USA Grocery & Food Market Outlook to 2030

Region:North America

Author(s):Sanjna

Product Code:KROD11254

November 2024

86

About the Report

USA Grocery & Food Market Overview

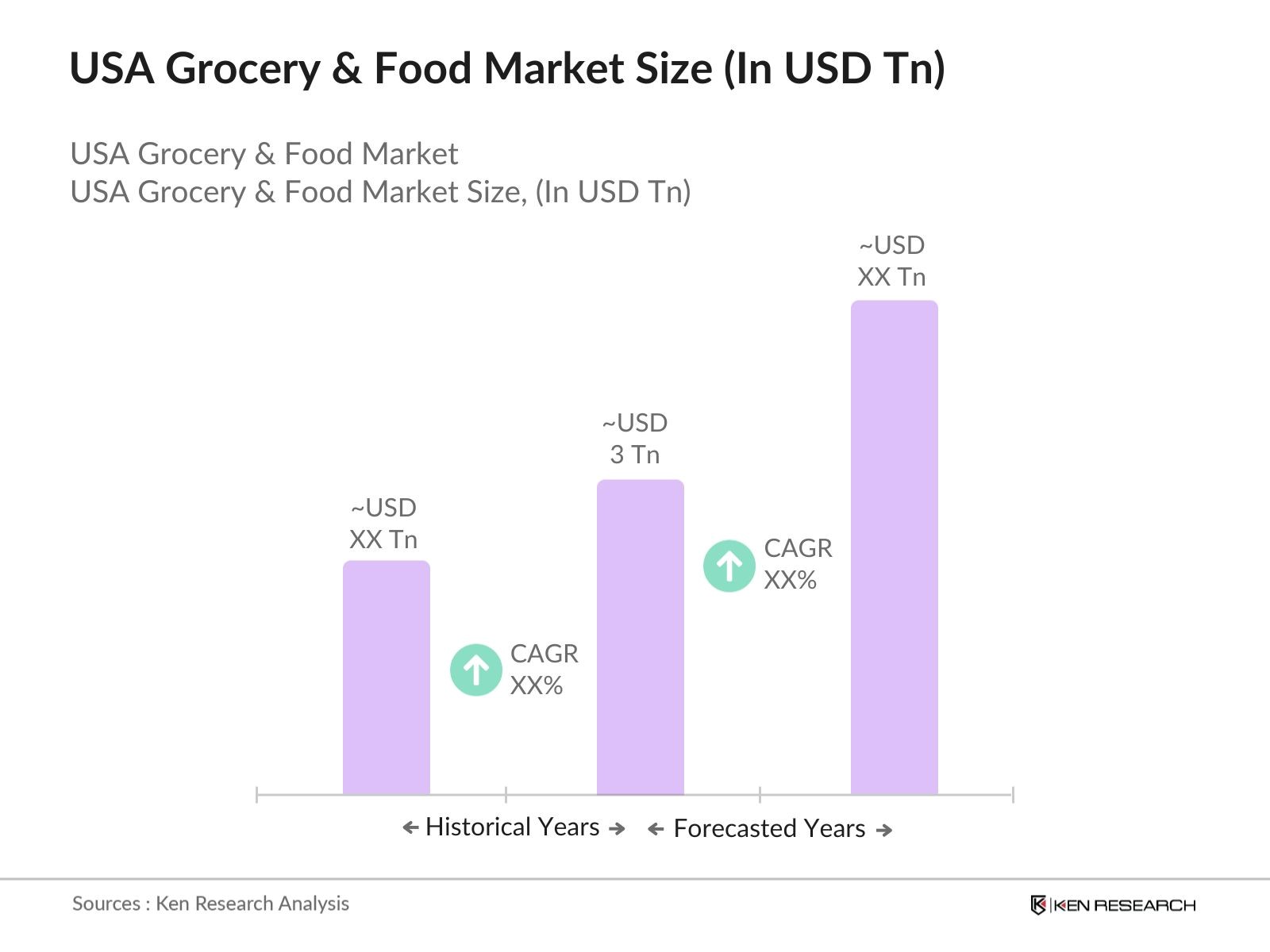

- The USA Grocery & Food Market is valued at USD 3 trillion, based on a five-year historical analysis, driven by consistent consumer demand for accessible, fresh, and diverse food options. Shifts toward organic and clean-label products, alongside the expansion of online grocery shopping, further fuel market growth. The industry is bolstered by consumer trends toward healthier and sustainable options, as well as the convenience of digital platforms that streamline the shopping experience.

