USA Emergency Department Market Outlook to 2030

Region:North America

Author(s):Shreya Garg

Product Code:KROD10100

November 2024

96

About the Report

USA Emergency Department Market Overview

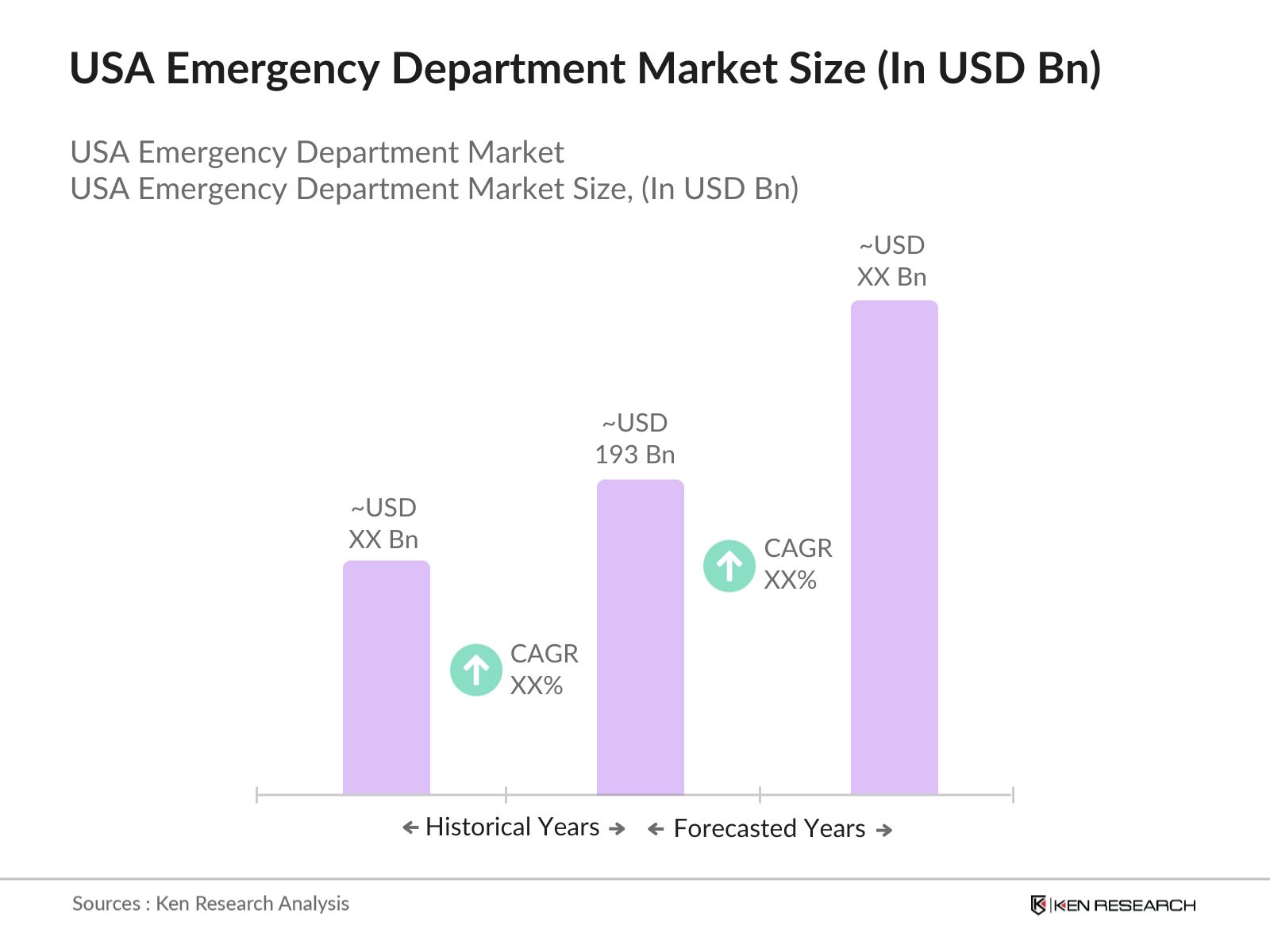

- The USA Emergency Department market is valued at USD 193 billion, driven by increasing demand for emergency healthcare services due to the rise in chronic illnesses, an aging population, and the increasing frequency of accidents. Additionally, the growing healthcare expenditure in the U.S. is pushing the expansion of emergency services across hospitals and free-standing emergency centers. This market size is based on historical analysis from reputable industry sources, reflecting the rapid development of healthcare infrastructure and services across the nation.

