USA Dynamic Random Access Memory (DRAM) Market Outlook to 2030

Region:United States

Author(s):Shreya Garg

Product Code:KROD4074

Region:United States

Author(s):Shreya Garg

Product Code:KROD4074

November 2024

90

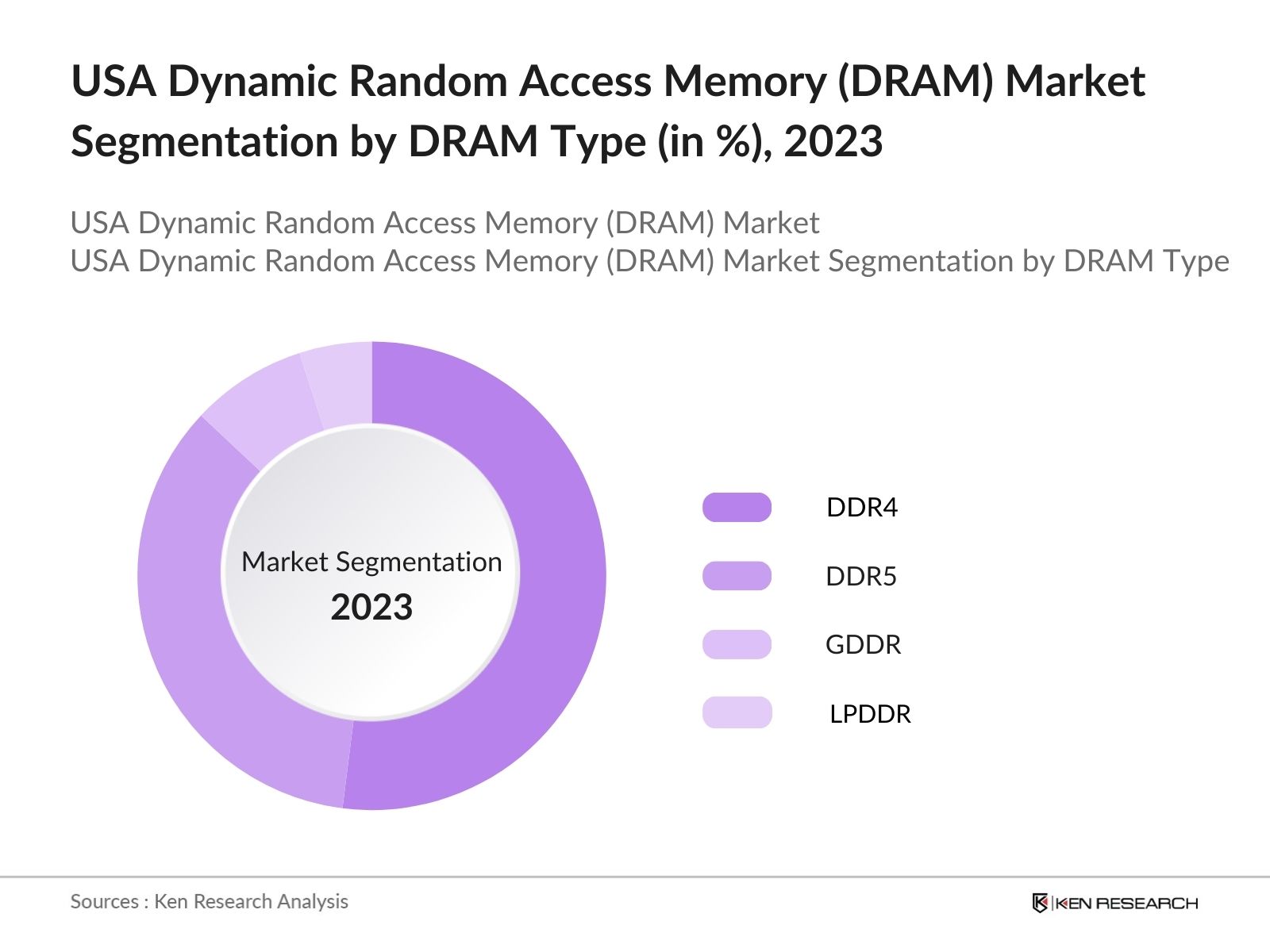

By DRAM Type: The market is segmented by product type into DDR4, DDR5, GDDR (Graphics DRAM), and LPDDR (Low Power DRAM). Recently, DDR4 has dominated the market due to its widespread usage in both consumer electronics and enterprise servers. Its versatility and cost-effectiveness have made it a staple in various industries, from cloud computing to smartphones. However, DDR5 is quickly catching up, driven by its superior performance and energy efficiency, which is increasingly critical for high-end computing applications, such as AI, machine learning, and big data analytics.

