USA Less Lethal Guns Market Outlook to 2030

Region:North America

Author(s):Shubham Kashyap

Product Code:KROD8996

December 2024

85

About the Report

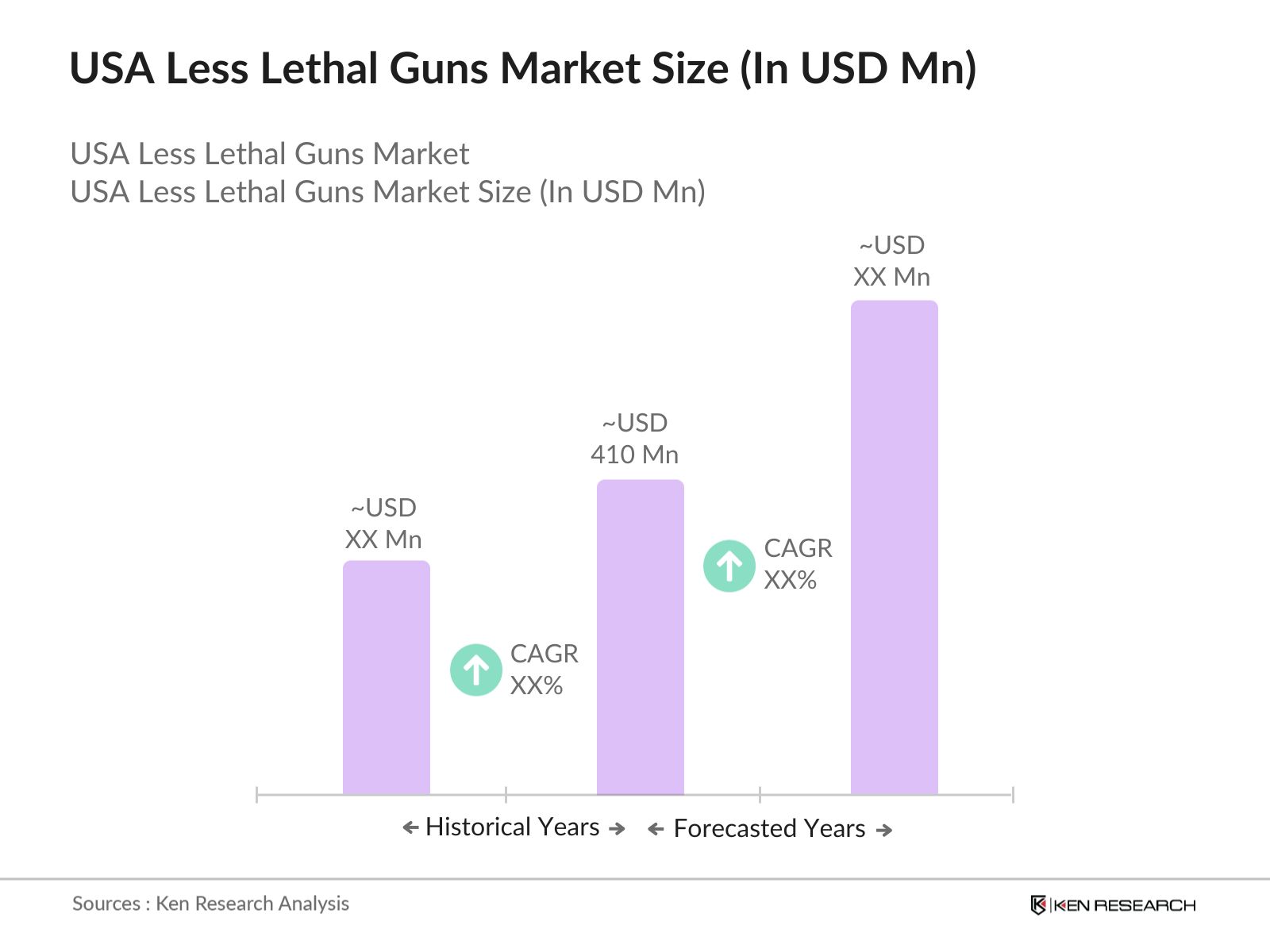

USA Less Lethal Guns Market Overview

- The USA less lethal guns market is valued at USD 410 million, primarily driven by the increasing need for non-lethal alternatives in law enforcement and personal defense sectors. As public safety concerns rise and incidents of civil unrest become more prevalent, there is a significant shift towards the adoption of less lethal weapons that can incapacitate individuals without causing permanent harm. The market continues to see growth due to advancements in technology and increased public awareness about the effectiveness of non-lethal options.