- Cities like New York, Los Angeles, and Chicago dominate the USA Emergency Department market. These cities have large populations, a high number of healthcare facilities, and experience frequent emergency visits due to both chronic health issues and high rates of accidents. Moreover, the advanced medical infrastructure and the availability of specialized emergency services contribute to their dominance in the emergency department landscape.

- The Emergency Medical Treatment and Labor Act (EMTALA) mandates that all patients presenting to emergency departments must receive appropriate medical screening and care, regardless of their ability to pay. As of 2024, U.S. hospitals are required to comply with EMTALA regulations, which are enforced by the Centers for Medicare & Medicaid Services (CMS). EMTALA has significantly shaped the operations of emergency departments, ensuring that patients receive timely and necessary care. Compliance with EMTALA has driven hospitals to invest in their emergency infrastructure to meet the growing patient demand

USA Emergency Department Market Segmentation

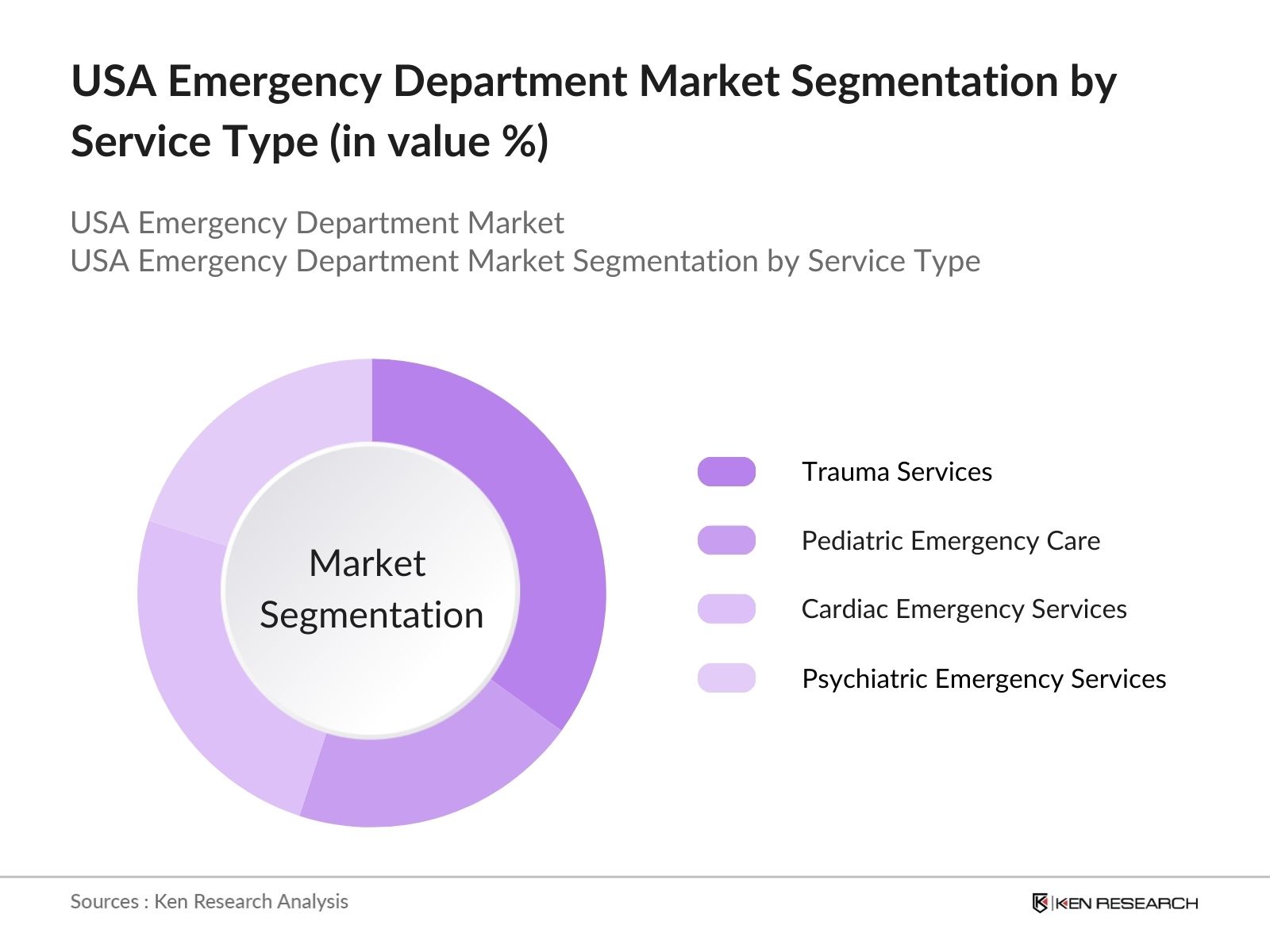

By Service Type: The market is segmented by service type into trauma services, pediatric emergency care, cardiac emergency services, and psychiatric emergency services. Recently, trauma services have held a dominant market share due to the increasing number of accidents and injuries, which require immediate medical attention. Emergency trauma care has become highly specialized, with hospitals investing in state-of-the-art trauma centers and skilled professionals to cater to patients suffering from critical injuries. As a result, the trauma services segment is leading the market in terms of revenue generation.

