USA Machine Control Systems Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD3406

October 2024

84

About the Report

USA Machine Control System Market Overview

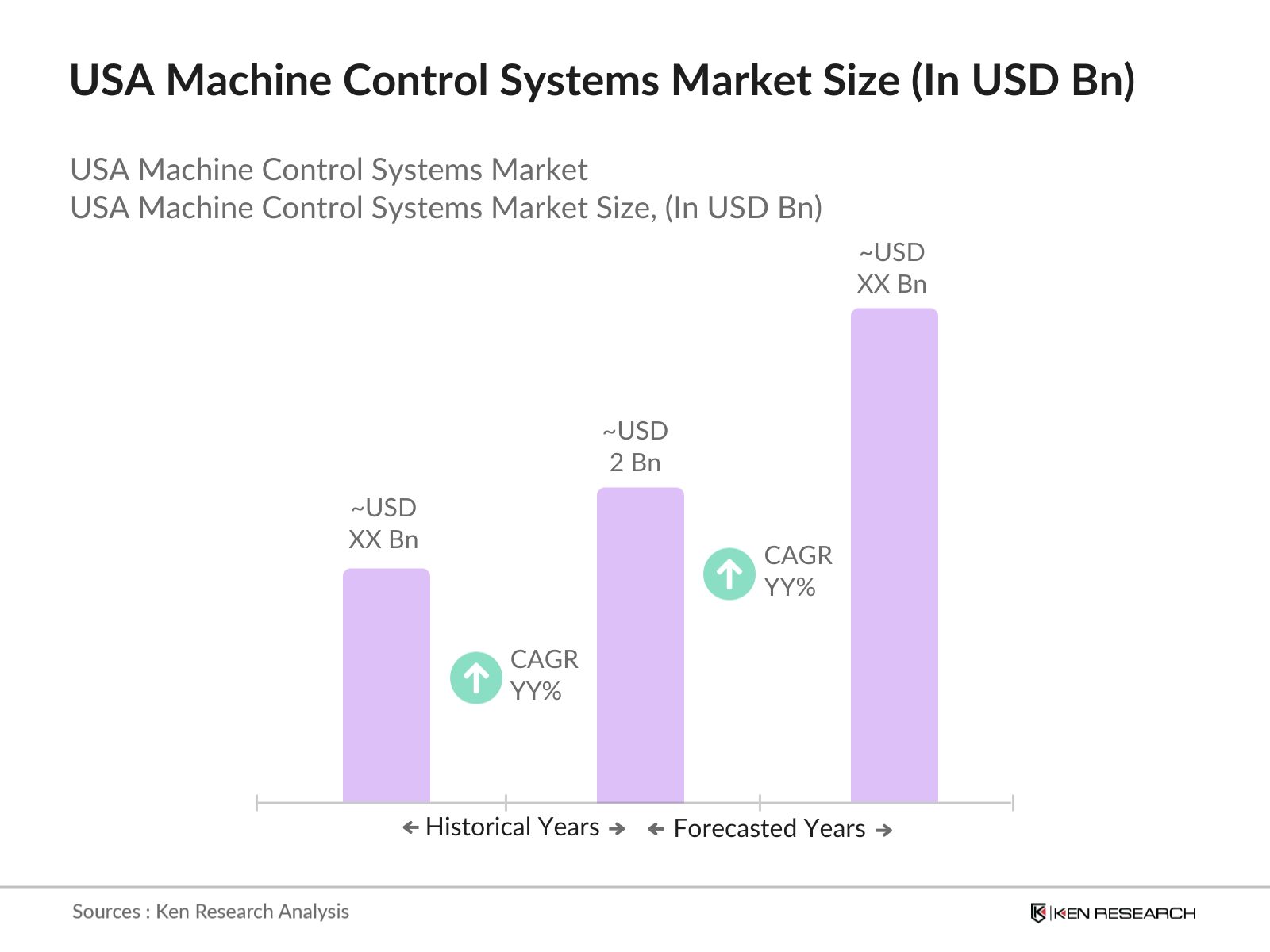

- The USA machine control systems market is valued at USD 2 billion, reflecting the growing demand for advanced technologies in the construction and mining sectors. The market has witnessed robust growth, driven by automation advancements and the need for precision and efficiency in infrastructure projects.

