USA Generator Market Outlook to 2030

Region:North America

Author(s):Shambhavi

Product Code:KROD2813

Region:North America

Author(s):Shambhavi

Product Code:KROD2813

November 2024

98

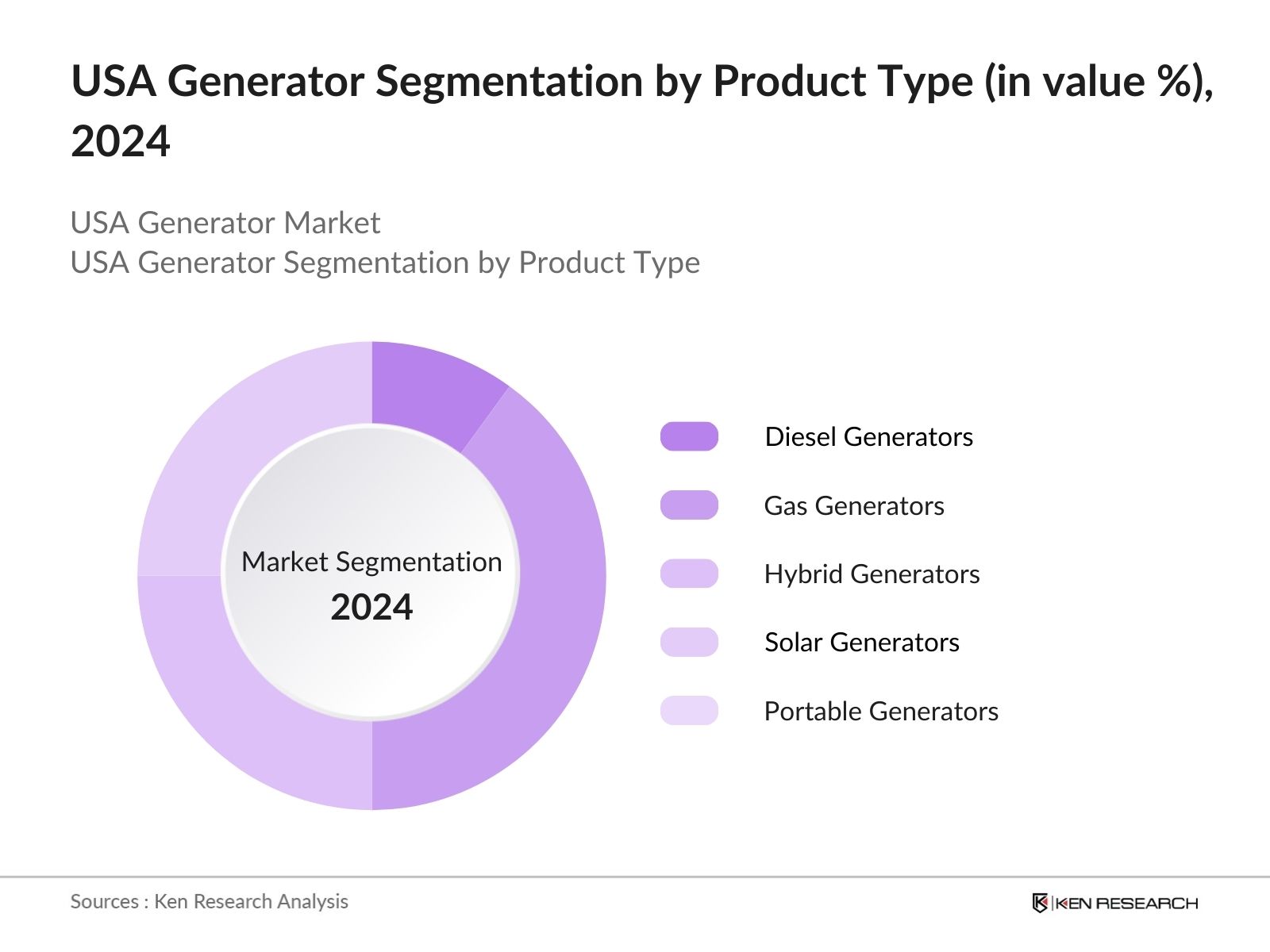

By Product Type

The USA generator market is segmented by product type into diesel generators, gas generators, hybrid generators, solar generators, and portable generators. Diesel generators maintain a dominant share due to their widespread application in industries such as oil and gas, construction, and manufacturing. The preference for diesel arises from its reliability, fuel efficiency, and ability to generate higher power output compared to alternative options. The robust supply chain for diesel fuel also contributes to its leadership within the market.