- Major demand centers for less lethal guns in the USA include metropolitan areas such as New York City, Los Angeles, and Chicago. The U.S. dominates the market due to its large law enforcement agencies, significant investment in public safety initiatives, and a growing trend among civilians seeking non-lethal self-defense solutions. These urban environments drive market growth through their emphasis on reducing lethal force and promoting de-escalation strategies in policing.

- In 2022, the U.S. Department of Justice issued updated guidelines emphasizing the necessity for transparency and accountability in the use of non-lethal technologies. These guidelines aim to standardize training procedures and operational protocols, ensuring that non-lethal weapons are employed ethically and effectively by law enforcement agencies. Additionally, individual states have enacted laws governing the possession and use of non-lethal weapons. For instance, California law permits the carrying of pepper spray up to 2.5 ounces and tasers, with certain restrictions.

USA Less Lethal Guns Market Segmentation

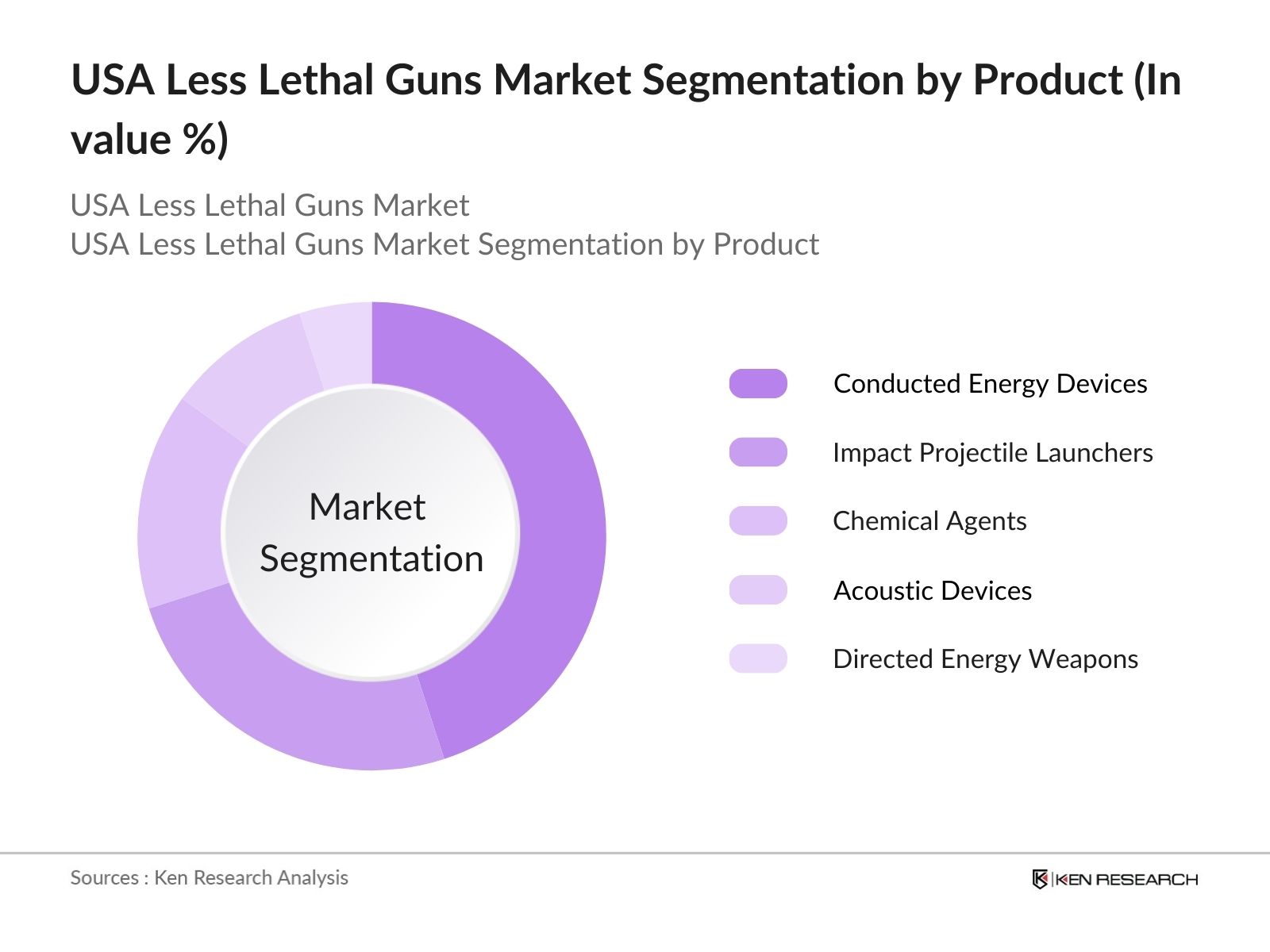

- By Product Type: The market is segmented by product type into conducted energy devices, impact projectile launchers, chemical agents, acoustic devices, and directed energy weapons. Conducted energy devices currently hold a dominant market share within this segmentation. Their effectiveness in temporarily incapacitating individuals without lasting harm makes them a preferred choice for law enforcement agencies. As public scrutiny on police use of force intensifies, the demand for these devices has surged, particularly in urban areas where crowd control is often necessary.

