USA Joint All Domain Command and Control (JADC2) Market Outlook to 2030

Region:North America

Author(s):Abhinav kumar

Product Code:KROD6304

Region:North America

Author(s):Abhinav kumar

Product Code:KROD6304

November 2024

84

By Domain: The USA Joint All Domain Command and Control market is segmented by domain into air, land, sea, cyber, and space. Recently, the cyber domain has been gaining dominance under this segmentation. This is due to the increasing reliance on digital networks for command and control operations, and the rising frequency of cyber threats targeting critical military infrastructure. The importance of securing data and maintaining operational integrity in a networked warfare environment positions the cyber domain at the forefront of JADC2 strategies.

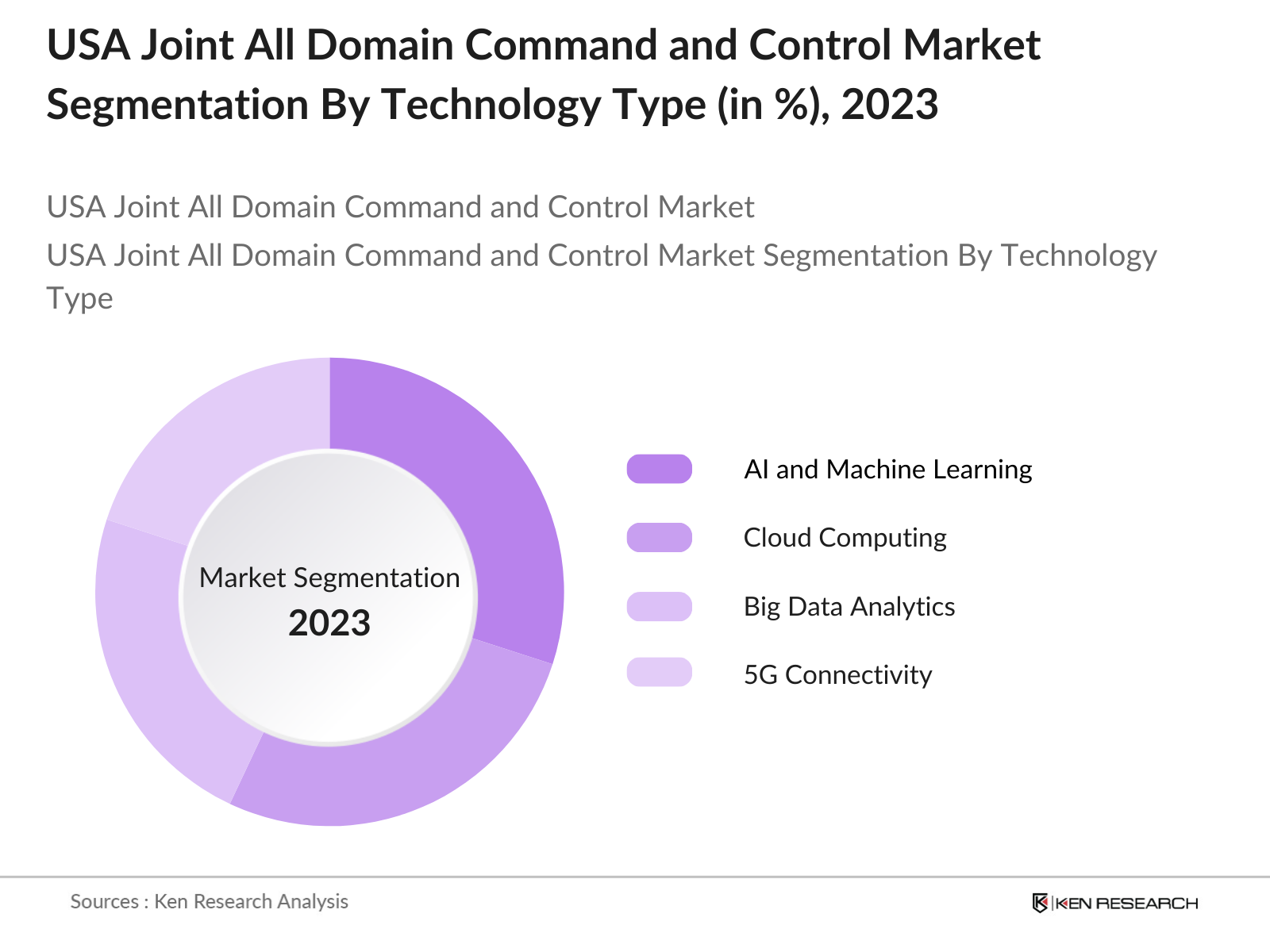

By Technology: The market is further segmented by technology into AI and machine learning, cloud computing, big data analytics, 5G connectivity, and Internet of Things (IoT). Among these, AI and machine learning hold the dominant market share, driven by their crucial role in enabling real-time decision-making and predictive analytics in warfare. AI helps process massive amounts of battlefield data, offering insights that enhance situational awareness, streamline command operations, and improve responsiveness during multi-domain operations.

