USA Endoscopic Devices Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD6717

November 2024

90

About the Report

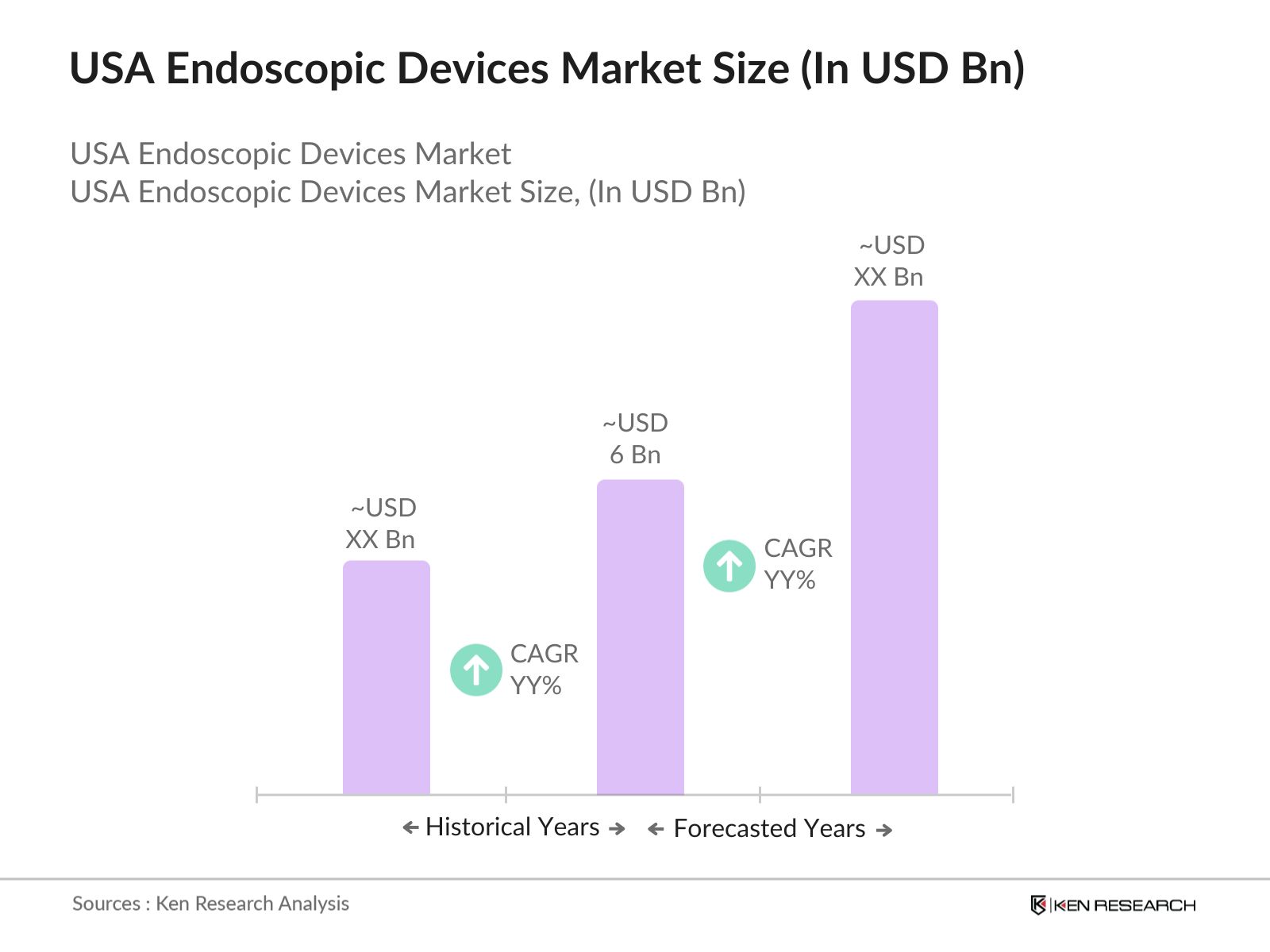

USA Endoscopic Devices Market Overview

- The USA endoscopic devices market is valued at USD 6 billion, driven by the rising demand for minimally invasive surgeries. This growth can be attributed to the increasing prevalence of chronic diseases, such as gastrointestinal disorders, colorectal cancer, and respiratory conditions, where endoscopy is a preferred diagnostic and therapeutic tool.

