USA Gallium Nitride Semiconductor Devices Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD3809

October 2024

82

About the Report

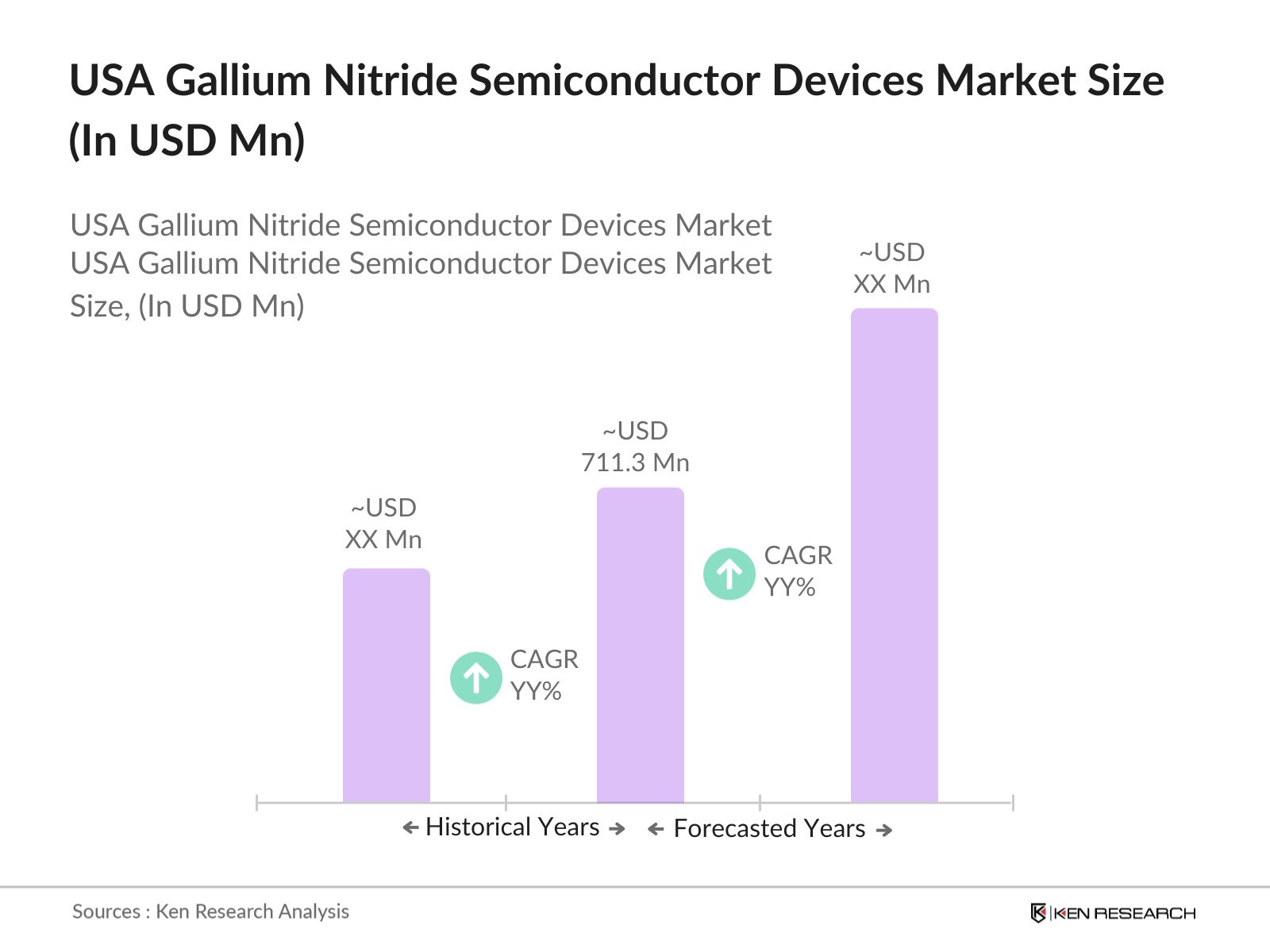

USA Gallium Nitride Semiconductor Devices Market Overview

- The USA Gallium Nitride (GaN) Semiconductor Devices Market is valued at USD 711.3 million, driven by increasing adoption in the power electronics, automotive, and telecommunications industries. GaN devices provide significant advantages in terms of efficiency, power density, and performance, especially in applications like RF amplifiers, electric vehicle (EV) inverters, and power conversion systems.