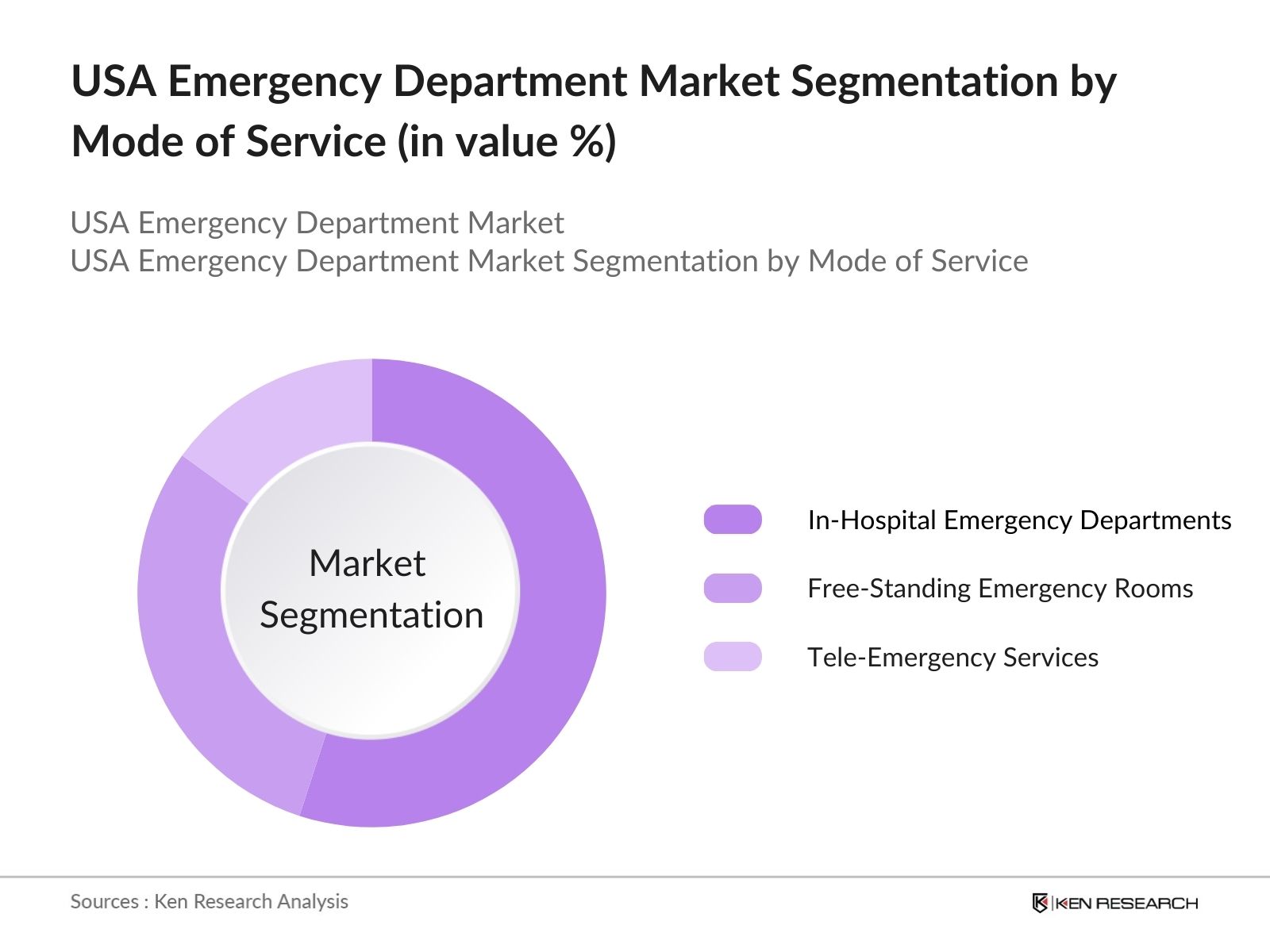

By Mode of Service: The market is also segmented by mode of service, including in-hospital emergency departments, free-standing emergency rooms, and tele-emergency services. In-hospital emergency departments are the dominant sub-segment, due to their established presence and accessibility for most patients. Hospitals provide comprehensive emergency care, equipped with specialists, advanced diagnostic tools, and intensive care units. The trusted reputation of hospitals in delivering quality emergency care keeps this mode of service as a market leader in 2023.

USA Emergency Department Market Competitive Landscape

The USA Emergency Department market is dominated by major healthcare players that have been steadily expanding their service offerings and enhancing their technological capabilities. These companies are engaged in mergers and acquisitions, strategic alliances, and technological innovation to maintain a competitive edge. The consolidation of market power among these players allows them to maintain dominance by leveraging advanced healthcare technologies and expanding their reach through mergers and acquisitions.

|

Company Name |

Establishment Year |

Headquarters |

No. of Employees |

Service Coverage |

Specialization in Emergency Care |

Technological Integration |

Revenue (USD) |

Market Share (%) |

Recent Investments |

|

Envision Healthcare |

1953 |

Nashville, TN |

|||||||

|

HCA Healthcare |

1968 |

Nashville, TN |

|||||||

|

TeamHealth |

1979 |

Knoxville, TN |

|||||||

|

US Acute Care Solutions |

2015 |

Canton, OH |

|||||||

|

American Physician Partners |

2015 |

Brentwood, TN |

USA Emergency Department Industry Analysis

Growth Drivers