- Dominant regions in the USA that drive this market include California and Texas, owing to their large population bases, the presence of advanced healthcare infrastructures, and a high concentration of specialized hospitals and clinics. These regions also have a high number of surgeries performed, driven by the availability of skilled professionals and early adoption of advanced medical technologies, which makes them market leaders in terms of revenue generation.

- The FDAs Center for Devices and Radiological Health (CDRH) has prioritized the approval of innovative endoscopic devices through its Expedited Access Pathway (EAP) program. This has resulted in faster approvals for endoscopic devices aimed at treating critical conditions like colorectal cancer, with more than 25 new devices receiving approval between 2022 and 2024.

USA Endoscopic Devices Market Segmentation

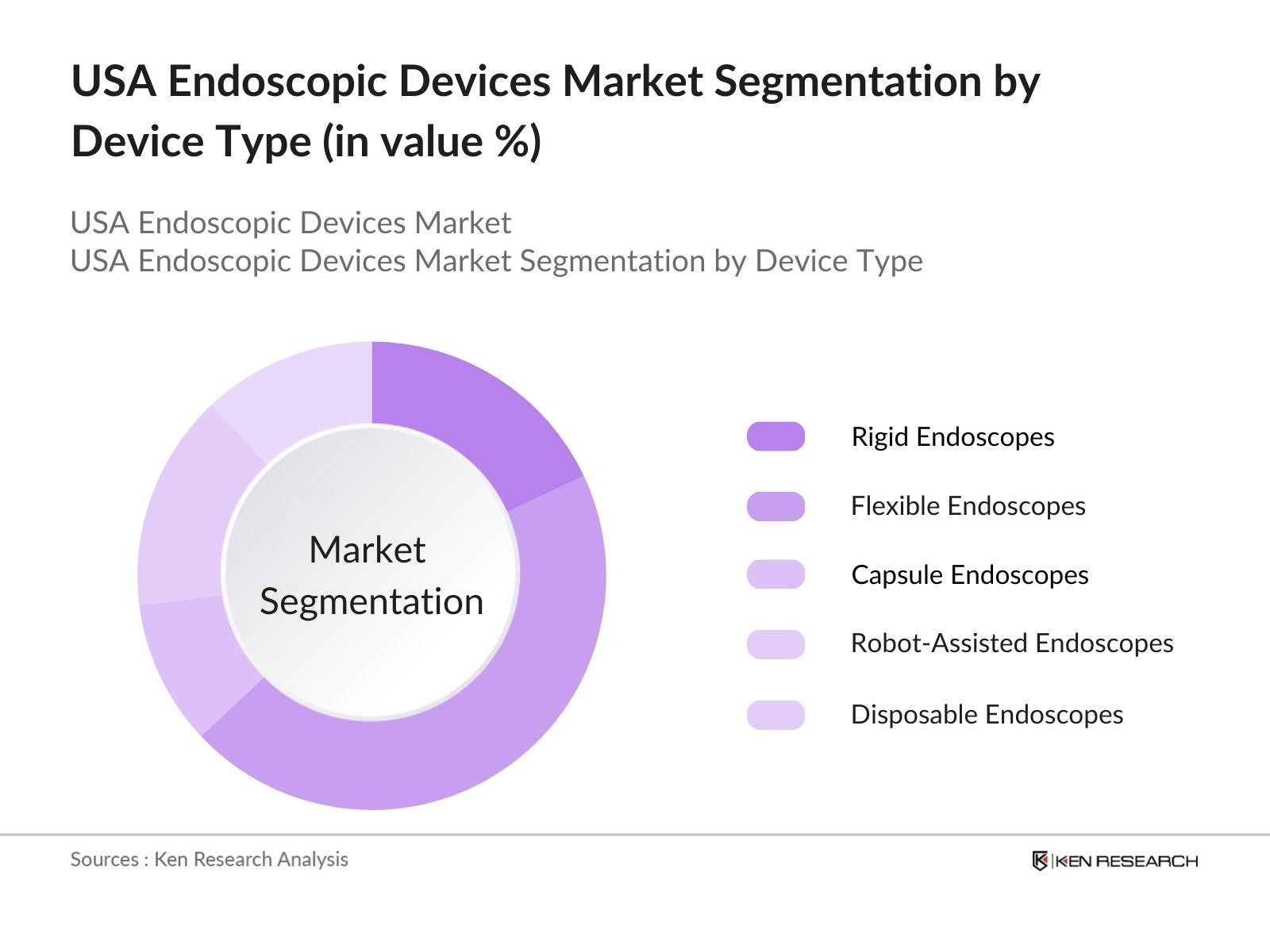

By Device Type: The market is segmented by device type into rigid endoscopes, flexible endoscopes, capsule endoscopes, robot-assisted endoscopes, and disposable endoscopes. Among these, flexible endoscopes hold a dominant market share, primarily due to their versatility in performing various types of endoscopic procedures, such as gastrointestinal and pulmonary procedures. These devices are preferred by healthcare professionals for their ability to navigate through complex anatomical structures, providing a minimally invasive option for patients.