- The market is predominantly concentrated in major cities such as New York, Los Angeles, and Houston. These regions are hubs of large-scale infrastructure projects, such as highways, bridges, and commercial construction. Additionally, cities with extensive mining operations, like Denver, also contribute to the dominance of machine control systems in these areas.

- The U.S. governments Infrastructure Investment and Jobs Act, signed into law, continues to impact the machine control systems market. By 2024, the act had invested include$110 billionfor roads and bridges,$65 billionfor broadband expansion, and$55 billionfor clean drinking water initiatives. These projects require precise and efficient execution, making machine control systems essential for meeting tight deadlines and ensuring safety.

USA Machine Control Systems Market Segmentation

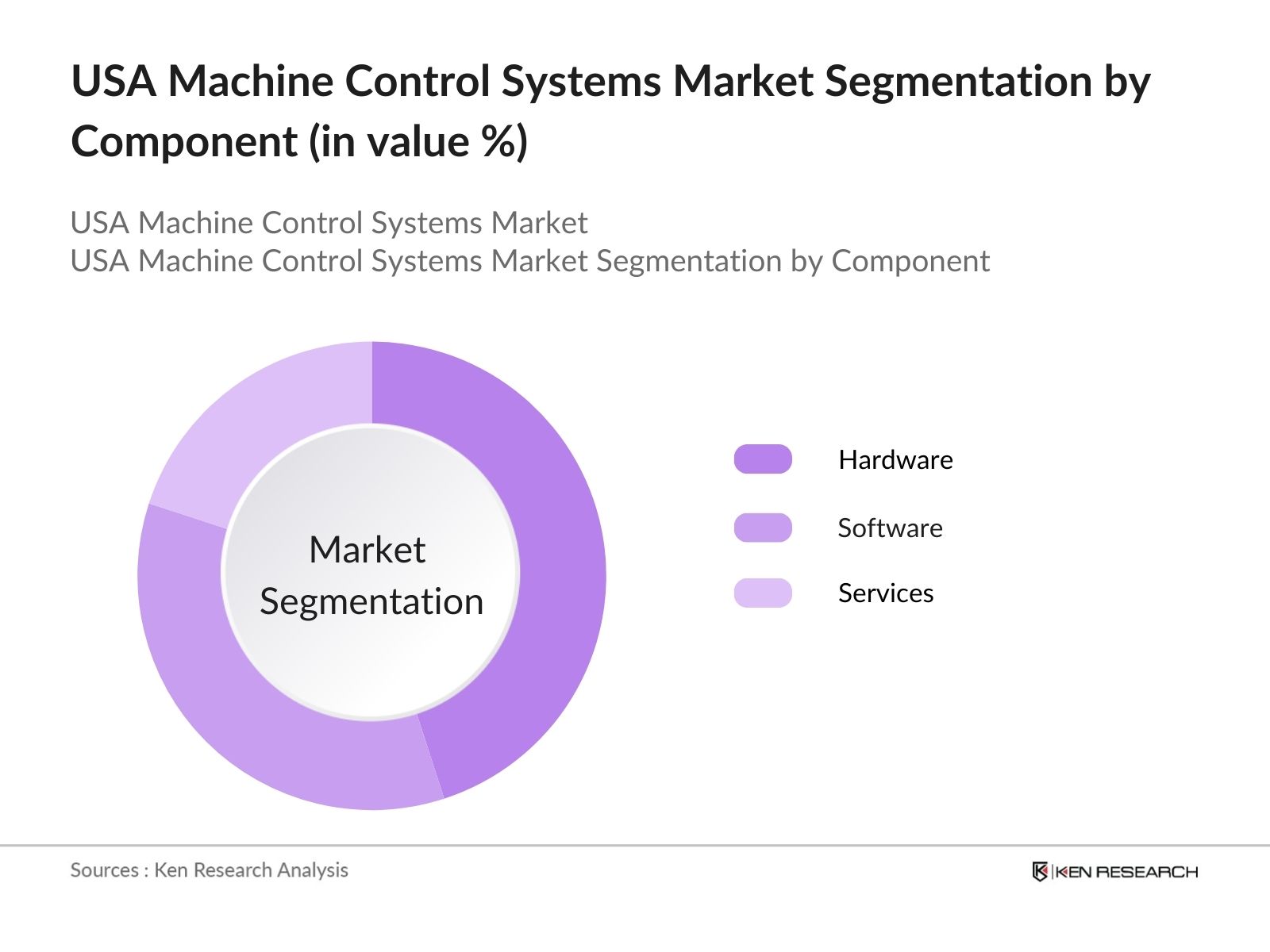

By Component: The market is segmented by component into hardware, software, and services. The hardware segment includes sensors, displays, and GNSS antennas, and dominates the market due to the essential role these components play in achieving accuracy in machine control systems. These devices are increasingly being integrated into construction and mining equipment, leading to their strong market presence.

