USA Material Handling Equipment Market Outlook to 2030

Region:North America

Author(s):Naman Rohilla

Product Code:KROD9040

December 2024

93

About the Report

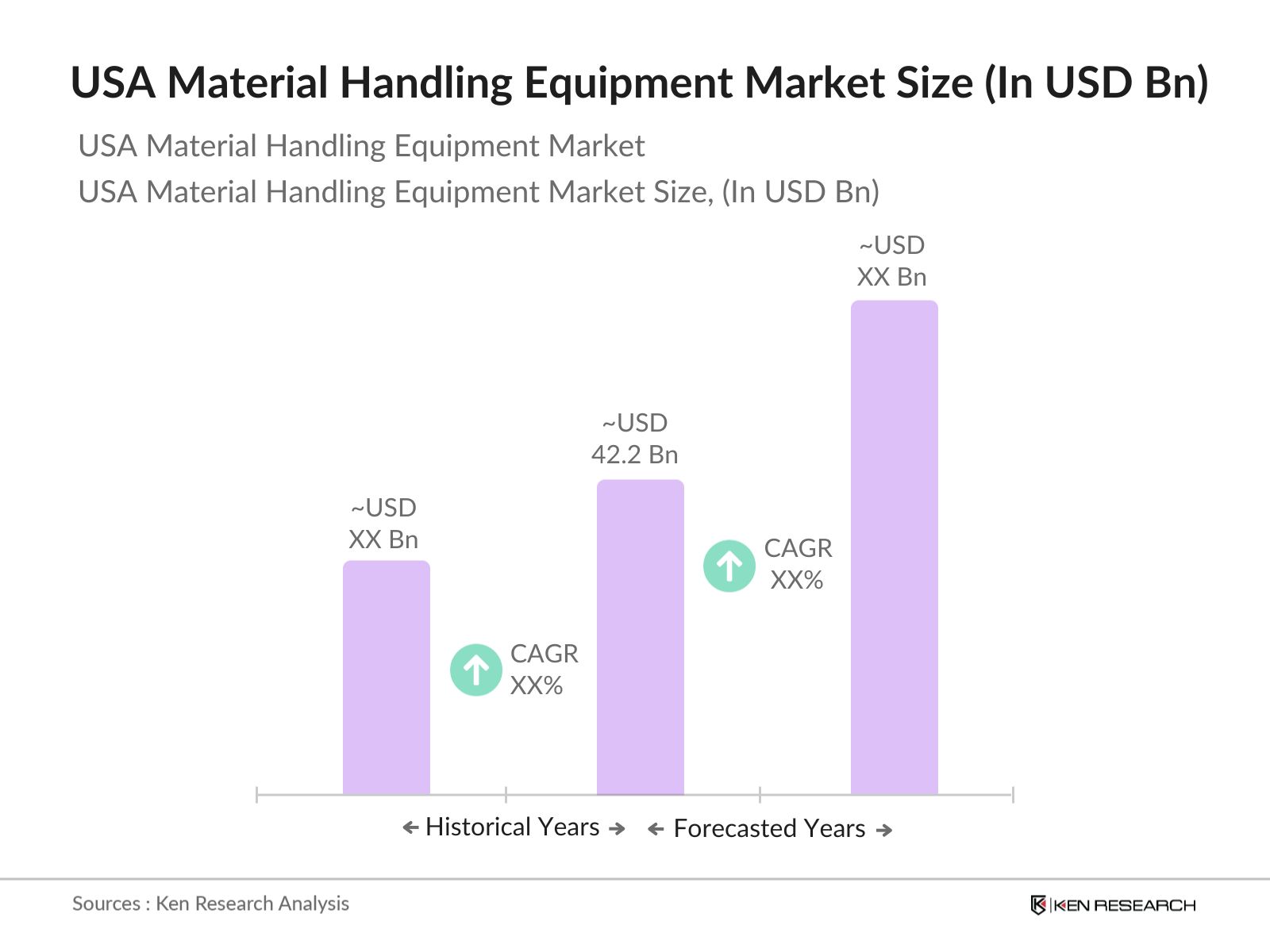

USA Material Handling Equipment Market Overview

- The USA Material Handling Equipment Market is valued at USD 42.2 billion. This valuation reflects the robust growth spurred by advancements in industrial automation and the burgeoning e-commerce sector. The demand for efficiency in logistics and warehouse operations further drives the adoption of automated systems, making material handling equipment critical for operational success. Factors such as labor shortages and the drive for improved productivity have accelerated investments in this equipment across various industries.

