USA Data Acquisition Market Outlook to 2030

Region:North America

Author(s):Sanjna

Product Code:KROD11219

November 2024

89

About the Report

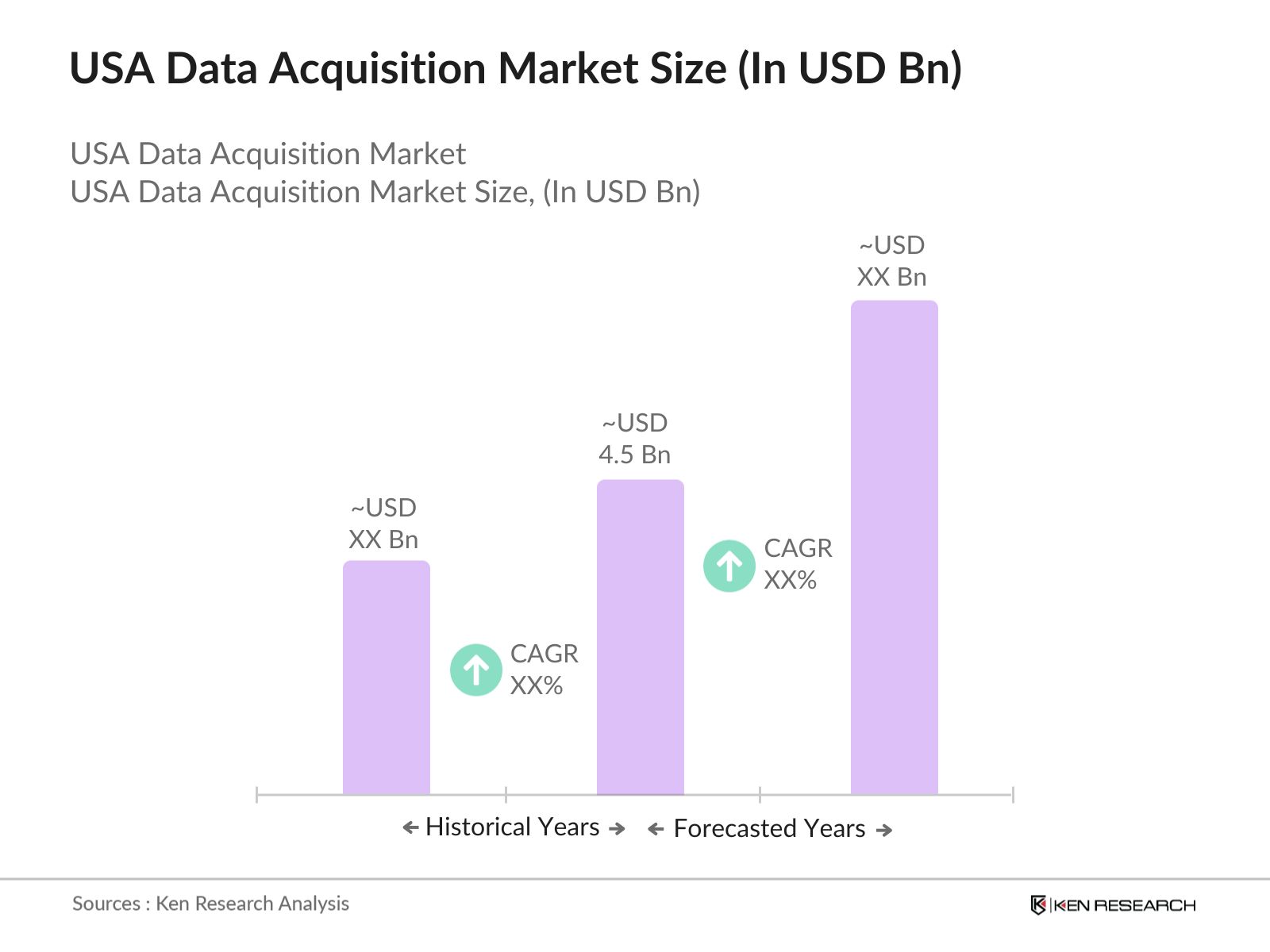

USA Data Acquisition Market Overview

- The USA Data Acquisition market is valued at USD 4.5 billion, primarily driven by increased adoption across industries seeking real-time analytics for operational efficiency. The rise of Industry 4.0 and the integration of IoT in manufacturing, healthcare, and automotive sectors have spurred demand, alongside heightened needs for data-driven decision-making. This markets momentum reflects substantial investments in advanced analytics and digital transformation across key verticals.