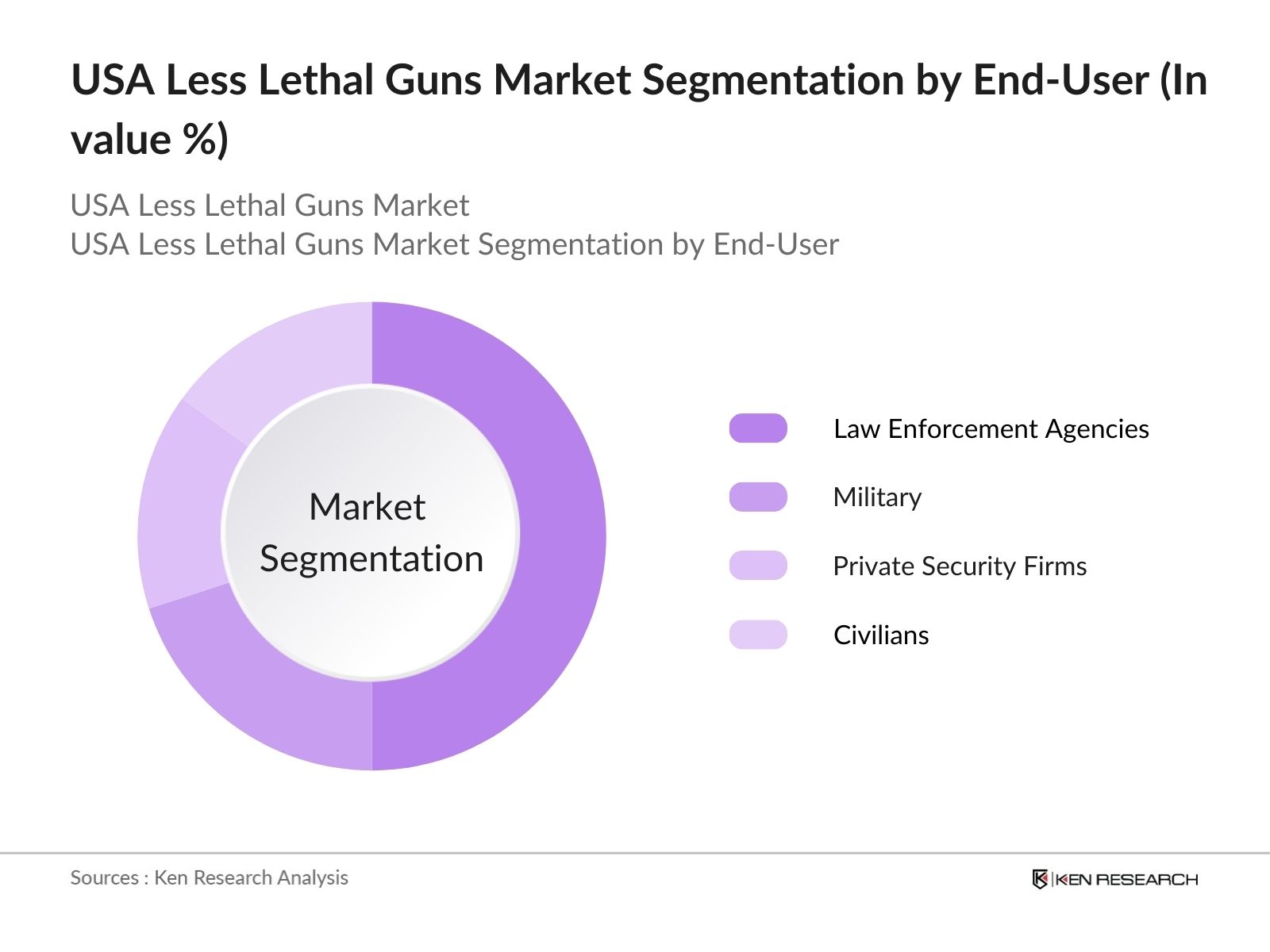

- By End-User: The market is also segmented by end-user into law enforcement agencies, military, private security firms, and civilians. Law enforcement agencies dominate this segment, driven by increasing adoption of non-lethal methods for crowd control and conflict resolution. As many police departments across the country implement policies aimed at minimizing lethal force, there is a significant push for the integration of less lethal options into standard operating procedures. This trend reflects a broader societal shift towards accountability and the prioritization of non-lethal measures.

USA Less Lethal Guns Market Competitive Landscape

The USA less lethal guns market is characterized by a competitive landscape with several major players, including Axon Enterprise, Inc., Byrna Technologies Inc., PepperBall Technologies, Inc., Safariland, LLC, and FN Herstal. These companies leverage strong brand recognition, technological innovation, and extensive distribution channels to maintain their leadership positions in the market.

USA Less Lethal Guns Market Analysis

Growth Drivers

- Archipelagic Geography Necessitating Satellite Solutions: Indonesia, comprising over 17,000 islands, faces unique challenges in providing consistent communication services across its vast archipelago. The country's reliance on satellite communication is evident as majority its population resides in remote areas, which are often inaccessible by traditional terrestrial networks. The Indonesian government has recognized this need, aiming to connect its rural and isolated regions effectively. In 2022, Indonesia's rural connectivity rate was around 55%, indicating significant room for improvement. The government plans to enhance satellite communication infrastructure to address these geographic challenges and improve connectivity for over 27 million underserved citizens.