- The market is dominated by cities and regions with strong semiconductor manufacturing bases, such as California, Texas, and Arizona. These regions are home to several key industry players and benefit from well-established supply chains, access to skilled labor, and government support through initiatives like the CHIPS Act.

- The U.S. Department of Defense has been funding GaN research projects aimed at improving performance in military applications. In 2024, the DoD allocated USD 50 million toward the development of GaN-based radar and communication systems, seeking to enhance the country's defense capabilities with more efficient and reliable semiconductor technology.

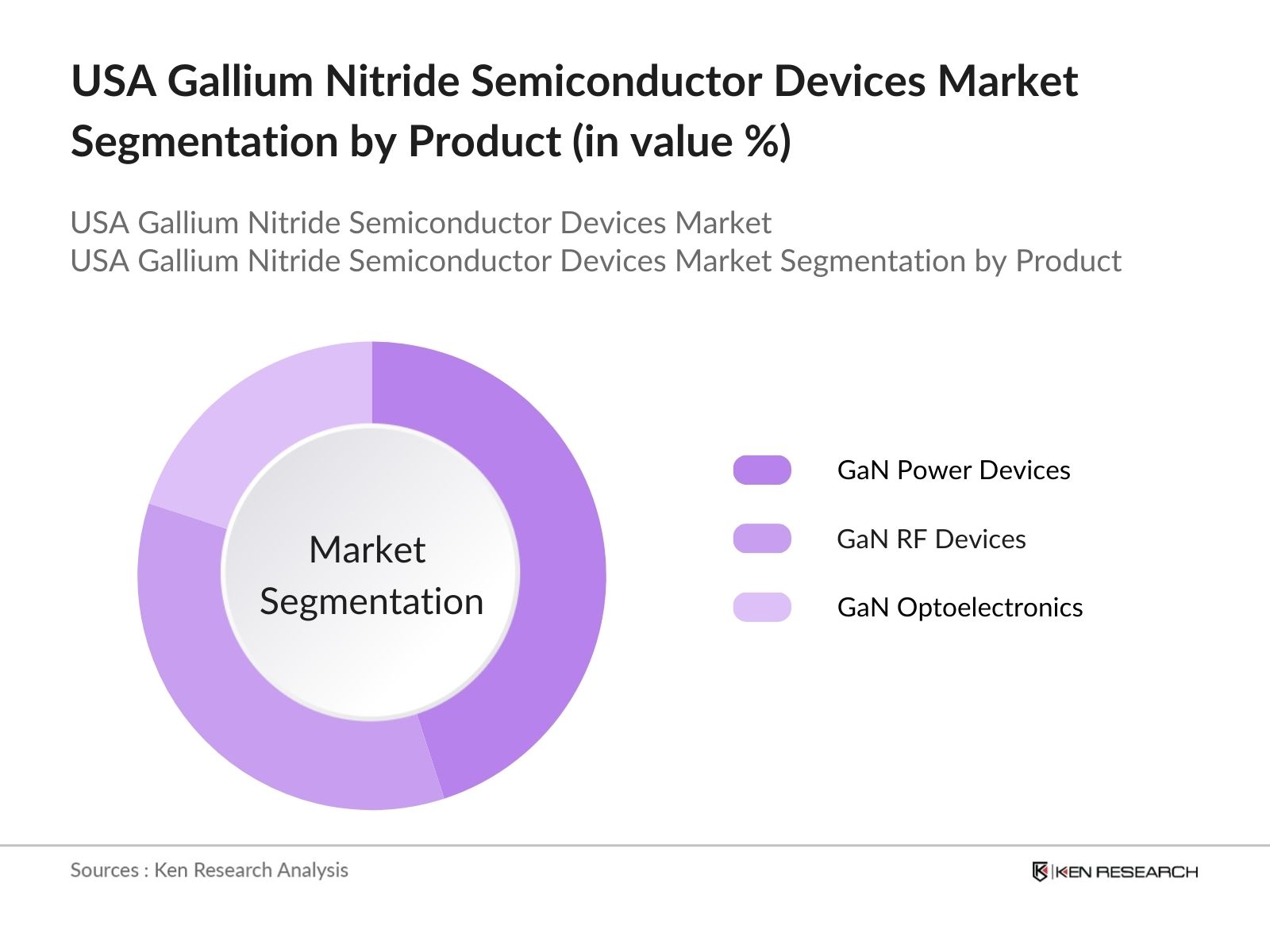

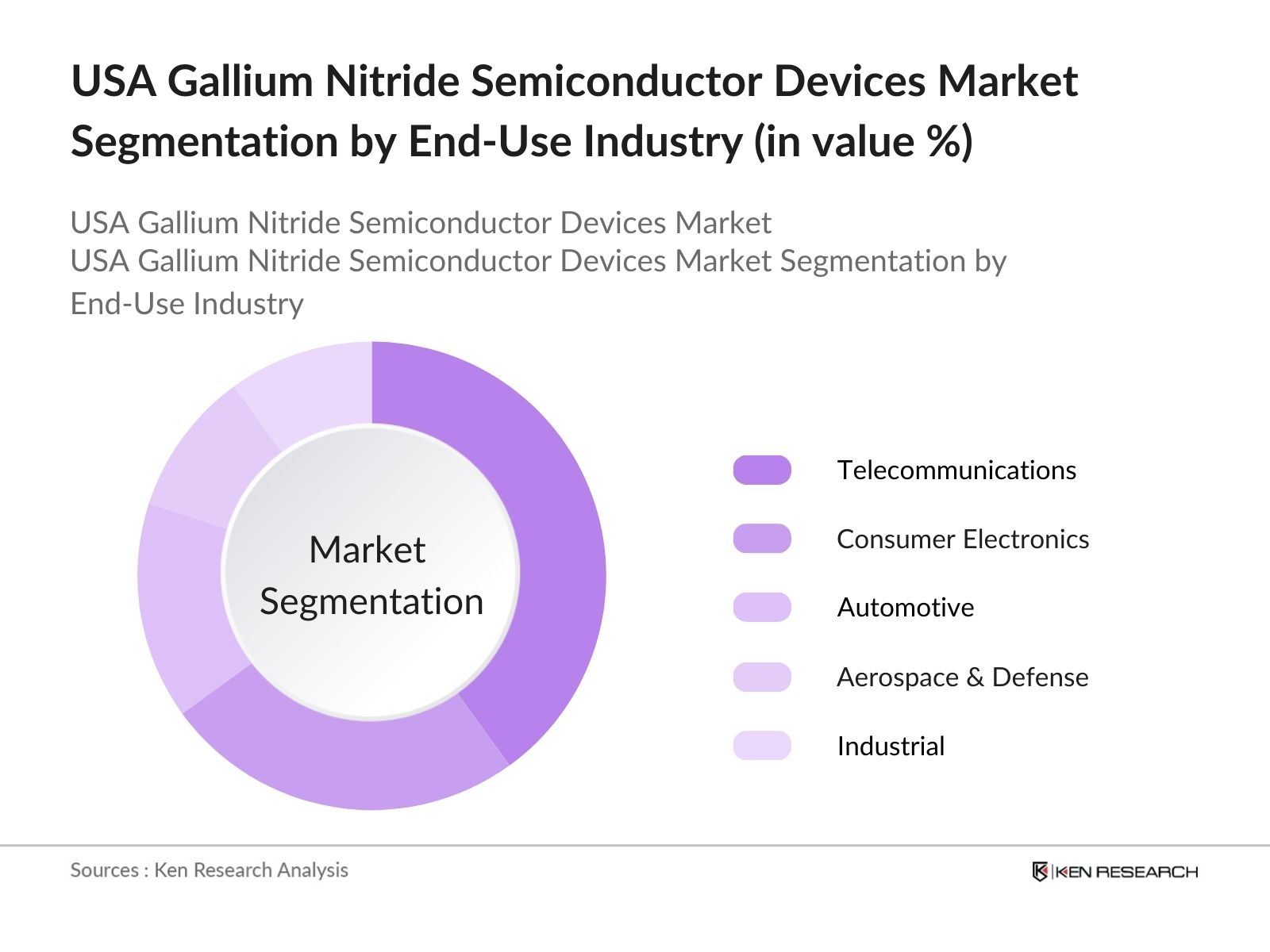

USA Gallium Nitride Semiconductor Devices Market Segmentation

By Product Type: The market is segmented by product type into GaN power devices, GaN RF devices, and GaN optoelectronics devices (LEDs, lasers). GaN power devices have emerged as the dominant market segment due to their application in high-efficiency power converters, electric vehicles, and renewable energy systems. The ability of GaN power devices to reduce energy loss and improve switching performance has led to their growing popularity, especially as industries focus on reducing energy consumption.

