USA Integrated Delivery Network Market Outlook to 2030

Region:North America

Author(s):Abhinav kumar

Product Code:KROD6612

December 2024

82

About the Report

USA Integrated Delivery Network Market Overview

- The USA Integrated Delivery Network (IDN) market is valued at approximately USD 1.9 trillion, reflecting robust growth driven by factors such as rising healthcare expenditures and an aging population. This market is propelled by the increasing need for coordinated care and value-based healthcare models, ensuring that patients receive comprehensive services across various healthcare settings. This growth is further supported by advancements in health information technology, which enhance communication and data sharing among providers, leading to improved patient outcomes.

- Dominant regions within the USA Integrated Delivery Network market include metropolitan areas such as New York, California, and Texas. These states boast a high concentration of healthcare facilities and advanced medical infrastructure, making them hubs for integrated healthcare services. The presence of major healthcare systems and a diverse patient population contributes to the market's dominance in these areas, facilitating innovative care models and partnerships that enhance service delivery and operational efficiency.

- The adoption of artificial intelligence (AI) and machine learning technologies is transforming the Integrated Delivery Network (IDN) landscape. As of 2023, around 30% of healthcare organizations reported utilizing AI in clinical decision support systems, enhancing diagnostic accuracy and treatment planning. These technologies facilitate data analysis and predictive modeling, enabling healthcare providers to identify at-risk patients and tailor interventions accordingly. The growing emphasis on personalized medicine and efficient resource allocation underscores the importance of integrating AI into healthcare practices. The trend towards AI adoption is expected to continue reshaping the operational dynamics within IDNs, ultimately improving patient outcomes and streamlining care processes

