USA Intravenous Immunoglobulin Market Outlook to 2030

Region:North America

Author(s):Meenakshi Bisht

Product Code:KROD8956

December 2024

84

About the Report

USA Intravenous Immunoglobulin Market Overview

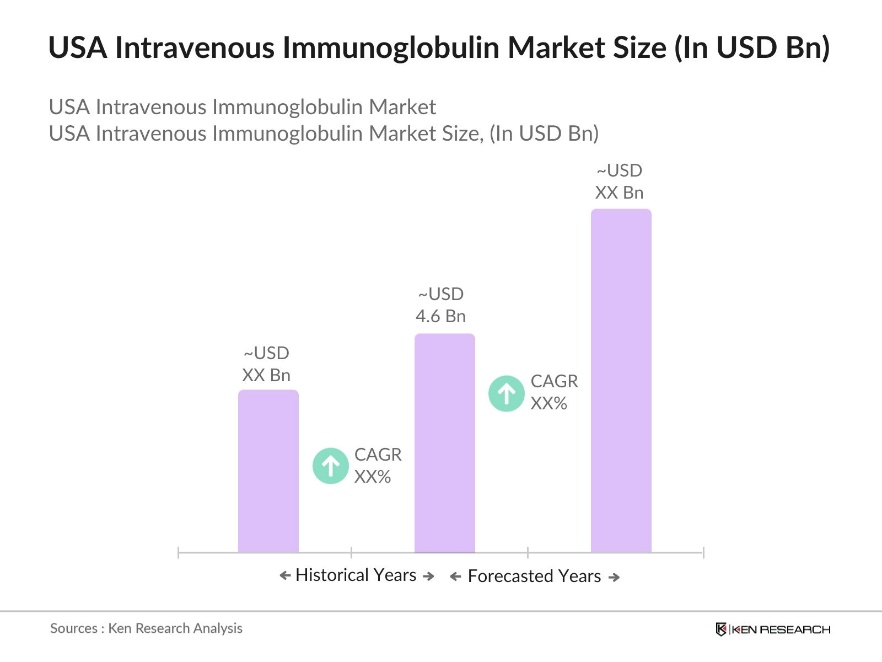

- The USA Intravenous Immunoglobulin (IVIG) Market is valued at USD 4.6 billion, based on a five-year historical analysis. This market is primarily driven by an increasing prevalence of autoimmune diseases and a growing geriatric population, which necessitates higher demand for immunoglobulin therapies. Factors such as advancements in IVIG formulations, improved treatment protocols, and favorable reimbursement policies contribute to this market's growth. Additionally, the expanding scope of IVIG applications for neurological and hematological disorders supports this upward trajectory.

- The USA dominates the global IVIG market due to its advanced healthcare infrastructure, high plasma collection capabilities, and the presence of major pharmaceutical players involved in the research, development, and production of immunoglobulin therapies. Cities such as New York, Los Angeles, and Chicago are prominent due to their large patient pools and access to state-of-the-art medical facilities, which facilitate higher adoption of IVIG treatments.

- The U.S. government has implemented a structured reimbursement framework for IVIG therapies, ensuring accessibility while balancing costs. For 2024, the payment rate for this bundled service (HCPCS code Q2052) is set at $420.48. The Centers for Medicare & Medicaid Services (CMS) continually adjusts reimbursement rates based on clinical necessity and patient outcomes. This framework supports the market by facilitating timely access to IVIG while allowing healthcare providers to deliver necessary treatments in both hospital and outpatient settings.