- Aging Population: As of 2024, the USA is experiencing a demographic shift with an increase in the aging population. According to the U.S. Census Bureau, around 54 million Americans are aged 65 and older, with projections indicating that this number will reach nearly 80 million by 2030. This surge in elderly individuals, who often have complex medical needs, drives higher demand for emergency department (ED) services. Additionally, older adults are more prone to chronic conditions, falls, and other health issues, further straining ED resources. This aging demographic will continue to be a critical factor in shaping emergency healthcare services.

- Rise in Chronic Diseases: Chronic diseases such as heart disease, diabetes, and respiratory disorders are on the rise in the USA. As per data from the CDC, approximately 133 million Americansmore than 40% of the populationare affected by at least one chronic illness, with these numbers expected to grow. Chronic conditions require frequent medical attention and, in many cases, lead to emergency care due to complications or acute episodes. This increasing burden of chronic diseases is one of the most significant drivers of ED visits, placing immense pressure on the healthcare system to provide timely and efficient care.

- Government Initiatives for Healthcare Expansion: The U.S. government has implemented various initiatives to expand healthcare access, particularly under the Affordable Care Act (ACA), which has increased healthcare coverage for millions of Americans. As of 2024, nearly 16 million people are enrolled in ACA marketplace plans, according to the Centers for Medicare & Medicaid Services (CMS). This expansion has resulted in a broader section of the population seeking emergency care services. Government policies supporting value-based care and enhancing healthcare infrastructure in underserved areas further drive the demand for emergency department services.