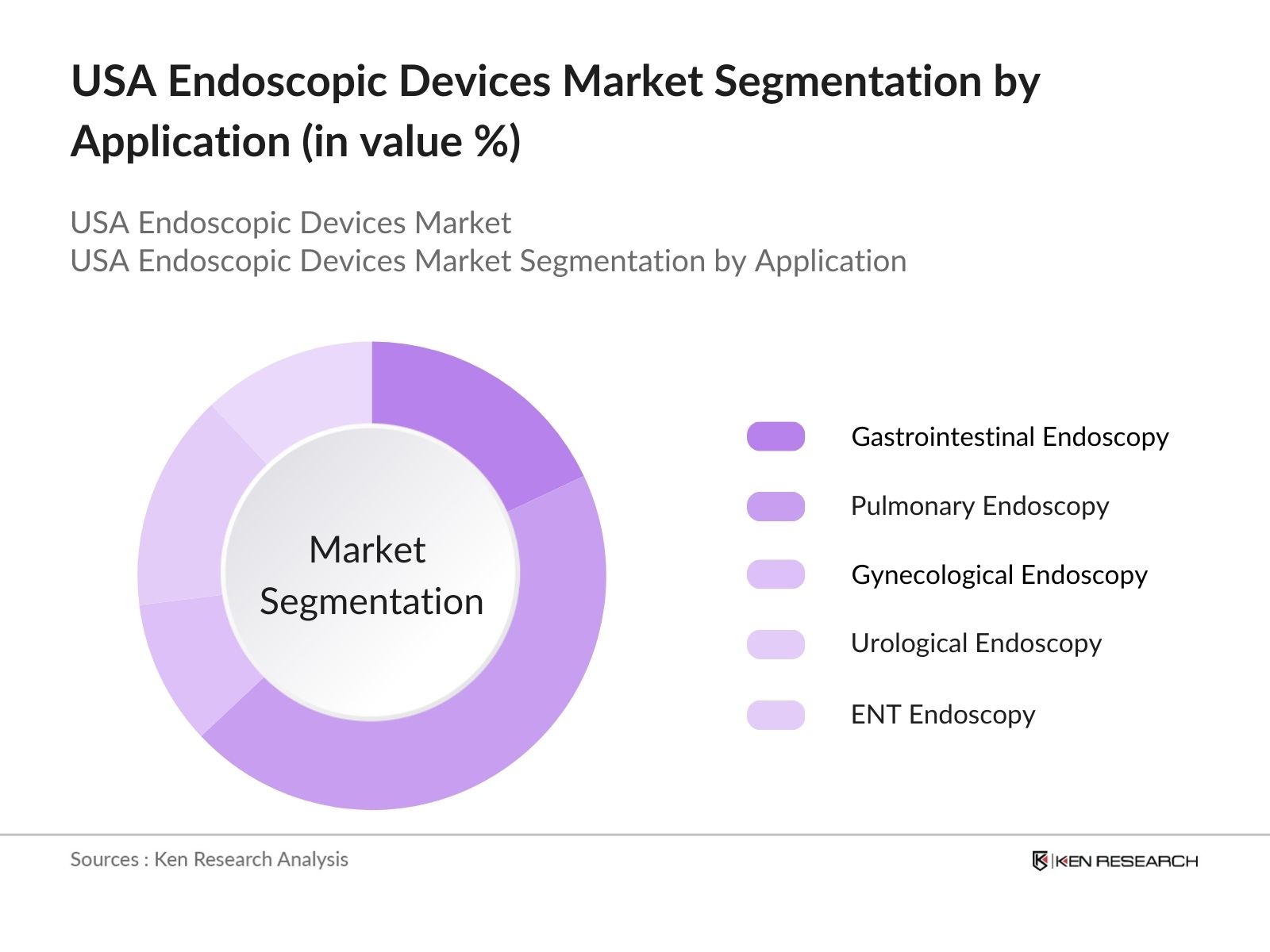

By Application: The market is also segmented by application into gastrointestinal endoscopy, pulmonary endoscopy, gynecological endoscopy, urological endoscopy, and ENT endoscopy. Gastrointestinal endoscopy is the largest sub-segment, dominating the market due to the high prevalence of gastrointestinal diseases such as colorectal cancer and irritable bowel syndrome (IBS). The increasing demand for colonoscopies and the role of endoscopic devices in early cancer detection have bolstered the growth of this segment.

USA Endoscopic Devices Market Competitive Landscape

The market is dominated by several key players, both local and global, who contribute to market growth through constant product innovations, partnerships, and strategic investments. The competitive landscape is largely consolidated, with leading companies such as Olympus Corporation, Boston Scientific, and Stryker Corporation taking a major share of the market.

|

Company Name |

Established Year |

Headquarters |

Revenue |

R&D Investment |

Product Range |

Strategic Partnerships |

Market Share |

Key Products |

|

Olympus Corporation |

1919 |

Tokyo, Japan |

||||||

|

Boston Scientific Corporation |

1979 |

Marlborough, USA |

||||||

|

Stryker Corporation |

1941 |

Kalamazoo, USA |

||||||

|

Karl Storz SE & Co. KG |

1945 |

Tuttlingen, Germany |

||||||

|

Medtronic plc |

1949 |

Dublin, Ireland |

USA Endoscopic Devices Market Analysis

Market Growth Drivers

- Increasing Prevalence of Gastrointestinal Disorders: According to the American Cancer Society, around 106,970 new cases of colon cancer and 46,050 cases of rectal cancer are estimated in 2024 in the USA. This surge in cases drives the demand for endoscopic devices, particularly colonoscopies and sigmoidoscopies, to detect early stages of gastrointestinal diseases, including cancer. With over 19 million colonoscopies performed annually in the U.S., the demand for high-quality, efficient devices has grown to cater to both diagnostic and therapeutic needs.

