USA Data Center Market Outlook to 2030

Region:North America

Author(s):Meenakshi Bisht

Product Code:KROD9980

Region:North America

Author(s):Meenakshi Bisht

Product Code:KROD9980

December 2024

94

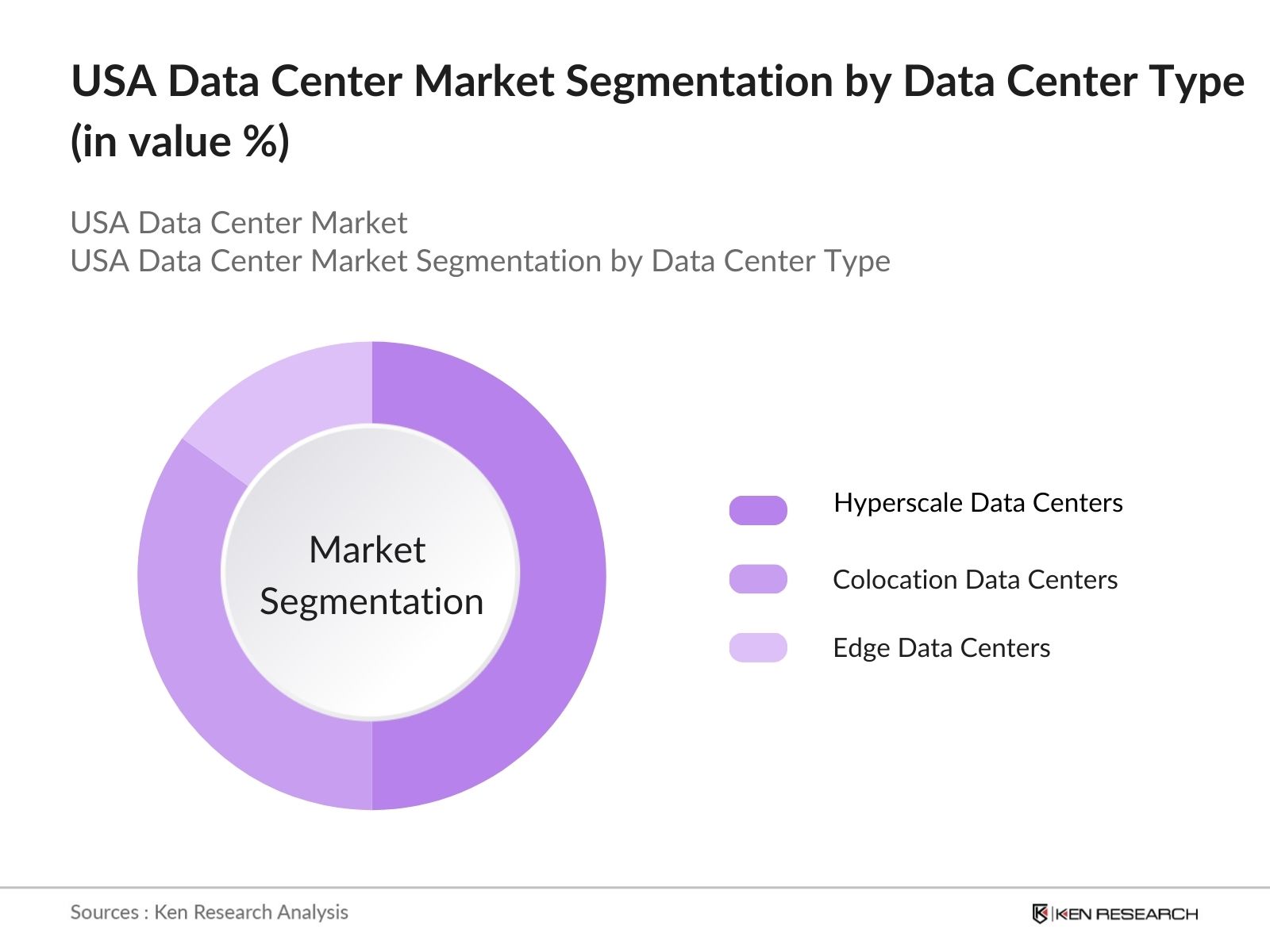

By Data Center Type: The market is segmented by type into colocation data centers, hyperscale data centers, and edge data centers. Recently, hyperscale data centers have gained a dominant market share due to the large-scale operations of companies like Amazon Web Services, Microsoft Azure, and Google Cloud. These companies continue to invest heavily in expanding their data center infrastructure to meet the growing demand for cloud services, leading to hyperscale data centers playing a crucial role in the market. The scalability, reliability, and cost-efficiency offered by hyperscale data centers make them a preferred choice for enterprises across industries.