The USA JADC2 market is characterized by the presence of several major players, each contributing significantly to the technological advancements and overall market competitiveness. The market is dominated by companies such as Lockheed Martin, Raytheon Technologies, and Northrop Grumman. These companies have solidified their positions through long-term defense contracts, innovation in multi-domain technologies, and strategic partnerships with government agencies.

Over the next five years, the USA Joint All Domain Command and Control market is expected to experience substantial growth, fueled by continuous advancements in military technology, increasing cyber threats, and growing defense budgets. The U.S. military's focus on integrating autonomous systems, real-time data analytics, and enhancing cross-domain capabilities will be key growth drivers. Furthermore, the development of next-generation AI and 5G technologies is set to transform how multi-domain operations are executed, allowing for quicker response times and improved decision-making in complex environments.

|

By Domain |

Air Land Sea Cyber Space |

|

By Technology |

AI and Machine Learning Cloud Computing Big Data Analytics 5G Connectivity Internet of Things (IoT) |

|

By Component |

Hardware Software Services |

|

By Application |

Combat Operations Intelligence Surveillance Reconnaissance (ISR) Logistics and Support Cybersecurity |

|

By Region |

North America Europe Asia-Pacific Middle East and Afric Latin America |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Integration of AI/ML in Defense Systems

3.1.2. Rising Military Modernization Efforts

3.1.3. Enhanced Focus on Cross-Domain Operations

3.1.4. Increased Defense Spending

3.2. Market Challenges

3.2.1. Cybersecurity Threats in Networked Operations

3.2.2. High Implementation Costs

3.2.3. Interoperability Issues Between Legacy Systems

3.3. Opportunities

3.3.1. Adoption of Autonomous Systems

3.3.2. Expansion of 5G Technology in Military Applications

3.3.3. Growing Focus on Space as a Military Domain

3.4. Trends

3.4.1. Increasing Utilization of Data-Centric Warfare

3.4.2. Multi-Domain Integration Efforts

3.4.3. Shift Toward Decentralized Command Structures

3.5. Government Regulations

3.5.1. U.S. Department of Defense JADC2 Strategy

3.5.2. Cybersecurity Maturity Model Certification (CMMC)

3.5.3. National Defense Authorization Act (NDAA) Provisions

3.5.4. Military AI Ethics Guidelines

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Domain (In Value %)

4.1.1. Air

4.1.2. Land

4.1.3. Sea

4.1.4. Cyber

4.1.5. Space

4.2. By Technology (In Value %)

4.2.1. AI and Machine Learning

4.2.2. Cloud Computing

4.2.3. Big Data Analytics

4.2.4. 5G Connectivity

4.2.5. Internet of Things (IoT)

4.3. By Component (In Value %)

4.3.1. Hardware

4.3.2. Software

4.3.3. Services

4.4. By Application (In Value %)

4.4.1. Combat Operations

4.4.2. Intelligence, Surveillance, and Reconnaissance (ISR)

4.4.3. Logistics and Support

4.4.4. Cybersecurity

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Middle East and Africa

4.5.5. Latin America

5.1. Detailed Profiles of Major Companies

5.1.1. Lockheed Martin Corporation

5.1.2. Raytheon Technologies Corporation

5.1.3. Northrop Grumman Corporation

5.1.4. Boeing Defense, Space & Security

5.1.5. General Dynamics Corporation

5.1.6. L3Harris Technologies, Inc.

5.1.7. BAE Systems

5.1.8. Leidos

5.1.9. CACI International Inc

5.1.10. SAIC (Science Applications International Corporation)

5.1.11. Elbit Systems

5.1.12. Thales Group

5.1.13. Kratos Defense & Security Solutions

5.1.14. Booz Allen Hamilton

5.1.15. Parsons Corporation

5.2. Cross Comparison Parameters

(Company Revenue, Military Contracts, Geographical Presence, Defense Partnerships, AI Integration Level, Cybersecurity Focus, R&D Expenditure, Number of Patents)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Defense Contracts

5.9. Private Equity Investments

6.1. DoD Regulations

6.2. Certification Processes

6.3. Cybersecurity Requirements

6.4. Operational Standards for AI and Autonomous Systems

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Domain (In Value %)

8.2. By Technology (In Value %)

8.3. By Component (In Value %)

8.4. By Application (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThis initial phase includes mapping the entire USA JADC2 market ecosystem, identifying key stakeholders such as defense contractors, government agencies, and technology providers. Comprehensive desk research is conducted to define the critical factors that influence the market.

Historical data on the USA JADC2 market is compiled and analyzed. Factors like defense budgets, military operations data, and technology adoption rates are reviewed to determine market penetration and segment performance.

