champagne industry, especially in the USA market.

In the final stage, the research was synthesized, and the findings were compiled into a comprehensive report. The report includes validated data from primary and secondary sources, offering a detailed analysis of the USA Champagne market, including segmentation by product type and distribution channel, as well as competitive landscape and future growth potential.

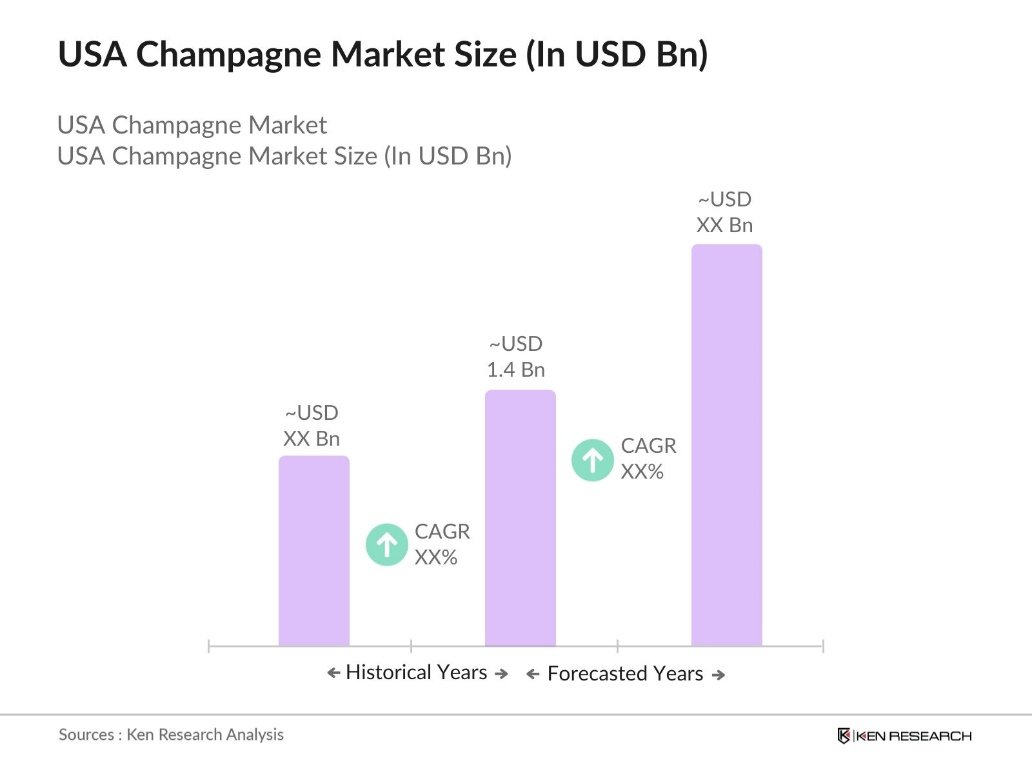

The USA Champagne Market is valued at USD 1.4 billion, driven by increasing demand for premium alcoholic beverages and the rise of e-commerce platforms.

Challenges in USA Champagne Market include stringent regulatory frameworks for alcoholic beverages, fluctuating production due to climate change, and rising competition from alternative sparkling wines like Prosecco and Cava.

Key players in the USA Champagne Market include Mot & Chandon, Veuve Clicquot, Dom Prignon, Louis Roederer, and Laurent-Perrier. These companies dominate due to their strong brand presence, premium product offerings, and global distribution networks.

The USA Champagne Market is propelled by the rising popularity of premium alcoholic beverages for celebratory events, increased disposable income among middle and upper-middle-class consumers, and the growth of e-commerce platforms.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.