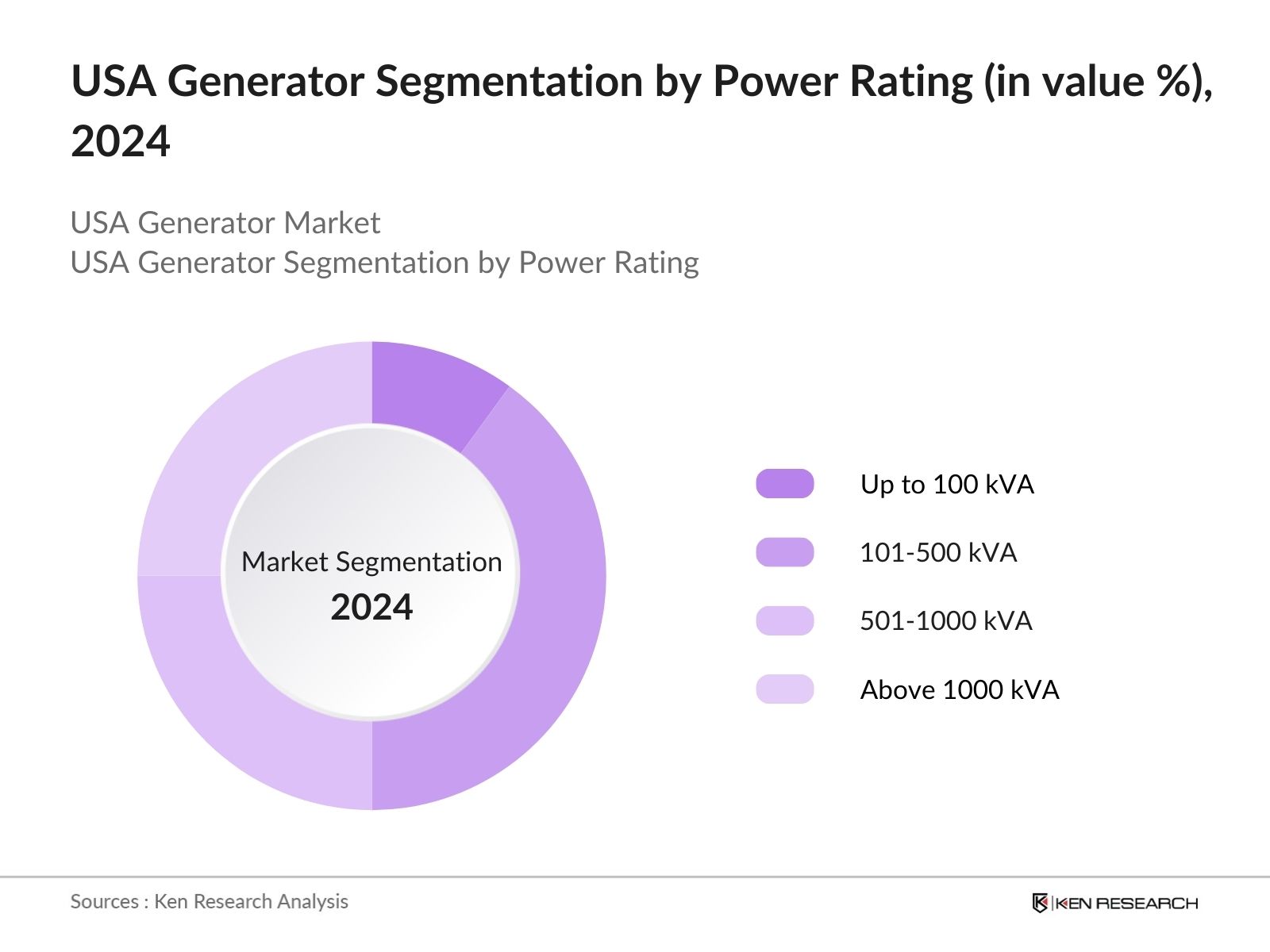

By Power Rating

The generator market is further segmented by power rating, including generators with ratings of up to 100 kVA, 101-500 kVA, 501-1000 kVA, and above 1000 kVA. Generators in the 101-500 kVA segment hold the largest share in the U.S. market, driven by their versatile use in both commercial and small industrial applications. Their adaptability in powering mid-sized facilities and meeting the energy needs of essential services makes them a popular choice across various sectors.