USA Integrated Delivery Network Market Segmentation

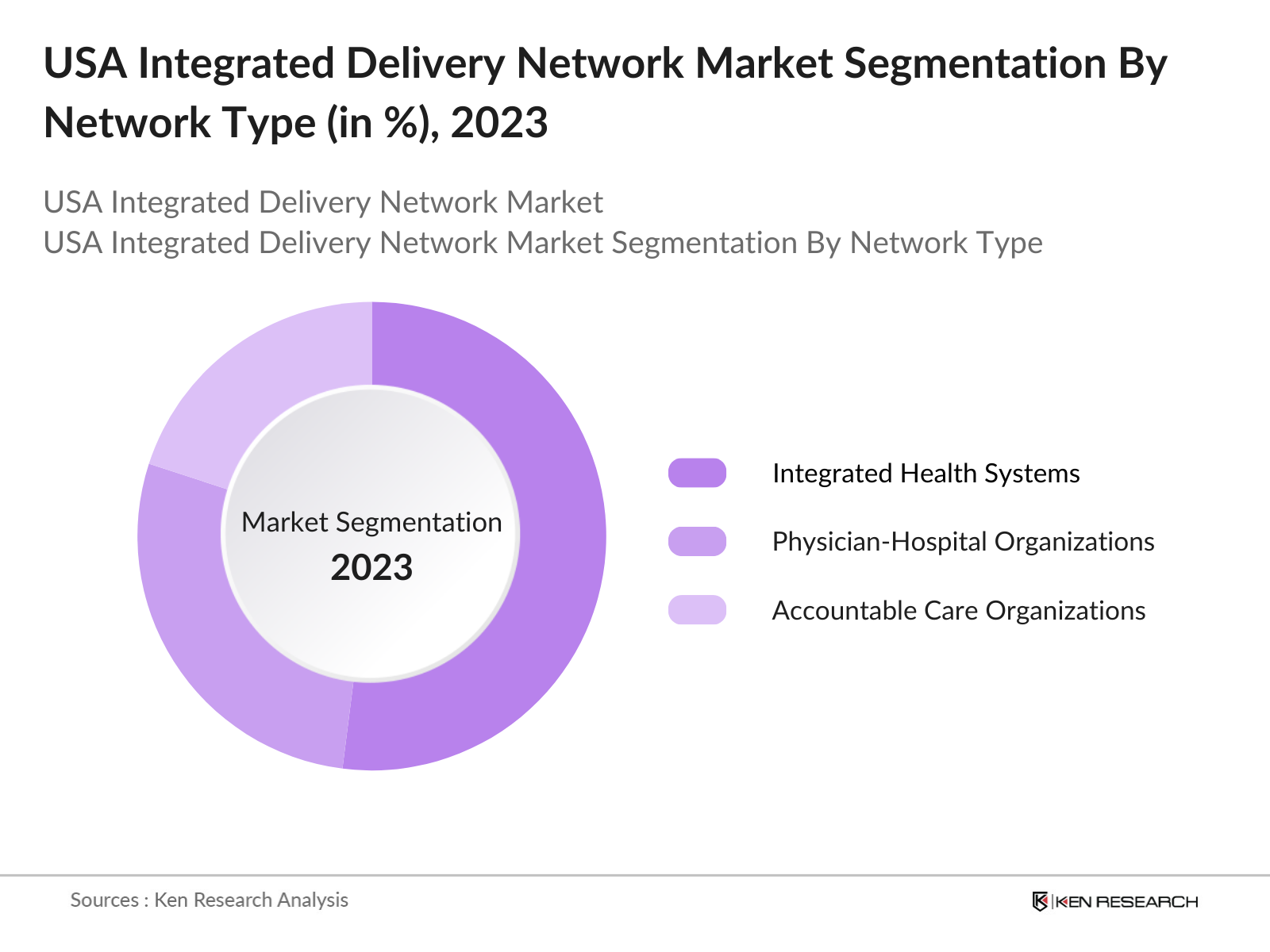

By Network Type: The USA Integrated Delivery Network market is segmented by network type into Physician-Hospital Organizations (PHOs), Accountable Care Organizations (ACOs), and Integrated Health Systems. Among these, Integrated Health Systems hold the largest market share, accounting for approximately 52% in 2023. This dominance stems from their ability to deliver a wide range of healthcare services under one umbrella, resulting in streamlined operations and improved patient management. Integrated Health Systems facilitate comprehensive care that encompasses preventive, acute, and post-acute services, thereby enhancing patient satisfaction and clinical outcomes.