- The market is dominated by tech-centric cities such as San Francisco, New York, and Austin due to their robust technological infrastructure, concentration of tech firms, and supportive policy frameworks for innovation. These urban areas attract major players and foster collaborative environments, encouraging the development of data acquisition solutions to meet specific regional demands in technology and manufacturing.

- Environmental compliance regulations have increased, with the Environmental Protection Agency reporting a 30% rise in regulatory checks for technology firms in 2023. Data acquisition systems in sectors like manufacturing must adhere to these regulations to minimize environmental impact, encouraging firms to adopt systems with lower carbon footprints.

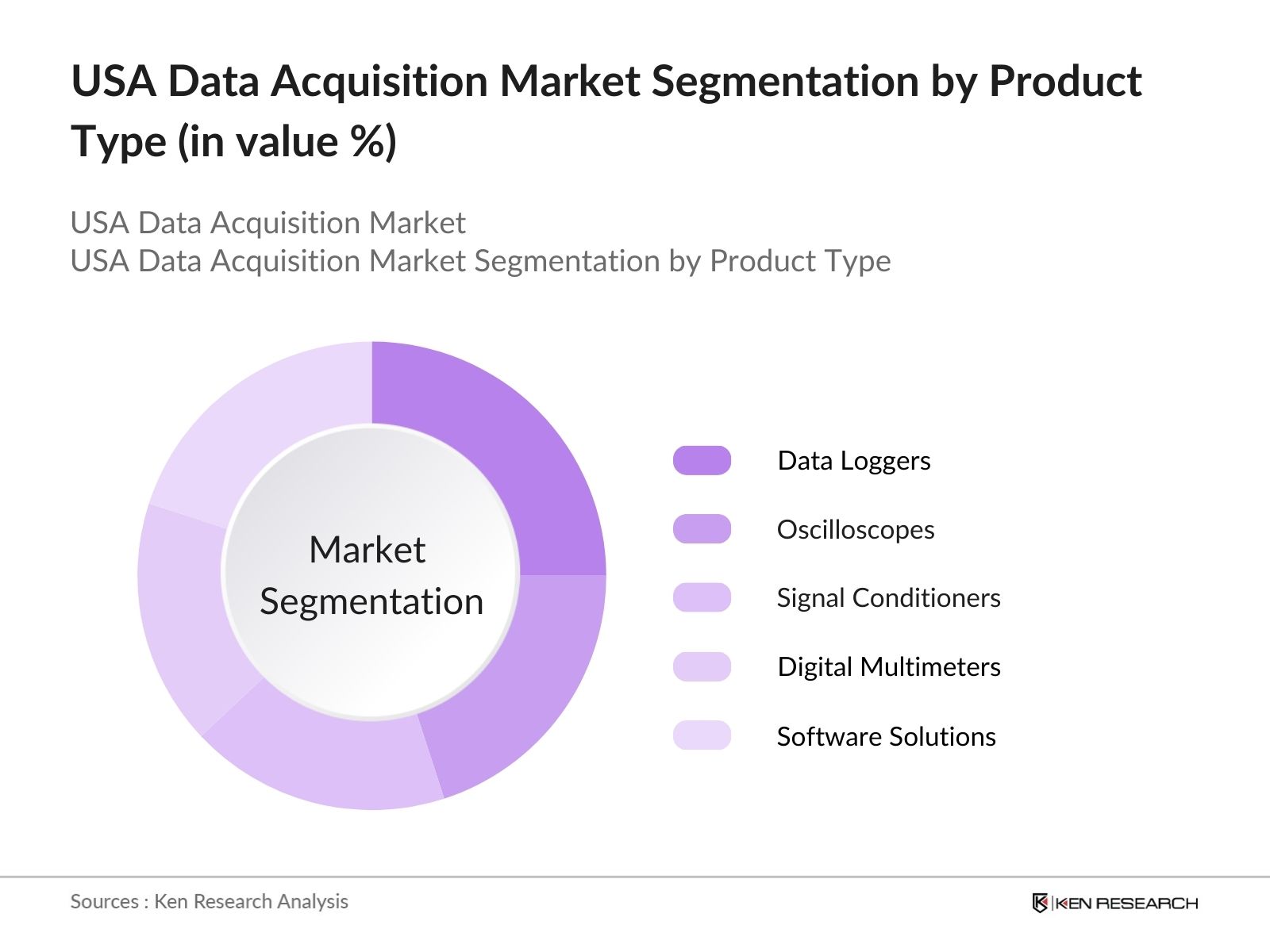

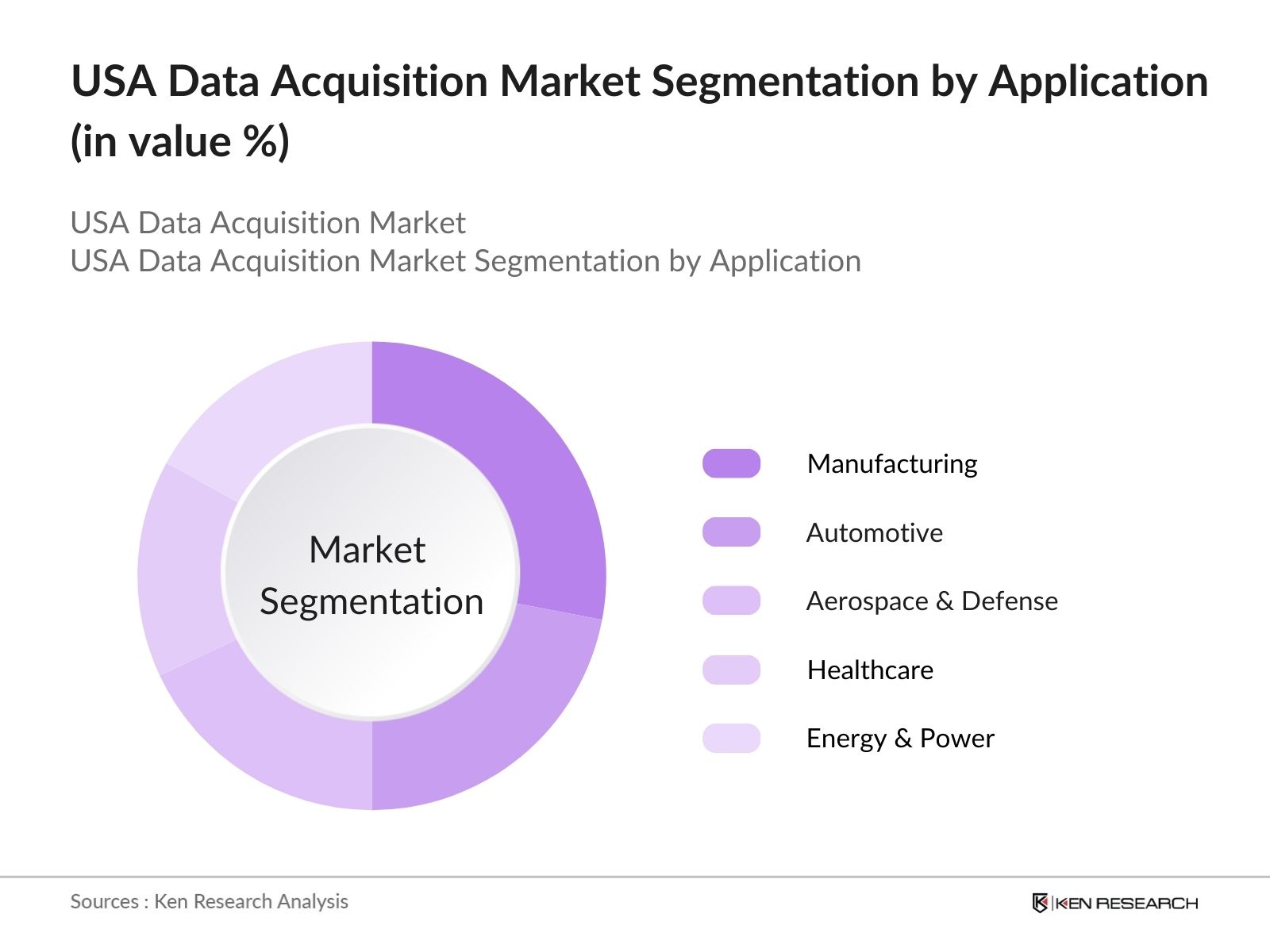

USA Data Acquisition Market Segmentation

By Product Type: The USA Data Acquisition market is segmented by product type into data loggers, oscilloscopes, signal conditioners, digital multimeters, and software solutions. Data loggers hold a dominant market share under this segmentation due to their adaptability in capturing and monitoring data across various environments, enhancing operational efficiencies in industrial applications. Their popularity is amplified by industries like energy and automotive, which rely on precise data capture for maintenance and real-time monitoring.