- Rising Geriatric Population: The United States Census Bureau estimates that by 2024, more than 58 million people in the USA will be aged 65 and older. This age group is particularly prone to conditions requiring endoscopic interventions, such as colorectal cancer, peptic ulcers, and gastrointestinal bleeding. The aging population has led to an increased number of procedures, with over 4.5 million upper GI endoscopies performed annually, enhancing the demand for advanced endoscopic devices to ensure effective treatment and patient care.

- Surge in Minimally Invasive Surgeries: In 2024, it is estimated that over 14.5 million minimally invasive surgeries will be performed in the USA, including a portion that utilizes endoscopic devices. Patients and healthcare providers increasingly prefer these procedures due to reduced recovery time and hospital stays. Endoscopic devices such as flexible endoscopes, camera systems, and energy devices are integral in procedures like laparoscopic surgeries, which account for over 3 million cases annually in the country.

Market Challenges

- Rising Incidents of Dry Eye and Lens Discomfort: According to the National Eye Institute, dry eye syndrome affects over 16 million Americans, with a number of them reporting discomfort while wearing contact lenses. This has led to a 20% decline in the use of contact lenses among this population in recent years, prompting manufacturers to invest in developing more breathable and comfortable materials.

- Lack of Insurance Coverage for Contact Lenses: In 2024, over 80 million Americans with vision correction needs had limited insurance coverage for contact lenses, according to the Centers for Medicare & Medicaid Services (CMS). Most insurance plans only cover eyeglasses, leaving a substantial out-of-pocket cost for contact lenses. This financial barrier has slowed the adoption of contact lenses in favor of glasses among price-sensitive consumers.