- Dominant regions within the U.S. include states with industrial bases and major logistics hubs, notably California, Texas, and Illinois. California, with its vast warehousing and distribution network to support both e-commerce and tech-driven logistics, holds a prominent place. Texas benefits from substantial manufacturing and energy industries, while Illinois serves as a central logistics hub, supported by extensive transportation networks that bolster its influence within the material handling equipment market.

- Occupational Safety and Health Administration (OSHA) regulations require businesses to implement safe handling practices to reduce workplace injuries. In 2023, OSHA implemented stricter guidelines, resulting in a 12% decline in handling-related injuries across warehouses. Compliance with these regulations has driven demand for safer automated systems, enhancing both worker safety and productivity.

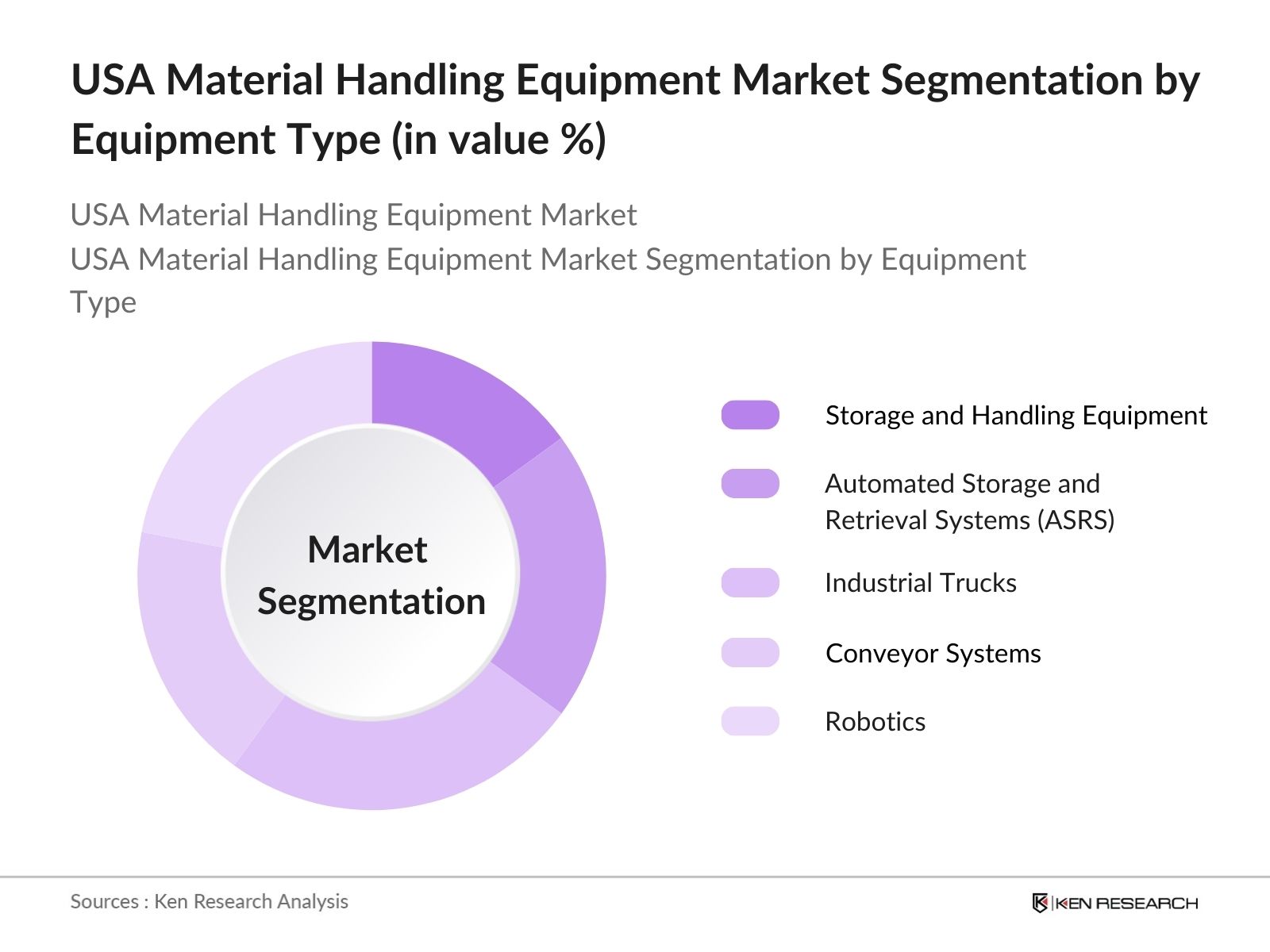

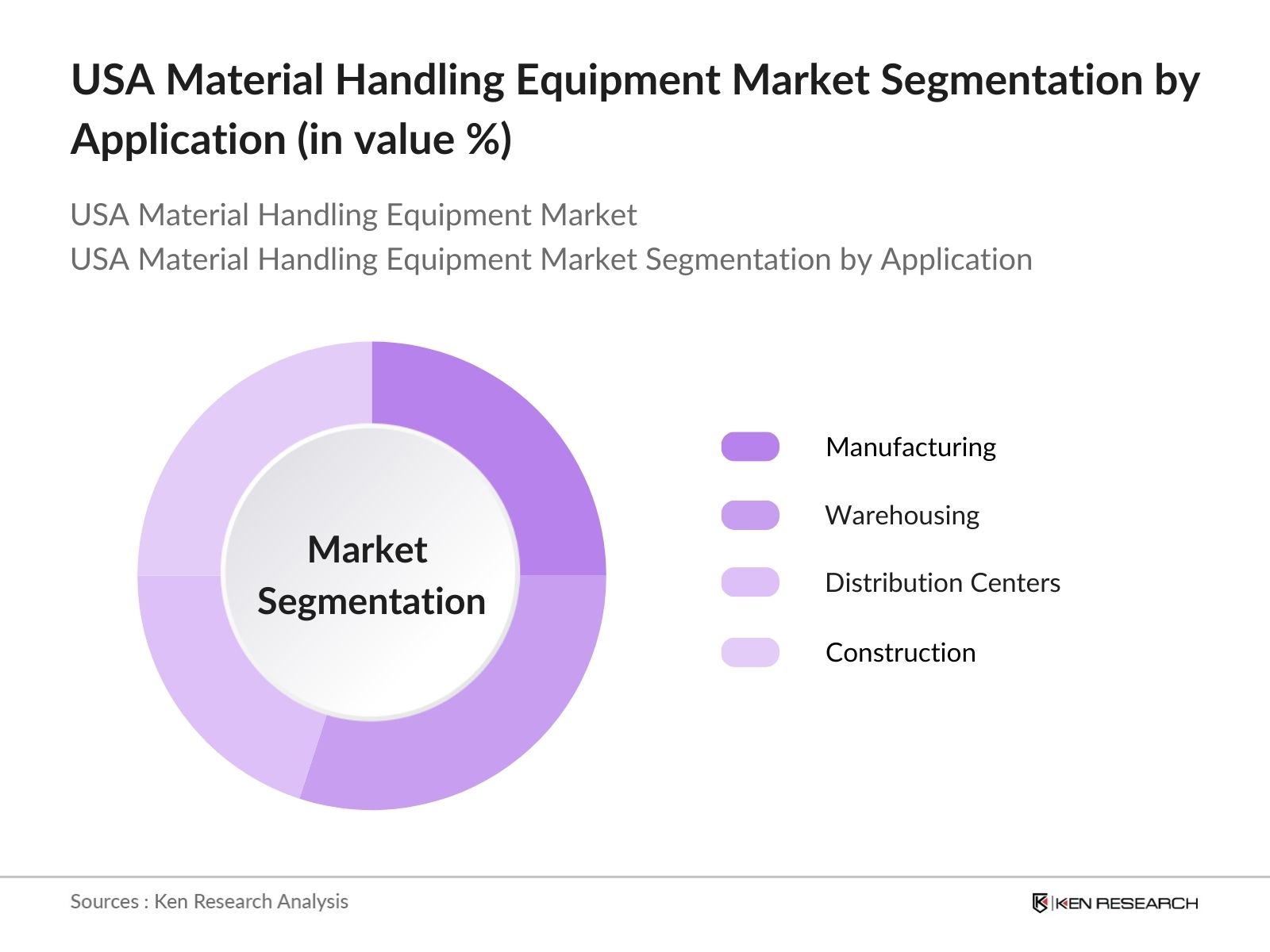

USA Material Handling Equipment Market Segmentation

- By Equipment Type: The market is segmented by equipment type into Storage and Handling Equipment, Automated Storage and Retrieval Systems (ASRS), Industrial Trucks, Conveyor Systems, and Robotics. Recently, Robotics has seen a dominant market share under this segmentation due to its essential role in automating repetitive tasks and enhancing productivity in warehouses and manufacturing facilities. Automation adoption driven by labor shortages and demand for high-speed order fulfillment solidifies robotics as a leader in this segment.