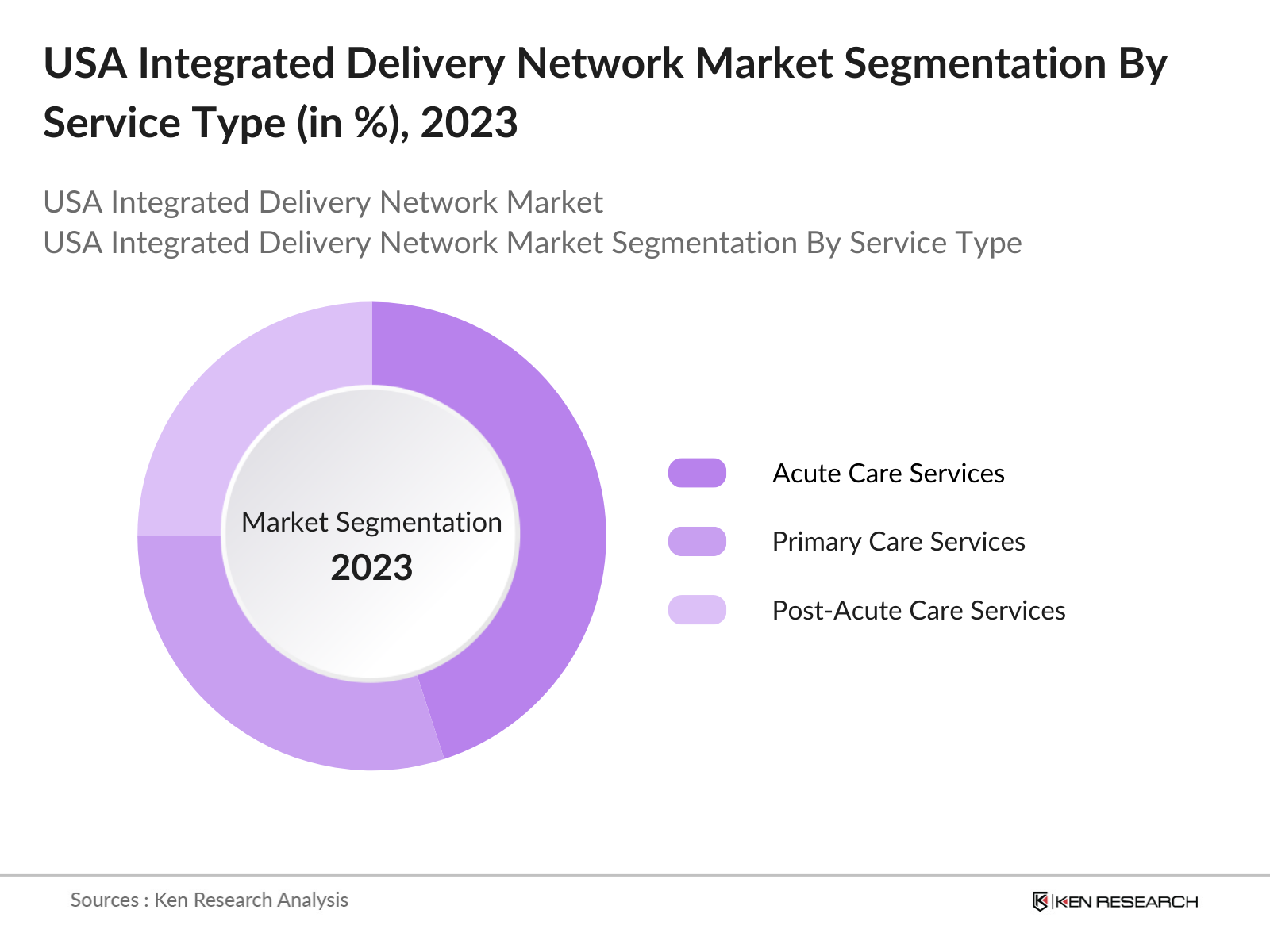

By Service Type: The market is also segmented by service type into Acute Care Services, Primary Care Services, and Post-Acute Care Services. Acute Care Services dominate the market with a 45% share in 2023. This segment's leading position is attributed to the high demand for immediate medical attention in hospitals and urgent care settings, especially in urban areas with significant population density. As the complexity of healthcare needs increases, the focus on acute care continues to rise, driven by advancements in medical technology and treatment protocols.

USA Integrated Delivery Network Competitive Landscape

The USA Integrated Delivery Network market is characterized by significant competition among major players. The market is dominated by key entities such as UnitedHealth Group, Anthem Inc., Aetna Inc. (CVS Health), and HCA Healthcare, each leveraging extensive networks and resources to enhance patient care and operational efficiency. This competitive landscape reflects a trend towards consolidation and strategic partnerships, aimed at improving healthcare delivery and expanding service offerings.

|

Major Player |

Establishment Year |

Headquarters |

Revenue (USD Bn) |

Network Type Focus |

Service Type Focus |

Key Innovations |

|

UnitedHealth Group |

1977 |

Minnetonka, Minnesota |

_ |

_ |

_ |

_ |

|

Anthem Inc. |

2004 |

Indianapolis, Indiana |

_ |

_ |

_ |

_ |

|

Aetna Inc. (CVS Health) |

1853 |

Hartford, Connecticut |

_ |

_ |

_ |

_ |

|

HCA Healthcare |

1968 |

Nashville, Tennessee |

_ |

_ |

_ |

_ |

|

Tenet Healthcare Corporation |

1967 |

Dallas, Texas |

_ |

_ |

_ |

_ |

USA Integrated Delivery Network Industry Analysis

Growth Drivers

- Aging Population: The aging population in the United States is a significant driver of the Integrated Delivery Network (IDN) market, with projections indicating that by 2030, around 20% of the U.S. population will be 65 years or older. As of 2022, approximately 54 million Americans were aged 65 and older, with estimates reaching 78 million by 2035. This demographic shift is leading to increased healthcare demands, particularly for chronic disease management, which often requires coordinated care. The U.S. Census Bureau reports that older adults typically have multiple chronic conditions, necessitating comprehensive healthcare solutions that integrated networks can provide, thereby boosting the IDN market.

- Increasing Healthcare Expenditure: Healthcare expenditure in the United States is projected to exceed $4.3 trillion in 2024, according to the Centers for Medicare & Medicaid Services (CMS). This upward trend is largely driven by rising costs associated with an aging population, technological advancements, and increased prevalence of chronic diseases. In 2022, healthcare spending per capita reached approximately $13,500, highlighting the growing financial commitment to healthcare services. As expenditures rise, the emphasis on efficient delivery methods, such as IDNs, becomes paramount, enabling better resource allocation and patient outcomes. The integration of services within these networks is crucial for managing these increasing costs effectively.

- Shift Towards Value-Based Care: The healthcare landscape in the U.S. is increasingly shifting from fee-for-service models to value-based care, which focuses on patient outcomes and cost-effectiveness. As of 2022, approximately 60% of Medicare payments were linked to value-based care models, a figure expected to rise as more payers and providers adopt these frameworks. This transition encourages integrated delivery systems to enhance care coordination and quality, as providers are incentivized to deliver better health outcomes for patients. The focus on value aligns with federal initiatives, including the Affordable Care Act, promoting integrated care approaches that improve health systems.