- Metropolitan areas such as New York City, Los Angeles, and Chicago, and states like California and Texas, hold dominance in the USA Grocery & Food Market. These regions are characterized by high population density and greater consumer spending power, which drive demand for diverse grocery and food products. Additionally, a substantial network of retail outlets and advanced distribution infrastructure contributes to their market prominence.

- USDA organic certification standards maintain rigorous criteria for organic food production, ensuring transparency and quality. In 2023, USDA data reported a 15% rise in organic certifications, reflecting increased consumer demand for organic products. USDAs annual audits and compliance assessments drive grocery brands to maintain high standards, benefitting consumer perception and trust.

USA Grocery & Food Market Segmentation

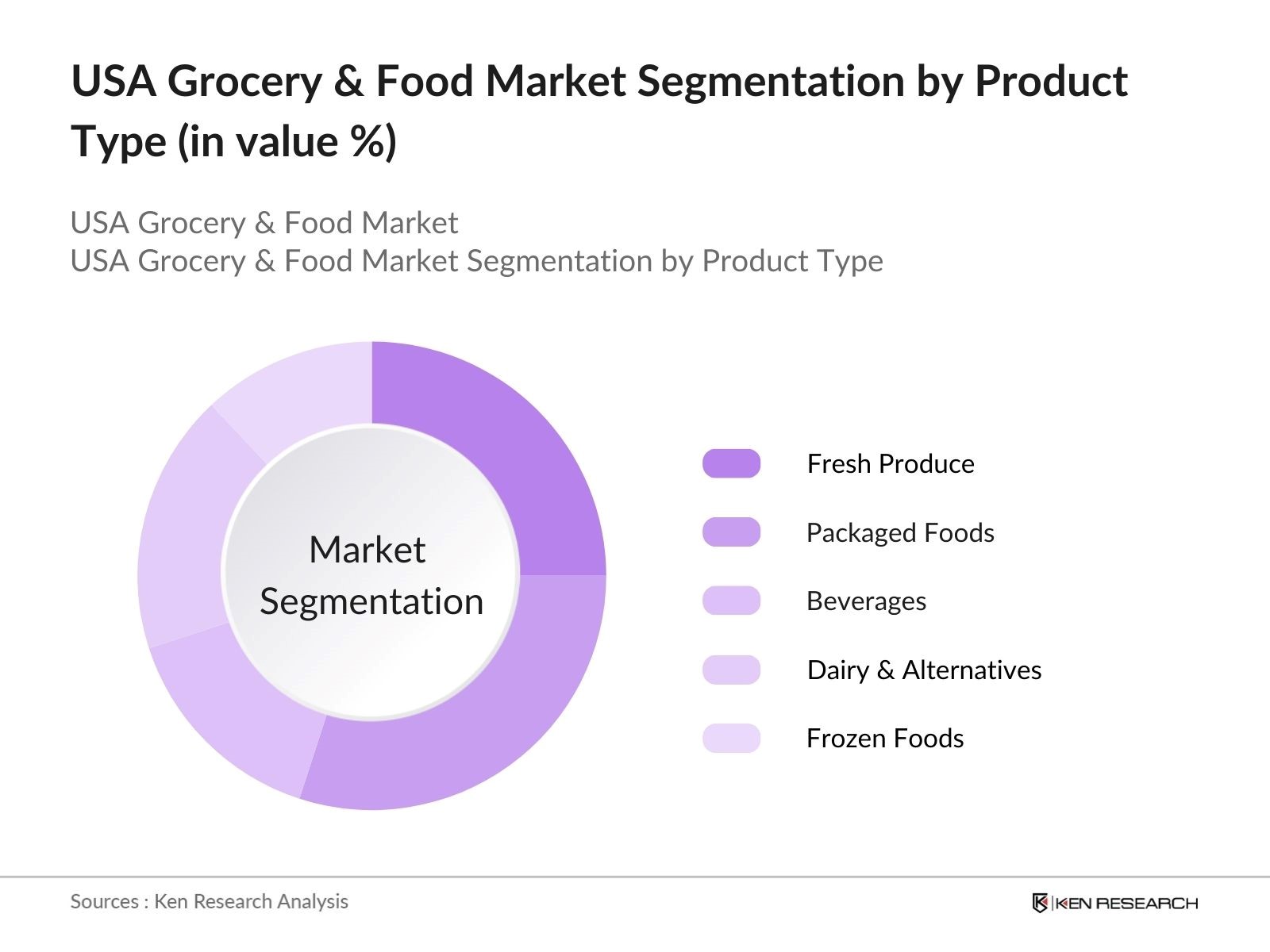

By Product Type: The USA Grocery & Food Market is segmented by product type into fresh produce, packaged foods, beverages, dairy and dairy alternatives, and frozen foods. Packaged foods currently lead the market share due to their convenience, longer shelf life, and versatility across a wide range of consumer segments. The robust demand for ready-to-eat meals, snack foods, and pantry staples has cemented the position of packaged foods as a dominant product type, with established brands driving consumer trust and loyalty.