- By Application: The market is also segmented by application, including Manufacturing, Warehousing, Distribution Centers, and Construction. Within these applications, Warehousing holds a dominant position. The rapid expansion of e-commerce has fueled the need for efficient warehousing solutions, propelling investment in material handling equipment that ensures seamless storage and retrieval processes. Companies are increasingly investing in automation to address logistical challenges and increase productivity, reinforcing warehousing as a pivotal application.

USA Material Handling Equipment Market Competitive Landscape

The USA Material Handling Equipment market is primarily shaped by a few key players with extensive experience, technological prowess, and industry reach. The competition among these players promotes innovation and fosters growth through the introduction of advanced products. Leading market participants include both established domestic manufacturers and global leaders in material handling solutions.

USA Material Handling Equipment Market Analysis

Market Growth Drivers

- Industrial Automation Demand: Industrial automation in the USA is witnessing growth, driven by manufacturing sectors investing heavily in machinery for streamlined production processes. In 2023, the U.S. manufacturing sector spent over $1 trillion on capital equipment to enhance production efficiency and quality, as per the Bureau of Economic Analysis (BEA). The growth in industrial automation aligns with rising labor costs and the push for quality control. In response to this trend, material handling equipment, including robotic arms and automated conveyor systems, has seen increased adoption, fueling market expansion across multiple industries.

- E-commerce Expansion: With the rapid expansion of e-commerce, the demand for efficient warehouse and logistics solutions has surged. In 2023, U.S. e-commerce sales totaled over $1.2 trillion, leading to heightened demand for warehousing and material handling equipment, including automated sorting and retrieval systems. This growth