USA Electric Scooter Sharing Market Outlook to 2030

Region:United States

Author(s):Yogita Sahu

Product Code:KROD3315

Region:United States

Author(s):Yogita Sahu

Product Code:KROD3315

October 2024

88

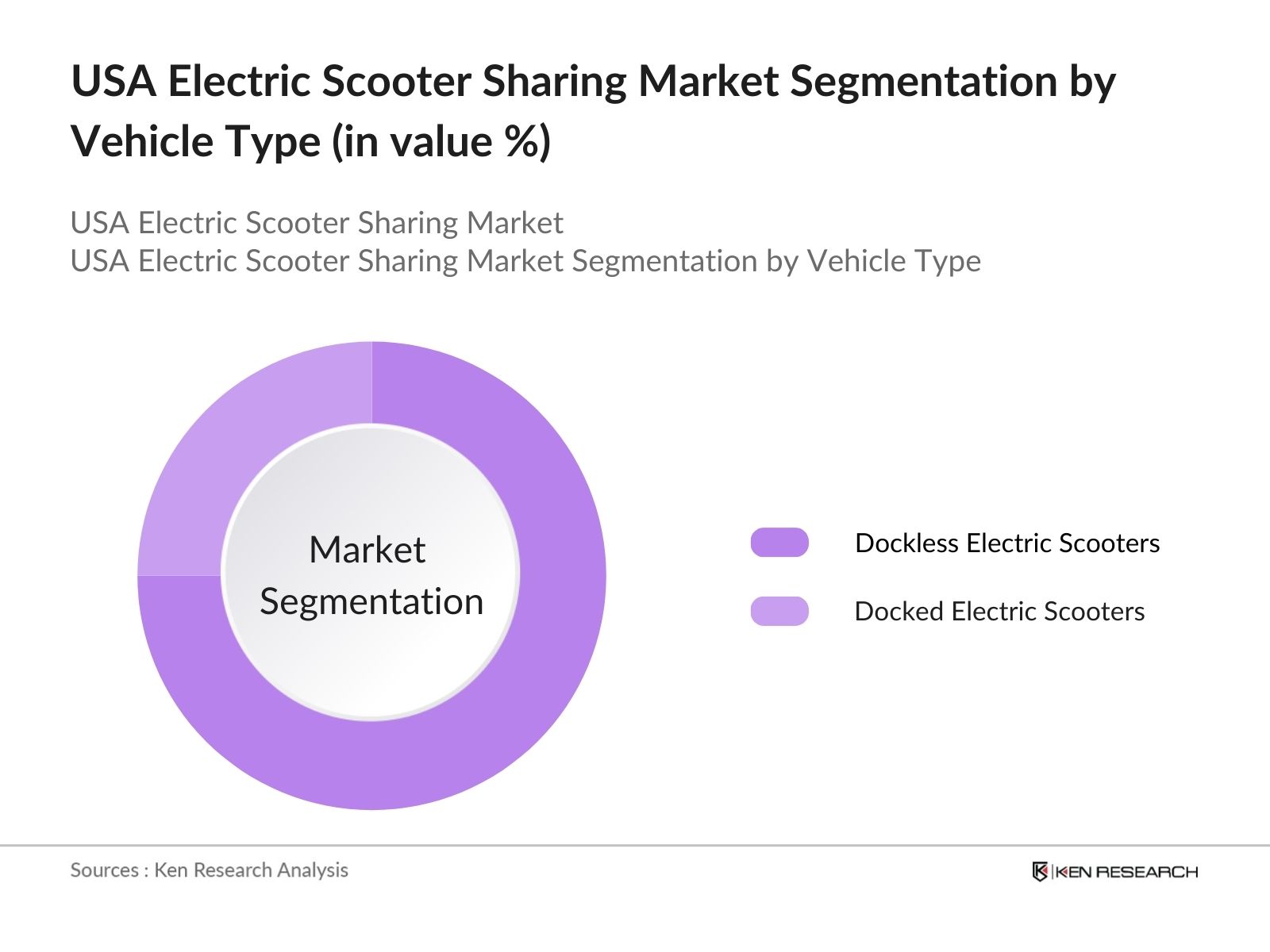

By Vehicle Type: The market is segmented by vehicle type into Dockless Electric Scooters and Docked Electric Scooters. Dockless Electric Scooters dominate the market due to their ease of use, allowing users to pick up and drop off scooters without needing to locate specific docking stations. The convenience and flexibility of this model make it ideal for urban areas, especially those with limited parking infrastructure.

