USA Computed Tomography Market Outlook to 2030

Region:North America

Author(s):Shubham Kashyap

Product Code:KROD3093

November 2024

82

About the Report

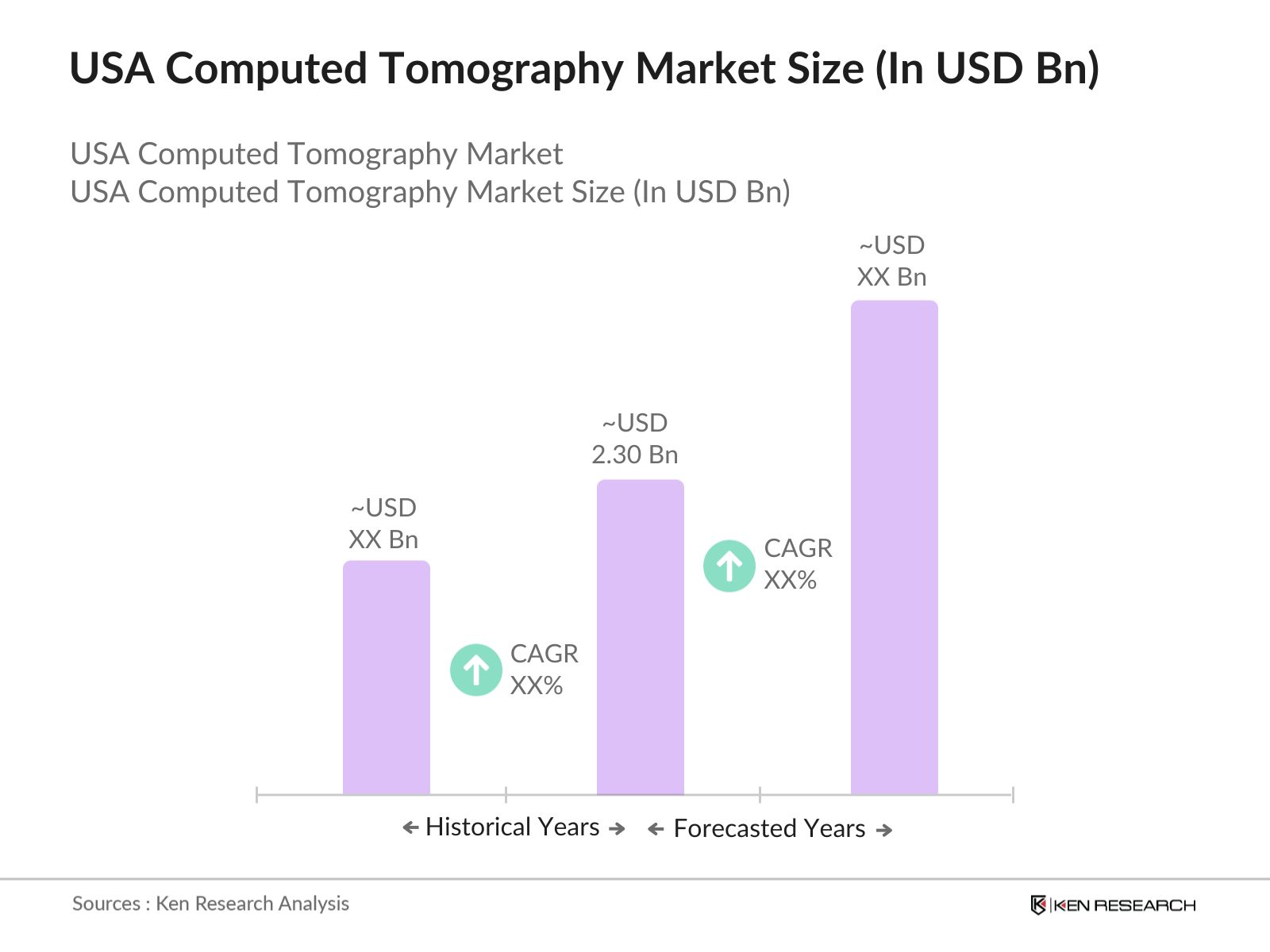

USA Computed Tomography Market Overview

- The USA Computed Tomography (CT) Market is valued at USD 2.30 billion, driven by the increasing prevalence of chronic diseases, the growing geriatric population, and the rising demand for diagnostic imaging technologies. Over the past five years, advancements in CT scanner technology, including low-dose radiation techniques and higher resolution imaging, have contributed to significant market growth. Additionally, the adoption of artificial intelligence in imaging analysis has enhanced diagnostic accuracy, further driving market expansion.

