USA Companion Animal Diagnostics Market Outlook to 2030

Region:North America

Author(s):Paribhasha Tiwari

Product Code:KROD5082

December 2024

95

About the Report

USA Companion Animal Diagnostics Market Overview

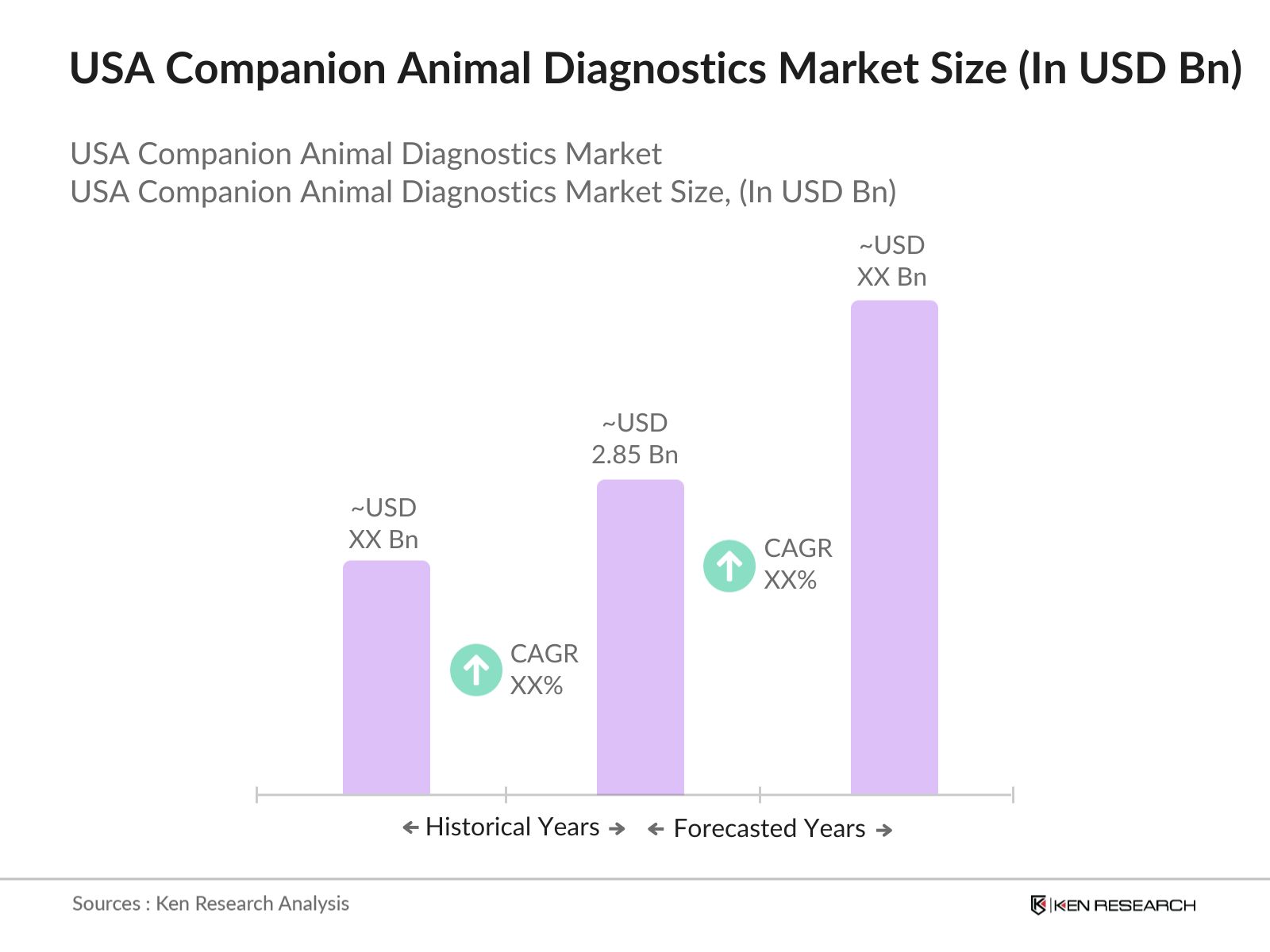

- The USA Companion Animal Diagnostics market is valued at USD 2.85 billion, based on a five-year historical analysis. The market is primarily driven by the increasing pet ownership trend in the country, coupled with rising expenditures on animal healthcare. Additionally, the adoption of advanced diagnostic technologies, such as molecular diagnostics and point-of-care testing, plays a significant role in expanding the market. The shift toward preventive healthcare in pets is further contributing to this robust growth.