By End-Use Industry: The market is also segmented by end-use industry into consumer electronics, telecommunications, automotive, aerospace & defense, and industrial. The telecommunications segment is currently leading the market, primarily driven by the widespread deployment of 5G networks that require high-performance GaN RF devices. GaN semiconductors are critical in 5G base stations and other wireless communication infrastructure due to their ability to handle high frequencies and power densities.

USA Gallium Nitride Semiconductor Devices Market Competitive Landscape

The market is dominated by several global and domestic players that have market shares due to their strong research and development capabilities, extensive product portfolios, and well-established manufacturing infrastructure.

|

Company Name |

Year Established |

Headquarters |

R&D Expenditure (USD) |

GaN Patents |

Revenue from GaN |

Technology Licenses |

No. of Manufacturing Facilities |

Presence in Telecom Industry |

|

Wolfspeed Inc. |

1987 |

Durham, NC |

||||||

|

Qorvo Inc. |

2015 |

Greensboro, NC |

||||||

|

GaN Systems Inc. |

2008 |

Ottawa, Canada |

||||||

|

Infineon Technologies AG |

1999 |

Neubiberg, Germany |

||||||

|

Texas Instruments Incorporated |

1930 |

Dallas, TX |

USA Gallium Nitride Semiconductor Market Analysis

Market Growth Drivers

- Increased Adoption in Electric Vehicles (EVs): The demand for Gallium Nitride (GaN) semiconductor devices in electric vehicles (EVs) is growing due to their efficiency in power conversion and charging systems. In 2024, the U.S. EV market is expected to reach over 2.4 million units, requiring advanced semiconductor solutions. GaN devices offer faster charging times and higher efficiency, directly supporting this growing sector. GaNs low heat dissipation and compact size reduce system costs, driving their adoption in the EV sector.

- Defense and Aerospace Sector Expansion: The U.S. Department of Defense's spending on advanced radar and satellite systems that use GaN semiconductors for superior power handling has seen an increase. In 2024, the budget for these technologies surpassed USD 100 billion, and GaN devices are key to enhancing the performance of defense communication systems and radar technology. Their higher power density and thermal conductivity improve reliability in harsh environments, making them vital in defense applications.

- 5G Infrastructure Rollout: The deployment of 5G networks across the U.S. has seen investment, with telecommunications companies spending USD 30 billion in 2024 on network infrastructure. GaN devices are increasingly used in 5G base stations for high-frequency signal transmission, offering improved performance over traditional silicon-based devices. Their ability to operate at higher frequencies and voltages is crucial for the efficient deployment of 5G infrastructure.

Market Challenges

- Limited Material Availability: GaN requires substrates such as silicon carbide (SiC), which are less abundant and more costly than silicon. In 2024, the global availability of high-quality SiC substrates stood at around 10,000 metric tons, significantly lower than the demand. This scarcity of raw materials contributes to the high cost and slow adoption of GaN technology in industries requiring mass production.

- Thermal Management Issues: While GaN semiconductors offer better efficiency, they face thermal management challenges, especially in high-power applications. The thermal conductivity of GaN is lower than that of SiC, making it difficult to manage heat dissipation effectively in some high-temperature environments. In 2024, research from key U.S. defense contractors highlighted that thermal management costs for GaN devices added around 20% to the overall system cost, particularly in high-performance defense systems.

USA Gallium Nitride Semiconductor Market Future Outlook

Over the next five years, the USA Gallium Nitride Semiconductor Devices industry is expected to show growth driven by advancements in 5G technology, increased adoption of electric vehicles, and rising demand for energy-efficient power devices. The ongoing transition from traditional silicon-based semiconductors to GaN-based solutions will continue to drive this growth, especially in high-demand sectors such as telecommunications, consumer electronics, and automotive.

Future Market Opportunities

- GaN's Role in Powering Electric Aircraft: In the coming years, the U.S. will see an increased use of GaN semiconductors in electric aircraft power systems, particularly for high-efficiency power conversion. By 2029, industry experts forecast that around 200 electric aircraft will be operational in the U.S., each using GaN components valued at USD 100,000 to support lightweight and high-efficiency power systems.