The USA generator market is dominated by key global and domestic players, with the competitive landscape shaped by product innovation, technological advancement, and strategic collaborations. Major players such as Cummins, Caterpillar, and Generac have established their dominance through strong distribution networks and a diverse portfolio of products catering to different sectors.

|

Company Name |

Establishment Year |

Headquarters |

Product Range |

Revenue (USD) |

R&D Investments |

No. of Employees |

Strategic Alliances |

Global Reach |

Fuel Type Specialization |

|

Cummins Inc. |

1919 |

Columbus, Indiana |

|||||||

|

Caterpillar Inc. |

1925 |

Deerfield, Illinois |

|||||||

|

Generac Power Systems |

1959 |

Waukesha, Wisconsin |

|||||||

|

Kohler Co. |

1873 |

Kohler, Wisconsin |

|||||||

|

Briggs & Stratton Corporation |

1908 |

Milwaukee, Wisconsin |

The U.S. generator market remains highly competitive, with companies continuously enhancing their technological capabilities, focusing on hybrid generators, and exploring renewable energy solutions. The market is also shaped by mergers and acquisitions, with major players leveraging their financial and operational strengths to gain a competitive edge.

Market Challenges

Over the next five years, the USA generator market is expected to witness substantial growth driven by increasing reliance on digital infrastructure, the need for resilient backup power, and rising energy demand across various sectors. Technological advancements in smart generators, the integration of renewable energy sources, and government initiatives supporting clean energy are key factors propelling market expansion. Additionally, growing awareness regarding energy efficiency and sustainability will likely lead to increased adoption of hybrid and solar-powered generators.

Opportunities

|

Segment |

Sub-Segments |

|

Product Type |

Diesel Generators, Gas Generators, Hybrid Generators, Solar Generators, Portable Generators |

|

Power Rating |

Up to 100 kVA, 101-500 kVA, 501-1000 kVA, Above 1000 kVA |

|

Application |

Residential, Commercial, Industrial, Data Centers, Healthcare Facilities |

|

End User |

Utility Providers, Oil & Gas, Manufacturing, Telecom, Construction |

|

Region |

North-East, Midwest, South, West |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Energy Demand (Energy Consumption Trends)

3.1.2. Rising Demand for Backup Power (Residential, Commercial, and Industrial Sectors)

3.1.3. Government Support for Clean Energy (Federal Energy Policies, Incentives for Renewable Energy Adoption)

3.1.4. Technological Advancements in Generator Design (Product Efficiency, Low Emission Generators)

3.2. Market Challenges

3.2.1. High Initial Costs (Capital Investment)

3.2.2. Stringent Environmental Regulations (EPA Standards, Emission Regulations)

3.2.3. Fluctuating Fuel Prices (Diesel, Natural Gas)

3.2.4. Competition from Renewable Energy Sources (Solar, Wind Energy Alternatives)

3.3. Opportunities

3.3.1. Expansion into Rural and Off-Grid Areas (Infrastructure Development)

3.3.2. Increasing Adoption of Hybrid Generators (Energy Efficiency, Sustainable Solutions)

3.3.3. Growth of Data Centers and Telecom Industries (Critical Backup Power Demand)

3.3.4. International Export Opportunities (Emerging Markets, Global Expansion)

3.4. Trends

3.4.1. Integration with Smart Grid Systems (Energy Management, Monitoring)

3.4.2. Adoption of Digital and Remote Monitoring (IoT Integration, Predictive Maintenance)

3.4.3. Growing Preference for Renewable Hybrid Solutions (Solar-Diesel Hybrids, Battery Integration)

3.4.4. Urbanization and Industrialization in the U.S. (Construction, Commercial Developments)

3.5. Government Regulations

3.5.1. EPA Standards for Emissions (Tier 4 Regulations, Air Quality Standards)

3.5.2. Federal Incentives for Renewable Energy (Tax Credits, Rebates for Low-Emission Generators)

3.5.3. Energy Efficiency Standards (DOE Policies, Efficiency Rating Systems)

3.5.4. Infrastructure Investment and Jobs Act (Funding for Energy Infrastructure Projects)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Diesel Generators