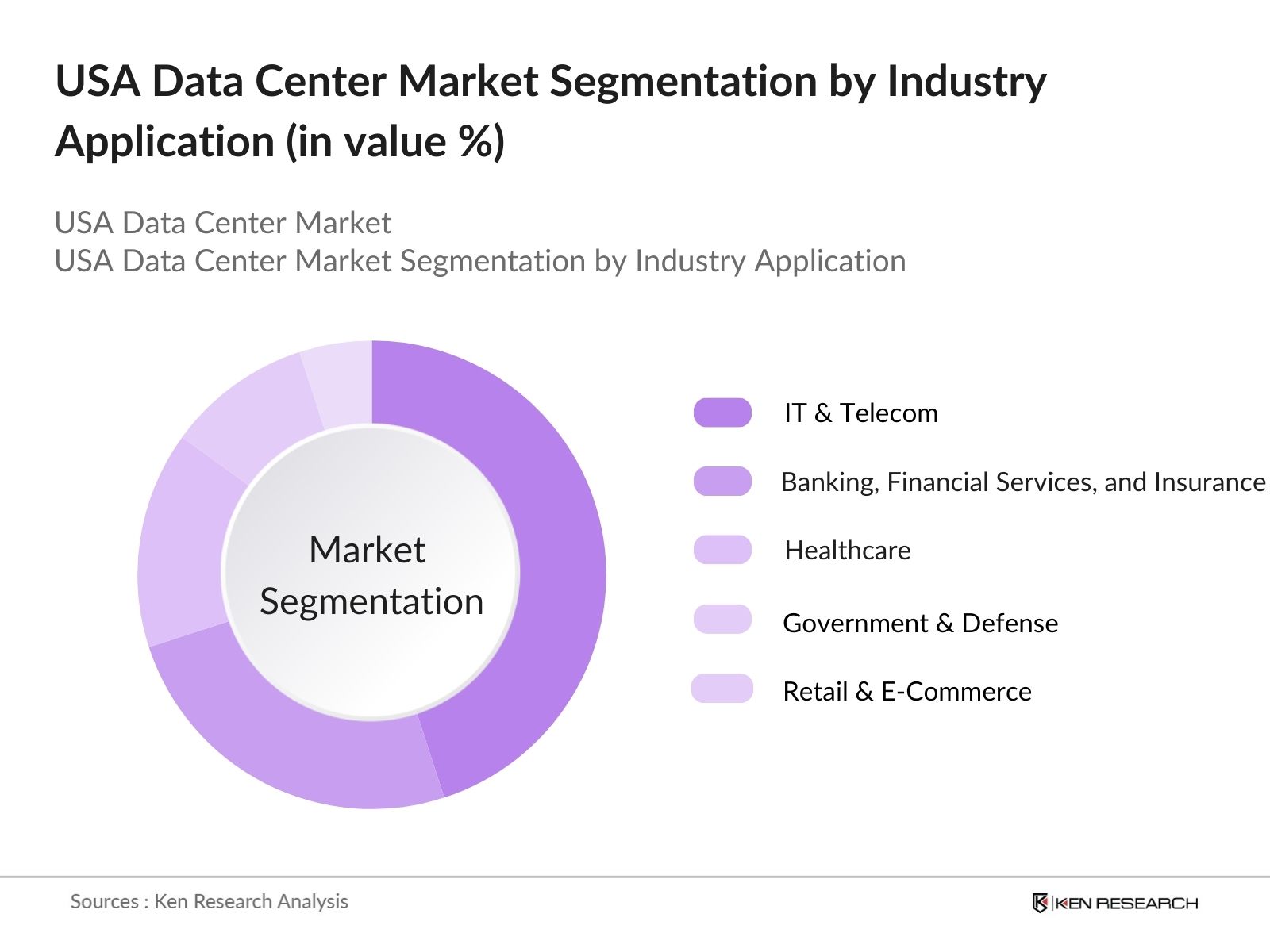

By Industry Application: The market is segmented by industry applications into IT & telecom, banking, financial services and insurance (BFSI), healthcare, government & defense, and retail & e-commerce. Among these, IT & telecom holds the largest market share due to the increasing adoption of cloud services, big data, and machine learning technologies. As companies within the IT sector rely heavily on data-driven operations, the demand for robust data center infrastructure has surged. The telecom sectors shift towards 5G also supports the need for advanced data center capabilities to handle high bandwidth and low-latency requirements.

The USA data center market is dominated by a mix of major global players and regional operators. The competitive landscape is shaped by ongoing investments in data center infrastructure and innovations in energy efficiency and sustainability. Companies are continually focusing on building hyperscale facilities and integrating renewable energy sources to meet increasing demand and sustainability regulations.

The USA data center market is expected to experience significant growth over the next five years, driven by advancements in AI, IoT, and 5G technologies. With increasing digital transformation across industries, the demand for data storage and processing capabilities is projected to rise exponentially. Moreover, government incentives for sustainable data center operations and tax breaks for companies investing in energy-efficient technologies will further boost the expansion of data center infrastructure across the country.

|

By Type |

Colocation Data Centers Hyperscale Data Centers Edge Data Centers |

|

By Application |