- Major metropolitan areas such as New York, Los Angeles, and Chicago are key regions for the CT market, benefiting from the presence of advanced healthcare facilities and a high concentration of radiology centers. In rural areas, the expansion of telemedicine and mobile imaging services is improving access to CT diagnostics, particularly for underserved populations.

- The FDAs regulatory framework for medical imaging equipment, particularly CT scanners, is essential in ensuring safety and performance standards. Recent regulations introduced in 2023 have set stricter guidelines on radiation exposure levels, influencing manufacturers to innovate and comply with safety requirements.

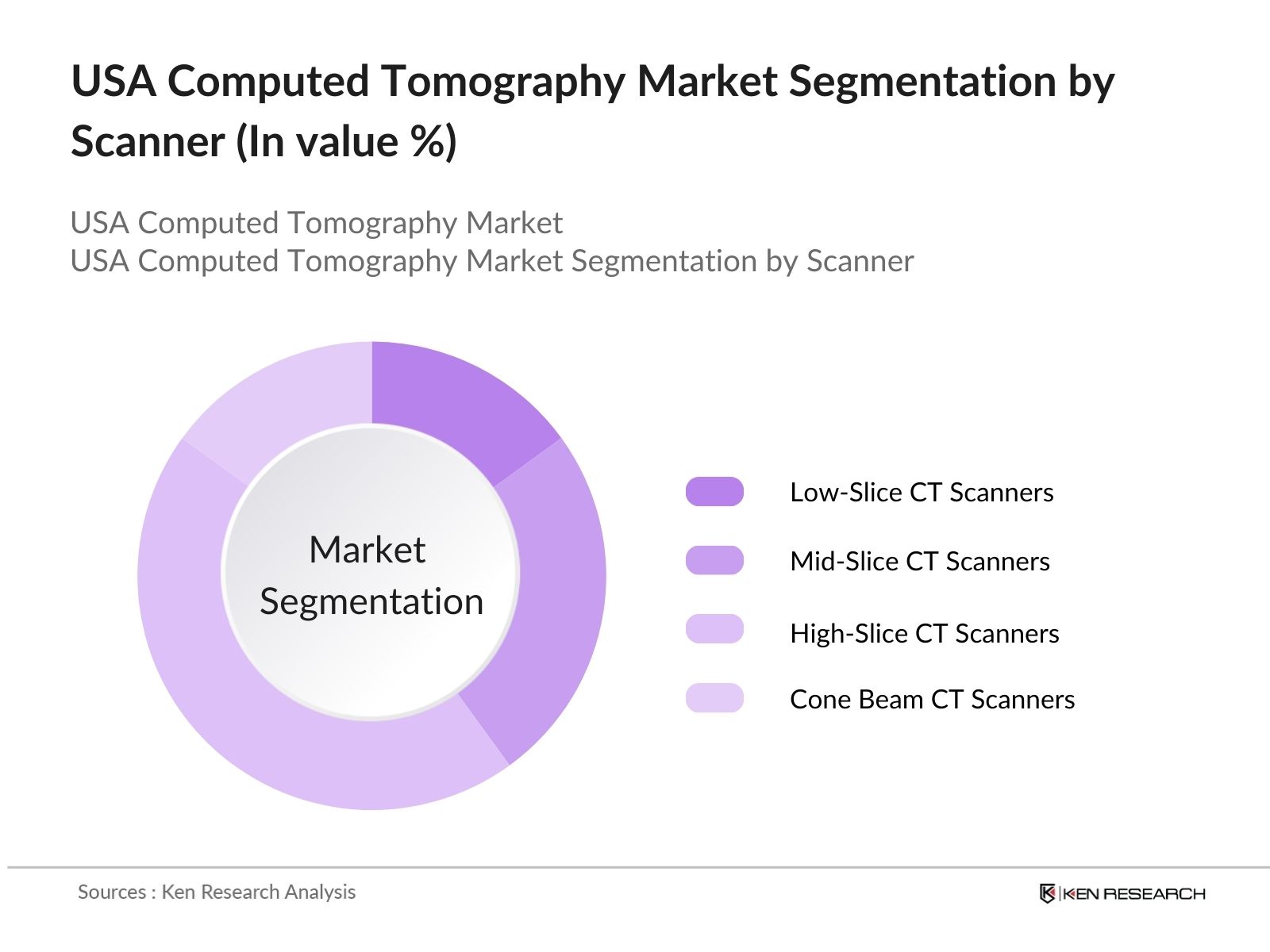

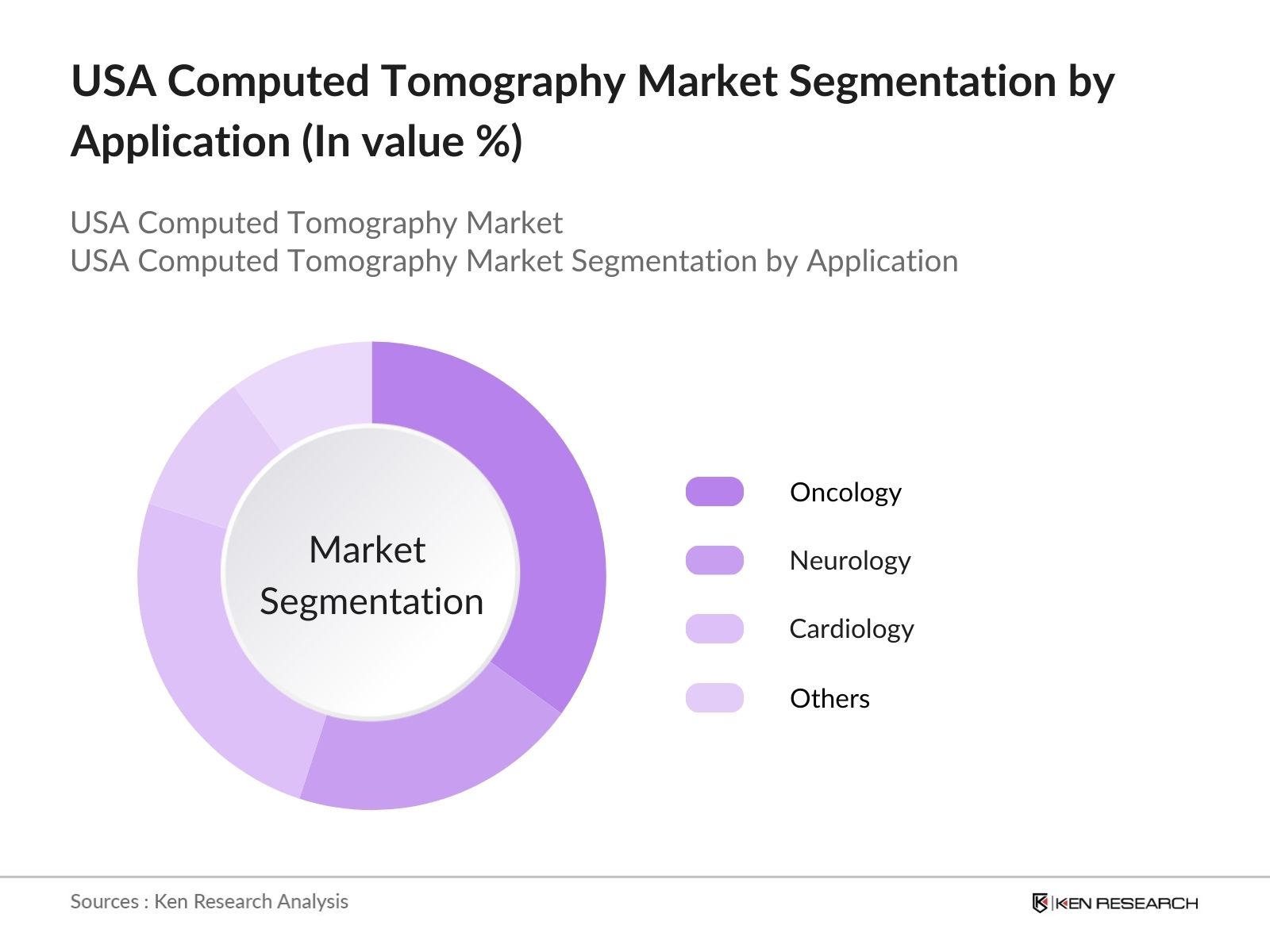

USA Computed Tomography Market Segmentation

- By Type of Scanner: The market is segmented into low-slice CT scanners, mid-slice CT scanners, high-slice CT scanners, and cone beam CT scanners. High-slice CT scanners dominate the market due to their ability to capture detailed images with lower radiation doses, making them suitable for complex cardiac and vascular diagnostics. Mid-slice scanners are popular in smaller hospitals and clinics for routine diagnostic imaging, while cone beam CT scanners are increasingly used in dental and orthopedic imaging due to their precision in smaller anatomical areas.