4.1.2. Gas Generators

4.1.3. Hybrid Generators

4.1.4. Solar Generators

4.1.5. Portable Generators

4.2. By Power Rating (In Value %)

4.2.1. Up to 100 kVA

4.2.2. 101-500 kVA

4.2.3. 501-1000 kVA

4.2.4. Above 1000 kVA

4.3. By Application (In Value %)

4.3.1. Residential

4.3.2. Commercial

4.3.3. Industrial

4.3.4. Data Centers

4.3.5. Healthcare Facilities

4.4. By End User (In Value %)

4.4.1. Utility Providers

4.4.2. Oil & Gas

4.4.3. Manufacturing

4.4.4. Telecom

4.4.5. Construction

4.5. By Region (In Value %)

4.5.1. North-East

4.5.2. Midwest

4.5.3. South

4.5.4. West

5.1. Detailed Profiles of Major Companies

5.1.1. Caterpillar Inc.

5.1.2. Cummins Inc.

5.1.3. Generac Power Systems

5.1.4. Kohler Co.

5.1.5. Briggs & Stratton Corporation

5.1.6. Rolls-Royce Power Systems

5.1.7. Atlas Copco AB

5.1.8. Honda Motor Co.

5.1.9. MTU Onsite Energy

5.1.10. John Deere

5.1.11. Wacker Neuson SE

5.1.12. Doosan Portable Power

5.1.13. Yanmar Holdings Co.

5.1.14. Mitsubishi Heavy Industries

5.1.15. Aksa Power Generation

5.2. Cross Comparison Parameters (Headquarters, Product Portfolio, Revenue, Market Share, R&D Investments, Fuel Type Specialization, Geographical Reach, Strategic Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives (New Product Launches, Collaborations, Joint Ventures)

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Venture Capital Funding, Private Equity)

5.7. Government Grants and Subsidies

6.1. Emission Standards (EPA Tier Standards)

6.2. Compliance Requirements (Safety Standards, Environmental Audits)

6.3. Certification Processes (ISO Certifications, Industry Certifications)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Power Rating (In Value %)

8.3. By Application (In Value %)

8.4. By End User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial step involved developing a detailed understanding of the USA generator market by mapping out key stakeholders, including manufacturers, suppliers, and end-users. This process was based on extensive secondary research and data collection from industry reports, government sources, and proprietary databases. The aim was to identify critical factors influencing the market.

Historical market data was collected to assess growth trends and developments within the U.S. generator market. Analysis of production and consumption patterns, as well as market penetration rates, was conducted to establish a detailed understanding of the competitive landscape. Revenue and service quality indicators were evaluated to validate market size estimates.

Our market projections were refined through consultation with industry experts, utilizing computer-assisted telephone interviews (CATI) and face-to-face discussions. These interviews provided valuable insights from market participants, validating key trends and strategic initiatives undertaken by leading companies in the generator market.

The final phase of research involved synthesizing data from multiple sources, including feedback from key market players, to produce a comprehensive and validated analysis of the U.S. generator market. This phase ensured that the research output accurately reflected market dynamics, incorporating both bottom-up and top-down methodologies for robust insights.