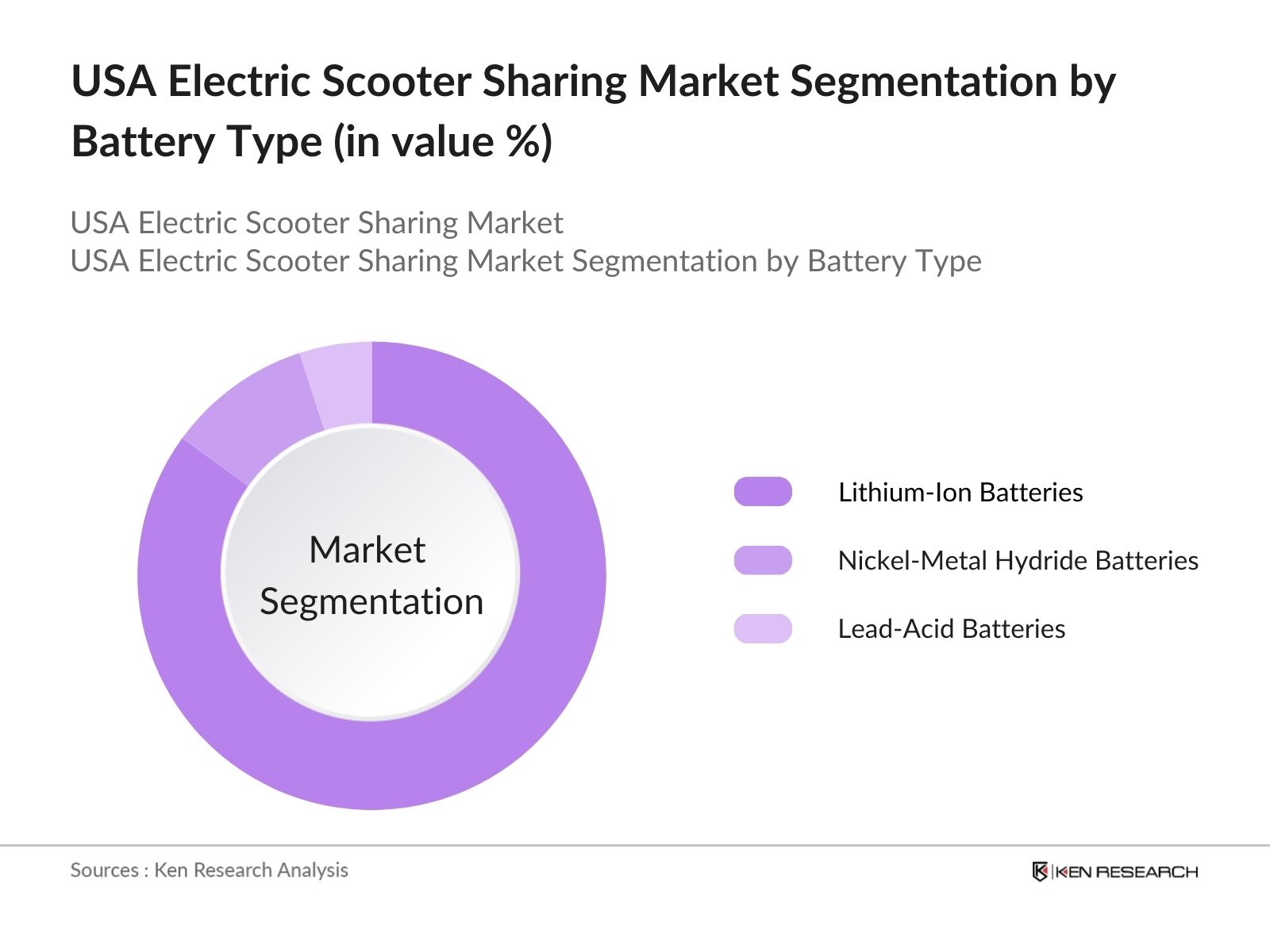

By Battery Type: The market is segmented by battery type into Lithium-Ion Batteries, Nickel-Metal Hydride Batteries, and Lead-Acid Batteries. Lithium-ion batteries lead the segment due to their superior energy density, longer lifespan, and faster charging times. The lightweight nature and declining costs of lithium-ion batteries have further accelerated their adoption in electric scooters, making them the preferred choice for scooter-sharing companies.