- The USA is home to several dominant cities that lead the companion animal diagnostics market. Cities like New York, Los Angeles, and Chicago are significant players due to their large population of pet owners and high concentration of veterinary hospitals and research institutes. These cities benefit from high disposable income, allowing pet owners to invest in sophisticated diagnostic tools and treatments. The strong presence of advanced veterinary infrastructure in these cities also drives their dominance in the market.

- The U.S. government, through the National Institute of Food and Agriculture (NIFA), invested in veterinary education programs to address the workforce shortage. In 2024, more than $30 million was allocated to fund veterinary schools and programs focused on rural areas, aiming to increase the number of qualified professionals entering the field. This initiative is designed to ensure that more veterinary clinics are equipped to offer comprehensive diagnostic services in underserved regions.

USA Companion Animal Diagnostics Market Segmentation

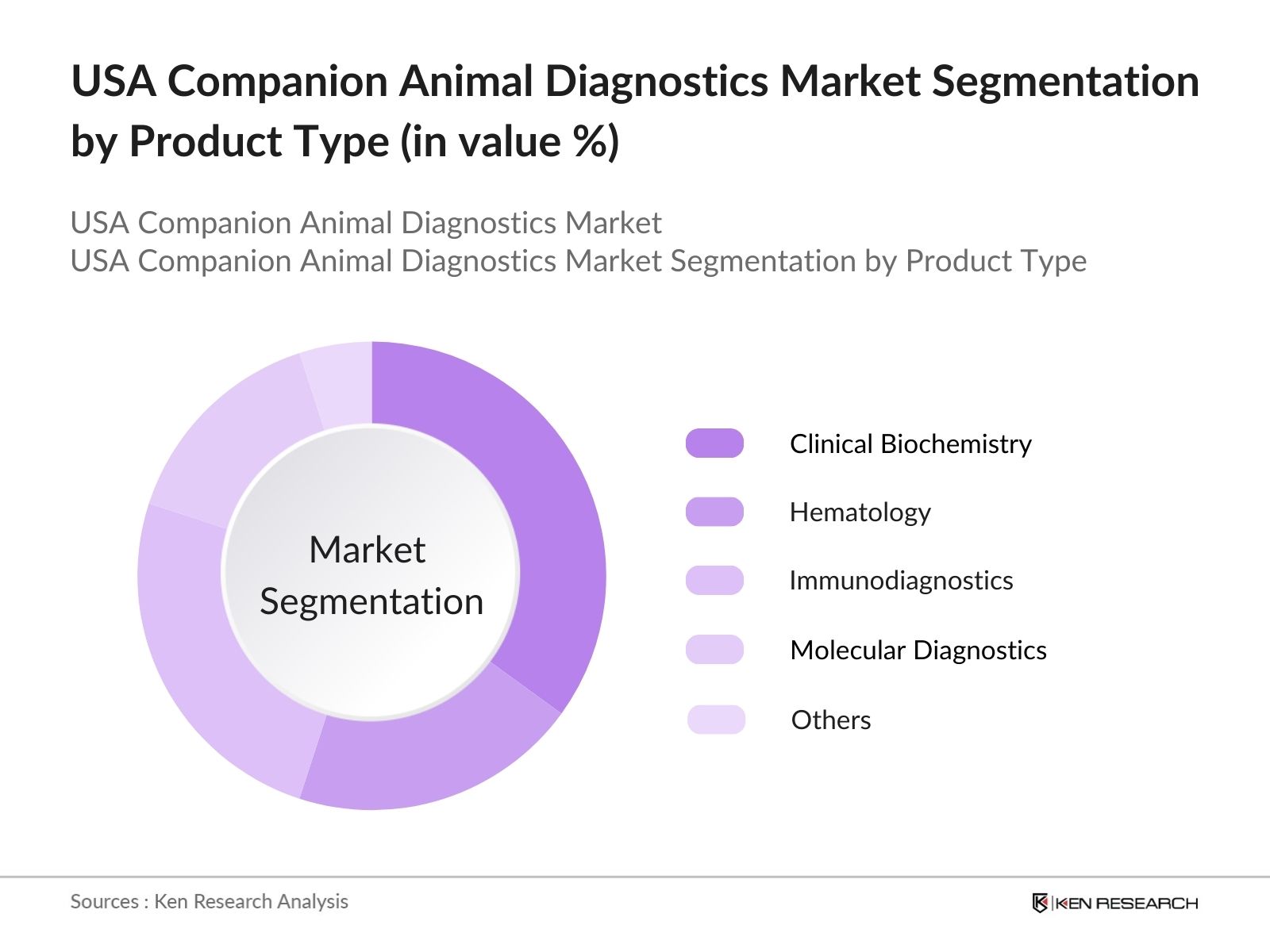

By Product Type: The USA Companion Animal Diagnostics market is segmented by product type into clinical biochemistry, hematology, immunodiagnostics, molecular diagnostics, and others (microbiology, cytology). Clinical biochemistry holds a dominant market share, largely due to its widespread use in routine diagnostic tests for pets, including kidney and liver function tests. The increasing demand for rapid diagnostic results in the treatment of common diseases such as diabetes and kidney disorders in pets further propels the growth of this segment.