IT & Telecom Banking, Financial Services, and Insurance (BFSI) Government & Defense Healthcare Retail & E-Commerce |

|

By Component |

IT Equipment Power Solutions Cooling Systems Networking Equipment |

|

By Infrastructure Type |

Electrical Infrastructure Mechanical Infrastructure General Construction |

|

By Region |

Midwest Northeast West Coast Southeast Southwest |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Growth in demand for hyperscale data centers, cloud computing adoption, sustainability standards)

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Developments in data center cooling, energy efficiency regulations, power consumption trends)

3.1. Growth Drivers

3.1.1. Increased Demand for Cloud Services

3.1.2. Growth of Edge Computing

3.1.3. Rising Investments in 5G and IoT

3.1.4. Focus on Green Data Centers (Environmental sustainability, carbon-neutral strategies)

3.2. Market Challenges

3.2.1. High Energy Costs

3.2.2. Scalability and Latency Concerns

3.2.3. Regulatory Compliance (Data privacy, energy regulations)

3.3. Opportunities

3.3.1. Adoption of AI and Machine Learning in Data Centers

3.3.2. Development of Modular Data Centers

3.3.3. Government Incentives for Data Center Infrastructure Development (Tax breaks, energy-efficient certification programs)

3.4. Trends

3.4.1. Use of Liquid Cooling Systems

3.4.2. Integration of Renewable Energy in Data Center Operations

3.4.3. Deployment of Micro Data Centers in Remote Areas

3.5. Government Regulations

3.5.1. Federal Data Center Consolidation Initiative (FDCCI)

3.5.2. State-Level Data Center Tax Incentives

3.5.3. Data Security and Compliance Standards (e.g., GDPR, HIPAA, CCPA)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Collaboration between data center operators, cloud service providers, hardware suppliers)