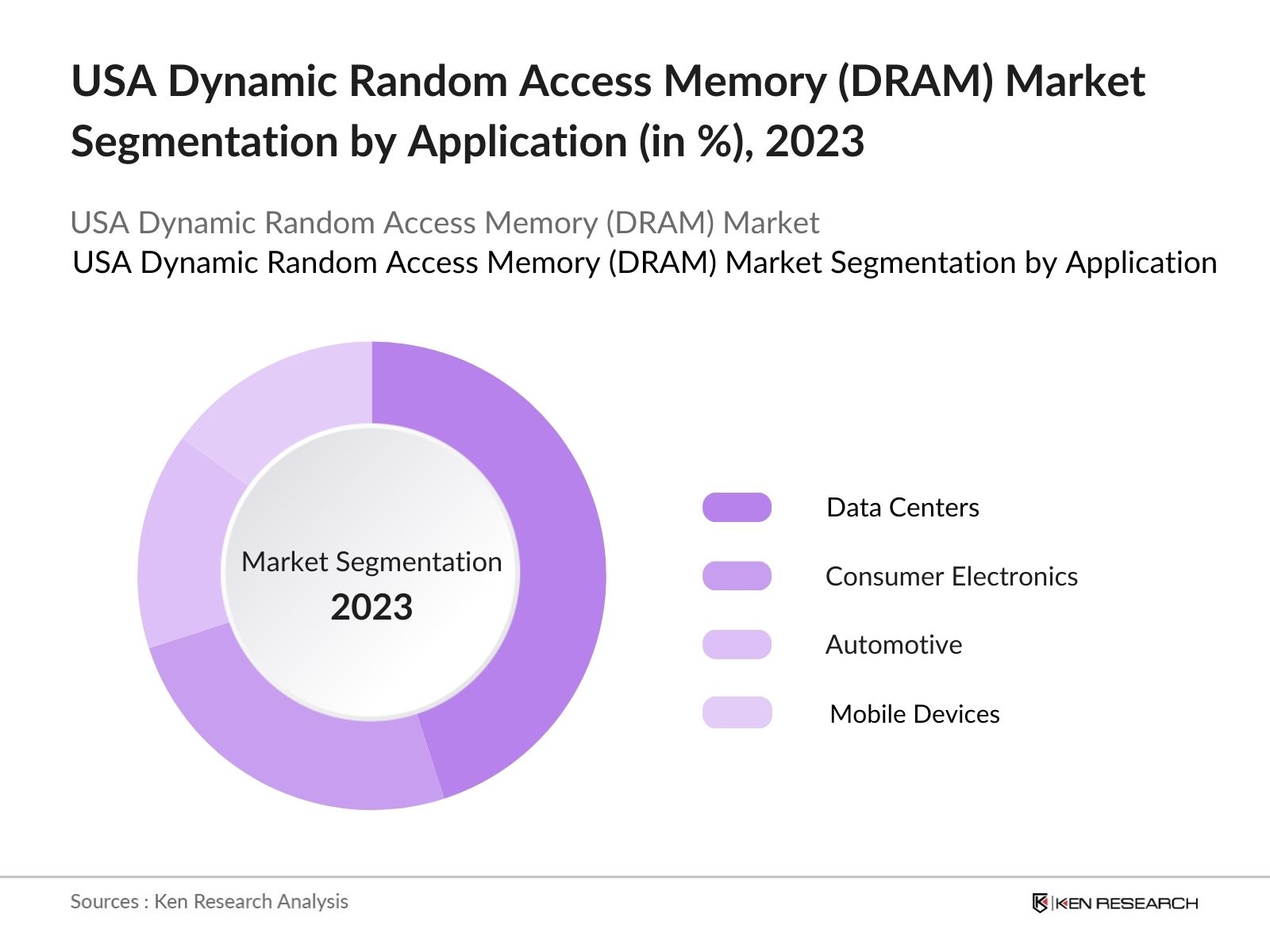

By Application: The market is also segmented by application into consumer electronics, data centers, automotive, and mobile devices. Data centers dominate the application segment due to the rapid expansion of cloud computing and the increased need for data storage and processing. DRAM is essential for providing fast access to large datasets, which is a key requirement for cloud service providers, enterprise IT environments, and AI systems. The rise in demand for faster and more efficient memory solutions in large-scale server farms has made this sub-segment the top consumer of DRAM.