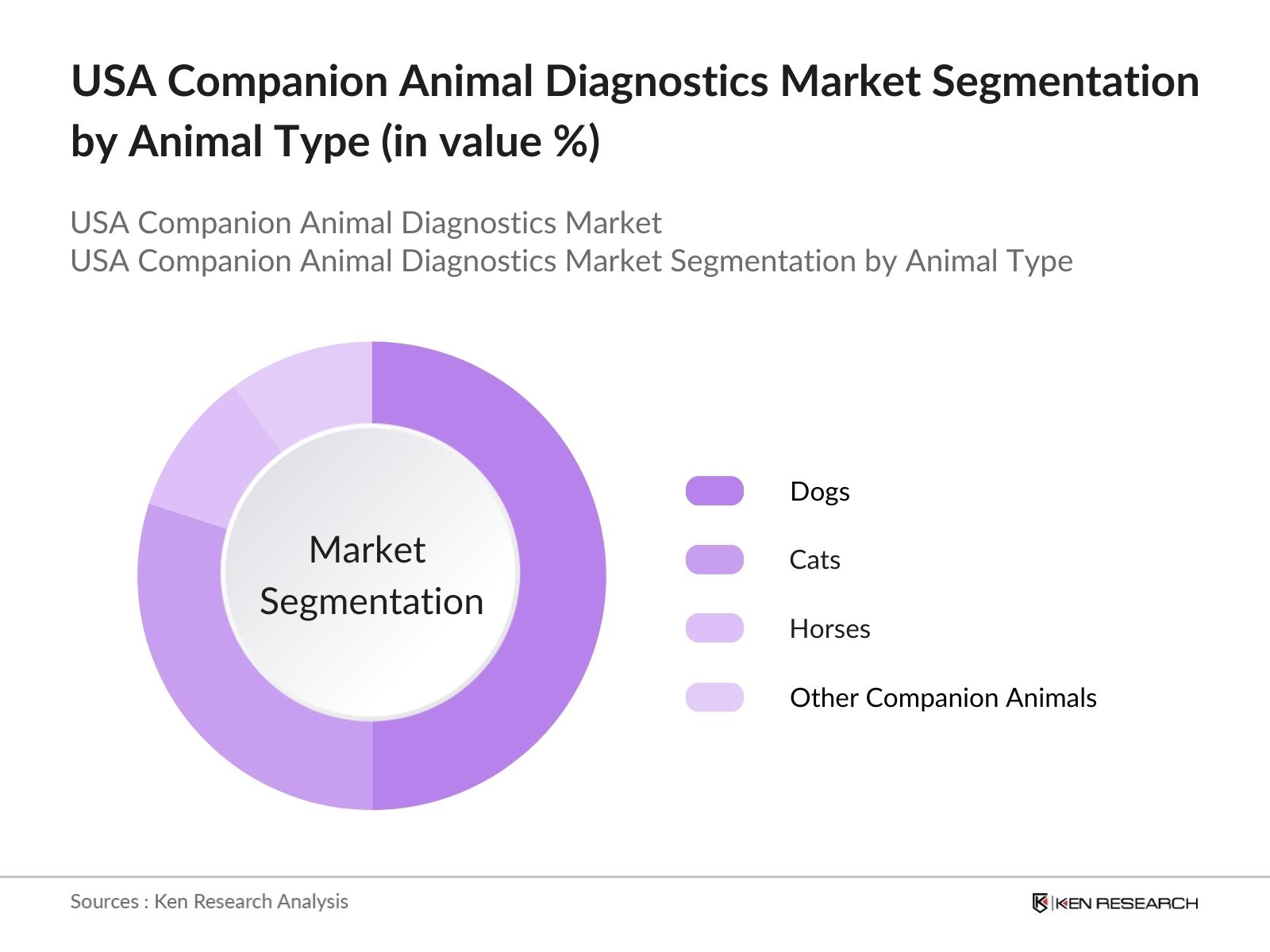

By Animal Type: The market is segmented by animal type into dogs, cats, horses, and other companion animals (birds, rabbits, etc.). Dogs account for the largest market share in the companion animal diagnostics market, as they are the most popular pets in the USA. Diagnostic tests for dogs are primarily driven by the high prevalence of chronic diseases such as arthritis, obesity, and diabetes. The rising demand for routine health checkups and preventive care in dogs further contributes to the segment's dominance.

USA Companion Animal Diagnostics Market Competitive Landscape

The USA Companion Animal Diagnostics market is dominated by a few key players that have established a strong presence through innovation, product development, and mergers and acquisitions. Companies like IDEXX Laboratories and Zoetis Inc. are leaders due to their extensive product portfolios and investments in research and development. The growing trend toward telemedicine and the use of digital platforms for veterinary diagnostics has also encouraged new entrants and innovation-driven competition.

|

Company Name |

Established Year |

Headquarters |

Product Portfolio |

R&D Investment |

Revenue (2023) |

Diagnostic Test Pipeline |

Market Presence |

Strategic Partnerships |

Distribution Network |

|

IDEXX Laboratories, Inc. |

1983 |

Westbrook, Maine |

- | - | - | - | - | - | - |

|

Zoetis Inc. |

1952 |

Parsippany, New Jersey |

- | - | - | - | - | - | - |

|

Heska Corporation |

1988 |

Loveland, Colorado |

- | - | - | - | - | - | - |

|

Thermo Fisher Scientific |

1956 |

Waltham, Massachusetts |

- | - | - | - | - | - | - |

|

Neogen Corporation |

1982 |

Lansing, Michigan |

- | - | - | - | - | - | - |

USA Companion Animal Diagnostics Market Analysis

Growth Drivers

- Increasing Pet Ownership: In 2024, the United States experienced a significant rise in pet ownership, with approximately 89 million dogs and 96 million cats kept as pets. This surge in pet ownership, driven by lifestyle changes and increased awareness of the mental health benefits of pets, has amplified the demand for companion animal diagnostics. The pet population growth has directly influenced the healthcare needs of these animals, creating opportunities in the diagnostics market. The American Pet Products Association reported a consistent rise in pet adoption and ownership since 2020, with a steady annual increase in pet-related expenditures, underscoring the potential for diagnostics demand.