The market is highly competitive, with several major players dominating the landscape. Companies like Lime, Bird, and Spin lead the market, leveraging their strong brand presence, extensive scooter fleets, and strategic partnerships with local governments. These key players invest heavily in technology, such as AI-driven fleet management and GPS tracking, to optimize operations and ensure efficient service delivery.

|

Company |

Establishment Year |

Headquarters |

Fleet Size |

Global Presence |

Revenue (USD Bn) |

Sustainability Initiatives |

Partnerships |

Ride Efficiency |

|

Lime |

2017 |

San Francisco, CA |

||||||

|

Bird |

2017 |

Santa Monica, CA |

||||||

|

Spin (Ford Mobility) |

2018 |

Detroit, MI |

||||||

|

VeoRide |

2018 |

Chicago, IL |

||||||

|

Superpedestrian |

2019 |

Cambridge, MA |

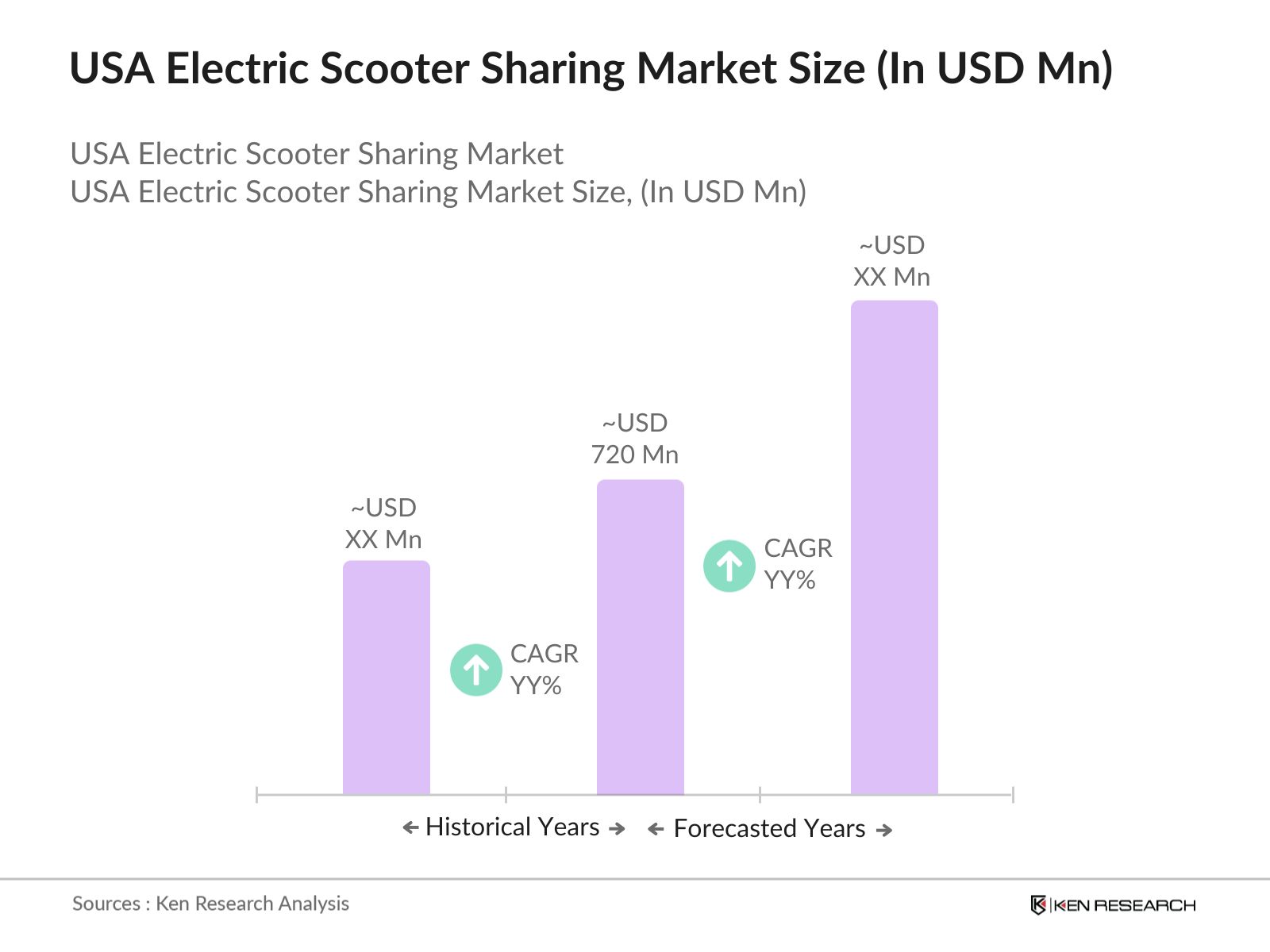

Over the next five years, the USA Electric Scooter Sharing industry is expected to experience growth, driven by the continuous expansion of urban micro-mobility networks and increased investments in sustainable transportation. As cities aim to reduce traffic congestion and carbon emissions, the demand for electric scooter-sharing services is expected to rise.

|

Vehicle Type |

Dockless Electric Scooters |

|

Battery Type |

Lithium-Ion Batteries |

|

Service Model |

Pay-Per-Ride Model |

|

Application |

Urban Mobility |

|

Region |

North South |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Urban Congestion Reduction Initiatives