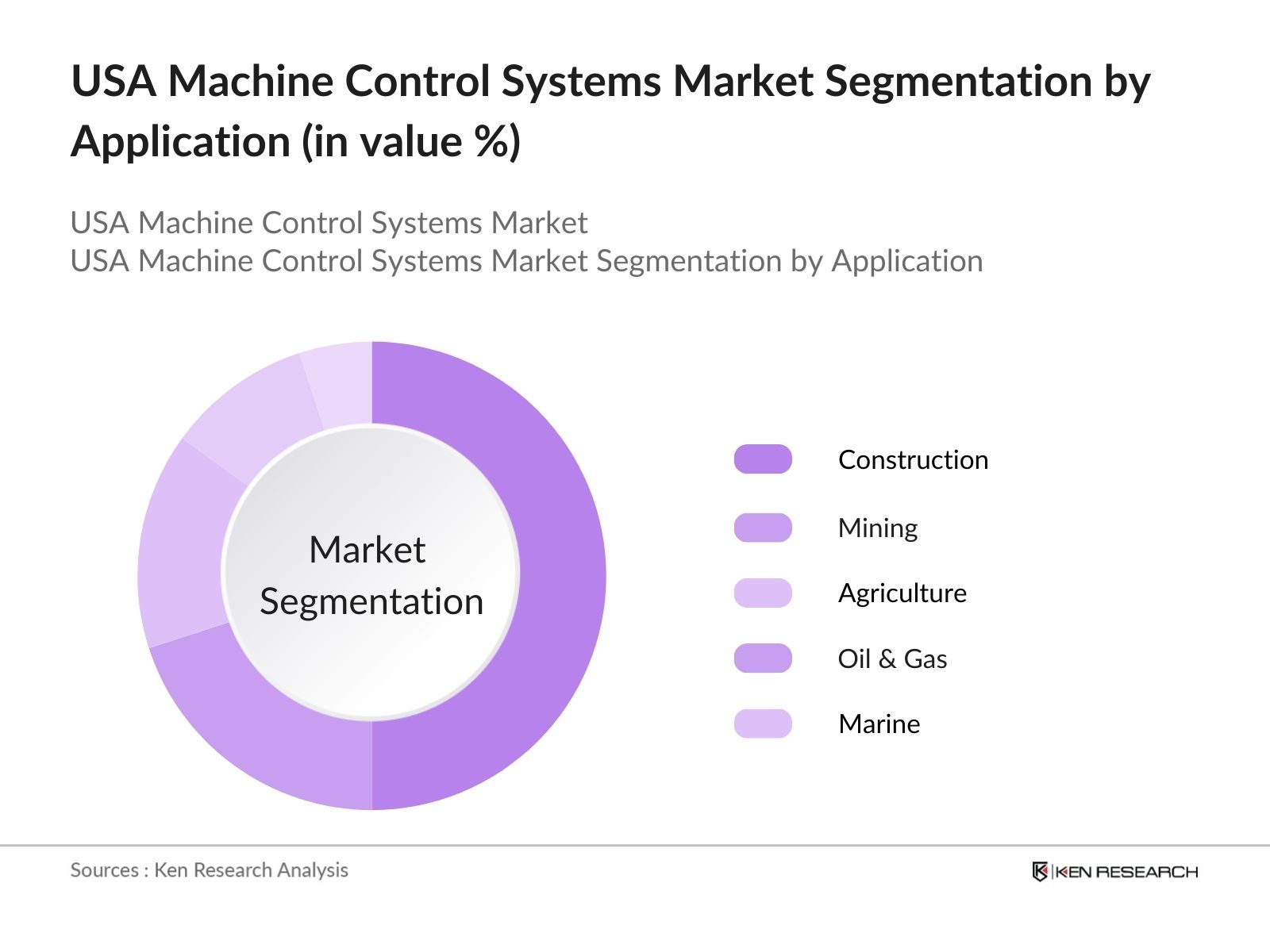

By Application: The market is segmented by application into construction, mining, agriculture, oil & gas, and marine. The construction sector holds the dominant share within the application segment, as machine control systems are critical in achieving precision, reducing labor costs, and improving safety on construction sites.

USA Machine Control Systems Market Competitive Landscape

The market is characterized by the presence of key global and domestic players. Companies such as Trimble, Leica Geosystems, and Topcon have a presence due to their extensive portfolios and innovation capabilities. The competition is further fueled by advancements in AI, robotics, and GPS technologies, making it an innovation-driven market.

|

Company Name |

Establishment Year |

Headquarters |

Product Range |

R&D Investment |

Technology Adoption |

Partnerships |

Revenue (2023) |

Market Penetration |

|

Trimble Inc. |

1978 |

Sunnyvale, California |

||||||

|

Leica Geosystems AG |

1921 |

Heerbrugg, Switzerland |

||||||

|

Topcon Corporation |

1932 |

Tokyo, Japan |

||||||

|

Komatsu Ltd. |

1921 |

Tokyo, Japan |

||||||

|

Caterpillar Inc. |

1925 |

Deerfield, Illinois |

USA Machine Control Systems Market Analysis

Market Growth Drivers

- Expansion of the Construction Industry: The market is primarily driven by the significant growth in the construction industry, particularly in public infrastructure projects. According to the U.S. Census Bureau, the value of public construction in the USA reached $487.1 billion in 2024, fueled by federal infrastructure initiatives. The demand for precision and efficiency in large-scale construction projects has led to a surge in the adoption of machine control systems, especially in projects like road development, bridges, and tunnels, where accuracy and speed are paramount to meet deadlines and budget constraints.

- Federal Support for Technological Innovation: The U.S. government has been supporting the development of innovative technologies, including machine control systems. In 2024, the U.S. Department of Energy support towards grants for automation and AI technologies in construction and agriculture. These grants aim to enhance precision, reduce waste, and improve the overall productivity of projects that implement machine control systems. This federal backing is encouraging companies to adopt these systems, ensuring future growth in both urban and rural applications.