- Technological Advancements: Technological advancements in the companion animal diagnostics market, particularly in rapid diagnostics and molecular diagnostics, are accelerating the market's growth. For instance, the availability of Polymerase Chain Reaction (PCR) technology for pets enables faster and more accurate disease detection. The global diagnostics industry has seen substantial investment in molecular diagnostic tools, and these technologies have reduced diagnosis time from days to hours. With over 12,000 veterinary clinics in the USA in 2024, the adoption of these tools has increased rapidly, making veterinary diagnostics more efficient and effective in delivering accurate results.

- Growing Focus on Animal Health: As veterinary medicine increasingly focuses on preventative care; pet owners are more proactive about diagnostics. In 2024, the American Veterinary Medical Association emphasized early diagnosis to prevent severe health conditions in pets, leading to greater use of diagnostics. This trend is aligned with increased veterinary visits, as around 80 million households in the U.S. have pets that require regular health check-ups. Diagnostic tests, including blood work and imaging, are becoming routine for pets, ensuring their health is maintained, and potential issues are identified earlier.

Market Challenges

- High Cost of Diagnostic Tests: Diagnostic tests for pets, such as advanced imaging and molecular diagnostics, can be expensive, with some tests costing between $300 to $1,000. This cost sensitivity is a significant challenge, particularly for pet owners without insurance or those with lower income. In 2024, despite the growing pet population, many owners still find it difficult to afford these diagnostic tests. This limits the markets reach, especially for non-life-threatening conditions, as owners may opt out of expensive diagnostic procedures, preferring to wait for visible symptoms instead of early detection, thereby restraining market growth.

