USA Liquid Biopsy Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD3224

October 2024

95

About the Report

USA Liquid Biopsy Market Overview

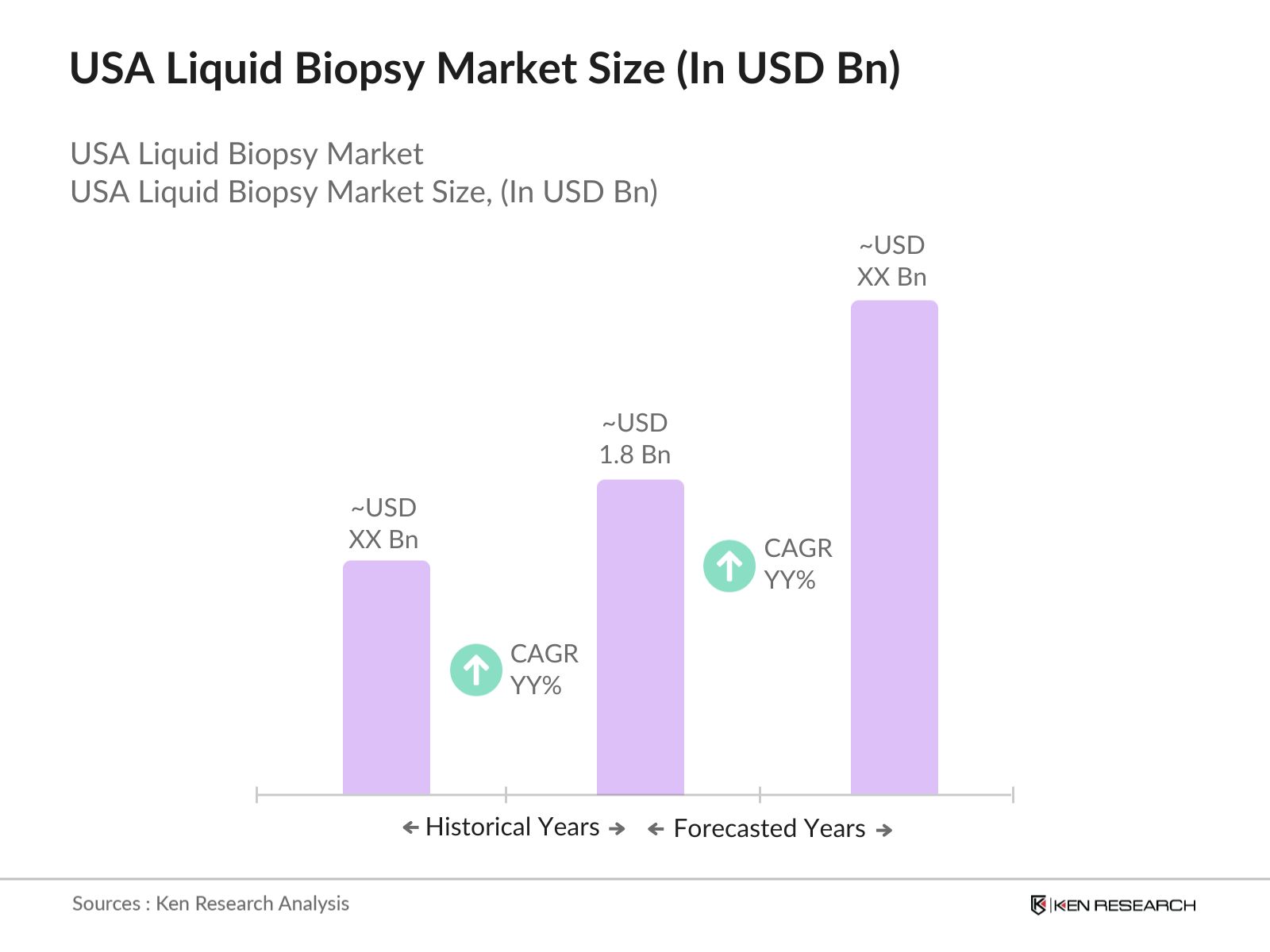

- The USA Liquid Biopsy market is valued at USD 1.8 billion based on a five-year historical analysis. This market is driven by the growing demand for non-invasive diagnostic methods, particularly in oncology, where liquid biopsies are increasingly used to detect circulating tumor DNA (ctDNA) and other biomarkers.