- Increased Focus on Infrastructure Safety: The U.S. Department of Transportation has emphasized safety regulations, especially in sectors like construction and mining. In 2024, the U.S. government introduced mandates requiring automation technologies like machine control systems in specific construction zones to reduce accidents. Machine control systems improve the accuracy of heavy equipment movements, reducing the likelihood of on-site accidents and fatalities. These safety enhancements are crucial, particularly in high-risk projects, and drive the market by compelling construction firms to adopt machine control systems for compliance and risk management.

Market Challenges

- Limited Skilled Workforce: The U.S. Bureau of Labor Statistics reported in 2023 that there is a shortage of skilled workers capable of operating and maintaining machine control systems. This workforce gap is particularly noticeable in sectors like construction and agriculture, where these systems are increasingly essential. The lack of skilled technicians has led to underutilization of the technology, as companies struggle to train employees or hire specialists capable of maximizing the potential of these systems.

- Regulatory Compliance Costs: While government regulations aim to promote safety and reduce emissions, complying with these regulations often increases operational costs for firms. In 2024, the U.S. Environmental Protection Agency introduced new emissions standards that required the use of automation and machine control systems in construction equipment. While these regulations improve safety and environmental outcomes, they also result in additional costs for firms needing to upgrade machinery and integrate control systems to meet the new standards.

USA Machine Control Systems Market Future Outlook

Over the next five years, the USA machine control systems industry is expected to experience growth due to the increased adoption of automation and precision technologies in construction and mining. The ongoing infrastructure development projects, alongside advancements in GNSS and sensor technologies, will continue to drive the demand for machine control systems.