By Application: The USA Data Acquisition market is segmented by application into manufacturing, automotive, aerospace & defense, healthcare, and energy & power. Manufacturing applications lead the segment, driven by the demand for real-time monitoring, process optimization, and stringent quality control standards. This dominance is bolstered by investments in smart manufacturing initiatives, which prioritize data-driven solutions to optimize production and improve productivity across diverse manufacturing setups.

USA Data Acquisition Market Competitive Landscape

The USA Data Acquisition market is dominated by leading players that leverage their technological capabilities and extensive distribution networks. Key companies include National Instruments, Keysight Technologies, and Schneider Electric, reflecting the market's focus on innovation and reliability in data acquisition.

USA Data Acquisition Market Analysis

Growth Drivers

- Technological Innovation: The USA Data Acquisition Market has seen significant advancements due to technological innovations. The National Institute of Standards and Technology (NIST) reported a growth in technological R&D, with federal spending on technology-focused research increasing by $125 billion in 2024. This funding fosters developments in data acquisition technology, enabling real-time analytics and improved data accuracy. Furthermore, over 1,800 patents related to data acquisition were filed in 2023, underscoring the focus on improving hardware and software efficiencies for data handling in various sectors, including manufacturing and healthcare.

- Cloud Integration: Cloud integration has accelerated in the data acquisition market, with approximately 60% of U.S. enterprises adopting cloud-based data solutions by 2023, as reported by the U.S. Department of Commerce. Cloud integration allows companies to access data remotely, increasing operational flexibility. In 2024, investments in cloud infrastructure reached $130 billion, enabling scalable data acquisition solutions essential for industries like finance and retail that require fast, reliable data processing for real-time insights.

- Edge Computing: Edge computing has become a crucial driver, with the market reaching an estimated 2 billion edge-connected devices in 2023, according to the U.S. Department of Energy. The increase in edge computing adoption is driven by the need for real-time data processing near the data source, reducing latency and improving response times. As of 2024, around 55% of data acquisition devices incorporate edge computing capabilities, which are essential for applications in manufacturing and autonomous systems.

Challenges

- High Initial Cost: High initial costs are a significant barrier, with the average cost of data acquisition systems ranging from $100,000 to $500,000 for mid-sized operations, as noted by the U.S. Department of Commerce. Smaller businesses often find these costs prohibitive, limiting widespread adoption. In 2024, only 40% of SMEs considered investing in data acquisition due to budget constraints, impacting the overall market growth.