- The dominant regions in this market include California and Massachusetts, known for their strong presence in biotech innovation. These states house numerous leading biotech companies and research institutions, such as Illumina and Foundation Medicine, that drive liquid biopsy research and product development.

- The FDA has launched initiatives to enhance cancer detection through liquid biopsies, including the expansion of the FoundationOne Liquid CDx test. This test analyzes over 300 genes and is pivotal for identifying targeted therapies. Currently, 87% of patients incur no costs for testing, promoting accessibility in cancer care.

USA Liquid Biopsy Market Segmentation

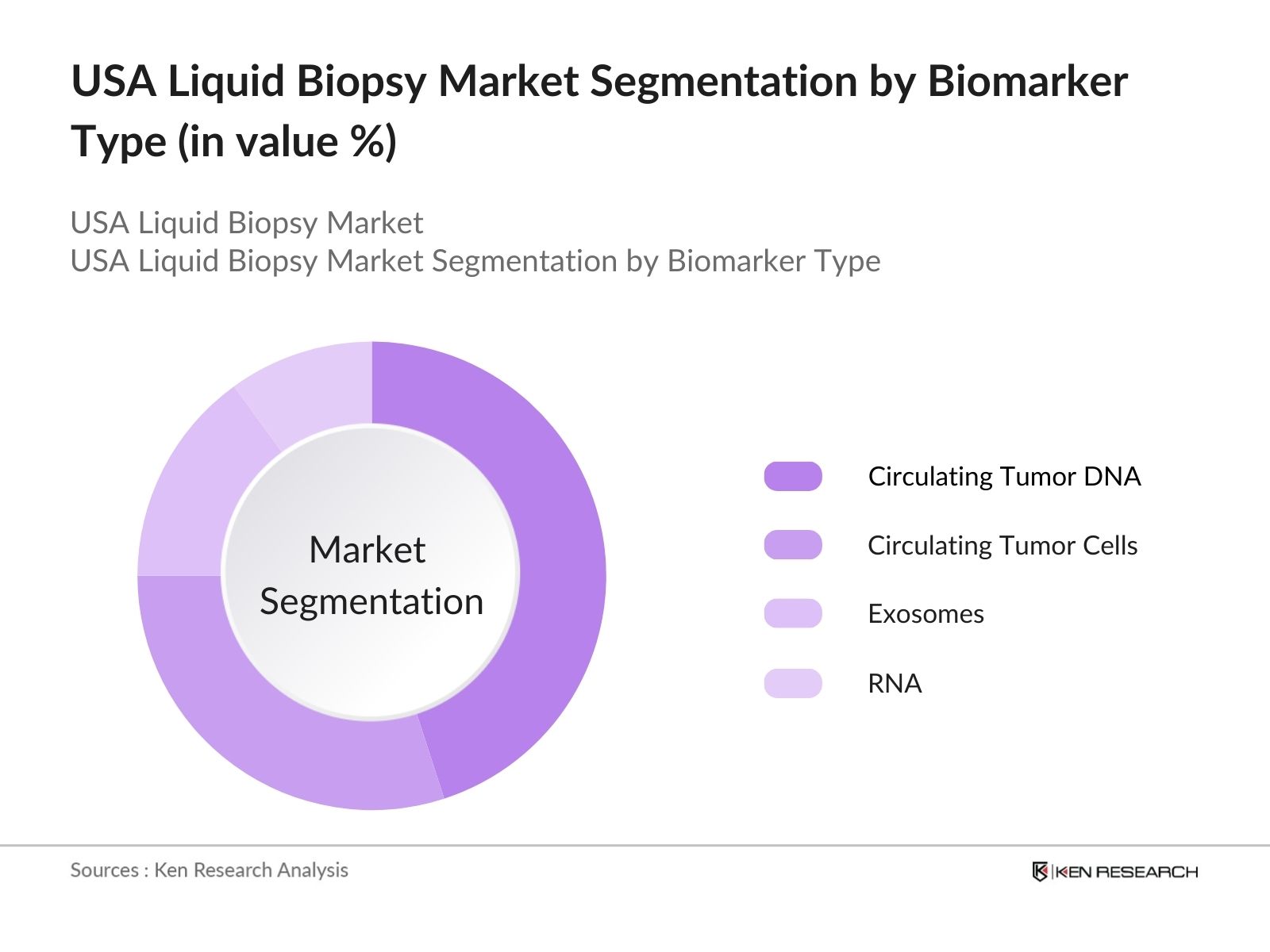

By Biomarker Type: The market is segmented by biomarker type into circulating tumor DNA (ctDNA), circulating tumor cells (CTCs), exosomes, and RNA. ctDNA dominates the market share due to its widespread use in oncology diagnostics. The high sensitivity of ctDNA in detecting genetic mutations and monitoring cancer progression makes it a preferred choice for clinicians.