Future Market Opportunities

- Increased Adoption of Autonomous Construction Equipment: Over the next five years, the U.S. construction sector will see an increase in the use of fully autonomous construction equipment integrated with machine control systems. The U.S. Department of Transportation has already begun testing autonomous equipment on major highway projects, and this trend is expected to expand to other infrastructure projects.

- Greater Integration with Artificial Intelligence: Machine control systems will become more reliant on artificial intelligence (AI) and machine learning over the next five years. AI will enable these systems to perform predictive maintenance, self-calibration, and autonomous decision-making, reducing the need for manual intervention. By 2029, AI-enabled machine control systems are expected to dominate the market, offering increased accuracy and operational efficiency in sectors like construction, mining, and agriculture.

Scope of the Report

|

By Component |

Hardware Software Services |

|

By Application |

Construction Agriculture Mining Oil & Gas Marine |

|

By Technology |

GNSS Total Stations Laser Scanners Optical Positioning Systems |

|

By End-User |

Large Enterprises SMEs |

|

By Region |

North East West South |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Construction Companies

Mining Companies

Agriculture Equipment Manufacturers

Oil & Gas Corporations

Government and Regulatory Bodies (e.g., Federal Highway Administration)

Investment and Venture Capitalist Firms

Marine Infrastructure Firms

Bank and Financial Institutes

Companies

Players Mentioned in the Report:

Trimble Inc.

Leica Geosystems AG (Hexagon AB)

Topcon Corporation

Komatsu Ltd.

Caterpillar Inc.

Hemisphere GNSS

MOBA Mobile Automation AG

Volvo Construction Equipment

Schneider Electric

RIB Software SE

Kobelco Construction Machinery Co., Ltd.

Deere & Company

Hitachi Construction Machinery Co., Ltd.

Trimble Earthworks

CASE Construction Equipment

Table of Contents

1. USA Machine Control Systems Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. USA Machine Control Systems Market Size (In USD Billion)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. USA Machine Control Systems Market Analysis

3.1. Growth Drivers (Automation Integration, Demand for Precision, Construction Boom, Reduced Labor Costs)

3.1.1. Integration of Automation in Construction and Mining

3.1.2. Rising Demand for High Precision in Operations

3.1.3. Construction Industry Expansion

3.1.4. Cost-Efficiency Through Reduced Labor

3.2. Market Challenges (High Initial Costs, Compatibility Issues, Training Gaps, Data Security)

3.2.1. High Initial Setup Costs

3.2.2. System Compatibility Across Equipment Brands

3.2.3. Shortage of Skilled Workforce for System Operation

3.2.4. Concerns Regarding Data Security

3.3. Opportunities (Technological Advancements, Expansion in Emerging Markets, Enhanced Integration with BIM, Government Infrastructure Projects)

3.3.1. Advancements in Sensor Technology and AI Integration

3.3.2. Increasing Adoption in Emerging Economies

3.3.3. Greater Integration with Building Information Modeling (BIM)

3.3.4. Government Infrastructure Initiatives

3.4. Trends (Adoption of GNSS Technology, AI-based Machine Control, Modular Construction, Robotics Integration)

3.4.1. Adoption of GNSS for Enhanced Accuracy

3.4.2. AI and Machine Learning in Machine Control Systems

3.4.3. Shift Towards Modular Construction Techniques

3.4.4. Increasing Use of Robotics in Construction and Mining

3.5. Government Regulations (Infrastructure Funding, Emission Control Standards, Safety Standards, Certification Programs)