- Lack of Awareness Among Pet Owners: A significant portion of the pet-owning population remains unaware of the diagnostic tools available for animals. In 2024, surveys indicated that about 40% of pet owners in rural and semi-urban areas in the U.S. are unaware of advanced diagnostic tests. This lack of awareness, combined with limited access to veterinary clinics in less urbanized regions, restricts the adoption of diagnostic services. Although the veterinary industry is growing, there is still a gap in educational outreach about preventive care and the importance of early diagnostics for companion animals.

USA Companion Animal Diagnostics Market Future Outlook

The USA Companion Animal Diagnostics market is expected to experience substantial growth over the next five years, fueled by increasing demand for early diagnosis and preventive care among pet owners. Advancements in diagnostic technologies, such as AI-driven tools and telemedicine solutions, will likely shape the future landscape of this market. Rising veterinary healthcare spending and the expansion of pet insurance coverage are also anticipated to contribute to this upward trend. The growing awareness of zoonotic diseases and the role of diagnostics in preventing disease transmission between pets and humans further highlight the market's importance in the future.

Market Opportunities

- Expansion of Point-of-Care Testing: The development of point-of-care testing technologies is poised to revolutionize the companion animal diagnostics market. In 2024, point-of-care diagnostic devices capable of delivering results within minutes have become increasingly popular among veterinary clinics. These portable diagnostic tools allow for rapid in-office testing of conditions like infections and metabolic diseases, reducing the need for external laboratory testing. The U.S. market has seen over 4,000 veterinary clinics adopt point-of-care diagnostics, enhancing the efficiency of care delivery, reducing the wait time for diagnosis, and improving treatment outcomes.

- Growth in Pet Insurance Coverage: In 2024, the U.S. pet insurance industry covered around 5 million pets, with policies increasingly covering diagnostic procedures, thus driving growth in diagnostic spending. Pet insurance companies have recognized the value of preventative care and diagnostics in minimizing long-term treatment costs, resulting in broader coverage of veterinary diagnostics. This trend has encouraged pet owners to opt for diagnostic services without the fear of high out-of-pocket costs, fostering increased adoption of advanced diagnostic tools like genetic testing and imaging. Insurance coverage is playing a crucial role in making diagnostics more accessible and affordable for pet owners.

Scope of the Report

Products

Key Target Audience

Veterinary Hospitals and Clinics

Diagnostic Laboratories

Animal Healthcare Providers

Companion Animal Diagnostic Tool Manufacturers

Veterinary Research Institutes

Government and Regulatory Bodies (FDA, USDA)

Pet Insurance Providers

Investments and Venture Capitalist Firms

Companies

Players Mentioned in the Report:

IDEXX Laboratories, Inc.

Zoetis Inc.

Heska Corporation

Thermo Fisher Scientific

Neogen Corporation

VCA Antech, Inc.

Virbac

Bio-Rad Laboratories, Inc.

Agrolabo S.p.A.

Eurolyser Diagnostica GmbH

Table of Contents

1. USA Companion Animal Diagnostics Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. USA Companion Animal Diagnostics Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. USA Companion Animal Diagnostics Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Pet Ownership (Companion Animal Population)