- Increasing Demand for GaN in 5G and Beyond: Over the next five years, GaN devices will play a critical role in the expansion of 5G infrastructure across the U.S., and they will also be essential for upcoming 6G technologies. By 2029, it is projected that over 50,000 5G base stations in the U.S. will integrate GaN technology, with each station requiring an estimated USD 10,000 worth of GaN components, driving the market.

Scope of the Report

|

Product Type |

GaN Power Devices |

|

GaN RF Devices |

|

|

GaN Optoelectronic Devices (LEDs, Lasers) |

|

|

End-Use Industry |

Consumer Electronics |

|

Automotive |

|

|

Telecommunications |

|

|

Aerospace & Defense |

|

|

Industrial |

|

|

Wafer Size |

2-Inch Wafers |

|

4-Inch Wafers |

|

|

6-Inch Wafers |

|

|

8-Inch Wafers |

|

|

Substrate Type |

GaN-on-Silicon (Si) |

|

GaN-on-Silicon Carbide (SiC) |

|

|

GaN-on-Sapphire |

|

|

Region |

North |

|

East |

|

|

South |

|

|

West |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Semiconductor Manufacturers

Telecommunication Companies

Electric Vehicle Manufacturers

Consumer Electronics Manufacturers

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., U.S. Department of Commerce, CHIPS Act Administration)

Power Electronics Industry

Companies

Players Mentioned in the Report:

Wolfspeed Inc.

Qorvo Inc.

GaN Systems Inc.

Infineon Technologies AG

Texas Instruments Incorporated

ON Semiconductor Corporation

MACOM Technology Solutions Holdings

STMicroelectronics N.V.

Northrop Grumman Corporation

Microchip Technology Inc.

Skyworks Solutions Inc.

Panasonic Corporation

Sumitomo Electric Industries Ltd.

Efficient Power Conversion Corporation (EPC)

Transphorm Inc.

Table of Contents

1. USA Gallium Nitride Semiconductor Devices Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. USA Gallium Nitride Semiconductor Devices Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. USA Gallium Nitride Semiconductor Devices Market Analysis

3.1. Growth Drivers

3.1.1. Adoption in Power Electronics (Wide Bandgap Materials)

3.1.2. Demand from RF Devices in Telecom (High-Frequency Applications)

3.1.3. Electric Vehicle Penetration (GaN-based Inverters)

3.1.4. Increasing Data Centers (Energy Efficiency and Heat Dissipation)

3.2. Market Challenges

3.2.1. High Manufacturing Costs (Substrate Material Costs)

3.2.2. Reliability Concerns at High Voltages (Thermal Management Issues)

3.2.3. Integration with Existing Silicon Technologies

3.3. Opportunities

3.3.1. Technological Advancements in 5G Infrastructure (RF Power Devices)

3.3.2. Expansion in Consumer Electronics (Fast-Charging Applications)

3.3.3. Growth in Satellite Communication Systems (High Power/Low Noise Amplifiers)

3.4. Trends

3.4.1. Increased Adoption in Military and Aerospace Applications (High Power, High Temperature Devices)

3.4.2. Miniaturization of GaN Devices (Integration with IoT Devices)

3.4.3. Migration to GaN-on-SiC (Silicon Carbide Substrate)

3.5. Government Regulations

3.5.1. Export Controls on Semiconductor Materials

3.5.2. Environmental Regulations (E-Waste Management, Lead-free Packaging)

3.5.3. Government Subsidies for Semiconductor Manufacturing (CHIPS Act)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Material Suppliers, Device Manufacturers, End-Users)