3.5.1. Infrastructure Funding from the US Federal Government

3.5.2. Emission Reduction Standards for Construction Equipment

3.5.3. National Safety Standards for Machine Control Usage

3.5.4. Certification Programs for Machine Control Operators

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Ecosystem

4. USA Machine Control Systems Market Segmentation

4.1. By Component (In Value %)

4.1.1. Hardware (Sensors, Displays, GNSS Antennas)

4.1.2. Software (Data Analytics, Cloud-based Solutions)

4.1.3. Services (Training, Maintenance)

4.2. By Application (In Value %)

4.2.1. Construction

4.2.2. Agriculture

4.2.3. Mining

4.2.4. Oil & Gas

4.2.5. Marine

4.3. By Technology (In Value %)

4.3.1. GNSS (Global Navigation Satellite System)

4.3.2. Total Stations

4.3.3. Laser Scanners

4.3.4. Optical Positioning Systems

4.4. By End-User (In Value %)

4.4.1. Large Enterprises

4.4.2. Small and Medium Enterprises (SMEs)

4.5. By Region (In Value %)

4.5.1. North

4.5.2. East

4.5.3. West

4.5.4. South

5. USA Machine Control Systems Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. Trimble Inc.

5.1.2. Leica Geosystems AG (Hexagon AB)

5.1.3. Topcon Corporation

5.1.4. Komatsu Ltd.

5.1.5. Caterpillar Inc.

5.1.6. Hemisphere GNSS

5.1.7. MOBA Mobile Automation AG

5.1.8. Volvo Construction Equipment

5.1.9. Schneider Electric

5.1.10. RIB Software SE

5.1.11. Kobelco Construction Machinery Co., Ltd.

5.1.12. Deere & Company

5.1.13. Hitachi Construction Machinery Co., Ltd.

5.1.14. Trimble Earthworks

5.1.15. CASE Construction Equipment

5.2. Cross Comparison Parameters (Revenue, Headquarters, Product Range, Technological Integration, R&D Spending, Market Penetration, Partnerships, Workforce Size)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, New Product Development, Joint Ventures)

5.5. Mergers & Acquisitions

5.6. Investment Analysis (Venture Capital, Private Equity)

5.7. Government Grants and Subsidies

5.8. Expansion Plans

6. USA Machine Control Systems Market Regulatory Framework

6.1. Environmental Compliance Standards

6.2. Certification and Licensing Programs

6.3. Federal and State Government Regulations

6.4. Industry-specific Safety Guidelines

7. USA Machine Control Systems Future Market Size (In USD Billion)

7.1. Future Market Size Projections

7.2. Key Factors Influencing Future Market Growth

8. USA Machine Control Systems Future Market Segmentation

8.1. By Component

8.2. By Application

8.3. By Technology

8.4. By End-User

8.5. By Region

9. USA Machine Control Systems Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Technology Adoption Roadmap

9.3. Customer Cohort Analysis

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The research began with identifying all major stakeholders in the USA machine control systems market. This involved extensive desk research using secondary databases and proprietary sources to map out the ecosystem and key variables influencing the market.

Step 2: Market Analysis and Construction

In this phase, historical data related to the machine control systems market was gathered and analyzed. This included evaluating the adoption of machine control systems across different industries, including construction, mining, and agriculture.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts were consulted through telephone interviews to validate the initial market hypotheses. Their insights helped refine the data related to system adoption, competitive dynamics, and technological advancements.

Step 4: Research Synthesis and Final Output

The final stage involved synthesizing the gathered data with insights from major machine control system manufacturers. This ensured a well-rounded and accurate analysis of market trends, competitive landscapes, and future projections.

Frequently Asked Questions

01. How big is the USA Machine Control Systems Market?

The USA machine control systems market is valued at USD 2 billion, driven by automation advancements and the increasing demand for precision in the construction and mining industries.

02. What are the challenges in the USA Machine Control Systems Market?

Challenges in the USA machine control systems market include high initial setup costs, system compatibility issues across various equipment brands, and a shortage of skilled operators familiar with the technology.

03. Who are the major players in the USA Machine Control Systems Market?

Key players in the USA machine control systems market include Trimble Inc., Leica Geosystems AG, Topcon Corporation, Komatsu Ltd., and Caterpillar Inc., all known for their extensive portfolios and technological innovations.

04. What are the growth drivers of the USA Machine Control Systems Market?

The USA machine control systems market is driven by automation integration in construction and mining, the need for precision, and significant investments in infrastructure development across major U.S. cities.

05. What is the future outlook for the USA Machine Control Systems Market?

The USA machine control systems market is expected to witness growth in the coming years, supported by technological advancements, AI integration, and government initiatives aimed at modernizing infrastructure.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.