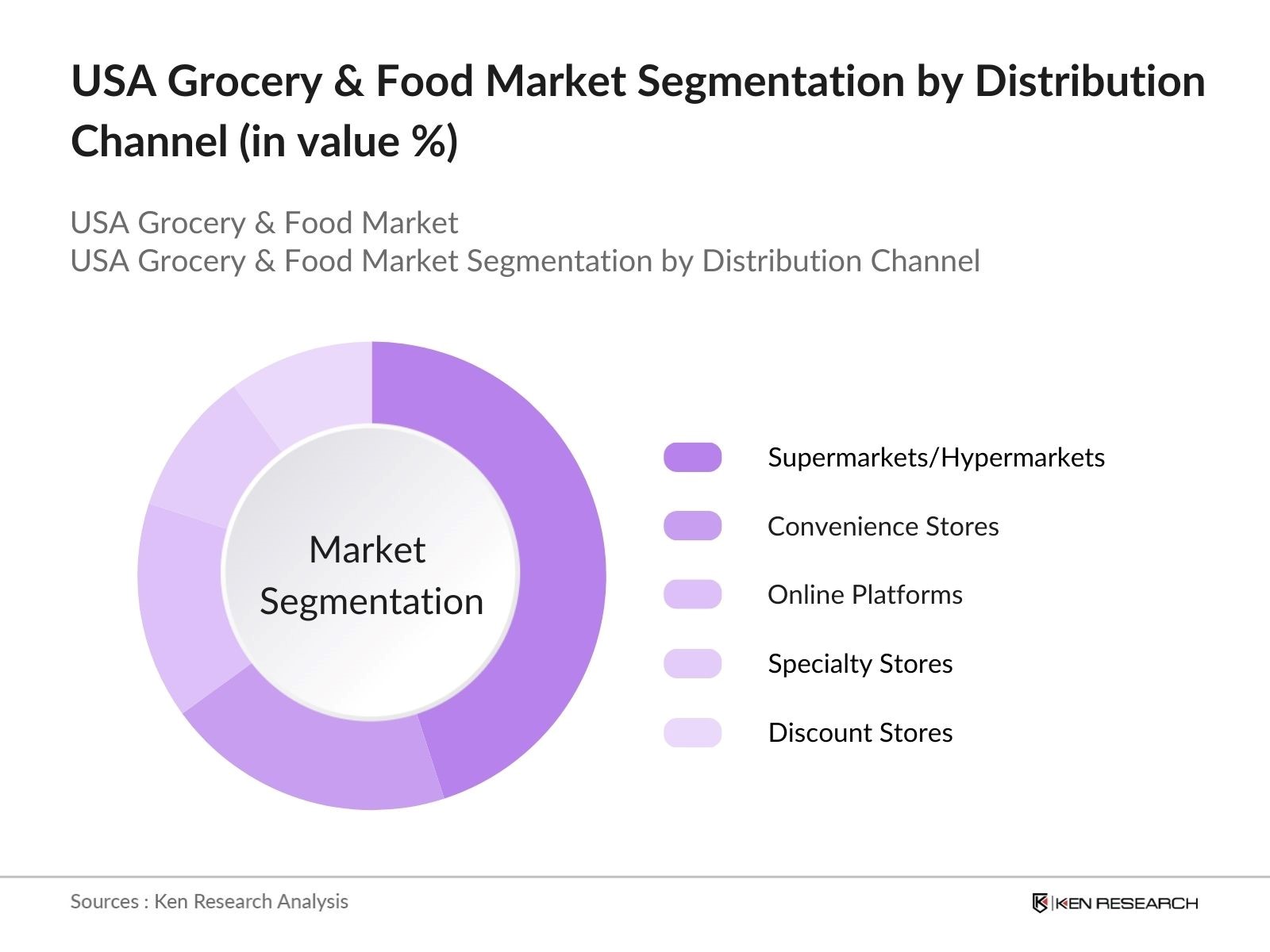

By Distribution Channel: Distribution channels in the USA Grocery & Food Market include supermarkets/hypermarkets, convenience stores, online platforms, specialty stores, and discount stores. Supermarkets and hypermarkets hold a significant share as the primary shopping destination for consumers, given their extensive selection, competitive pricing, and frequent promotional offers. Additionally, the large-scale and established presence of supermarket chains across the U.S. contributes to their dominance within the market.

USA Grocery & Food Market Competitive Landscape

The USA Grocery & Food Market is shaped by both domestic and international companies, many of which have an extensive distribution network, wide product portfolio, and high consumer trust. Major players include Walmart, Kroger, and Amazon (Whole Foods), which highlight the consolidated market power among key players.

USA Grocery & Food Market Analysis

Growth Drivers

- Rise of E-commerce in Grocery: The growth of e-commerce in the grocery sector is substantial, with nearly 12.5% of consumers purchasing groceries online in 2023. The U.S. Census Bureau reports that the retail e-commerce sales reached $1.06 trillion in 2023, with food and beverage accounting for a significant portion. High-speed internet access and digital payment adoption are key enablers, alongside expanding logistics networks improving last-mile delivery efficiency. The USDA further emphasizes increased online grocery access in rural areas, showing government-supported digital infrastructure improvements contributing to sector growth.

- Demand for Organic & Clean Label Foods: Demand for organic products is fueled by heightened consumer awareness, with organic food sales reaching $60 billion in 2023, as per USDA reports. The demographic shift, particularly among younger consumers, has driven demand for cleaner labels, with 73% of millennials reportedly seeking foods free from synthetic ingredients. This trend aligns with FDAs increased regulations for organic certifications, assuring transparency in product labeling, which builds consumer trust and drives market growth.

- Health and Wellness Trends: Health and wellness trends impact the grocery sector as 68% of American adults prioritize nutritional quality in food purchases, reports the National Health and Nutrition Examination Survey (NHANES). Demand for functional foods with added health benefits surged, especially in categories like probiotics and whole foods. Increased incidence of diet-related conditions, highlighted in CDC reports, drives consumer preference for natural, health-enhancing grocery options.