- By Application: The market is segmented by application into oncology, neurology, cardiology, musculoskeletal, and others. Oncology holds the largest market share due to the increasing incidence of cancer in the U.S., with CT being a vital tool in tumor detection and monitoring. Cardiology and neurology are also significant applications, driven by the growing prevalence of heart disease and stroke, where CT imaging provides critical diagnostic insights.

USA Computed Tomography Market Competitive Landscape

The USA Computed Tomography Market is highly competitive, with leading manufacturers continually investing in technological advancements and expanding their product offerings. Major players include General Electric (GE) Healthcare, Siemens Healthineers, Canon Medical Systems, Philips Healthcare, and Hitachi Medical Systems. These companies are focusing on developing AI-powered imaging platforms, improving scanner efficiency, and reducing radiation exposure to enhance patient outcomes and maintain market leadership.

|

Company Name |

Establishment Year |

Headquarters |

No. of Employees |

Revenue (USD) |

Key Products |

Sustainability Initiatives |

Geographical Reach |

Technology Adoption |

Partnerships |

|

GE Healthcare |

1892 |

Chicago, IL |

|||||||

|

Siemens Healthineers |

1847 |

Erlangen, Germany |

|||||||

|

Canon Medical Systems |

1937 |

Otawara, Japan |

|||||||

|

Philips Healthcare |

1891 |

Amsterdam, NL |

|||||||

|

Hitachi Medical Systems |

1910 |

Tokyo, Japan |

USA Computed Tomography Industry Analysis

Growth Drivers

- Growing Prevalence of Chronic Diseases: The increasing incidence of chronic diseases such as cancer and cardiovascular disorders is driving the demand for computed tomography (CT) in the USA. According to the National Cancer Institute, over 2 million new cancer cases are expected in 2024, necessitating more diagnostic imaging services, including CT scans, for early detection. Cardiovascular diseases also remain a leading cause of mortality, with the CDC reporting 680,000 deaths in 2023, further expanding the demand for CT diagnostics in treatment planning and follow-up care.

- Technological Advancements in CT Scanners: Technological advancements in CT scanners, including AI-powered analytics and low-dose radiation techniques, are revolutionizing diagnostics. In 2024, manufacturers have introduced AI-enhanced CT scanners that reduce radiation exposure while enhancing imaging precision, benefiting healthcare providers concerned with radiation safety. AI also accelerates diagnostic workflows by automating data analysis. The FDA's clearance of AI-assisted CT systems in 2023, which streamline complex imaging processes, has increased adoption in hospitals. This shift toward technology-driven solutions is aimed at improving diagnostic accuracy and reducing patient radiation exposure.

- Expanding Geriatric Population: The growing geriatric population in the USA is a significant driver for the CT market, with an increased need for diagnostic imaging among older adults. As of 2024, 59 million Americans are aged 65 or older, according to the U.S. Census Bureau, and this group is more likely to suffer from age-related diseases like osteoporosis, cancers, and cardiovascular conditions. This trend necessitates more frequent use of CT imaging for timely diagnosis, early treatment, and disease monitoring, especially in the context of complex health conditions associated with aging.

Market Challenges

- High Costs of CT Equipment and Maintenance: High equipment and maintenance costs continue to challenge the widespread adoption of advanced CT scanners in the USA. Smaller healthcare facilities often face financial barriers in acquiring the latest diagnostic equipment, limiting access to cutting-edge imaging technologies. This financial burden impacts the overall growth of the CT market, as hospitals and clinics are required to allocate significant resources for purchasing and maintaining equipment. The high upfront costs of advanced multi-slice CT scanners, coupled with ongoing maintenance expenses, make it difficult for smaller institutions to keep pace with technological advancements in diagnostic imaging.

- Regulatory Compliance and Safety Concerns: Stringent FDA regulations governing radiation exposure are another challenge in the U.S. CT market. The FDAs regulations on medical imaging devices ensure patient safety by limiting radiation doses. As of 2024, the FDA has maintained its guidance under the Initiative to Reduce Unnecessary Radiation Exposure from Medical Imaging, emphasizing dose optimization for CT procedures. Although these guidelines protect patients, they require manufacturers and hospitals to invest heavily in equipment that adheres to low-dose standards, potentially increasing operational costs for healthcare providers.