Market Challenges

- Regulatory Compliance: Regulatory compliance poses a significant challenge for Integrated Delivery Networks (IDNs) in the United States. The healthcare sector is subject to a myriad of regulations, including the Affordable Care Act, HIPAA, and Medicare/Medicaid guidelines, which mandate stringent operational standards. Non-compliance can result in penalties exceeding millions of dollars. In 2022, the Office of Inspector General reported that over $2 billion in fines were imposed for violations related to Medicare and Medicaid regulations. IDNs must invest considerable resources in compliance initiatives, potentially diverting funds from patient care and innovation. This regulatory burden complicates operational efficiency and hinders the ability to adapt quickly to changing market dynamics.

- Data Security Concerns: Data security concerns represent a critical challenge for Integrated Delivery Networks, especially given the rise in cyberattacks targeting healthcare institutions. In 2023, approximately 45% of healthcare organizations reported experiencing a data breach, with the average cost per breach estimated at $4.35 million. These breaches not only jeopardize patient information but also lead to financial losses and reputational damage. Compliance with the Health Insurance Portability and Accountability Act (HIPAA) mandates strict data protection measures, requiring IDNs to allocate significant resources to cybersecurity efforts. The increasing frequency and sophistication of cyber threats necessitate ongoing investments in technology and personnel to safeguard sensitive health information. Source: IBM Security.

USA Integrated Delivery Network Market Future Outlook

Over the next five years, the USA Integrated Delivery Network market is expected to experience substantial growth driven by continuous government support for healthcare reforms, advancements in technology, and a rising demand for integrated care solutions. The increasing emphasis on patient-centered care and value-based payment models will further propel the adoption of integrated delivery systems. Additionally, as healthcare providers aim to enhance operational efficiency and patient outcomes, investments in technology and infrastructure will be critical in shaping the future of the IDN market.

Opportunities

- Expansion of Telehealth Services: The expansion of telehealth services presents a significant opportunity for Integrated Delivery Networks (IDNs) in the United States. In 2022, telehealth visits surged to approximately 30 million, a substantial increase from pre-pandemic levels, reflecting changing patient preferences for remote healthcare options. The convenience and accessibility of telehealth align with the growing demand for integrated services, enabling IDNs to enhance care delivery while reaching underserved populations. Federal funding and policy support for telehealth initiatives are further propelling this growth. The shift towards virtual care represents an opportunity for IDNs to innovate their service offerings and improve patient engagement and satisfaction.

- Increasing Consumer Engagement: Increasing consumer engagement is driving the transformation of Integrated Delivery Networks in the U.S. healthcare landscape. As of 2024, around 77% of patients expressed a preference for engaging with healthcare providers through digital platforms, highlighting the demand for accessible communication channels. This trend is prompting IDNs to adopt innovative strategies to improve patient experience and involvement in their care journeys. By leveraging technologies such as patient portals and mobile health applications, IDNs can enhance communication, promote preventative care, and facilitate better health outcomes. Engaging patients actively in their care processes aligns with the broader shift towards value-based care, ultimately benefiting both providers and patients.

Scope of the Report

|

Network Type |

Physician-Hospital Organizations (PHOs) Accountable Care Organizations (ACOs) Integrated Health Systems |

|

Service Type |

Acute Care Services Primary Care Services Post-Acute Care Services |

|

Technology |

Electronic Health Records (EHR) Telehealth Platforms Health Information Exchange (HIE) |

|

Geographic Region |

Northeast Midwest South West |

|

Patient Demographics |

Pediatric Adult Geriatric |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report:

Healthcare Companies

Insurance Companies

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (Centers for Medicare & Medicaid Services)

Health Technology Companies

Pharmaceutical Companies

Healthcare Companies

Companies

Players Mentioned in the Report:

UnitedHealth Group

Anthem Inc.

Aetna Inc. (CVS Health)

HCA Healthcare

Tenet Healthcare Corporation

CommonSpirit Health

Mayo Clinic

Providence St. Joseph Health

Ascension Health

WellStar Health System

Intermountain Healthcare

Trinity Health

UPMC (University of Pittsburgh Medical Center)

Kaiser Permanente

Mednax

Table of Contents

1. USA Integrated Delivery Network Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. USA Integrated Delivery Network Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. USA Integrated Delivery Network Market Analysis

