USA Medical Billing Outsourcing Market Outlook to 2030

Region:North America

Author(s):Vijay Kumar

Product Code:KROD4783

December 2024

90

About the Report

USA Medical Billing Outsourcing Market Overview

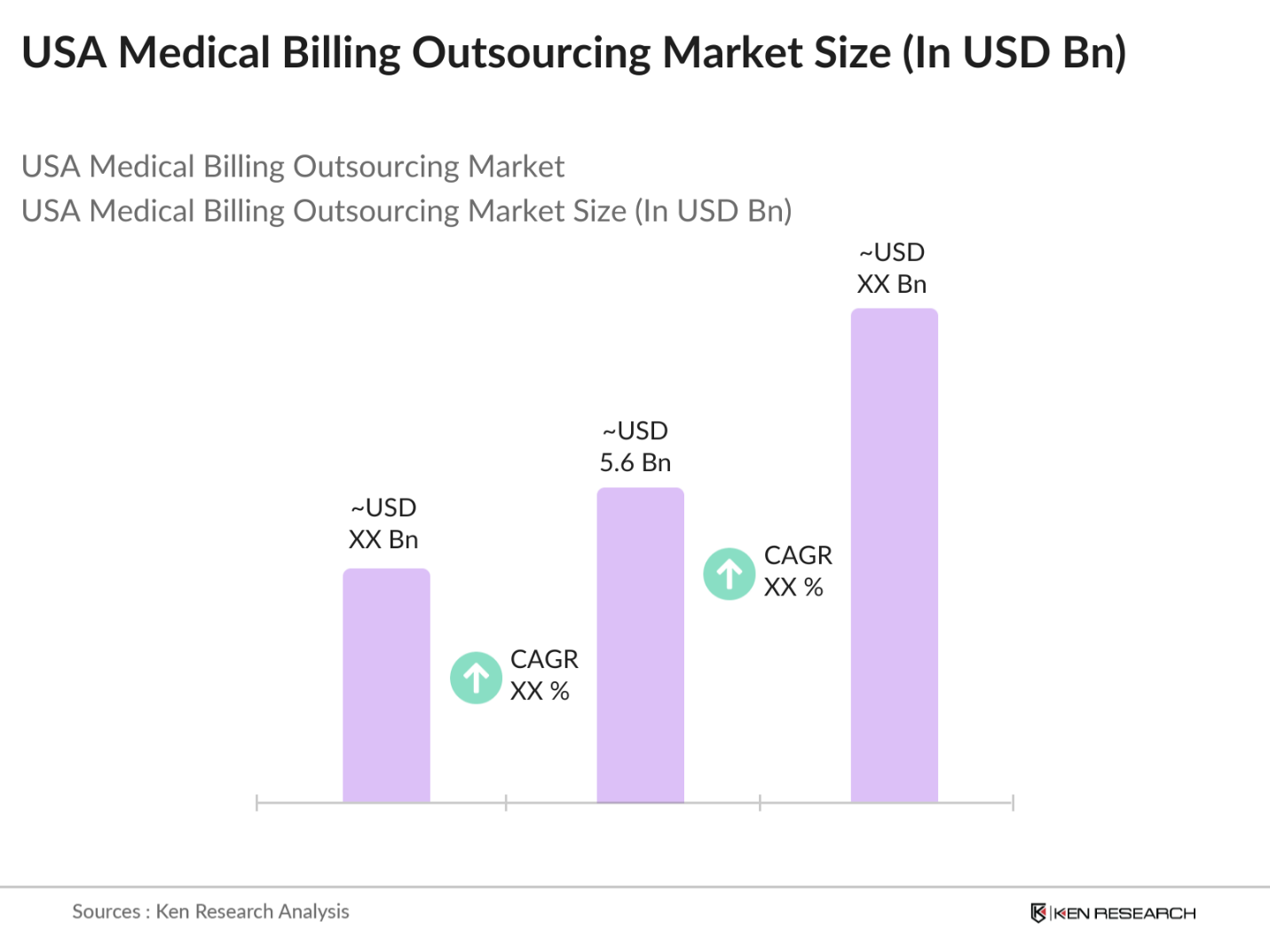

- The USA Medical Billing Outsourcing Market is valued at USD 5.6 billion, based on a five-year historical analysis. This market is primarily driven by the increasing complexities of healthcare regulations, such as HIPAA compliance, and the rising adoption of revenue cycle management (RCM) solutions across healthcare providers. The shift towards value-based care models has prompted healthcare organizations to streamline billing operations, reduce administrative costs, and maintain compliance, thereby enhancing the demand for outsourcing these services.

- Dominant regions in the USA Medical Billing Outsourcing Market include states like California, New York, and Texas. These regions are hubs for the healthcare industry with a high density of healthcare facilities and physicians, driving a higher demand for outsourced billing services. The dominance is primarily due to the extensive number of private practices, large hospital networks, and a higher adoption of advanced IT systems in healthcare administration.