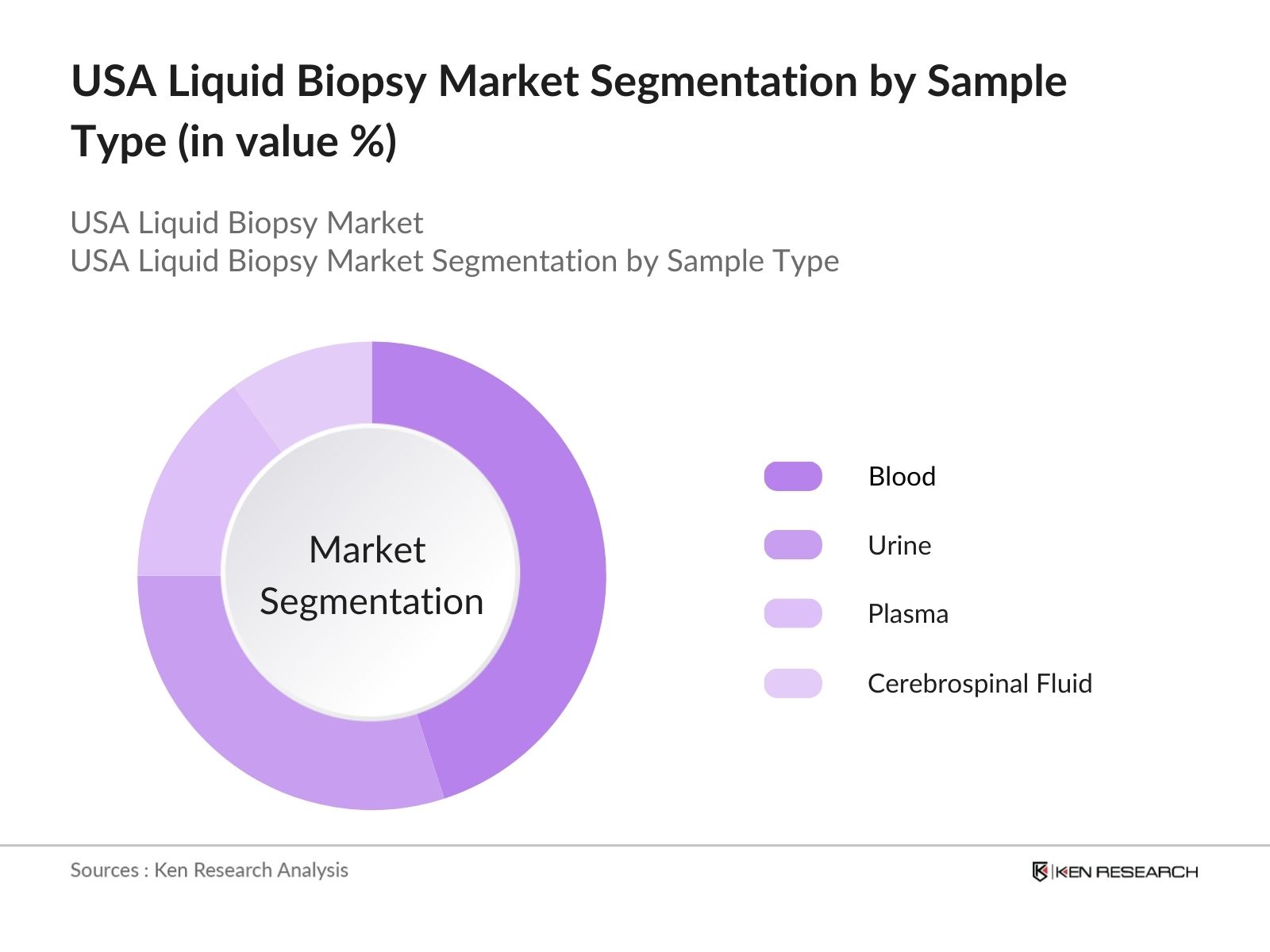

By Sample Type: The market is also segmented by sample type into blood, urine, plasma, and cerebrospinal fluid. Blood samples dominate this segment due to their ease of collection and the significant amount of tumor-derived material they contain. Blood-based liquid biopsies are considered the most practical for frequent monitoring, allowing for the detection of tumor mutations over time, which is particularly important for treatment decisions in cancer patients.