3.8. Porters Five Forces

3.9. Competition Ecosystem (Data center colocation, managed services)

4.1. By Type (In Value %)

4.1.1. Colocation Data Centers

4.1.2. Hyperscale Data Centers

4.1.3. Edge Data Centers

4.2. By Application (In Value %)

4.2.1. IT & Telecom

4.2.2. Banking, Financial Services, and Insurance (BFSI)

4.2.3. Government & Defense

4.2.4. Healthcare

4.2.5. Retail & E-Commerce

4.3. By Component (In Value %)

4.3.1. IT Equipment

4.3.2. Power Solutions

4.3.3. Cooling Systems

4.3.4. Networking Equipment

4.4. By Infrastructure Type (In Value %)

4.4.1. Electrical Infrastructure

4.4.2. Mechanical Infrastructure

4.4.3. General Construction

4.5. By Region (In Value %)

4.5.1. Midwest

4.5.2. Northeast

4.5.3. West Coast

4.5.4. Southeast

4.5.5. Southwest

5.1. Detailed Profiles of Major Companies

5.1.1. Equinix, Inc.

5.1.2. Digital Realty Trust, Inc.

5.1.3. CyrusOne Inc.

5.1.4. CoreSite Realty Corporation

5.1.5. NTT Communications Corporation

5.1.6. Iron Mountain Incorporated

5.1.7. Switch, Inc.

5.1.8. QTS Realty Trust

5.1.9. Flexential Corp.

5.1.10. Cyxtera Technologies

5.1.11. Amazon Web Services, Inc.

5.1.12. Microsoft Corporation (Azure)

5.1.13. Google LLC

5.1.14. AT&T Inc.

5.1.15. Verizon Communications Inc.

5.2. Cross Comparison Parameters

5.2.1. Data Center Footprint (Total Sq. Ft.)

5.2.2. Energy Efficiency (PUE Rating)

5.2.3. Total Number of Data Centers

5.2.4. Market Share (Colocation, Hyperscale)

5.2.5. Revenue (Data Center Services)

5.2.6. Number of Employees

5.2.7. Inception Year

5.2.8. HQ Location

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Energy Usage Regulations (Energy Star for Data Centers, LEED certifications)

6.2. Data Privacy Compliance (e.g., GDPR, HIPAA)

6.3. Data Center Certification Processes (Tier Certification from Uptime Institute)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Type (In Value %)

8.2. By Application (In Value %)

8.3. By Component (In Value %)

8.4. By Infrastructure Type (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThe initial step involved mapping all stakeholders within the USA data center market. A comprehensive ecosystem map was developed by leveraging industry-level information from proprietary databases and government reports to define the key variables influencing market trends and growth.

In this step, historical data from the USA data center market was collected and analyzed, focusing on market penetration, industry service providers, and revenue generation. A qualitative assessment was also conducted to gauge service quality and reliability.

Hypotheses regarding market drivers and barriers were formulated and validated through interviews with industry professionals, including data center operators and IT experts. These consultations provided real-time insights into market operations and technological adoption trends.

In the final phase, data from various primary and secondary sources was consolidated to form a detailed market report. This involved engaging with data center companies to verify insights on key segments and market trends, ensuring the accuracy and reliability of the report.