USA Computed Tomography Market Future Outlook

The USA Computed Tomography Market is expected to grow steadily over the next five years, driven by advancements in imaging technology, increased healthcare spending, and the rising prevalence of chronic diseases. The adoption of AI and machine learning in imaging analysis will enhance diagnostic accuracy, while the integration of telemedicine and mobile imaging units will expand access to CT services across underserved regions.

Future Market Opportunities

- Integration with Telemedicine and Mobile Imaging: The growing integration of CT technology with telemedicine and mobile imaging solutions presents a key opportunity for market expansion. Mobile CT units are increasingly deployed in remote and underserved areas, providing essential diagnostic services to populations without easy access to hospitals. In 2024, the U.S. Department of Health and Human Services has expanded its support for telemedicine initiatives, increasing funding for mobile diagnostic units across rural America. These mobile units, combined with telemedicine platforms, allow for real-time imaging diagnostics, bridging gaps in healthcare access.

- Expansion of AI-Powered Diagnostic Solutions: The expansion of AI-powered diagnostic solutions offers significant growth potential for the CT market. AI tools integrated with CT imaging can enhance diagnostic precision and reduce interpretation times. In 2024, healthcare facilities will increasingly adopt AI-enhanced systems to streamline workflows and improve diagnostic accuracy, particularly in detecting complex conditions like cancers and cardiovascular diseases. According to the FDA, several AI-driven CT applications received clearance in the past year, further supporting the trend toward automated imaging analysis and positioning the market for broader adoption of AI-based solutions

Scope of the Report

|

By Scanner |

Low-Slice CT Scanners Mid-Slice CT Scanners High-Slice CT Scanners Cone Beam CT Scanners |

|

By Application |

Oncology Neurology Cardiology Musculoskeletal Others |

|

By Technology |

Hospitals Diagnostic Imaging Centers Ambulatory Care Centers |

|

By End-User |

Hospitals Diagnostic Laboratories Research Institutions |

|

By Region |

North-East Midwest West Coast Southern |

Products

Key Target Audience

Hospitals and Diagnostic Centers

CT Scanner Manufacturers

Medical Device Distributors

Banks and Financial Institutes

Healthcare Providers

Government and Regulatory Bodies (FDA, CMS)

Investors and Venture Capitalist Firms

Telemedicine Providers

Health Insurance Providers

Banks and Financial Institutions

Companies

Major Players Mentioned in the Report

General Electric (GE) Healthcare

Siemens Healthineers

Canon Medical Systems

Philips Healthcare

Hitachi Medical Systems

Fujifilm Holdings

Medtronic Plc

Carestream Health

Samsung NeuroLogica

Neusoft Medical Systems

United Imaging Healthcare

Konica Minolta Healthcare

Shimadzu Corporation

Varian Medical Systems

Esaote SpA

Table of Contents

01 USA Computed Tomography Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

02 USA Computed Tomography Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

03 USA Computed Tomography Market Analysis

3.1. Growth Drivers (Market-specific parameters like increasing chronic diseases, advancements in imaging technologies, rise in AI-powered diagnostics)