- Government Initiatives for Digital Infrastructure: The Indonesian government is actively investing in digital infrastructure, with a focus on enhancing connectivity through satellite solutions. In 2023, it announced a noteworthy budget for digital infrastructure projects aimed at expanding internet access in underserved areas. Additionally, the Ministry of Communications and Informatics reported that as of 2022, only about 12,000 of the 83,000 villages had access to high-speed internet, underscoring the critical need for satellite communication to bridge this digital divide. These initiatives reflect a strategic priority to increase digital access and drive economic growth through improved communication networks. Ministry of Communications and Informatics, Indonesia.

- Expansion of 5G and High-Throughput Satellites: The rollout of 5G technology is expected to complement satellite communication solutions in Indonesia. By 2025, it is projected that 5G will cover majority of urban areas, enhancing mobile broadband speeds significantly. Furthermore, the increasing deployment of High-Throughput Satellites (HTS) is crucial, as these satellites can deliver internet speeds up to 1 Gbps, dramatically improving connectivity for users in rural areas. In 2023, HTS accounted for a major portion of the satellite capacity launched globally, indicating a growing trend that Indonesia can leverage to enhance its communication infrastructure. The combination of these technologies will facilitate better connectivity across diverse geographic landscapes.

Challenges

- High Initial Investment and Operational Costs: The satellite communication market in Indonesia faces significant challenges related to high initial investments and operational costs. The setup costs for satellite systems create barriers for new entrants, making it difficult to compete in the market. The ongoing operational costs per satellite can be substantial, adding to the financial burden and deterring potential investments. This situation is particularly challenging in a market where profitability remains uncertain. Additionally, ongoing maintenance and upgrades contribute to the overall financial strain, highlighting the need for government incentives and support to encourage further investment in satellite infrastructure.