USA Liquid Biopsy Market Competitive Landscape

The market is dominated by several key players, each contributing to innovation and market growth. These companies are involved in developing cutting-edge technologies, expanding their product portfolios, and engaging in mergers and acquisitions to strengthen their market positions. The consolidation in the market is driven by technological advancements and strategic collaborations.

|

Company |

Establishment Year |

Headquarters |

Revenue |

Product Portfolio |

Patent Holdings |

R&D Expenditure |

Collaborations |

Number of Employees |

|

Guardant Health |

2012 |

Redwood City, CA |

||||||

|

Exact Sciences Corporation |

1995 |

Madison, WI |

||||||

|

Illumina, Inc. |

1998 |

San Diego, CA |

||||||

|

Foundation Medicine, Inc. |

2010 |

Cambridge, MA |

||||||

|

Roche Diagnostics |

1896 |

Basel, Switzerland |

USA Liquid Biopsy Market Analysis

Market Growth Drivers

- Increasing Incidence of Cancer: The rising global prevalence of cancer is a major growth driver for the liquid biopsy market. According to GLOBOCAN 2020 estimates, there were approximately 19.3 million new cancer cases and 10 million cancer deaths worldwide in 2020.Liquid biopsy offers early detection, non-invasive monitoring, and personalized treatment for cancer, fueling its adoption. This demand for early cancer detection, particularly in high-risk populations, is expected to increase the adoption of liquid biopsy technologies across U.S. healthcare facilities.

- Government Backing for Precision Medicine: The U.S. governments Precision Medicine Initiative, launched in 2015 and significantly expanded through 2024, continues to encourage personalized cancer treatments, including liquid biopsy applications. The National Institutes of Health (NIH) allocated over $1.5 billion in 2023 to cancer research projects aimed at advancing personalized medicine. This funding is accelerating the development of liquid biopsy technologies to enable more accurate and tailored treatment options for cancer patients, driving market demand.

- Expanding Insurance Coverage: Private and public insurance providers in the USA are increasingly covering liquid biopsy procedures, which is driving market growth. In 2023, CMS expanded its coverage to include several FDA-approved liquid biopsy tests, making these tests accessible to over 60 million Americans under Medicare. As private insurers follow suit, the adoption of liquid biopsy technologies is expected to rise, especially in oncology, where non-invasive diagnostics are in high demand.

Market Challenges

- Regulatory Challenges: Regulatory approvals for liquid biopsy technologies remain complex and time-consuming. Although the FDA has approved a few liquid biopsy tests, many other promising technologies are still awaiting clearance. This lengthy approval process can delay market entry for newer technologies and reduce the availability of cutting-edge diagnostics in U.S. healthcare facilities. The complexity of these regulations has posed challenges for manufacturers aiming to bring innovative liquid biopsy tests to the market.

- Data Privacy Concerns: The use of patient genetic information in liquid biopsies raises data privacy concerns in the USA. The Health Insurance Portability and Accountability Act (HIPAA) has stringent guidelines regarding the protection of patient data, and non-compliance can result in hefty penalties. These regulations create additional challenges for healthcare providers and diagnostic companies that rely on genetic data for liquid biopsy tests, as they must invest in robust data protection systems, increasing operational costs.

USA Liquid Biopsy Market Future Outlook

Over the next five years, the USA Liquid Biopsy industry is expected to show significant growth, driven by increasing adoption of personalized medicine, technological advancements in genomic testing, and government support for cancer research. Liquid biopsies are gaining traction as a less invasive, more comprehensive alternative to traditional tissue biopsies, particularly in oncology.

Future Market Opportunities

- Increased Integration with Artificial Intelligence: Over the next five years, the integration of artificial intelligence (AI) in liquid biopsy technologies is expected to enhance the accuracy and speed of cancer detection. AI-driven liquid biopsy platforms will likely enable faster analysis of genomic data, allowing for quicker diagnosis and more precise treatment plans.