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

4. USA Gallium Nitride Semiconductor Devices Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. GaN Power Devices

4.1.2. GaN RF Devices

4.1.3. GaN Optoelectronic Devices (LEDs, Lasers)

4.2. By End-Use Industry (In Value %)

4.2.1. Consumer Electronics

4.2.2. Automotive

4.2.3. Telecommunications

4.2.4. Aerospace & Defense

4.2.5. Industrial

4.3. By Wafer Size (In Value %)

4.3.1. 2-Inch Wafers

4.3.2. 4-Inch Wafers

4.3.3. 6-Inch Wafers

4.3.4. 8-Inch Wafers

4.4. By Substrate Type (In Value %)

4.4.1. GaN-on-Silicon (Si)

4.4.2. GaN-on-Silicon Carbide (SiC)

4.4.3. GaN-on-Sapphire

4.5. By Region (In Value %)

4.5.1. North

4.5.2. East

4.5.3. South

4.5.4. West

5. USA Gallium Nitride Semiconductor Devices Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Wolfspeed Inc.

5.1.2. Qorvo Inc.

5.1.3. GaN Systems Inc.

5.1.4. Efficient Power Conversion Corporation (EPC)

5.1.5. Transphorm Inc.

5.1.6. Infineon Technologies AG

5.1.7. Texas Instruments Incorporated

5.1.8. ON Semiconductor Corporation

5.1.9. MACOM Technology Solutions Holdings

5.1.10. STMicroelectronics N.V.

5.1.11. Northrop Grumman Corporation

5.1.12. Microchip Technology Inc.

5.1.13. Skyworks Solutions Inc.

5.1.14. Panasonic Corporation

5.1.15. Sumitomo Electric Industries Ltd.

5.2 Cross Comparison Parameters (R&D Expenditure, Technology Licensing, Key Patent Holdings, End-User Focus, Market Presence, Revenue from GaN Segment, Number of GaN Patents, Manufacturing Capacity)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. USA Gallium Nitride Semiconductor Devices Market Regulatory Framework

6.1. Semiconductor Export Regulations

6.2. Compliance with Environmental Standards

6.3. Certification and Quality Assurance Processes

7. USA Gallium Nitride Semiconductor Devices Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Gallium Nitride Semiconductor Devices Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By End-Use Industry (In Value %)

8.3. By Wafer Size (In Value %)

8.4. By Substrate Type (In Value %)

8.5. By Region (In Value %)

9. USA Gallium Nitride Semiconductor Devices Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves creating an ecosystem map covering all significant stakeholders in the USA Gallium Nitride Semiconductor Devices Market. This step is supported by extensive desk research and the use of secondary and proprietary databases to gather comprehensive market-level data. The goal is to identify the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data relevant to the USA GaN Semiconductor Devices Market. This includes an assessment of market penetration, revenue generation ratios between product segments, and an evaluation of technological advancements that have impacted the market.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through direct consultations with industry experts, using computer-assisted telephone interviews (CATIs) and industry surveys. This feedback provides valuable insights into operational and financial metrics, contributing to accurate market forecasts.

Step 4: Research Synthesis and Final Output

In the final phase, we engage directly with GaN semiconductor manufacturers and suppliers to acquire detailed insights into product sales, demand trends, and manufacturing capacities. These insights are integrated with the bottom-up approach data to produce a validated and accurate report of the USA GaN Semiconductor Devices Market.

Frequently Asked Questions

01. How big is the USA Gallium Nitride Semiconductor Devices Market?

The USA GaN semiconductor devices market is valued at USD 711.3 million, driven by increasing demand from power electronics, telecommunications, and electric vehicles, where GaN technology is recognized for its superior efficiency.

02. What are the challenges in the USA Gallium Nitride Semiconductor Devices Market?

Challenges in this USA GaN semiconductor devices market include high manufacturing costs due to expensive substrate materials, thermal management issues, and integration challenges with existing silicon technologies, especially in legacy systems.

03. Who are the major players in the USA Gallium Nitride Semiconductor Devices Market?

Key players in the USA GaN semiconductor devices market include Wolfspeed Inc., Qorvo Inc., GaN Systems Inc., Infineon Technologies AG, and Texas Instruments Incorporated, who dominate the market with strong R&D efforts and significant GaN patent portfolios.

04. What are the growth drivers of the USA Gallium Nitride Semiconductor Devices Market?

The USA GaN semiconductor devices market is primarily driven by advancements in 5G infrastructure, increased demand for energy-efficient devices in data centers and renewable energy, and the growing adoption of electric vehicles that require high-performance power electronics.

05. What is the future outlook for the USA Gallium Nitride Semiconductor Devices Market?

The USA GaN semiconductor devices market is expected to experience strong growth in the coming years, driven by government support for domestic semiconductor manufacturing, advancements in power conversion technologies, and the increasing penetration of GaN in new application areas like space and defense.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.