USA Intravenous Immunoglobulin Market Segmentation

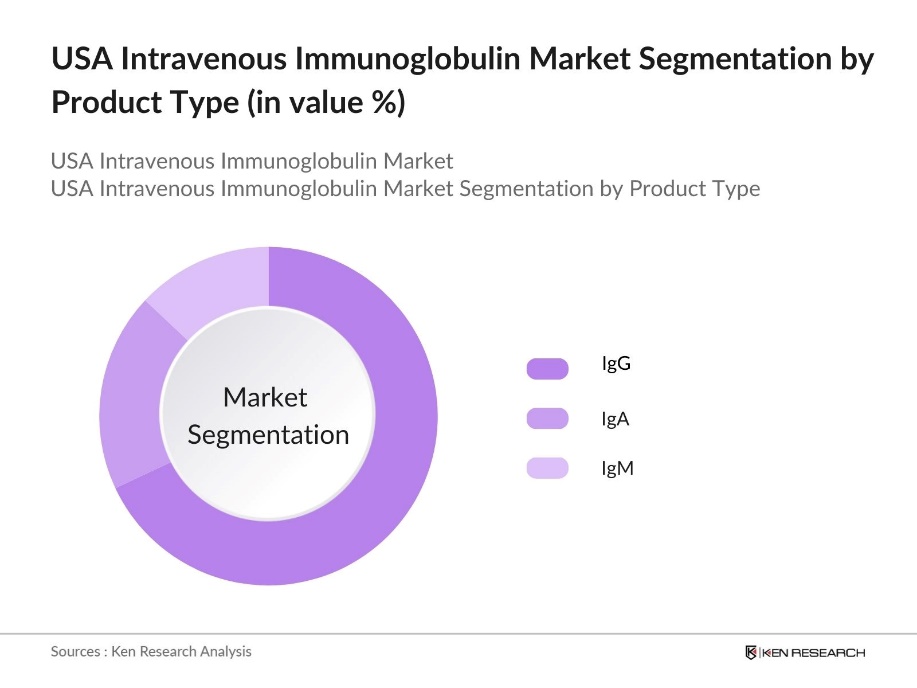

By Product Type: The USA Intravenous Immunoglobulin market is segmented by product type into IgG, IgA, and IgM. Recently, the IgG segment has held a dominant market share within the IVIG product type category. This dominance is primarily due to IgG's widespread use in treating primary immunodeficiency and various autoimmune conditions, such as Chronic Inflammatory Demyelinating Polyneuropathy (CIDP). The extensive clinical studies supporting the efficacy and safety of IgG-based therapies, along with its broader availability, make it the preferred choice among healthcare providers and patients.