By Application: The market is also segmented by application into consumer electronics, data centers, automotive, and mobile devices. Data centers dominate the application segment due to the rapid expansion of cloud computing and the increased need for data storage and processing. DRAM is essential for providing fast access to large datasets, which is a key requirement for cloud service providers, enterprise IT environments, and AI systems. The rise in demand for faster and more efficient memory solutions in large-scale server farms has made this sub-segment the top consumer of DRAM.

USA Dynamic Random Access Memory (DRAM) Market Competitive Landscape

USA Dynamic Random Access Memory (DRAM) Market Competitive LandscapeThe market is dominated by a few major players that maintain strong control over supply, innovation, and pricing. This consolidation is driven by heavy capital investment in research and development, advanced manufacturing capabilities, and long-term contracts with large-scale buyers like cloud service providers. Key players such as Micron and Intel continue to lead in innovation and market share, with others like Samsung and SK Hynix playing significant roles due to their global production capacity and technological prowess.

|

Company |

Established Year |

Headquarters |

R&D Investment (USD) |

Technology Node |

Production Capacity |

Patent Portfolio |

Employee Strength |

Revenue (USD) |

Global Rank |

|---|---|---|---|---|---|---|---|---|---|

|

Micron Technology |

1978 |

Boise, Idaho |

|||||||

|

SK Hynix |

1983 |

Icheon, South Korea |

|||||||

|

Samsung Electronics |

1969 |

Suwon, South Korea |

|||||||

|

Intel Corporation |

1968 |

Santa Clara, California |

|||||||

|

Nanya Technology |

1995 |

Taiwan |

Over the next five years, the USA DRAM market is expected to witness significant advancements, driven by rapid technological evolution in the semiconductor industry. The transition from DDR4 to DDR5 is expected to accelerate, offering increased speeds, bandwidth, and energy efficiency. Additionally, the rise of AI, 5G, and autonomous driving will drive demand for advanced DRAM products that can handle intensive data processing workloads. The government's emphasis on domestic semiconductor production through initiatives such as the CHIPS Act is also expected to boost local manufacturing capacity, making the USA a more competitive player in the global DRAM market.