- Regulatory and Spectrum Allocation Issues: Regulatory challenges and spectrum allocation issues significantly impact the growth of the satellite communication market in Indonesia. The country has faced delays in licensing new satellite operators, hindering the timely deployment of satellite services and resulting in a lack of competition and innovation in the sector. The complexity of the spectrum allocation process complicates the establishment of new satellite networks, as compliance with both national regulations and international treaties is necessary. Addressing these regulatory hurdles is essential for fostering a more competitive and efficient satellite communication market.

USA Less Lethal Guns Market Future Outlook

The USA less lethal guns market is poised for substantial growth, driven by increasing adoption by law enforcement agencies, advancements in product technology, and a heightened focus on public safety measures. As societal attitudes shift toward minimizing lethal force, the demand for innovative less lethal solutions is expected to rise significantly. The market will likely witness the introduction of advanced technologies that enhance the effectiveness and safety of these products.

Future Market Opportunities

- Integration of Low Earth Orbit (LEO) Satellites: The integration of Low Earth Orbit (LEO) satellites presents significant opportunities for the Indonesian satellite communication market. LEO satellites offer lower latency and improved data transmission speeds compared to traditional geostationary satellites. Currently, Indonesia's internet penetration stands at about 77 million users, with LEO technology potentially increasing this number significantly by providing high-speed internet access to rural and underserved areas. Several global companies are actively launching LEO constellations, which could provide Indonesia with opportunities for collaboration and technology transfer, enhancing local capabilities and fostering innovation in satellite communication solutions.

- Partnerships with International Satellite Operators: Forming strategic partnerships with international satellite operators can help enhance Indonesias satellite communication capabilities. As of 2023, majority of Indonesia's satellite capacity is sourced from international providers, highlighting the importance of collaboration. These partnerships can facilitate technology transfer, enhance local infrastructure, and improve service offerings. By leveraging expertise from established international players, Indonesia can develop its satellite ecosystem, ultimately increasing market competitiveness and addressing the growing demand for connectivity in both urban and rural regions. These alliances are crucial for ensuring that Indonesia remains at the forefront of satellite communication advancements.

Scope of the Report

|

By Product Type |

Conducted Energy Devices (e.g., Tasers) |

|

By End-User |

Law Enforcement Agencies |

|

By Technology |

Mechanical and Kinetic |

|

By Distribution Channel |

Direct Sales Distributors Online Retail |

|

By Region |

Northeast Midwest South West |

Products

Key Target Audience

Law Enforcement Agencies

Military Organizations

Private Security Firms

Civilian Self-Defense Enthusiasts

Government and Regulatory Bodies (e.g., Bureau of Alcohol, Tobacco, Firearms and Explosives)

Investors and Venture Capitalist Firms

Banks and Financial Institutions

Non-Governmental Organizations (NGOs) focusing on public safety

Companies

Players Mentioned in the Report

Axon Enterprise, Inc.

Byrna Technologies Inc.

PepperBall Technologies, Inc.

Safariland, LLC

FN Herstal

Lamperd Less Lethal, Inc.

NonLethal Technologies, Inc.

Mace Security International, Inc.

Zarc International, Inc.

Rheinmetall AG

ISPRA by EL Ltd.

Condor Non-Lethal Technologies

Bruzer Less Lethal

Armament Systems & Procedures, Inc.

Combined Systems, Inc.