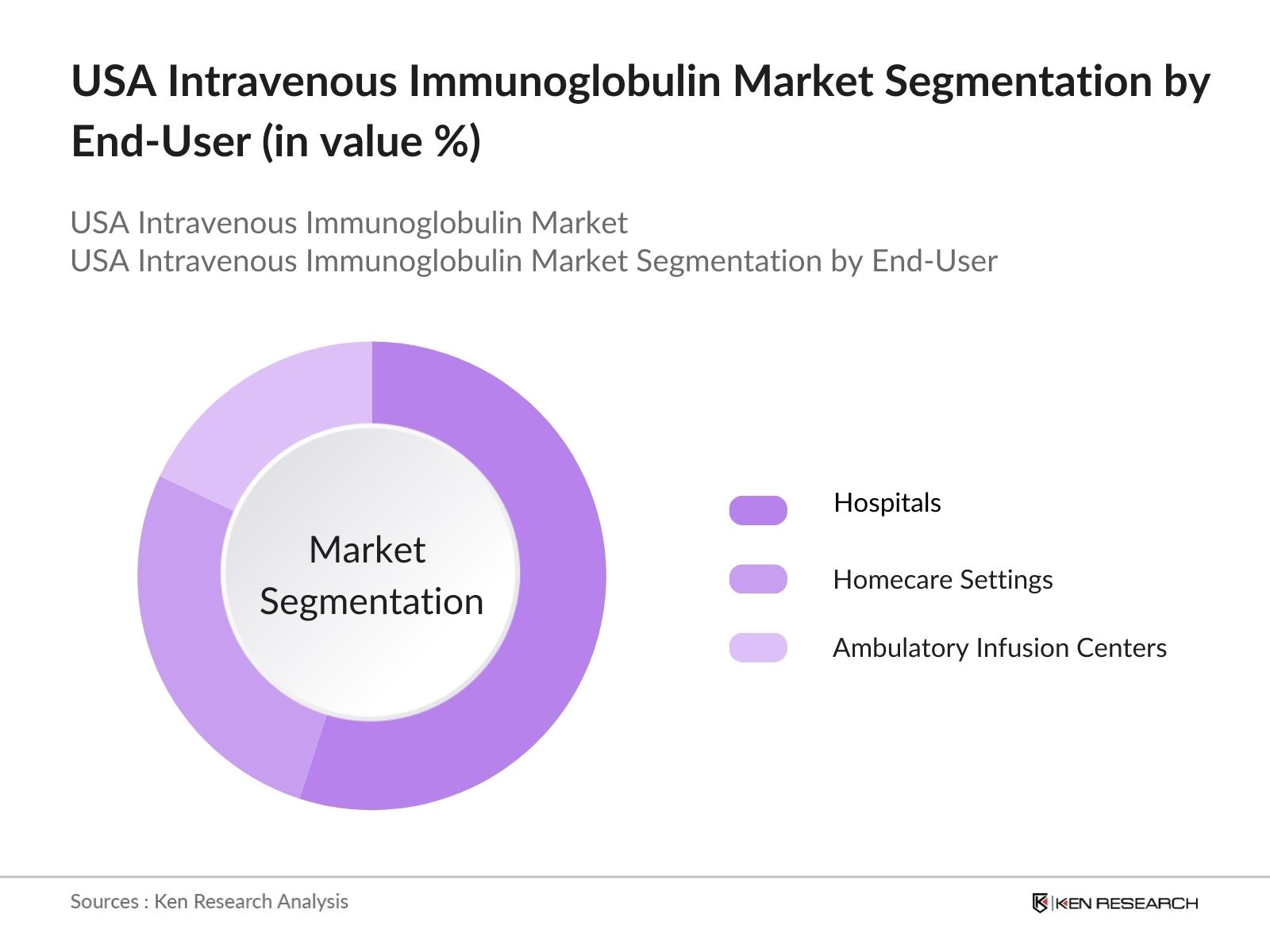

By End-User: The USA Intravenous Immunoglobulin market is segmented by end-users, including hospitals, homecare settings, and ambulatory infusion centers. Hospitals have a dominant share in this segment due to the complexity of IVIG administration, which requires monitoring for adverse effects and precision in dosage. Hospitals are equipped with the necessary infrastructure to manage patients undergoing IVIG therapy, including facilities for critical care and emergency management, which makes them a preferred setting for both patients and physicians.

USA Intravenous Immunoglobulin Market Competitive Landscape

The market is dominated by a few major players, such as Grifols S.A., CSL Behring, and Takeda Pharmaceutical Company, among others. This consolidation highlights the significant influence of these key companies, which have established extensive plasma collection networks and strong research and development capabilities. The market's competitive nature is driven by factors such as pricing strategies, product innovation, and strategic alliances.

|

Company |

Establishment Year |

Headquarters |

Plasma Collection Centers |

R&D Expenditure |

Global Presence |

Annual Revenue |

Key Products |

Market Strategy |

Number of Employees |

|

Grifols S.A. |

1940 |

Barcelona, Spain |

|||||||

|

CSL Behring |

1916 |

Melbourne, Australia |

|||||||

|

Takeda Pharmaceutical Company |

1781 |

Tokyo, Japan |

|||||||

|

Octapharma AG |

1983 |

Lachen, Switzerland |

|||||||

|

Pfizer Inc. |

1849 |

New York, USA |

USA Intravenous Immunoglobulin Industry Analysis

Growth Drivers

- Increasing Prevalence of Autoimmune Disorders: The USA has experienced a rising incidence of autoimmune diseases like Guillain-Barr Syndrome, CIDP (Chronic Inflammatory Demyelinating Polyneuropathy), and Myasthenia Gravis. The prevalence of CIDP is generally estimated to be around 5 to 7 cases per 100,000 individuals in the general population. This trend has led to a greater demand for Intravenous Immunoglobulin (IVIG) as a key treatment option. With an expanding patient base, the market is witnessing significant demand for IVIG therapies, ensuring a continuous need for supply in the healthcare sector.

- Rising Geriatric Population (Demographic Analysis): The USA's geriatric population, aged 65 and above, has reached over 57.8 million in 2022. This demographic shift has direct implications for the IVIG market, as the elderly are more susceptible to immune deficiencies and chronic conditions like primary immunodeficiency disorders (PIDDs). With a growing number of aging adults, the demand for immunoglobulin therapies to manage age-related immune conditions is on the rise. This demographic trend underscores the expanding patient pool and reinforces the need for IVIG in managing age-associated health challenges.

- Favorable Reimbursement Policies (Medicare, Medicaid): The U.S. governments reimbursement frameworks through Medicare and Medicaid have made IVIG therapies more accessible. Medicare Part B covers IVIG treatment for eligible patients with primary immunodeficiency, supporting broader usage. Additionally, the Centers for Medicare & Medicaid Services (CMS) has updated guidelines to include home-based IVIG therapy, making it easier for patients to receive treatments outside hospital settings, thus boosting the overall adoption of IVIG therapies.

Market Challenges

- High Treatment Costs (Cost-Benefit Analysis): IVIG therapy is vital for treating various immune-related conditions, but its high costs present a major barrier for many patients. The substantial expenses associated with regular treatments can be challenging, especially for those without comprehensive insurance coverage. While insurance helps to offset some of these costs, out-of-pocket expenses can still be a significant burden, limiting access to IVIG therapies and creating disparities in treatment availability across different economic groups.