3.1.2. Technological Advancements (Rapid Diagnostics, Molecular Diagnostics)

3.1.3. Growing Focus on Animal Health (Preventative Care)

3.1.4. Rising Veterinary Expenditures

3.2. Market Challenges

3.2.1. High Cost of Diagnostic Tests (Cost Sensitivity)

3.2.2. Lack of Awareness Among Pet Owners (Limited Access to Diagnostic Tools)

3.2.3. Shortage of Veterinary Professionals (Veterinary Workforce Constraints)

3.3. Opportunities

3.3.1. Expansion of Point-of-Care Testing (Rapid Diagnostics for Vets)

3.3.2. Growth in Pet Insurance Coverage (Increased Spending on Diagnostics)

3.3.3. Integration of Artificial Intelligence in Diagnostics

3.4. Trends

3.4.1. Rise in Preventative Diagnostics (Routine Diagnostic Testing)

3.4.2. Increasing Use of Molecular Diagnostic Tools (PCR, Genomic Tests)

3.4.3. Digital Platforms for Veterinary Diagnostics (Telemedicine Integration)

3.5. Government Regulations

3.5.1. FDA Guidelines on Companion Animal Diagnostics

3.5.2. USDA Regulations for Veterinary Products

3.5.3. Animal Health Monitoring Programs

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape Analysis

4. USA Companion Animal Diagnostics Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Clinical Biochemistry

4.1.2. Hematology

4.1.3. Immunodiagnostics

4.1.4. Molecular Diagnostics

4.1.5. Others (Microbiology, Cytology)

4.2. By Animal Type (In Value %)

4.2.1. Dogs

4.2.2. Cats

4.2.3. Horses

4.2.4. Other Companion Animals (Birds, Rabbits)

4.3. By End-User (In Value %)

4.3.1. Veterinary Hospitals & Clinics

4.3.2. Diagnostic Laboratories

4.3.3. Research Institutes

4.4. By Technology (In Value %)

4.4.1. Point-of-Care Testing (POCT)

4.4.2. Polymerase Chain Reaction (PCR)

4.4.3. Immunohistochemistry (IHC)

4.4.4. ELISA (Enzyme-linked Immunosorbent Assay)

4.4.5. Others (Electrochemiluminescence, Mass Spectrometry)

4.5. By Region (In Value %)

4.5.1. Northeast USA

4.5.2. Midwest USA

4.5.3. South USA

4.5.4. West USA

5. USA Companion Animal Diagnostics Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. IDEXX Laboratories, Inc.

5.1.2. Zoetis Inc.

5.1.3. Heska Corporation

5.1.4. Thermo Fisher Scientific

5.1.5. Neogen Corporation

5.1.6. VCA Antech, Inc.

5.1.7. Virbac

5.1.8. Bio-Rad Laboratories, Inc.

5.1.9. Agrolabo S.p.A.

5.1.10. Eurolyser Diagnostica GmbH

5.1.11. FUJIFILM Corporation

5.1.12. Abaxis

5.1.13. Idvet

5.1.14. Randox Laboratories

5.1.15. Biomerieux SA

5.2. Cross Comparison Parameters (Product Portfolio, Distribution Network, R&D Investment, Market Presence, Strategic Partnerships, Revenue, Key Technologies, Diagnostic Test Pipeline)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Mergers, Acquisitions, Collaborations)

5.5. Investment Analysis

5.6. Government Grants and Funding

5.7. Private Equity Investments

6. USA Companion Animal Diagnostics Market Regulatory Framework

6.1. FDA Guidelines

6.2. Compliance with Veterinary Medical Devices Act

6.3. Certification and Approval Processes

7. USA Companion Animal Diagnostics Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Companion Animal Diagnostics Future Market Segmentation

8.1. By Product Type

8.2. By Animal Type

8.3. By End-User

8.4. By Technology

8.5. By Region

9. USA Companion Animal Diagnostics Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Segment Analysis

9.3. Marketing and Distribution Strategies

9.4. Growth Opportunities in Diagnostic Innovations

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves creating an industry ecosystem map that includes all major stakeholders in the USA Companion Animal Diagnostics Market. This step uses desk research to gather extensive industry-level information from secondary databases. The focus is on defining the key variables driving the market, such as technology trends, pet ownership, and healthcare expenditure.

Step 2: Market Analysis and Construction

The second phase involves gathering and analyzing historical data on market penetration, service provider ratios, and revenue generation. This analysis will include service quality metrics to ensure accurate and reliable revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are formulated and validated using computer-assisted telephone interviews (CATIs) with industry experts. These interviews provide critical insights that will help refine the initial data collected and ensure its accuracy.

Step 4: Research Synthesis and Final Output

In the final stage, direct interviews with key players in the companion animal diagnostics industry are conducted to acquire detailed insights into product segmentation, sales performance, and consumer trends. This ensures the synthesis of a comprehensive and validated final market report.

Frequently Asked Questions

01. How big is the USA Companion Animal Diagnostics Market?

The USA Companion Animal Diagnostics market is valued at USD 2.85 billion and is driven by the rising adoption of pets and increasing investments in animal healthcare.

02. What are the key challenges in the USA Companion Animal Diagnostics Market?

Challenges in the USA Companion Animal Diagnostics market include the high costs of diagnostic tests, limited awareness among pet owners, and a shortage of skilled veterinary professionals to operate advanced diagnostic tools.

03. Who are the major players in the USA Companion Animal Diagnostics Market?

Major players in the USA Companion Animal Diagnostics market include IDEXX Laboratories, Zoetis Inc., Heska Corporation, Thermo Fisher Scientific, and Neogen Corporation, who lead due to their broad product portfolios and investments in innovation.

04. What are the growth drivers of the USA Companion Animal Diagnostics Market?

Key drivers in the USA Companion Animal Diagnostics market include the increasing focus on preventive care, rising demand for point-of-care testing, and growing awareness of zoonotic diseases.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.