Interviews with industry experts and stakeholders are conducted to validate the initial findings. These consultations provide valuable insights into market challenges, technological integration, and defense operational needs.

In this final stage, insights from major defense contractors are integrated to ensure a comprehensive understanding of market dynamics, product performance, and end-user preferences. The data is refined and verified using both top-down and bottom-up methodologies.

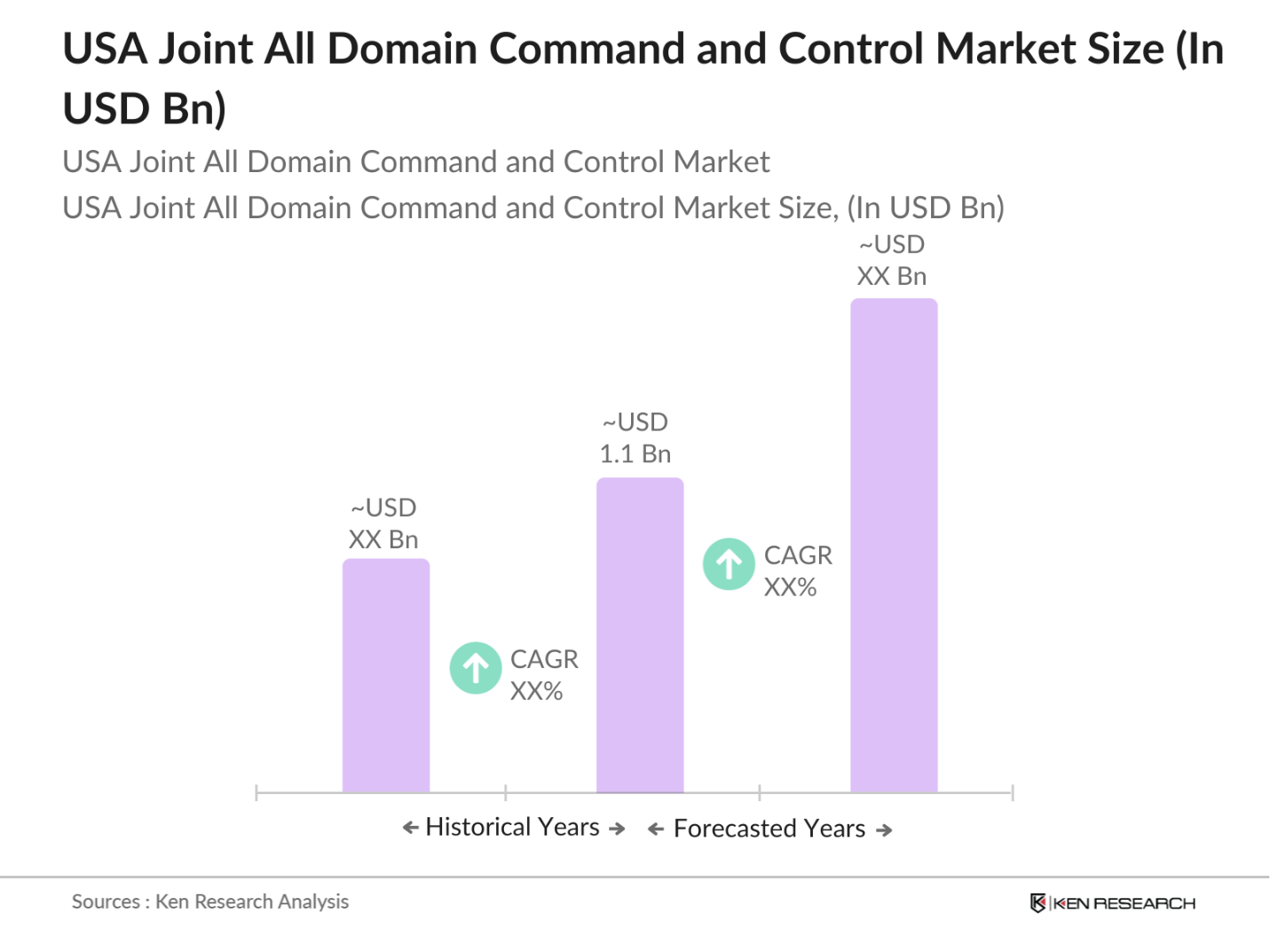

The USA Joint All Domain Command and Control market is valued at USD 1.1 billion, driven by increasing technological integration into military operations across multiple domains.

Challenges include cybersecurity threats, interoperability issues between legacy systems and modern technologies, and the high cost of implementing advanced multi-domain systems.

Key players in the market include Lockheed Martin Corporation, Raytheon Technologies Corporation, Northrop Grumman Corporation, Boeing Defense, and L3Harris Technologies.

The market is driven by advancements in AI, 5G connectivity, and increasing defense spending on multi-domain operations. The push for real-time data sharing across domains also fuels growth.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.