- Supply Chain Constraints (Production Bottlenecks, Plasma Supply): IVIG production is highly dependent on the availability of plasma, a critical raw material. Demand for plasma-derived products like IVIG often surpasses supply, creating challenges in maintaining a stable supply chain. The COVID-19 pandemic further strained plasma collections, resulting in shortages that continue to affect the market. As collection centers work to increase plasma availability, the IVIG market faces ongoing challenges in balancing production levels with demand.

USA Intravenous Immunoglobulin Market Future Outlook

The USA Intravenous Immunoglobulin (IVIG) market is expected to witness steady growth, driven by advancements in therapeutic applications, increased availability of plasma, and technological improvements in manufacturing processes. Moreover, the ongoing expansion of indications for IVIG in treating neurological disorders and the development of more efficient infusion methods are likely to play a pivotal role in shaping the market's future. The market is anticipated to continue benefiting from strong research and development efforts, aimed at enhancing product safety and efficacy.

Market Opportunities

- Emerging Indications for IVIG (Neurological Disorders): Recent research suggests that IVIG may be effective in treating various neurological conditions, such as Alzheimers disease and Multiple Sclerosis. These emerging therapeutic applications could expand the market beyond its traditional use in immune deficiencies. Research institutions and pharmaceutical companies are conducting clinical trials to validate these new uses, which could lead to broader regulatory approval and a more diverse range of applications for IVIG therapies.

- Strategic Collaborations and Partnerships (Research Initiatives): Pharmaceutical companies are increasingly partnering with research institutions to advance IVIG applications. These strategic collaborations aim to develop next-generation IVIG therapies and improve production techniques, focusing on innovative approaches to meet specific patient needs. Such partnerships also facilitate faster development and regulatory approval processes, helping address supply challenges while enhancing the clinical effectiveness and availability of IVIG treatments across a broader range of conditions.

Scope of the Report

|

By Product Type |

IgG IgA IgM |

|

By Application |

Primary Immunodeficiency Secondary Immunodeficiency Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) Guillain-Barr Syndrome (GBS) |

|

By Route of Administration |

Intravenous Administration (IV) Subcutaneous Administration (SC) |

|

By End-User |

Hospitals Homecare Settings Ambulatory Infusion Centers |

|

By Distribution Channel |

Hospital Pharmacies Retail Pharmacies Specialty Pharmacies |

Products

Key Target Audience

Pharmaceutical Manufacturers

Medical Device Manufacturers

Healthcare Technology Companies

Geriatric Care Management Firms

Government and Regulatory Bodies (FDA, Centers for Medicare & Medicaid Services)

Investors and venture capital Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

Grifols S.A.

CSL Behring

Octapharma AG

Kedrion Biopharma Inc.

Takeda Pharmaceutical Company Limited

Pfizer Inc.

Bio Products Laboratory (BPL)

LFB Group

Biotest AG

ADMA Biologics

Table of Contents

1. USA Intravenous Immunoglobulin Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Annual Growth Trends, Market Momentum)

1.4. Market Segmentation Overview

1.5. Market Entry Barriers (Regulatory Requirements, Clinical Trials)

2. USA Intravenous Immunoglobulin Market Size (In USD Bn)

2.1. Historical Market Size (Past Performance Analysis)

2.2. Year-On-Year Growth Analysis (YoY Growth Trends)

2.3. Key Market Developments and Milestones (Product Launches, FDA Approvals)

3. USA Intravenous Immunoglobulin Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Prevalence of Autoimmune Disorders

3.1.2. Rising Geriatric Population (Demographic Analysis)

3.1.3. Favorable Reimbursement Policies (Medicare, Medicaid)

3.1.4. Advancements in IVIG Formulation (Clinical Efficacy)

3.2. Market Challenges

3.2.1. High Treatment Costs (Cost-Benefit Analysis)

3.2.2. Supply Chain Constraints (Production Bottlenecks, Plasma Supply)

3.2.3. Risk of Adverse Effects (Patient Safety Concerns)

3.3. Opportunities

3.3.1. Emerging Indications for IVIG (Neurological Disorders)

3.3.2. Strategic Collaborations and Partnerships (Research Initiatives)

3.3.3. Expansion into Ambulatory Infusion Centers (Distribution Strategy)

3.4. Trends

3.4.1. Shift Towards Subcutaneous Immunoglobulins (Therapeutic Preference)

3.4.2. Increased R&D Investment (Pipeline Analysis)

3.4.3. Focus on Personalized Immunoglobulin Therapy

3.5. Government Regulation

3.5.1. FDA Guidelines for IVIG Usage (Regulatory Compliance)

3.5.2. Orphan Drug Designation (Incentives and Grants)

3.5.3. Pricing and Reimbursement Framework

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Plasma Donors, Hospitals, Infusion Centers)