Market Challenges

- Overcrowding in Emergency Departments: Overcrowding in emergency departments has become a significant challenge across the USA. According to the CDC, there were over 130 million emergency department visits in 2023. This high patient influx, combined with limited bed availability, creates bottlenecks in the system, leading to longer wait times and delays in care delivery. The American Hospital Association (AHA) notes that overcrowding can lead to compromised patient outcomes, including delayed diagnosis and treatment. Addressing overcrowding requires not just additional infrastructure but also efficient patient flow management systems.

- Physician Shortages: Physician shortages in emergency departments have been a growing concern, with data from the Association of American Medical Colleges (AAMC) showing a shortfall of between 38,000 and 124,000 physicians across various specialties by 2034. This shortage directly impacts the quality of emergency care services, as workforce constraints lead to increased workload and stress for existing staff, causing longer patient wait times and diminished care quality. Recruitment and retention of emergency care physicians are crucial to meeting the rising demand for healthcare services.

USA Emergency Department Market Future Outlook

The USA Emergency Department market is expected to experience steady growth over the next few years. Continuous advancements in healthcare technology, including the integration of artificial intelligence and telemedicine in emergency departments, are likely to drive growth. Additionally, as healthcare systems prioritize patient experience and operational efficiency, the use of AI-driven triage systems and real-time data analytics will significantly enhance emergency services' quality and effectiveness.

Future Market Opportunities

- Integration of Telemedicine in Emergency Services: Telemedicine has emerged as a vital tool for addressing some of the challenges faced by emergency departments. According to the American Telemedicine Association, over 70% of U.S. healthcare providers have incorporated telehealth solutions into their practice as of 2024. Telemedicine in emergency care allows healthcare providers to triage patients remotely, reducing the burden on emergency departments and enabling timely intervention. It also enhances access to emergency care in rural and underserved areas, where healthcare infrastructure is limited. Telemedicine's growing integration is set to transform emergency care delivery in the coming years.

- Development of AI-based Emergency Care Solutions: AI technologies are increasingly being integrated into emergency care to improve diagnostics, patient triage, and decision-making processes. AI-based tools, such as predictive analytics platforms, assist healthcare professionals in identifying high-risk patients and prioritizing care accordingly. The U.S. healthcare industry has seen significant investment in AI applications, with over $5 billion invested in 2023 alone, according to the National Institutes of Health (NIH). These AI-driven innovations are expected to streamline emergency department operations, reduce patient wait times, and improve overall outcomes.

Scope of the Report

|

By Service Type |

Trauma Services Pediatric Emergency Care Cardiac Emergency Services Psychiatric Emergency Services |

|

By Mode of Service |

In-Hospital Emergency Departments Free-Standing Emergency Rooms Tele-Emergency Services |

|

By Acuity Level |

High Acuity Low Acuity |

|

By Patient Demographics |

Adults Pediatrics Geriatrics |

|

By Region |

Northeast Midwest South West |

Products

Key Target Audience

Emergency Healthcare Providers

Hospitals & Medical Centers

Telemedicine Companies

Health Insurance Providers

Medical Device Manufacturers

Venture Capitalist Firms & Investors

Government and Regulatory Bodies (Centers for Medicare & Medicaid Services)

Technology Providers (for Healthcare Solutions)

Companies

Major Players

Envision Healthcare

HCA Healthcare

TeamHealth

US Acute Care Solutions

American Physician Partners

ApolloMD

Tenet Healthcare

Sound Physicians

Fresenius Medical Care

Centene Corporation

Aetna

Anthem Inc.

CVS Health (Aetna)