USA Endoscopic Devices Market Future Outlook

Over the next five years, the USA endoscopic devices industry is expected to exhibit growth, driven by the increasing demand for less invasive diagnostic procedures and advances in imaging technologies. The growing elderly population in the USA and the rise in chronic diseases such as colorectal cancer and digestive disorders will also fuel the market's growth.

Future Market Opportunities

- Growing Demand for Multifocal Lenses in Aging Population: By 2029, the U.S. population over the age of 65 is expected to reach 60 million, further driving demand for multifocal contact lenses as presbyopia becomes more prevalent. This demographic shift will prompt manufacturers to develop more advanced lenses that cater specifically to the elderly, increasing the availability of lenses designed for prolonged wear and enhanced comfort.

- Advancement in Smart Contact Lens Technology: The market for smart contact lenses is expected to grow exponentially over the next five years, with projections indicating over 1 million units in circulation by 2029. These lenses, featuring AR capabilities, glucose monitoring for diabetic patients, and real-time health data, will attract tech-savvy consumers and revolutionize the way contact lenses are used in everyday life.

Scope of the Report

|

By Device Type |

Rigid Endoscopes Flexible Endoscopes Capsule Endoscopes Robot-Assisted Endoscopes Disposable Endoscopes |

|

By Application |

Gastrointestinal Endoscopy Pulmonary Endoscopy Gynecological Endoscopy Urological Endoscopy ENT Endoscopy |

|

By End User |

Hospitals Ambulatory Surgical Centers Diagnostic Centers Specialty Clinics |

|

By Technology |

HD Imaging Systems 3D Endoscopy Narrow Band Imaging Capsule Endoscopy |

|

By Region |

North South East West |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Endoscopy Equipment Manufacturers

Banks and Financial Institution

Healthcare Service Providers

Government & Regulatory Bodies (FDA, Department of Health and Human Services)

Private Equity Firms

Investors and Venture Capitalist Firms

Companies

Players Mentioned in the Report:

Olympus Corporation

Boston Scientific Corporation

Stryker Corporation

Fujifilm Holdings Corporation

Pentax Medical

Medtronic plc

Smith & Nephew plc

Hoya Corporation

Richard Wolf GmbH

Cook Medical

Table of Contents

1. USA Endoscopic Devices Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate (Revenue Growth, CAGR)

1.4 Market Segmentation Overview

2. USA Endoscopic Devices Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis (Volume Growth, USD Contribution)

2.3 Key Market Developments and Milestones (Product Launches, Regulatory Approvals, Collaborations)

3. USA Endoscopic Devices Market Analysis

3.1 Growth Drivers

3.1.1 Increasing Prevalence of Chronic Diseases

3.1.2 Rising Geriatric Population

3.1.3 Growing Demand for Minimally Invasive Surgeries

3.1.4 Favorable Healthcare Reimbursement Policies

3.2 Market Challenges

3.2.1 High Cost of Advanced Endoscopic Devices

3.2.2 Stringent Regulatory Approvals

3.2.3 Limited Skilled Workforce

3.3 Opportunities

3.3.1 Technological Advancements in Endoscopic Devices

3.3.2 Expansion in Emerging Markets

3.3.3 Integration of AI in Endoscopy

3.4 Trends

3.4.1 Use of 4K and 3D Imaging Technologies

3.4.2 Rising Adoption of Robotic-Assisted Endoscopy

3.4.3 Growing Demand for Disposable Endoscopic Devices

3.5 Government Regulation (FDA Regulations, ISO Standards)

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem (Hospitals, Diagnostic Centers, Manufacturers)