3.1. Growth Drivers

3.1.1. Aging Population

3.1.2. Increasing Healthcare Expenditure

3.1.3. Shift Towards Value-Based Care

3.1.4. Advancements in Health Information Technology

3.2. Market Challenges

3.2.1. Regulatory Compliance

3.2.2. Data Security Concerns

3.2.3. Integration of Diverse Systems

3.3. Opportunities

3.3.1. Expansion of Telehealth Services

3.3.2. Increasing Consumer Engagement

3.3.3. Partnerships with Technology Providers

3.4. Trends

3.4.1. Adoption of AI and Machine Learning

3.4.2. Integration of Behavioral Health Services

3.4.3. Focus on Social Determinants of Health

3.5. Government Regulation

3.5.1. Affordable Care Act Compliance

3.5.2. Medicare and Medicaid Regulations

3.5.3. Data Privacy Laws

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Landscape

4. USA Integrated Delivery Network Market Segmentation

4.1. By Network Type (In Value %)

4.1.1. Physician-Hospital Organizations (PHOs)

4.1.2. Accountable Care Organizations (ACOs)

4.1.3. Integrated Health Systems

4.2. By Service Type (In Value %)

4.2.1. Acute Care Services

4.2.2. Primary Care Services

4.2.3. Post-Acute Care Services

4.3. By Technology (In Value %)

4.3.1. Electronic Health Records (EHR)

4.3.2. Telehealth Platforms

4.3.3. Health Information Exchange (HIE)

4.4. By Geographic Region (In Value %)

4.4.1. Northeast

4.4.2. Midwest

4.4.3. South

4.4.4. West

4.5. By Patient Demographics (In Value %)

4.5.1. Pediatric

4.5.2. Adult

4.5.3. Geriatric

5. USA Integrated Delivery Network Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. UnitedHealth Group

5.1.2. Anthem Inc.

5.1.3. Aetna Inc. (CVS Health)

5.1.4. Cigna Corporation

5.1.5. HCA Healthcare

5.1.6. Tenet Healthcare Corporation

5.1.7. CommonSpirit Health

5.1.8. Mayo Clinic

5.1.9. Providence St. Joseph Health

5.1.10. Ascension Health

5.1.11. WellStar Health System

5.1.12. Intermountain Healthcare

5.1.13. Trinity Health

5.1.14. UPMC (University of Pittsburgh Medical Center)

5.1.15. Kaiser Permanente

5.2. Cross Comparison Parameters (Revenue, Market Share, Number of Employees, Geographic Reach, Service Offerings, Patient Demographics, Integration Capabilities, Technology Utilization)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. USA Integrated Delivery Network Market Regulatory Framework

6.1. Healthcare Compliance Standards

6.2. Accreditation Requirements

6.3. Telehealth Regulations

7. USA Integrated Delivery Network Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Integrated Delivery Network Future Market Segmentation

8.1. By Network Type (In Value %)

8.2. By Service Type (In Value %)

8.3. By Technology (In Value %)

8.4. By Geographic Region (In Value %)

8.5. By Patient Demographics (In Value %)

9. USA Integrated Delivery Network Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

This phase involves creating an ecosystem map that includes all major stakeholders within the USA Integrated Delivery Network market. Extensive desk research is conducted using a mix of secondary and proprietary databases to gather comprehensive industry-level information. The goal is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, historical data pertaining to the USA Integrated Delivery Network market is compiled and analyzed. This includes assessing market penetration, the ratio of healthcare providers to patients, and the resultant revenue generation. Additionally, an evaluation of service quality metrics is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through computer-assisted telephone interviews (CATIs) with industry experts from various organizations. These consultations yield valuable operational and financial insights directly from industry practitioners, refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves engaging with multiple integrated delivery network providers to gather detailed insights into service offerings, performance metrics, consumer preferences, and other pertinent factors. This interaction serves to validate and complement the statistics derived from the bottom-up approach, ensuring a comprehensive and accurate analysis of the USA Integrated Delivery Network market.

Frequently Asked Questions

1. How big is the USA Integrated Delivery Network market?

The USA Integrated Delivery Network market is valued at approximately USD 1.9 trillion, driven by increasing healthcare expenditures and the need for coordinated care models.

2. What are the challenges in the USA Integrated Delivery Network market?

Challenges include regulatory compliance, data security concerns, and the integration of diverse healthcare systems, which can hinder operational efficiency and patient care.

3. Who are the major players in the USA Integrated Delivery Network market?

Key players include UnitedHealth Group, Anthem Inc., Aetna Inc. (CVS Health), and HCA Healthcare. Their dominance is due to extensive networks, strong brand presence, and innovative service models.

4. What are the growth drivers of the USA Integrated Delivery Network market?

The market is propelled by factors such as government support for healthcare reforms, advancements in health information technology, and an increasing demand for integrated care solutions.t.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.