- Expansion of At-Home Testing: The market will see a rise in at-home testing options by 2029. With advancements in sample collection and remote monitoring technologies, patients will be able to undergo liquid biopsy tests without visiting healthcare facilities. This trend is expected to expand access to diagnostics, especially in rural and underserved regions, contributing to the overall growth of the market.

Scope of the Report

|

By Biomarker Type |

Circulating Tumor DNA (ctDNA) |

|

Circulating Tumor Cells (CTCs) |

|

|

Exosomes |

|

|

RNA |

|

|

By Sample Type |

Blood |

|

Urine |

|

|

Plasma |

|

|

Cerebrospinal Fluid |

|

|

By Application |

Oncology |

|

Non-Oncology Applications |

|

|

Companion Diagnostics |

|

|

Therapy Monitoring |

|

|

By Technology |

Polymerase Chain Reaction (PCR) |

|

Next-Generation Sequencing (NGS) |

|

|

Microarrays |

|

|

Isothermal Amplification |

|

|

By End User |

Hospitals and Clinics |

|

Diagnostic Laboratories |

|

|

Research Institutes |

|

|

Pharmaceutical and Biotechnology Companies |

|

|

By Region |

North |

|

East |

|

|

West |

|

|

South |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Pharmaceutical Companies

Biotechnology Firms

Government Regulatory Bodies (FDA, NIH)

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (Centers for Medicare & Medicaid Services)

Genomics and Precision Medicine Companies

Medical Device Manufacturers

Insurance Providers

Companies

Players Mentioned in the Report:

Guardant Health

Exact Sciences Corporation

Illumina, Inc.

Foundation Medicine, Inc.

Roche Diagnostics

Biocept Inc.

NeoGenomics Laboratories

Thermo Fisher Scientific

Genomic Health

RainDance Technologies

Personal Genome Diagnostics

Qiagen

Angle Plc

Adaptive Biotechnologies

Natera Inc.

Table of Contents

1. USA Liquid Biopsy Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. USA Liquid Biopsy Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. USA Liquid Biopsy Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Prevalence of Cancer (oncology-specific driver)

3.1.2. Demand for Non-Invasive Diagnostics (minimally invasive procedures)

3.1.3. Technological Advancements in Genomic Profiling (biomarkers, NGS, cfDNA)

3.1.4. Government Initiatives for Early Cancer Detection (FDA approvals, NIH support)

3.2. Market Challenges

3.2.1. High Cost of Liquid Biopsy Tests (affordability and accessibility)

3.2.2. Limited Availability of Clinical Data (accuracy and validation concerns)

3.2.3. Regulatory Hurdles (FDA regulations and compliance)

3.2.4. Competition from Traditional Biopsy Methods (adoption challenges)

3.3. Opportunities

3.3.1. Increasing Demand for Personalized Medicine (precision medicine applications)

3.3.2. Expansion into Non-Oncology Applications (neurodegenerative and cardiovascular diseases)

3.3.3. Collaborations with Pharma for Companion Diagnostics (drug development support)

3.3.4. Growth in Home-based Testing (telemedicine and remote monitoring)

3.4. Trends

3.4.1. Integration of Artificial Intelligence in Data Analysis (AI-driven liquid biopsy platforms)

3.4.2. Rising Adoption of Circulating Tumor DNA (ctDNA) Testing

3.4.3. Expansion of Multi-Gene Panels (broad-spectrum biomarker testing)

3.4.4. Increasing Investment in Clinical Trials for Liquid Biopsy (pharmaceutical partnerships)

3.5. Government Regulations

3.5.1. FDA Guidelines for Liquid Biopsy Tests (approval standards)

3.5.2. Medicare and Reimbursement Policies (coverage for liquid biopsy diagnostics)

3.5.3. Oncology Care Model (OCM) and Its Impact on Market Adoption

3.5.4. National Cancer Institute (NCI) Initiatives (funding and support for liquid biopsy research)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. USA Liquid Biopsy Market Segmentation