Challenges

- Logistic and Supply Chain Constraints: Supply chain disruptions due to global logistics constraints persist in 2024, with the U.S. Department of Transportation reporting increased delays in shipping lanes and port congestion. The average delivery time for imported groceries has doubled from 2022 levels, escalating costs and slowing inventory turnover. Government mandates on domestic food sourcing, per the USDA, aim to address these disruptions but increase dependence on local suppliers.

- Price Competition and Cost Inflation: Price sensitivity remains high in the grocery market, where inflationary pressures led to a 12% increase in consumer food prices in 2023. Labor and raw material costs, as outlined by the Bureau of Labor Statistics, are contributing factors, while intense price competition among retailers limits profit margins. Lower-income consumers allocate up to 30% of their budget to groceries, driving retailers to prioritize cost-efficiency to maintain market share.

USA Grocery & Food Market Future Outlook

Over the next five years, the USA Grocery & Food Market is projected to grow steadily, supported by a combination of consumer preferences for convenience, innovation in food and beverage options, and an increasing focus on sustainability. This period is expected to witness further digital transformation within the grocery sector, including the adoption of AI-driven personalized shopping experiences and the expansion of e-commerce platforms to meet changing consumer needs.

Market Opportunities

- Growth in Plant-Based and Alternative Proteins: The U.S. grocery market has witnessed rising demand for plant-based foods, with retail sales of alternative proteins reaching $7.4 billion in 2023, driven by health and environmental concerns. Government-backed sustainability programs encourage the growth of plant-based products as they reduce carbon emissions and support dietary diversity. USDA reports show a shift in dietary patterns, reflecting a broader consumer base for plant-based protein.

- Private Label Expansion in Grocery Chains: Private-label products continue to grow, representing nearly 20% of total grocery sales in 2023, according to NielsenIQ. Competitive pricing and quality improvement have strengthened consumer acceptance, especially among cost-conscious buyers. Store brands offer retailers higher margins and customer loyalty, prompting chains like Walmart and Kroger to expand private-label portfolios.

Scope of the Report

|

Segment |

Sub-Segments |

|

By Product Type |

Fresh Produce |

|

By Distribution Channel |

Supermarkets/Hypermarkets |

|

By Consumer Demographics |

Age Groups |

|

By Dietary Preferences |

Organic |

|

By Region |

Northeast |

Products

Key Target Audience

Grocery Retail Chains and Supermarkets

Food and Beverage Manufacturers

E-commerce and Online Grocery Platforms

Organic and Sustainable Product Providers

Packaging and Logistics Companies

Technology Solution Providers (for supply chain and retail solutions)

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (FDA, USDA)

Companies

Players Mentioned in the Report

Walmart Inc.

Kroger Co.

Amazon (Whole Foods Market)

Costco Wholesale Corporation

Albertsons Companies Inc.

Ahold Delhaize USA

Target Corporation

Publix Super Markets, Inc.

Sprouts Farmers Market, Inc.

Trader Joe's Company

Table of Contents

1. USA Grocery & Food Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. USA Grocery & Food Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. USA Grocery & Food Market Analysis