- Complexity in Integration: The complexity involved in integrating new data acquisition systems with existing IT infrastructure is a challenge for many industries. The U.S. Bureau of Economic Analysis reports that in 2023, 60% of firms faced operational delays due to integration challenges, which often require specialized personnel and time-intensive processes. Such integration issues hinder the seamless adoption of data acquisition systems across industries, affecting deployment timelines and market growth.

USA Data Acquisition Market Future Outlook

USA Data Acquisition Market is anticipated to grow significantly due to advancements in data management technologies, the increasing prevalence of IoT in industrial sectors, and a strong emphasis on real-time data-driven decision-making. This growth is likely to be fueled by strategic partnerships between tech firms and manufacturing companies, along with an upsurge in government-supported digital infrastructure projects.

Market Opportunities

- 5G Deployment: The deployment of 5G across the U.S., which covered 75% of the population by 2023, as per the Federal Communications Commission (FCC), enhances data acquisition capabilities. The increased bandwidth and reduced latency facilitate real-time data processing, critical for applications in autonomous vehicles, manufacturing, and healthcare. The expansion of 5G networks is projected to create opportunities for high-speed data acquisition in previously underserved sectors.

- Automation in Industrial Processes: Industrial automation, supported by investments totaling $1.2 trillion in 2023, according to the U.S. Department of Energy, is driving demand for advanced data acquisition systems. Automation enables industries like manufacturing to monitor, control, and optimize operations in real-time. Data acquisition systems play a pivotal role in collecting and analyzing data to support automated decision-making, leading to increased efficiency and reduced operational costs.

Scope of the Report

|

Segment |

Sub-Segments |

|

Product Type |

Data Loggers Oscilloscopes Signal Conditioners Digital Multimeters Software Solutions |

|

Application |

Manufacturing Automotive Aerospace & Defense Healthcare Energy & Power |

|

End-User Industry |

Industrial Automation Telecom & IT Research & Academia Transportation Construction |

|

Technology |

Wired Data Acquisition Wireless Data Acquisition Portable Data Acquisition |

|

Data Type |

Analog Data Acquisition Digital Data Acquisition |

Products

Key Target Audience

Technology and Software Development Companies

Manufacturing and Industrial Firms

Healthcare Equipment Manufacturers

Aerospace & Defense Contractors

Automotive Industry Suppliers

Energy & Power Utilities

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., National Institute of Standards and Technology)

Companies

Players Mentioned in the Report

National Instruments

Keysight Technologies

Siemens AG

Honeywell International

Schneider Electric

Yokogawa Electric Corporation

Rockwell Automation

Advantech Co., Ltd.

HBM Test and Measurement

General Electric

Table of Contents

1. USA Data Acquisition Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. USA Data Acquisition Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. USA Data Acquisition Market Analysis