|

By DRAM Type |

DDR4 DDR5 GDDR LPDDR |

|

By Application |

Consumer Electronics Data Centers Automotive Mobile Devices |

|

By End-User Industry |

Information Technology Telecom Healthcare Automotive |

|

By Technology Node |

14nm 10nm 7nm and Below |

|

By Region |

West Coast Southeast Midwest Northeast |

1.1. Definition and Scope

1.2. Market Taxonomy (DRAM Types, Use Cases)

1.3. Market Growth Rate (Market Drivers)

1.4. Market Segmentation Overview

2.1. Historical Market Size (In-Depth Growth Breakdown)

2.2. Year-On-Year Growth Analysis (Production Volume, Consumption)

2.3. Key Market Developments and Milestones (Technological Advancements, Manufacturing Trends)

3.1. Growth Drivers (Technological Shift, Data Center Expansion, AI & ML Integration)

3.1.1. Rise of Cloud Computing

3.1.2. Demand for High-Speed Processing

3.1.3. Government Policies Favoring Semiconductor Manufacturing

3.2. Market Challenges (Supply Chain Disruptions, High Production Costs, Global Semiconductor Shortage)

3.2.1. Raw Material Scarcity (Impact on Production)

3.2.2. Technical Complexities in Manufacturing Advanced DRAM (Scaling Issues, Technical Barriers)

3.2.3. Fluctuations in Pricing and Demand

3.3. Opportunities (AI, 5G, and Autonomous Vehicle Growth; Emerging Use Cases)

3.3.1. Expanding Edge Computing Applications

3.3.2. Rising Demand in Consumer Electronics and Mobile Devices

3.3.3. Strategic Collaborations and Joint Ventures in Memory Tech

3.4. Trends (Miniaturization, 3D DRAM, DDR5 Transition, Energy-Efficient DRAM)

3.4.1. Emergence of Next-Gen DRAM Technologies (DDR5, LPDDR5)

3.4.2. Increasing Adoption of DRAM in AI and ML Applications

3.4.3. Development of 3D Stacked DRAM for High-Density Applications

3.5. Government Regulation (US Chips Act, Semiconductor Subsidies, Tariffs on Imports)

3.5.1. Government Incentives for Local Semiconductor Production

3.5.2. Environmental and Safety Regulations in Semiconductor Manufacturing

3.5.3. Trade Policies Impacting DRAM Imports and Exports

4.1. By DRAM Type (In Value %)

4.1.1. DDR4

4.1.2. DDR5

4.1.3. GDDR (Graphics DRAM)

4.1.4. LPDDR (Low Power DRAM)

4.2. By Application (In Value %)

4.2.1. Consumer Electronics

4.2.2. Data Centers and Enterprise Servers

4.2.3. Automotive and Industrial Applications

4.2.4. Mobile Devices

4.3. By End-User Industry (In Value %)

4.3.1. Information Technology

4.3.2. Telecom

4.3.3. Healthcare

4.3.4. Automotive

4.4. By Technology Node (In Value %)

4.4.1. 14nm

4.4.2. 10nm

4.4.3. 7nm and Below

4.5. By Region (In Value %)

4.5.1. West Coast (Silicon Valley, Tech Giants' DRAM Demand)

4.5.2. Southeast (Manufacturing Hubs)

4.5.3. Midwest (Automotive Industry)

4.5.4. Northeast (Data Center Concentration)

5.1. Detailed Profiles of Major Companies (15 Competitors)

5.1.1. Micron Technology

5.1.2. SK Hynix

5.1.3. Samsung Electronics

5.1.4. Nanya Technology

5.1.5. Winbond Electronics

5.1.6. Powerchip Semiconductor

5.1.7. Western Digital Corporation

5.1.8. Intel Corporation

5.1.9. Rambus

5.1.10. Infineon Technologies

5.1.11. Broadcom Inc.

5.1.12. Kingston Technology

5.1.13. Nvidia Corporation (DRAM for GPUs)

5.1.14. AMD (DRAM for Servers and HPC)

5.1.15. Qualcomm (DRAM for Mobile Devices)

5.2. Cross Comparison Parameters (Inception Year, R&D Investments, DRAM Manufacturing Capacity, Market Share, Technology Node)

5.3. Market Share Analysis (Segment-Wise Share of Leading Companies)

5.4. Strategic Initiatives (Expansion, New Product Launches, Partnerships)

5.5. Mergers and Acquisitions (Recent Activity)

5.6. Investment Analysis (Capital Expenditure on New DRAM Manufacturing Facilities)

5.7. Venture Capital Funding (Emerging Startups in DRAM Technology)

5.8. Government Grants and Subsidies for DRAM Manufacturing

5.9. Private Equity Investments

6.1. Compliance Requirements (Environmental, Labor)

6.2. Certification Processes (Industry Standards, Energy-Efficient DRAM)

6.3. Tariff Policies and Trade Barriers

7.1. Future Market Size Projections (Based on Technological Shifts)

7.2. Key Factors Driving Future Market Growth (AI, IoT, 5G, Autonomous Vehicles)

8.1. By DRAM Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology Node (In Value %)

8.4. By End-User Industry (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis (Tech Giants, SME DRAM Consumers)

9.3. Marketing Initiatives (Collaborations, Product Awareness Campaigns)

9.4. White Space Opportunity Analysis

The research began by identifying critical variables impacting the USA DRAM Market, focusing on demand patterns across key sectors like cloud computing, automotive, and AI. This step involved extensive secondary research using government data, industry reports, and proprietary databases to construct a robust framework.

Historical data were analyzed to understand DRAM market dynamics, including production volumes, sales, and demand fluctuations across sectors. Market penetration was evaluated alongside technological advancements, enabling precise revenue estimates for different DRAM segments.

Initial market hypotheses were validated through interviews with industry experts, including executives from leading DRAM manufacturers and tech companies. Insights into future trends and emerging technologies were obtained through these consultations.

A final synthesis of findings was conducted by combining quantitative data with qualitative insights from industry leaders. This synthesis helped finalize market forecasts and segment-wise analysis, ensuring a well-rounded view of the USA DRAM market.