4.1. By Biomarker Type (In Value %)

4.1.1. Circulating Tumor DNA (ctDNA)

4.1.2. Circulating Tumor Cells (CTCs)

4.1.3. Exosomes

4.1.4. RNA

4.2. By Sample Type (In Value %)

4.2.1. Blood

4.2.2. Urine

4.2.3. Plasma

4.2.4. Cerebrospinal Fluid

4.3. By Application (In Value %)

4.3.1. Oncology

4.3.2. Non-Oncology Applications

4.3.3. Companion Diagnostics

4.3.4. Therapy Monitoring

4.4. By Technology (In Value %)

4.4.1. Polymerase Chain Reaction (PCR)

4.4.2. Next-Generation Sequencing (NGS)

4.4.3. Microarrays

4.4.4. Isothermal Amplification

4.5. By End User (In Value %)

4.5.1. Hospitals and Clinics

4.5.2. Diagnostic Laboratories

4.5.3. Research Institutes

4.5.4. Pharmaceutical and Biotechnology Companies

4.6. By Region (In Value %)

4.6.1. North

4.6.2. East

4.6.3. West

4.6.4. South

5. USA Liquid Biopsy Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Guardant Health

5.1.2. Exact Sciences Corporation

5.1.3. Biocept Inc.

5.1.4. Foundation Medicine, Inc.

5.1.5. Roche Diagnostics

5.1.6. Illumina, Inc.

5.1.7. NeoGenomics Laboratories

5.1.8. Thermo Fisher Scientific

5.1.9. Genomic Health

5.1.10. RainDance Technologies

5.1.11. Personal Genome Diagnostics

5.1.12. Qiagen

5.1.13. Angle Plc

5.1.14. Adaptive Biotechnologies

5.1.15. Natera Inc.

5.2. (Revenue, Product Portfolio, Patent Holdings, R&D Expenditure, Collaborations, Number of Employees, Headquarters, Inception Year)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. USA Liquid Biopsy Market Regulatory Framework

6.1. FDA Approval Processes

6.2. Regulatory Compliance Standards

6.3. Intellectual Property and Patent Laws

7. USA Liquid Biopsy Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Liquid Biopsy Market Analysts' Recommendations

8.1. TAM/SAM/SOM Analysis

8.2. Customer Cohort Analysis

8.3. Marketing Initiatives

8.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial step involves mapping out the major stakeholders in the USA Liquid Biopsy market. Extensive desk research was performed using proprietary databases and public resources to identify the primary variables affecting market trends, such as biomarker types and sample collection methods.

Step 2: Market Analysis and Construction

The historical data for the USA Liquid Biopsy market was gathered and analyzed to establish a foundation for market sizing and growth forecasts. This step also involved an assessment of market penetration rates, revenue trends, and technology adoption across various sample types and biomarkers.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses regarding market growth drivers and challenges were validated through expert consultations with industry professionals from leading biotechnology firms and diagnostic laboratories. These insights were used to refine market projections and identify key trends shaping the industry.

Step 4: Research Synthesis and Final Output

Finally, direct interviews with liquid biopsy manufacturers were conducted to gather detailed insights into market performance, customer preferences, and product innovations. The data collected through this bottom-up approach ensured the accuracy and comprehensiveness of the market analysis.

Frequently Asked Questions

01. How big is the USA Liquid Biopsy Market?

The USA Liquid Biopsy market is valued at USD 1.8 billion, driven by the increasing need for non-invasive diagnostic tools in oncology and advancements in genomic testing technologies.

02. What are the challenges in the USA Liquid Biopsy Market?

Challenges in the USA Liquid Biopsy market include high costs associated with liquid biopsy tests, regulatory hurdles, and limited availability of clinical validation data, which can hinder widespread adoption.

03. Who are the major players in the USA Liquid Biopsy Market?

Key players in the USA Liquid Biopsy market include Guardant Health, Exact Sciences Corporation, Illumina, Foundation Medicine, and Roche Diagnostics, dominating the market due to their advanced technologies and extensive product portfolios.

04. What are the growth drivers of the USA Liquid Biopsy Market?

The USA Liquid Biopsy market is driven by the rising prevalence of cancer, technological advancements in next-generation sequencing, and government support for early cancer detection and personalized medicine initiatives.

05. What are the future opportunities in the USA Liquid Biopsy Market?

Future opportunities in the USA Liquid Biopsy market include expanding the use of liquid biopsies in non-oncology applications, increasing investments in research and clinical trials, and advancing the integration of artificial intelligence in diagnostic platforms.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.