3.1. Growth Drivers

3.1.1. Technological Innovation

3.1.2. Data-Driven Decision-Making

3.1.3. Cloud Integration

3.1.4. Edge Computing

3.1.5. IoT Integration

3.1.6. Increased R&D

3.1.7. Industry-Specific Customization

3.2. Market Challenges

3.2.1. High Initial Cost

3.2.2. Complexity in Integration

3.2.3. Data Security Concerns

3.2.4. Legacy System Compatibility

3.3. Opportunities

3.3.1. 5G Deployment

3.3.2. Automation in Industrial Processes

3.3.3. Smart City Initiatives

3.3.4. Real-Time Data Processing

3.3.5. Advanced Analytics Capabilities

3.4. Trends

3.4.1. Modular Data Acquisition Systems

3.4.2. AI and Machine Learning Integration

3.4.3. Expansion in Renewable Energy Sector

3.4.4. Industrial IoT Adoption

3.5. Regulatory Environment

3.5.1. Data Privacy Standards

3.5.2. Environmental Compliance

3.5.3. Industry-Specific Standards

3.5.4. Cybersecurity Regulations

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competitive Landscape

4. USA Data Acquisition Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Data Loggers

4.1.2. Oscilloscopes

4.1.3. Signal Conditioners

4.1.4. Digital Multimeters

4.1.5. Software Solutions

4.2. By Application (In Value %)

4.2.1. Manufacturing

4.2.2. Automotive

4.2.3. Aerospace and Defense

4.2.4. Healthcare

4.2.5. Energy & Power

4.3. By End-User Industry (In Value %)

4.3.1. Industrial Automation

4.3.2. Telecom & IT

4.3.3. Research & Academia

4.3.4. Transportation

4.3.5. Construction

4.4. By Technology (In Value %)

4.4.1. Wired Data Acquisition Systems

4.4.2. Wireless Data Acquisition Systems

4.4.3. Portable Data Acquisition Systems

4.5. By Data Type (In Value %)

4.5.1. Analog Data Acquisition

4.5.2. Digital Data Acquisition

5. USA Data Acquisition Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. National Instruments

5.1.2. Keysight Technologies

5.1.3. Siemens AG

5.1.4. Honeywell International Inc.

5.1.5. Yokogawa Electric Corporation

5.1.6. Schneider Electric

5.1.7. General Electric

5.1.8. Rockwell Automation

5.1.9. Advantech Co., Ltd.

5.1.10. HBM Test and Measurement

5.2. Cross Comparison Parameters (Annual Revenue, Market Presence, Employee Count, Data Types Supported, Technological Innovations, R&D Investment, Product Portfolio Breadth, Customer Base Size)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Private Equity and Venture Funding

6. USA Data Acquisition Market Regulatory Framework

6.1. Compliance Standards (ISO 9001, NIST, IEC, GDPR)

6.2. Certification Requirements

6.3. Industry-Specific Regulations

7. USA Data Acquisition Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Data Acquisition Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-User Industry (In Value %)

8.4. By Technology (In Value %)

8.5. By Data Type (In Value %)

9. USA Data Acquisition Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Target Customer Analysis

9.3. Go-to-Market Strategy

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

An extensive map of the data acquisition markets ecosystem was constructed, highlighting stakeholders across various applications. The identification of variables focused on gathering information on technological advancements, regional adoption rates, and industry-specific data requirements.

Step 2: Market Analysis and Construction

Comprehensive analysis involved historical data gathering from industry reports and proprietary databases, emphasizing market penetration and product performance metrics. This step provided a structured assessment of product and application-level revenue generation.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses on market drivers and challenges were validated through interviews with experts across multiple sectors, including healthcare and automotive. These insights helped refine and support the market estimations with operational data.

Step 4: Research Synthesis and Final Output

Data acquisition firms and end-user feedback were collected to validate the compiled statistics. This interaction enabled a balanced approach to the final report synthesis, ensuring accuracy and comprehensiveness of the USA Data Acquisition Market analysis.

Frequently Asked Questions

1. big is the USA Data Acquisition Market?

The USA Data Acquisition market was valued at USD 4.5 billion, driven by the rise of Industry 4.0, digital transformation, and growing demand for real-time data monitoring across key industries.

2. What are the major challenges in the USA Data Acquisition Market?

Key challenges in USA Data Acquisition market include high initial investment costs, data security concerns, and the complexities of integrating advanced data acquisition solutions into legacy systems across various industries.

3. Who are the prominent players in the USA Data Acquisition Market?

Major players in USA Data Acquisition market include National Instruments, Keysight Technologies, Siemens AG, Honeywell International, and Schneider Electric, each distinguished by their innovation capabilities and strong market presence.

4. What factors are driving the growth of the USA Data Acquisition Market?

Growth in USA Data Acquisition market is propelled by the increasing need for operational efficiency, advancements in IoT and cloud integration, and the adoption of data acquisition technologies across healthcare, automotive, and manufacturing sectors.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.