has fueled investment in handling solutions, essential to support the higher volume and speed requirements in e-commerce fulfilment centers. This trend directly impacts material handling equipment deployment, especially in states like California and Texas, which host large distribution hubs.

- Safety and Labor Efficiency: Stringent safety regulations mandate the adoption of equipment like automated lifts, which reduce workplace injuries and increase efficiency. The Occupational Safety and Health Administration (OSHA) reported that workplace injuries in warehouses were reduced by nearly 15% between 2022 and 2023 due to automation. This decline in injuries correlates with an increase in automated handling solutions, highlighting the value of mechanized equipment in both reducing labor costs and adhering to safety standards.

Market Challenges

- High Initial Investment Costs: High initial investments required for advanced material handling solutions present a major barrier for smaller enterprises. The average cost of an industrial automated system installation can range from $50,000 to $500,000, making it challenging for businesses with limited capital budgets to adopt. This substantial financial requirement can impact small and medium-sized enterprises (SMEs), delaying their adoption of efficient material handling solutions.

- Skilled Workforce Shortage: The U.S. Bureau of Labor Statistics (BLS) reported that by 2024, the workforce gap in skilled positions, including operators and technicians for material handling systems, could result in a shortage of over 200,000 skilled positions in logistics and related industries. This shortage affects the markets capacity to scale operations, as finding skilled labor becomes increasingly challenging, impacting the pace at which companies can adopt complex handling solutions.