3.1.1. Growing Prevalence of Chronic Diseases (Cancer, Cardiovascular diseases)

3.1.2. Technological Advancements in CT Scanners (AI-powered, low-dose radiation)

3.1.3. Expanding Geriatric Population (Aging population requiring diagnostic imaging)

3.1.4. Rising Demand for Early Diagnostics (Minimally invasive diagnostics, personalized medicine)

3.2. Market Challenges (Regulatory scrutiny, high equipment costs, radiation safety concerns)

3.2.1. High Equipment and Maintenance Costs

3.2.2. Stringent FDA Regulations on Radiation Exposure

3.2.3. Skilled Workforce Shortage in Advanced CT Imaging

3.3. Opportunities (Telemedicine integration, mobile CT units, AI-based analytics)

3.3.1. Integration with Telemedicine and Mobile Imaging

3.3.2. Expansion of AI-Powered Diagnostic Solutions

3.3.3. Growth in Portable and Mobile CT Scanners

3.4. Trends (AI integration, multi-energy CT imaging, personalized diagnostics)

3.4.1. Increasing Adoption of AI in CT Imaging

3.4.2. Multi-Energy and Spectral Imaging Advancements

3.4.3. Increased Focus on Personalized Diagnostic Solutions

3.5. Government Regulation (FDA standards, radiation exposure limits, healthcare policy)

3.5.1. FDAs Regulation on Low-Dose Radiation Standards

3.5.2. Compliance with Health Information Technology for Economic and Clinical Health Act (HITECH)

3.5.3. Federal Incentives for Adoption of Advanced Imaging Technologies

3.6. SWOT Analysis (Market-specific factors)

3.7. Stake Ecosystem (Diagnostic imaging centers, hospitals, research institutions)

3.8. Porters Five Forces (Competition intensity, threat of new entrants, bargaining power)

3.9. Competition Ecosystem (Product offerings, partnerships, market share)

04 USA Computed Tomography Market Segmentation

4.1. By Scanner Type (In Value %)

4.1.1. Low-Slice CT Scanners

4.1.2. Mid-Slice CT Scanners

4.1.3. High-Slice CT Scanners

4.1.4. Cone Beam CT Scanners

4.2. By Application (In Value %)

4.2.1. Oncology

4.2.2. Neurology

4.2.3. Cardiology

4.2.4. Musculoskeletal

4.2.5. Others

4.3. By Technology (In Value %)

4.3.1. Conventional CT

4.3.2. Dual-Energy CT

4.3.3. Spectral CT

4.4. By End-User (In Value %)

4.4.1. Hospitals

4.4.2. Diagnostic Imaging Centers

4.4.3. Ambulatory Care Centers

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

05 USA Computed Tomography Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. General Electric (GE) Healthcare

5.1.2. Siemens Healthineers

5.1.3. Canon Medical Systems

5.1.4. Philips Healthcare

5.1.5. Hitachi Medical Systems

5.1.6. Fujifilm Holdings

5.1.7. Carestream Health

5.1.8. Medtronic Plc

5.1.9. Samsung NeuroLogica

5.1.10. Neusoft Medical Systems

5.1.11. United Imaging Healthcare

5.1.12. Konica Minolta Healthcare

5.1.13. Shimadzu Corporation

5.1.14. Esaote SpA

5.1.15. Varian Medical Systems

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Technology Adoption, Product Differentiation, Market Share, AI Integration, Strategic Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Product launches, expansions, partnerships)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7 Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

06 USA Computed Tomography Market Regulatory Framework

6.1. FDA Guidelines on CT Scanning Technology

6.2. Compliance with Radiation Safety Standards

6.3. Certification and Accreditation Processes for CT Systems

07 USA Computed Tomography Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Technological advancements, AI integration, rising chronic disease incidence)

08 USA Computed Tomography Future Market Segmentation

8.1. By Scanner Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

09 USA Computed Tomography Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map that includes all major stakeholders in the USA Computed Tomography Market. This step is supported by comprehensive desk research, utilizing both secondary and proprietary databases to gather detailed industry-level data. The goal is to identify and define the key variables influencing the market's growth dynamics, such as technological advancements and regulatory standards.

Step 2: Market Analysis and Construction

This step focuses on compiling and analyzing historical data relevant to the USA Computed Tomography Market. Key data points include the adoption rates of CT scanners, revenue generation from diagnostic centers, and technological advancements in the sector. Market penetration levels, service provider ratios, and CT scan utilization rates are assessed to ensure the accuracy and reliability of the market size and growth estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through interviews with industry experts, including representatives from hospitals, diagnostic centers, and medical device manufacturers. These consultations provide valuable insights into market trends, operational challenges, and the competitive landscape, helping refine and corroborate the market data collected through desk research.

Step 4: Research Synthesis and Final Output

In the final phase, detailed insights are gathered directly from CT scanner manufacturers and healthcare providers to verify the statistics obtained through the bottom-up approach. This engagement ensures that the data is comprehensive, accurate, and validated, providing a clear understanding of the market landscape and growth potential.

Frequently Asked Questions

01. How big is the USA Computed Tomography Market?

The USA Computed Tomography market is valued at USD 4.5 billion, driven by the increasing demand for advanced diagnostic imaging technologies, especially in oncology and cardiology.

02. What are the challenges in the USA Computed Tomography Market?

Challenges in the USA Computed Tomography Market include the high costs of CT scanners and regulatory scrutiny over radiation safety standards. Compliance with stringent FDA regulations and the ongoing need for skilled personnel also pose significant hurdles for market participants.

03. Who are the major players in the USA Computed Tomography Market?

Key players in the USA Computed Tomography Market include General Electric (GE) Healthcare, Siemens Healthineers, Canon Medical Systems, Philips Healthcare, and Hitachi Medical Systems, all of which lead the market through technological advancements and strategic partnerships.

04. What are the growth drivers of the USA Computed Tomography Market?

Growth drivers in the USA Computed Tomography Market include technological advancements, increasing prevalence of chronic diseases, the rising demand for early diagnostics, and the integration of AI in CT systems.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.