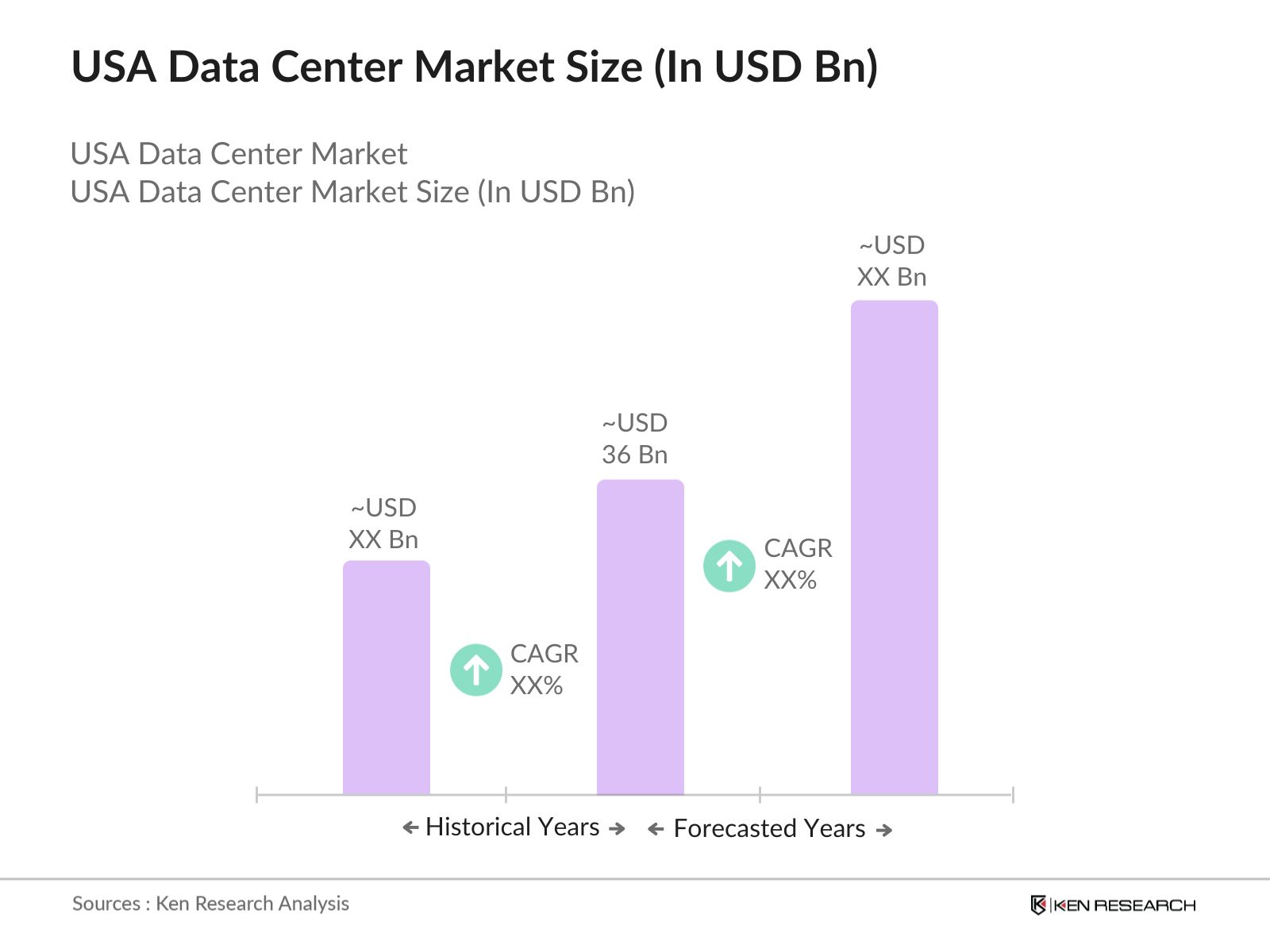

The USA data center market is valued at USD 36 billion, driven by the growing demand for cloud services, edge computing, and AI-powered applications.

The key challenges in USA data center market include high energy consumption, scalability issues, and the need to comply with strict regulatory requirements regarding data privacy and energy usage.

Key players in USA data center market include Equinix, Inc., Digital Realty Trust, Inc., CyrusOne Inc., CoreSite Realty Corporation, and NTT Communications Corporation.

The USA data center market growth is driven by increasing digital transformation, the expansion of cloud services, advancements in AI and IoT, and the deployment of 5G infrastructure.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.