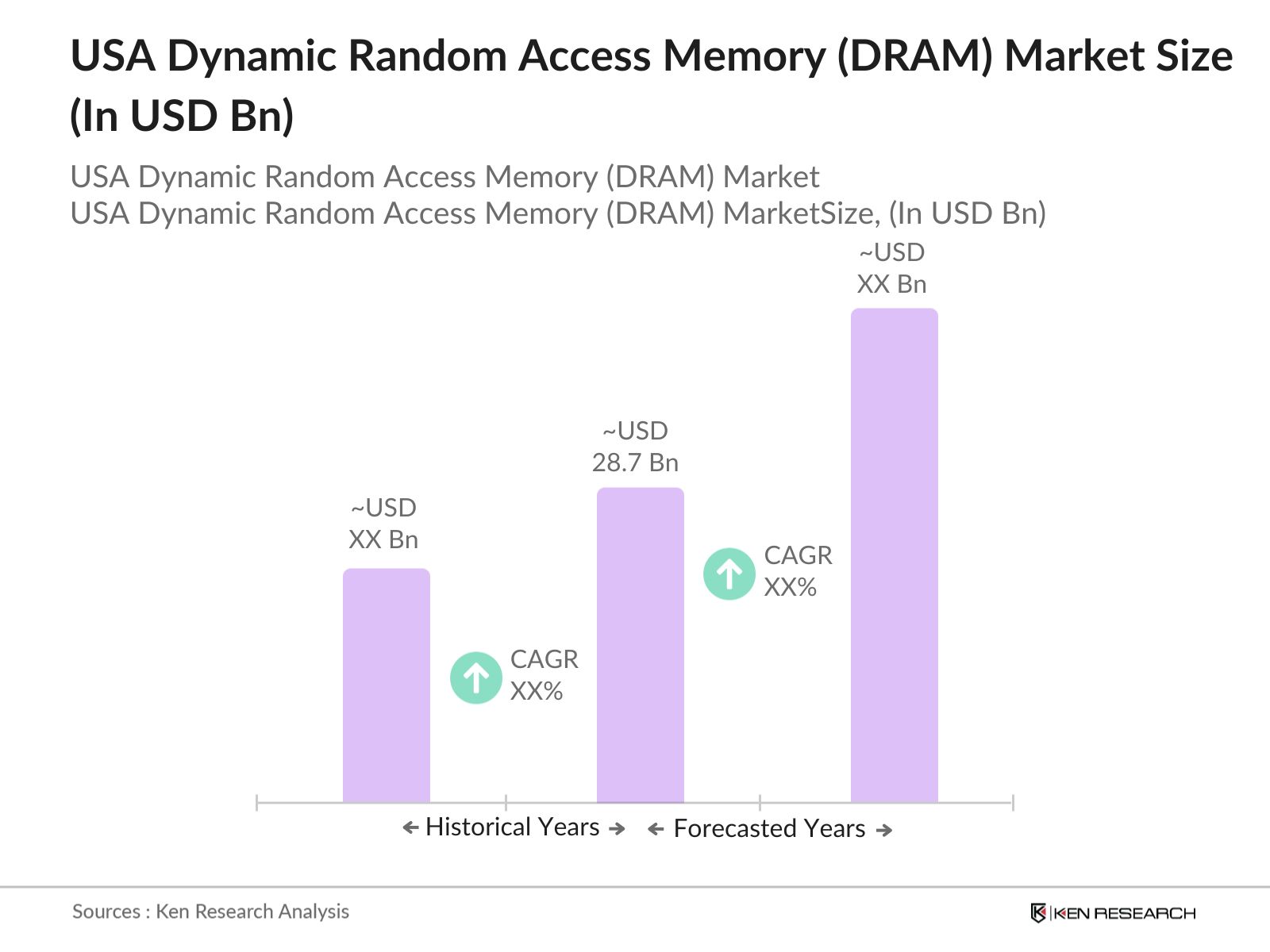

The USA DRAM market is valued at USD 28.7 billion in 2023, driven by surging demand from data centers, cloud services, and advancements in AI technology.

Key challenges in the USA DRAM market include global semiconductor supply chain disruptions, high manufacturing costs, and technical complexities in scaling DRAM production to newer technology nodes like 7nm and below.

Key players in the USA DRAM market include Micron Technology, Intel, Samsung Electronics, SK Hynix, and Nanya Technology. These companies dominate the market due to their innovation and large-scale manufacturing capacity.

The USA DRAM market is driven by the increasing need for high-performance memory in data centers, cloud computing, artificial intelligence, and autonomous vehicles. The shift towards DDR5 also offers improved performance and efficiency, driving adoption across various industries.

Emerging opportunities in the USA DRAM market include the rise of edge computing, 5G infrastructure expansion, and AI-driven advancements, all of which require faster, higher-capacity DRAM solutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.