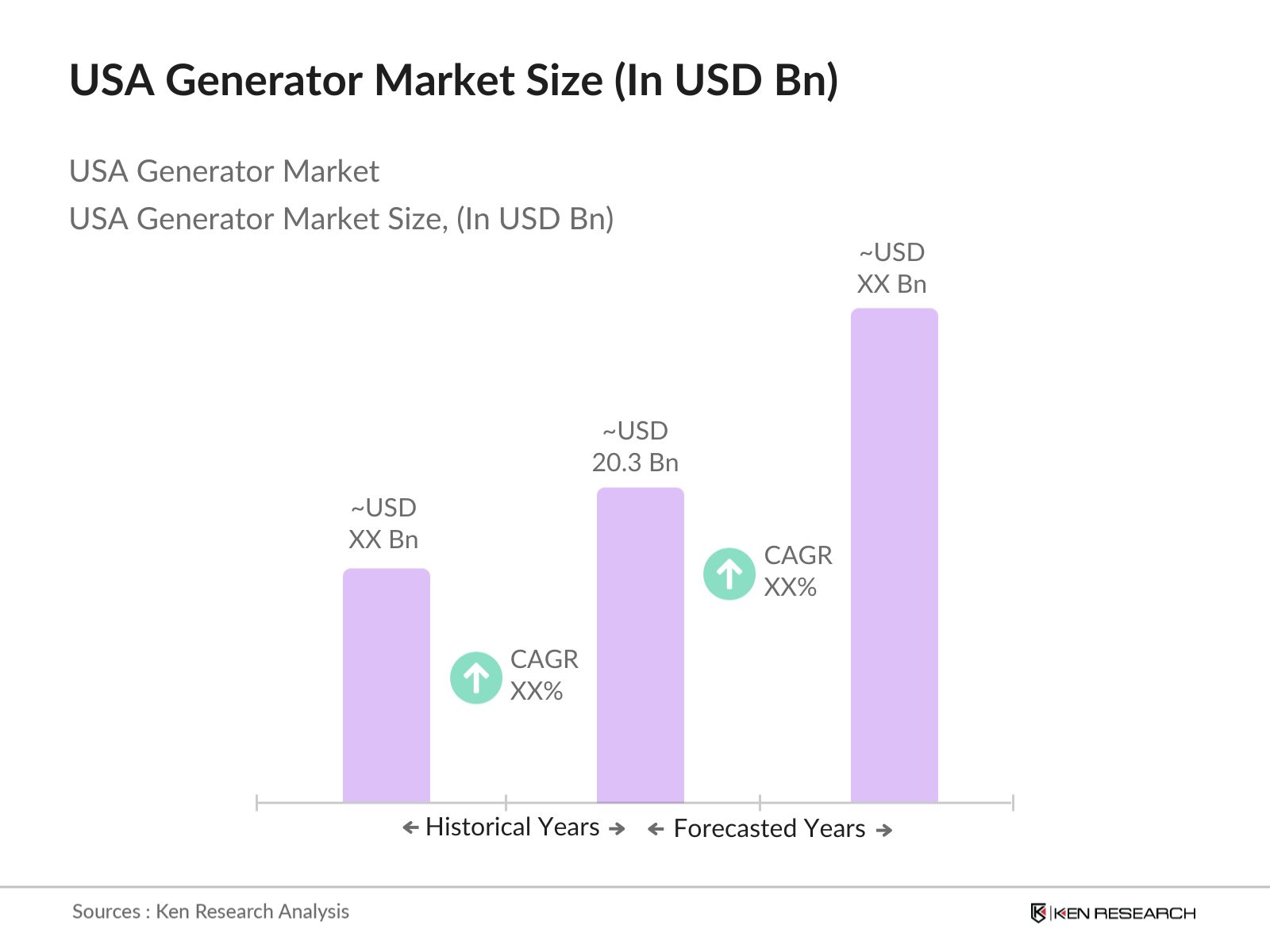

The USA generator market was valued at USD 20.3 billion, driven by increasing demand for backup power across various industries, including healthcare, telecommunications, and manufacturing.

Challenges include stringent environmental regulations, fluctuating fuel prices, and competition from renewable energy sources. The rising focus on sustainability is pushing companies to innovate, adding pressure to stay compliant while maintaining profitability.

Key players include Cummins Inc., Caterpillar Inc., Generac Power Systems, Kohler Co., and Briggs & Stratton Corporation. These companies dominate due to their extensive product portfolios, strong R&D investments, and global distribution networks.

The market is driven by increasing energy demand, the need for reliable backup power solutions, and advancements in smart generator technology. Additionally, government support for clean energy initiatives is fostering the growth of hybrid and renewable-powered generators.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.