USA Material Handling Equipment Market Future Outlook

Over the coming years, the USA Material Handling Equipment market is anticipated to experience substantial growth, driven by technological advancements and an increasing emphasis on automation across sectors. The accelerated digital transformation within logistics and warehousing, coupled with heightened demand for operational efficiency, is expected to fuel market expansion further. Sustainable practices and the integration of green technologies are also projected to play a crucial role in shaping future industry developments, aligning with the global movement toward eco-friendly industrial practices.

Market Opportunities

- Advancements in Robotics: Robotics in material handling, particularly collaborative robots (cobots), is advancing rapidly. The U.S. robotics sector saw investments of over $6 billion in 2023, driven by the manufacturing and logistics industries. Cobots that assist workers in tasks such as sorting and lifting are gaining popularity due to their flexibility and ease of integration. These advancements allow companies to boost productivity and manage high-volume operations, creating opportunities for growth in the material handling equipment market.

- Increasing Demand for Green Logistics: The U.S. Environmental Protection Agency (EPA) emphasizes green logistics, encouraging the adoption of electric and energy-efficient equipment to reduce carbon footprints. As of 2024, nearly 20,000 companies in the logistics sector had committed to green initiatives, leading to an increased demand for sustainable material handling solutions like energy-efficient forklifts and electric conveyors. This trend is opening doors for equipment manufacturers focused on green technology.

Scope of the Report

|

Equipment Type |

Storage and Handling Equipment Automated Storage Retrieval Systems (ASRS) Industrial Trucks Conveyor Systems Robotics |

|

Function |

Storage Transport Assembly Sorting |

|

Application |

Manufacturing Warehousing Distribution Centers Construction |

|

Industry Vertical |

Automotive Retail and E-commerce Food and Beverage Chemicals |

|

Region |

Northeast Midwest South West |

Products

Key Target Audience

Material Handling Equipment Manufacturers

E-commerce and Retail Warehousing Facilities

Industrial Automation Firms

Banks and Financial Institutions

Automotive and Aerospace Manufacturers

Government and Regulatory Bodies (OSHA, EPA)

Logistics and Distribution Centers

Investor and Venture Capitalist Firms

Robotics and AI Technology Providers

Companies

Players Mentioned in the Report

Toyota Industries Corporation

KION Group

Crown Equipment Corporation

Honeywell Intelligrated

Daifuku Co., Ltd.