Sutter Health

Banner Health

Table of Contents

USA Emergency Department Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

USA Emergency Department Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

USA Emergency Department Market Analysis

3.1. Growth Drivers

3.1.1. Aging Population

3.1.2. Rise in Chronic Diseases

3.1.3. Government Initiatives for Healthcare Expansion

3.1.4. Increasing Healthcare Expenditure

3.2. Market Challenges

3.2.1. Overcrowding in Emergency Departments (High patient influx, lack of beds)

3.2.2. Physician Shortages (Workforce constraints, recruitment issues)

3.2.3. Rising Healthcare Costs (Reimbursement challenges, high operational costs)

3.3. Opportunities

3.3.1. Integration of Telemedicine in Emergency Services

3.3.2. Development of AI-based Emergency Care Solutions

3.3.3. Expansion of Urgent Care Centers

3.4. Trends

3.4.1. Increased Adoption of Electronic Health Records (EHRs)

3.4.2. Focus on Patient Triage Systems (AI-powered tools)

3.4.3. Mobile Health Technologies in Emergency Care

3.5. Government Regulation

3.5.1. EMTALA Compliance (Emergency Medical Treatment and Labor Act)

3.5.2. Medicare and Medicaid Reimbursements (Value-based care)

3.5.3. State-Specific Healthcare Regulations

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

USA Emergency Department Market Segmentation

4.1. By Service Type (In Value %)

4.1.1. Trauma Services

4.1.2. Pediatric Emergency Care

4.1.3. Cardiac Emergency Services

4.1.4. Psychiatric Emergency Services

4.2. By Mode of Service (In Value %)

4.2.1. In-Hospital Emergency Departments

4.2.2. Free-Standing Emergency Rooms

4.2.3. Tele-Emergency Services

4.3. By Acuity Level (In Value %)

4.3.1. High Acuity

4.3.2. Low Acuity

4.4. By Patient Demographics (In Value %)

4.4.1. Adults

4.4.2. Pediatrics

4.4.3. Geriatrics

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

USA Emergency Department Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Envision Healthcare

5.1.2. HCA Healthcare

5.1.3. TeamHealth

5.1.4. US Acute Care Solutions

5.1.5. American Physician Partners

5.1.6. ApolloMD

5.1.7. Tenet Healthcare

5.1.8. Sound Physicians

5.1.9. Fresenius Medical Care

5.1.10. Centene Corporation

5.1.11. Aetna

5.1.12. Anthem Inc.

5.1.13. CVS Health (Aetna)

5.1.14. Sutter Health

5.1.15. Banner Health

5.2 Cross Comparison Parameters (Revenue, Employee Strength, Market Share, Service Expansion, Reimbursement Coverage, Technology Adoption, Emergency Services Coverage, Financial Health)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

USA Emergency Department Market Regulatory Framework

6.1. Compliance Requirements for Emergency Department Services

6.2. Accreditation and Certification Processes

6.3. Medicare and Medicaid Policies

USA Emergency Department Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

USA Emergency Department Future Market Segmentation

8.1. By Service Type (In Value %)

8.2. By Mode of Service (In Value %)

8.3. By Acuity Level (In Value %)

8.4. By Patient Demographics (In Value %)

8.5. By Region (In Value %)

USA Emergency Department Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

We initiated the research by identifying crucial factors that influence the emergency department market. A comprehensive ecosystem map was developed to highlight the key players and influencers in the sector. Primary data was collected from government healthcare databases, while secondary data was sourced from industry reports.

Step 2: Market Analysis and Construction

Historical data from government sources and hospitals were compiled to assess the current state of the USA Emergency Department market. This involved analyzing patient visits, services rendered, and operational revenues, as well as evaluating the role of technological integration in streamlining services.

Step 3: Hypothesis Validation and Expert Consultation

Through direct consultations with healthcare professionals and analysts from leading emergency service providers, we validated our market hypotheses. Their insights on emerging trends, challenges, and opportunities helped refine the market estimates and service-based segmentation.

Frequently Asked Questions

01. How big is the USA Emergency Department market?

The USA Emergency Department market is valued at USD 193 billion, driven by increasing demand for emergency healthcare services due to an aging population and the rising prevalence of chronic diseases.

02. What are the key challenges in the USA Emergency Department market?

The key challenges in the USA Emergency Department market include overcrowding in emergency rooms, physician shortages, and rising operational costs due to the high demand for emergency services.

03. Who are the major players in the USA Emergency Department market?

Major players in the USA Emergency Department market include Envision Healthcare, HCA Healthcare, TeamHealth, US Acute Care Solutions, and American Physician Partners.

04. What drives the growth of the USA Emergency Department market?

Growth in the USA Emergency Department market is driven by an aging population, increased incidence of chronic diseases, and advancements in healthcare technologies, such as AI-driven triage and telemedicine.

05. What are the future opportunities in the USA Emergency Department market?

Opportunities in the USA Emergency Department market lie in the integration of AI and telemedicine, as well as the expansion of urgent care centers to cater to the rising patient demand for emergency services.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.