3.1. Growth Drivers

3.1.1. Rise of E-commerce in Grocery

3.1.2. Demand for Organic & Clean Label Foods

3.1.3. Health and Wellness Trends

3.1.4. Technological Integration in Retail

3.2. Market Challenges

3.2.1. Logistic and Supply Chain Constraints

3.2.2. Price Competition and Cost Inflation

3.2.3. Regulatory Compliance Challenges

3.3. Opportunities

3.3.1. Growth in Plant-Based and Alternative Proteins

3.3.2. Sustainable and Eco-Friendly Initiatives

3.3.3. Private Label Expansion in Grocery Chains

3.4. Trends

3.4.1. Rise of Subscription Services in Food Retail

3.4.2. Increasing Demand for Ready-to-Eat Meals

3.4.3. Omnichannel and Hybrid Retail Models

3.5. Government Regulations

3.5.1. FDA Regulations on Food Safety

3.5.2. USDA Standards for Organic Certification

3.5.3. Labeling and Nutritional Transparency

3.6. SWOT Analysis

3.7. Stake Ecosystem (Retailers, Distributors, Suppliers, Regulatory Bodies)

3.8. Porter’s Five Forces

3.9. Competition Ecosystem

4. USA Grocery & Food Market Segmentation

4.1. By Product Type

4.1.1. Fresh Produce

4.1.2. Packaged Foods

4.1.3. Beverages

4.1.4. Dairy and Dairy Alternatives

4.1.5. Frozen Foods

4.2. By Distribution Channel

4.2.1. Supermarkets/Hypermarkets

4.2.2. Convenience Stores

4.2.3. Online Platforms

4.2.4. Specialty Stores

4.2.5. Discount Stores

4.3. By Consumer Demographics

4.3.1. Age Groups

4.3.2. Income Levels

4.3.3. Family Size

4.4. By Dietary Preferences

4.4.1. Organic

4.4.2. Plant-Based

4.4.3. Gluten-Free

4.4.4. Keto and Low-Carb

4.5. By Region

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

5. USA Grocery & Food Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Walmart Inc.

5.1.2. Kroger Co.

5.1.3. Amazon (Whole Foods Market)

5.1.4. Costco Wholesale Corporation

5.1.5. Albertsons Companies Inc.

5.1.6. Ahold Delhaize USA

5.1.7. Target Corporation

5.1.8. Publix Super Markets, Inc.

5.1.9. Sprouts Farmers Market, Inc.

5.1.10. Trader Joe's Company

5.2. Cross Comparison Parameters

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Private Equity and Venture Capital Investments

5.8. Government Grants and Subsidies

5.9. Technological Innovations and Partnerships

6. USA Grocery & Food Market Regulatory Framework

6.1. Food Safety Standards

6.2. Labeling and Nutritional Information Requirements

6.3. Import and Export Regulations

6.4. Certifications and Compliance Requirements

7. USA Grocery & Food Market Future Market Size (In USD Mn)

7.1. Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Grocery & Food Market Future Segmentation

8.1. By Product Type

8.2. By Distribution Channel

8.3. By Dietary Preferences

8.4. By Consumer Demographics

8.5. By Region

9. USA Grocery & Food Market Analysts’ Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

This phase involves constructing an ecosystem map, identifying all critical players in the USA Grocery & Food Market. Comprehensive desk research, drawing on secondary and proprietary databases, helps establish a foundation of market-relevant data.

Step 2: Market Analysis and Construction

Historical data is compiled, focusing on market size, revenue growth, and distribution channels. Comparative analysis within these parameters ensures accurate estimates and trends that inform future projections.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses based on initial findings are validated through expert interviews, conducted with industry insiders who provide direct insights on competitive dynamics, consumer preferences, and technological advances.

Step 4: Research Synthesis and Final Output

The last phase incorporates insights gathered, merging qualitative and quantitative findings to produce a well-rounded, accurate picture of the USA Grocery & Food Market. This approach assures a reliable, data-backed analysis.

Frequently Asked Questions

01. How big is the USA Grocery & Food Market?

The USA Grocery & Food Market is valued at USD 3 trillion, with steady growth attributed to consumer demand for diverse, fresh, and health-conscious options, as well as the rapid growth of e-commerce grocery services.

02. What are the challenges in the USA Grocery & Food Market?

Key challenges in USA Grocery & Food Market include logistics and supply chain disruptions, regulatory compliance costs, and intense price competition, which pressure companies to innovate and optimize their operations.

03. Who are the major players in the USA Grocery & Food Market?

Leading companies in USA Grocery & Food Market include Walmart, Kroger, and Amazon (Whole Foods Market), which maintain dominance through extensive distribution networks and robust brand loyalty.

04. What factors are driving growth in the USA Grocery & Food Market?

USA Grocery & Food Market growth is propelled by consumer preferences for healthier, organic, and ready-to-eat options, coupled with the rise of digital grocery shopping platforms and convenient delivery options.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.