3.8 Porters Five Forces (Supplier Power, Buyer Power, Competition Intensity, Threat of Substitutes)

3.9 Competition Ecosystem

4. USA Endoscopic Devices Market Segmentation

4.1 By Device Type (In Value %)

4.1.1 Rigid Endoscopes

4.1.2 Flexible Endoscopes

4.1.3 Capsule Endoscopes

4.1.4 Robot-Assisted Endoscopes

4.1.5 Disposable Endoscopes

4.2 By Application (In Value %)

4.2.1 Gastrointestinal Endoscopy

4.2.2 Pulmonary Endoscopy

4.2.3 Gynecological Endoscopy

4.2.4 Urological Endoscopy

4.2.5 Ear, Nose, and Throat (ENT) Endoscopy

4.3 By End User (In Value %)

4.3.1 Hospitals

4.3.2 Ambulatory Surgical Centers

4.3.3 Diagnostic Centers

4.3.4 Specialty Clinics

4.4 By Technology (In Value %)

4.4.1 High-Definition (HD) Imaging Systems

4.4.2 3D Endoscopy

4.4.3 Narrow Band Imaging (NBI)

4.4.4 Capsule Endoscopy

4.5 By Region (In Value %)

4.5.1 North-East

4.5.2 South

4.5.3 Midwest

4.5.4 West

5. USA Endoscopic Devices Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Olympus Corporation

5.1.2 Karl Storz SE & Co. KG

5.1.3 Boston Scientific Corporation

5.1.4 Stryker Corporation

5.1.5 Fujifilm Holdings Corporation

5.1.6 Pentax Medical

5.1.7 Medtronic plc

5.1.8 Smith & Nephew plc

5.1.9 Hoya Corporation

5.1.10 Richard Wolf GmbH

5.1.11 Cook Medical

5.1.12 B. Braun Melsungen AG

5.1.13 CONMED Corporation

5.1.14 Ethicon (Johnson & Johnson)

5.1.15 Intuitive Surgical, Inc.

5.2 Cross Comparison Parameters (Employee Count, Headquarters Location, Product Portfolio, R&D Investments, Market Share, Revenue, Strategic Partnerships, Inception Year)

5.3 Market Share Analysis

5.4 Strategic Initiatives (Product Innovation, Partnerships, Collaborations, Regional Expansion)

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Government Funding and Grants

5.8 Private Equity and Venture Capital Investments

6. USA Endoscopic Devices Market Regulatory Framework

6.1 FDA Regulations and Approvals

6.2 Certification Processes (ISO Certifications, CE Marking)

6.3 Environmental Compliance

7. USA Endoscopic Devices Market Future Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Growth (Aging Population, New Technology Adoption, Reimbursement Reforms)

8. USA Endoscopic Devices Market Future Segmentation

8.1 By Device Type (In Value %)

8.2 By Application (In Value %)

8.3 By End User (In Value %)

8.4 By Technology (In Value %)

8.5 By Region (In Value %)

9. USA Endoscopic Devices Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The research process begins with constructing an ecosystem map that includes all the major stakeholders in the USA endoscopic devices market. Extensive desk research is conducted to gather industry-specific data, focusing on key variables that affect the market, such as technological advancements and regulatory changes.

Step 2: Market Analysis and Construction

Historical data pertaining to the USA endoscopic devices market is analyzed. This involves assessing market penetration, revenue trends, and the adoption of advanced endoscopy technologies. The data is then used to build a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

The market hypotheses are validated through consultations with industry experts, including professionals from leading endoscopy device manufacturers and healthcare providers. These consultations help verify the accuracy of the market estimates.

Step 4: Research Synthesis and Final Output

In the final step, data from both top-down and bottom-up approaches is synthesized to provide a validated report. Insights from multiple stakeholders in the market are included to ensure that the analysis is comprehensive and accurate.

Frequently Asked Questions

01. How big is the USA Endoscopic Devices Market?

The USA endoscopic devices market is valued at USD 6 billion, driven by the increasing demand for minimally invasive surgeries and technological advancements in endoscopy equipment.

02. What are the challenges in the USA Endoscopic Devices Market?

Key challenges in the USA endoscopic devices market include the high cost of advanced endoscopic devices, stringent regulatory approvals, and the lack of a skilled workforce for performing complex endoscopic procedures.

03. Who are the major players in the USA Endoscopic Devices Market?

Major players in the USA endoscopic devices market include Olympus Corporation, Boston Scientific Corporation, Stryker Corporation, Fujifilm Holdings Corporation, and Medtronic plc. These companies dominate due to their broad product portfolios and innovative technologies.

04. What are the growth drivers of the USA Endoscopic Devices Market?

Growth drivers in the USA endoscopic devices market include the rising prevalence of chronic diseases, technological advancements in endoscopy, and the increasing demand for minimally invasive procedures. The integration of AI in diagnostics is also a significant growth factor.

05. What are the future trends in the USA Endoscopic Devices Market?

Future trends in the USA endoscopic devices market include the growing adoption of robotic-assisted endoscopy, the integration of AI in imaging systems, and the increasing use of disposable endoscopes to reduce infection risks.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.