3.1.2 Increasing Environmental Awareness

3.1.3 Rise in Micro-Mobility Solutions

3.1.4 Expansion of Sustainable Transport Policies

3.2 Market Challenges

3.2.1 Regulatory and Licensing Issues

3.2.2 Maintenance and Operational Costs

3.2.3 Safety Concerns Among Users

3.2.4 Infrastructure Limitations

3.3 Opportunities

3.3.1 Integration with Public Transportation Networks

3.3.2 Expanding Smart City Projects

3.3.3 Partnerships with Ride-Hailing Platforms

3.3.4 Potential Growth in Suburban and Tier-2 Markets

3.4 Trends

3.4.1 Increasing Adoption of Subscription-Based Models

3.4.2 Use of AI for Fleet Optimization

3.4.3 Rising Demand for Electric Charging Infrastructure

3.4.4 Growth in App-Based Real-Time Monitoring

3.5 Government Regulation

3.5.1 Federal Micro-Mobility Safety Standards

3.5.2 State-Level Shared Mobility Policies

3.5.3 Incentives for Electrification of Mobility

3.5.4 Urban Traffic Control and Scooter Parking Laws

3.6 SWOT Analysis

3.7 Stake Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Ecosystem

4.1 By Vehicle Type (In Value %)

4.1.1 Dockless Electric Scooters

4.1.2 Docked Electric Scooters

4.2 By Battery Type (In Value %)

4.2.1 Lithium-Ion Batteries

4.2.2 Nickel-Metal Hydride Batteries

4.2.3 Lead-Acid Batteries

4.3 By Service Model (In Value %)

4.3.1 Pay-Per-Ride Model

4.3.2 Subscription-Based Model

4.4 By Application (In Value %)

4.4.1 Urban Mobility

4.4.2 Campus Transport

4.4.3 Tourism and Leisure

4.5 By Region (In Value %)

4.5.1 North

4.5.2 West

4.5.3 East

4.5.4 South

5.1 Detailed Profiles of Major Companies

5.1.1 Lime

5.1.2 Bird

5.1.3 Spin (Ford Mobility)

5.1.4 Helbiz

5.1.5 Skip Scooters

5.1.6 Lyft Scooters

5.1.7 VeoRide

5.1.8 Tier Mobility

5.1.9 Razor Share

5.1.10 Superpedestrian (Link)

5.1.11 Wheels

5.1.12 Scoot Networks

5.1.13 Bolt Mobility

5.1.14 Spinlister

5.1.15 Revel Transit

5.2 Cross Comparison Parameters (Fleet Size, Expansion Strategy, Pricing Models, Revenue,Partnerships, Sustainability Initiatives, User Base, Ride Efficiency)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Shared Mobility Policy Compliance

6.2 Data Privacy and User Protection Laws

6.3 Safety Standards for Electric Scooters

6.4 Licensing and Permits for Operation

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Vehicle Type (In Value %)

8.2 By Battery Type (In Value %)

8.3 By Service Model (In Value %)

8.4 By Application (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact Us

In this phase, we create a comprehensive ecosystem map of the USA Electric Scooter Sharing Market, identifying all major stakeholders such as manufacturers, service providers, and regulatory authorities. Extensive desk research is used to collect data on industry-level dynamics.

We analyze historical data on market penetration, revenue generation, and fleet utilization rates. This step also includes assessing infrastructure development and regulations that impact service providers. The gathered data is used to construct reliable market estimates.

Through expert interviews with market participants and industry practitioners, we validate our market hypotheses. These consultations offer operational insights, ensuring the accuracy of projected market trends and growth drivers.

Finally, we consolidate our findings through direct consultations with key electric scooter manufacturers. This ensures a comprehensive and validated analysis, encompassing fleet size, pricing models, consumer preferences, and regulatory impacts.

The USA Electric Scooter Sharing Market was valued at USD 720 million, driven by urban mobility trends, increased environmental awareness, and strong governmental support for sustainable transportation solutions.

Key challenges in the USA Electric Scooter Sharing Market include regulatory barriers, infrastructure limitations, and safety concerns. Additionally, the high cost of fleet maintenance and repairs poses significant operational hurdles for service providers.

Major players in the USA Electric Scooter Sharing Market include Lime, Bird, Spin (Ford Mobility), VeoRide, and Superpedestrian. These companies dominate due to their expansive scooter fleets, strong technology platforms, and partnerships with local governments.

The USA Electric Scooter Sharing Market is propelled by the increasing demand for micro-mobility solutions, urban traffic congestion, and environmental concerns. Technological advancements in fleet management and battery technology also contribute to market growth.

In the coming years, the USA Electric Scooter Sharing Market integration with public transportation systems and the expansion of smart city initiatives will drive further growth. Additionally, advancements in battery technology and AI-driven fleet management will create new opportunities for innovation in the sector.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.