3.8. Porters Five Forces

3.9. Competition Ecosystem (Market Concentration, Competitive Landscape)

4. USA Intravenous Immunoglobulin Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. IgG (Immunoglobulin G)

4.1.2. IgA (Immunoglobulin A)

4.1.3. IgM (Immunoglobulin M)

4.2. By Application (In Value %)

4.2.1. Primary Immunodeficiency

4.2.2. Secondary Immunodeficiency

4.2.3. Chronic Inflammatory Demyelinating Polyneuropathy (CIDP)

4.2.4. Guillain-Barr Syndrome (GBS)

4.3. By Route of Administration (In Value %)

4.3.1. Intravenous Administration (IV)

4.3.2. Subcutaneous Administration (SC)

4.4. By End-User (In Value %)

4.4.1. Hospitals

4.4.2. Homecare Settings

4.4.3. Ambulatory Infusion Centers

4.5. By Distribution Channel (In Value %)

4.5.1. Hospital Pharmacies

4.5.2. Retail Pharmacies

4.5.3. Specialty Pharmacies

5. USA Intravenous Immunoglobulin Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Grifols S.A.

5.1.2. CSL Behring

5.1.3. Octapharma AG

5.1.4. Kedrion Biopharma Inc.

5.1.5. Takeda Pharmaceutical Company Limited

5.1.6. Pfizer Inc.

5.1.7. Bio Products Laboratory (BPL)

5.1.8. LFB Group

5.1.9. Biotest AG

5.1.10. ADMA Biologics

5.1.11. Baxter International Inc.

5.1.12. Emergent BioSolutions

5.1.13. Sanquin

5.1.14. China Biologic Products Holdings Inc.

5.1.15. Hualan Biological Engineering Inc.

5.2. Cross Comparison Parameters (R&D Spend, Market Share, Therapeutic Coverage, Global Presence, Patient Assistance Programs, Supply Chain Network, Plasma Collection Capacity, Manufacturing Sites)

5.3. Market Share Analysis (Top Players, Market Fragmentation)

5.4. Strategic Initiatives (Expansion Plans, Market Penetration Strategies)

5.5. Mergers And Acquisitions (Notable Deals)

5.6. Investment Analysis (Private Equity, Venture Capital)

5.7. Government Grants (Research Funding)

5.8. Market Consolidation Trends

6. USA Intravenous Immunoglobulin Market Regulatory Framework

6.1. FDA Approval Process (Clinical Trials, Licensing)

6.2. Compliance Requirements (Quality Standards, Good Manufacturing Practice - GMP)

6.3. Certification Processes (Product Certification, Patient Safety Protocols)

7. USA Intravenous Immunoglobulin Future Market Size (In USD Bn)

7.1. Future Market Size Projections (Growth Potential)

7.2. Key Factors Driving Future Market Growth (Pipeline Products, New Indications)

8. USA Intravenous Immunoglobulin Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Route of Administration (In Value %)

8.4. By End-User (In Value %)

8.5. By Distribution Channel (In Value %)

9. USA Intravenous Immunoglobulin Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives (Brand Positioning, Patient Engagement)

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the USA Intravenous Immunoglobulin Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the USA Intravenous Immunoglobulin Market. This includes assessing market penetration, the ratio of hospitals to homecare settings, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple intravenous immunoglobulin manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the USA Intravenous Immunoglobulin market.

Frequently Asked Questions

01 How big is the USA Intravenous Immunoglobulin Market?

The USA Intravenous Immunoglobulin Market is valued at approximately USD 4.6 billion, driven by increasing demand for immunodeficiency treatments and a robust healthcare infrastructure.

02 What are the challenges in the USA Intravenous Immunoglobulin Market?

Key challenges in USA Intravenous Immunoglobulin Market include the high cost of treatments, limited plasma supply, and the risk of adverse reactions during IVIG therapy. These factors can hinder market expansion and pose barriers for new entrants.

03 Who are the major players in the USA Intravenous Immunoglobulin Market?

Major players in USA Intravenous Immunoglobulin Market include Grifols S.A., CSL Behring, Octapharma AG, Takeda Pharmaceutical Company, and Pfizer Inc., known for their extensive plasma collection networks and strong R&D focus.

04 What are the growth drivers of the USA Intravenous Immunoglobulin Market?

The USA Intravenous Immunoglobulin Market is driven by an increasing number of patients with autoimmune disorders, advancements in IVIG formulations, and favorable reimbursement policies, particularly for treatments administered in hospitals and clinics.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.