Jungheinrich AG

Hyster-Yale Materials Handling

SSI Schaefer

BEUMER Group

Murata Machinery

Table of Contents

1. USA Material Handling Equipment Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Key Market Dynamics

1.4. Value Chain Analysis

2. USA Material Handling Equipment Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Market Growth Trends

2.3. Key Industry Developments

3. USA Material Handling Equipment Market Analysis

3.1. Growth Drivers

3.1.1. Industrial Automation Demand

3.1.2. E-commerce Expansion

3.1.3. Government Infrastructure Investments

3.1.4. Safety and Labor Efficiency

3.2. Market Challenges

3.2.1. High Initial Investment Costs

3.2.2. Skilled Workforce Shortage

3.2.3. Technological Compatibility Issues

3.3. Opportunities

3.3.1. Advancements in Robotics

3.3.2. Increasing Demand for Green Logistics

3.3.3. Urban Warehousing Growth

3.4. Trends

3.4.1. Integration of IoT in Equipment

3.4.2. Adoption of Automated Guided Vehicles (AGVs)

3.4.3. Growth of Modular Solutions

3.5. Regulatory Landscape

3.5.1. OSHA Compliance

3.5.2. Environmental Regulations

3.5.3. Safety Standards

3.6. SWOT Analysis

3.7. Porters Five Forces Analysis

3.8. Competitive Ecosystem Overview

4. USA Material Handling Equipment Market Segmentation

4.1. By Equipment Type (In Value %)

4.1.1. Storage and Handling Equipment

4.1.2. Automated Storage Retrieval Systems (ASRS)

4.1.3. Industrial Trucks

4.1.4. Conveyor Systems

4.1.5. Robotics

4.2. By Function (In Value %)

4.2.1. Storage

4.2.2. Transport

4.2.3. Assembly

4.2.4. Sorting

4.3. By Application (In Value %)

4.3.1. Manufacturing

4.3.2. Warehousing

4.3.3. Distribution Centers

4.3.4. Construction

4.4. By Industry Vertical (In Value %)

4.4.1. Automotive

4.4.2. Retail and E-commerce

4.4.3. Food and Beverage

4.4.4. Chemicals

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

5. USA Material Handling Equipment Market Competitive Analysis

5.1. Profiles of Major Competitors

5.1.1. Toyota Industries Corporation

5.1.2. KION Group

5.1.3. Mitsubishi Logisnext

5.1.4. Jungheinrich AG

5.1.5. Crown Equipment Corporation

5.1.6. Hyster-Yale Materials Handling

5.1.7. Daifuku Co., Ltd.

5.1.8. SSI Schaefer

5.1.9. BEUMER Group

5.1.10. Honeywell Intelligrated

5.1.11. KNAPP AG

5.1.12. Vanderlande Industries

5.1.13. Fives Group

5.1.14. Murata Machinery

5.1.15. Swisslog

5.2. Cross Comparison Parameters (Number of Employees, Headquarters, Inception Year, Revenue, Product Offerings, R&D Investments, Manufacturing Capabilities, Key Clientele)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers & Acquisitions

5.6. Investment Analysis

5.7. Key Partnerships

5.8. Recent Product Launches

6. USA Material Handling Equipment Market Regulatory Framework

6.1. Environmental Standards

6.2. Compliance Mandates

6.3. Certification Processes

7. USA Material Handling Equipment Market Analysts Recommendations

7.1. Market Expansion Strategies

7.2. Product Differentiation Opportunities

7.3. Technology Investment Focus

7.4. White Space Opportunity Analysis

8. USA Material Handling Equipment Market Future Market Segmentation

8.1. By Equipment Type (In Value %)

8.2. By Function (In Value %)

8.3. By Application (In Value %)

8.4. By Industry Vertical (In Value %)

8.5. By Region (In Value %)

9. USA Material Handling Equipment Market Analysts Recommendations

9.1. Market Expansion Strategies

9.2. Product Differentiation Opportunities

9.3. Technology Investment Focus

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

An initial mapping of the USA Material Handling Equipment Market was conducted to identify core stakeholders, equipment types, and applications. This was supported by data collection from secondary databases and proprietary sources to define primary variables impacting market dynamics.

Step 2: Market Analysis and Construction

Historical data was compiled and analyzed, focusing on factors such as equipment adoption rates and the prevalence of automation technologies. This phase also examined the penetration of digital systems and IoT integration across key industry sectors.

Step 3: Hypothesis Validation and Expert Consultation

Data-driven hypotheses were formulated and validated through consultations with industry experts, enabling an in-depth understanding of market shifts. This step also included extensive engagement with experts in automation, warehousing, and logistics.

Step 4: Research Synthesis and Final Output

The final research output was synthesized through interactions with market stakeholders and manufacturers to cross-verify data accuracy. The bottom-up approach utilized ensured precision in the statistical and market data presented in this report.

Frequently Asked Questions

01. How big is the USA Material Handling Equipment Market?

The USA Material Handling Equipment Market is valued at USD 42.2 bn, largely fueled by industrial automation and the e-commerce boom that demands robust warehousing infrastructure.

02. What are the primary challenges in the USA Material Handling Equipment Market?

Key challenges include high capital costs, a shortage of skilled labor, and integration hurdles with existing infrastructure, which can impede the seamless deployment of advanced equipment.

03. Who are the major players in the USA Material Handling Equipment Market?

Leading players include Toyota Industries Corporation, KION Group, and Crown Equipment Corporation, recognized for their advanced product lines and innovation in automation solutions.

04. What factors drive the USA Material Handling Equipment Market?

Market growth is propelled by a rise in e-commerce, an expanding logistics sector, and increasing industrial automation, each contributing to the demand for material handling solutions.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.