Table of Contents

Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

Market Size (USD Million)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

Market Analysis

3.1 Growth Drivers

3.1.1 Rising Incidents of Civil Unrest

3.1.2 Advancements in Non-Lethal Technology

3.1.3 Increased Law Enforcement Adoption

3.1.4 Stringent Regulations on Lethal Weapons

3.2 Market Challenges

3.2.1 Ethical and Legal Concerns

3.2.2 High Development and Manufacturing Costs

3.2.3 Limited Public Awareness

3.3 Opportunities

3.3.1 Expansion into Civilian Self-Defense Market

3.3.2 Integration with Smart Technologies

3.3.3 Government Funding and Support

3.4 Trends

3.4.1 Adoption of Electroshock Weapons

3.4.2 Development of Multi-Function Devices

3.4.3 Use of Non-Lethal Drones

3.5 Government Regulations

3.5.1 Federal Guidelines on Non-Lethal Weapons

3.5.2 State-Specific Legislation

3.5.3 International Compliance Standards

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape

Market Segmentation

4.1 By Product Type (Value %)

4.1.1 Conducted Energy Devices (e.g., Tasers)

4.1.2 Impact Projectile Launchers

4.1.3 Chemical Agents (e.g., Pepper Spray)

4.1.4 Acoustic Devices

4.1.5 Directed Energy Weapons

4.2 By End-User (Value %)

4.2.1 Law Enforcement Agencies

4.2.2 Military

4.2.3 Private Security Firms

4.2.4 Civilians

4.3 By Technology (Value %)

4.3.1 Mechanical and Kinetic

4.3.2 Chemical

4.3.3 Electromagnetic

4.3.4 Acoustic

4.4 By Distribution Channel (Value %)

4.4.1 Direct Sales

4.4.2 Distributors

4.4.3 Online Retail

4.5 By Region (Value %)

4.5.1 Northeast

4.5.2 Midwest

4.5.3 South

4.5.4 West

Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Axon Enterprise, Inc.

5.1.2 Byrna Technologies Inc.

5.1.3 PepperBall Technologies, Inc.

5.1.4 Safariland, LLC

5.1.5 Combined Systems, Inc.

5.1.6 FN Herstal

5.1.7 Lamperd Less Lethal, Inc.

5.1.8 NonLethal Technologies, Inc.

5.1.9 Mace Security International, Inc.

5.1.10 Zarc International, Inc.

5.1.11 Rheinmetall AG

5.1.12 ISPRA by EL Ltd.

5.1.13 Condor Non-Lethal Technologies

5.1.14 Bruzer Less Lethal

5.1.15 Armament Systems & Procedures, Inc.

5.2 Cross Comparison Parameters

5.2.1 Number of Employees

5.2.2 Headquarters Location

5.2.3 Year of Establishment

5.2.4 Annual Revenue

5.2.5 Product Portfolio Diversity

5.2.6 Market Share Percentage

5.2.7 Recent Innovations

5.2.8 Strategic Partnerships

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.6.1 Venture Capital Funding

5.6.2 Government Grants

5.6.3 Private Equity Investments

Regulatory Framework

6.1 Federal Regulations

6.2 State-Specific Laws

6.3 Compliance Requirements

6.4 Certification Processes

Future Market Size (USD Million)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

Future Market Segmentation

8.1 By Product Type (Value %)

8.2 By End-User (Value %)

8.3 By Technology (Value %)

8.4 By Distribution Channel (Value %)

8.5 By Region (Value %)

Analysts Recommendations

9.1 Total Addressable Market (TAM) Analysis

9.2 Serviceable Available Market (SAM) Analysis

9.3 Serviceable Obtainable Market (SOM) Analysis

9.4 Customer Segmentation Analysis

9.5 Marketing Strategies

9.6 Identification of Market Gaps

9.7 Strategic Entry Points

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the USA less lethal guns market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the USA less lethal guns market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple less lethal gun manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the USA less lethal guns market.

Frequently Asked Questions

01. How big is the USA less lethal guns market?

The USA less lethal guns market is valued at USD 410 million, driven by increasing demand from law enforcement agencies and civilians seeking non-lethal self-defense options.

02. What are the challenges in the USA less lethal guns market?

Challenges in the USA less lethal guns market include ethical and legal concerns regarding their use, high development and manufacturing costs, and limited public awareness about the effectiveness and availability of non-lethal options.

03. Who are the major players in the USA less lethal guns market?

Key players in the USA less lethal guns market include Axon Enterprise, Inc., Byrna Technologies Inc., PepperBall Technologies, Inc., Safariland, LLC, and FN Herstal. These companies dominate due to their extensive product portfolios, strong distribution networks, and continuous innovation.

04. What are the growth drivers of the USA less lethal guns market?

The USA less lethal guns market is propelled by factors such as rising incidents of civil unrest, advancements in non-lethal technology, increased adoption by law enforcement agencies, and stringent regulations on lethal weapons.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.