- The stringent compliance requirements for Medicare and Medicaid programs necessitate constant updates and monitoring, making it challenging for healthcare providers to manage these processes in-house. Outsourcing firms with expertise in these areas provide valuable support in navigating these complex regulations, ensuring accurate billing and minimizing compliance risks.

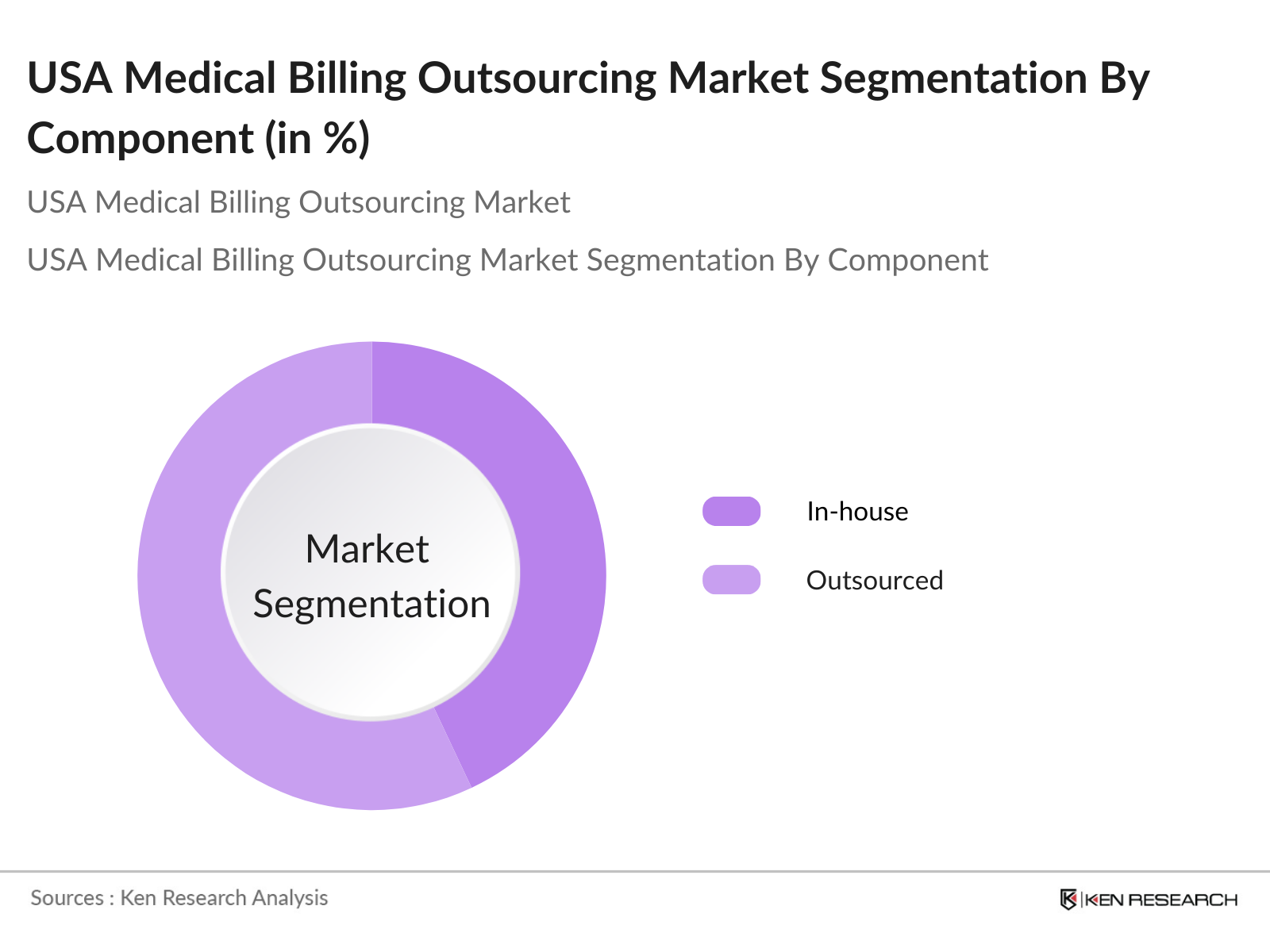

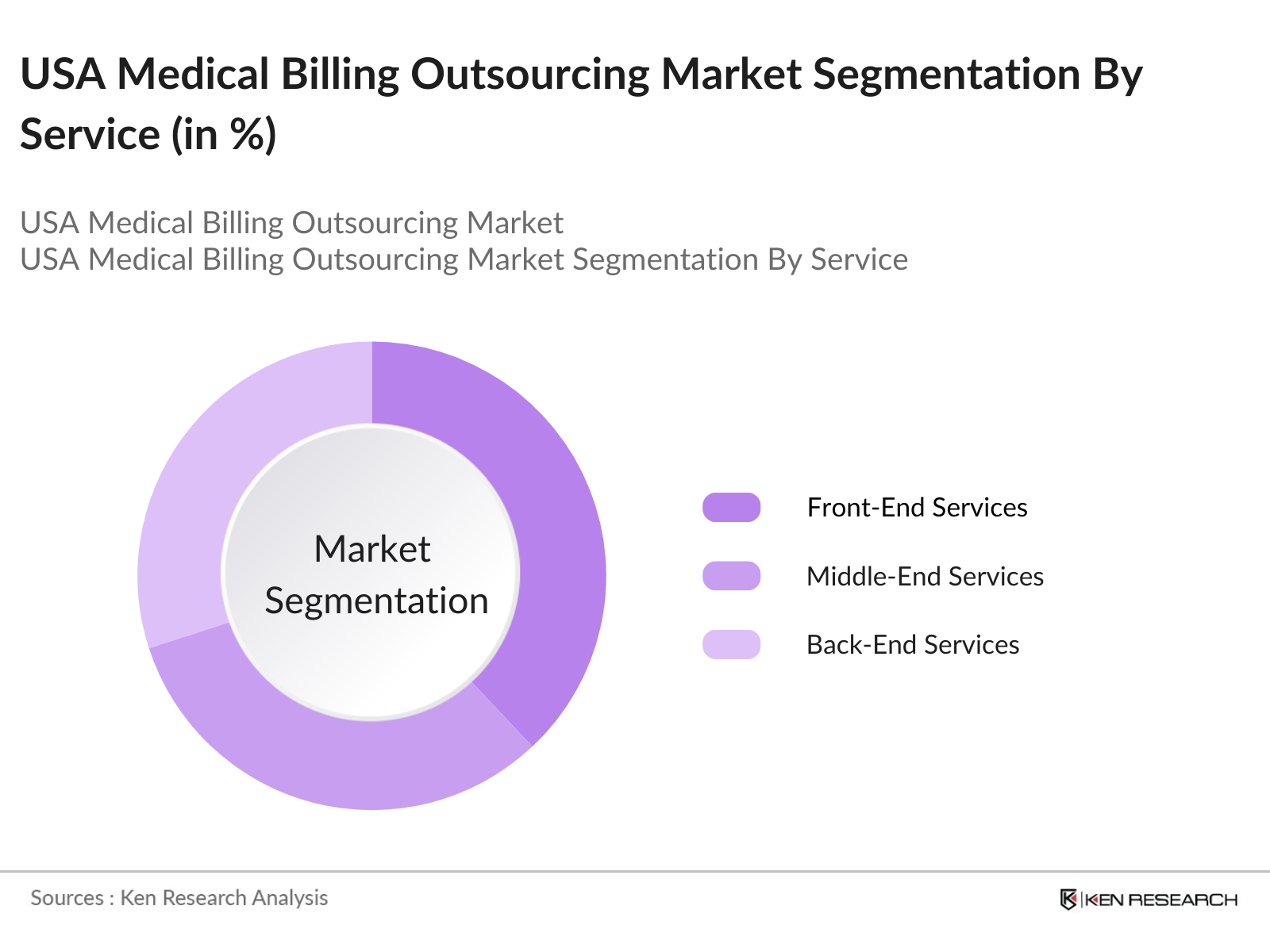

USA Medical Billing Outsourcing Market Segmentation

By Component: The market is segmented by component into In-house and Outsourced billing services. Outsourced billing services are the dominant segment, accounting for 57% of the market share in 2023. The dominance of outsourced billing can be attributed to the rising pressure on healthcare providers to reduce costs and improve operational efficiency.

By Service: The market is further segmented by service type into Front-End Services, Middle-End Services, and Back-End Services. The front-end services segment held the largest share of over 38% in 2023. This includes patient scheduling, pre-registration, eligibility verification, and insurance pre-authorization. The front-end services are critical for ensuring that patient information is accurately recorded and validated before treatment, reducing claim denials and improving patient satisfaction.

USA Medical Billing Outsourcing Market Competitive Landscape

The USA Medical Billing Outsourcing Market is consolidated, with a few major players holding a significant market share. Key companies like R1RCM Inc., Veradigm LLC, Oracle (Cerner Corporation), McKesson Corporation, and AdvancedMD Inc. dominate the competitive landscape. These companies leverage their established networks, technological expertise, and comprehensive service portfolios to cater to a wide array of healthcare providers.

USA Medical Billing Outsourcing Industry Analysis

Growth Drivers

- Increasing Emphasis on Compliance and Risk Management: The emphasis on compliance and risk management in the U.S. healthcare sector has grown due to increased regulatory scrutiny. Public Financial Management (PFM) systems in the healthcare industry are crucial for mitigating risk, ensuring compliance, and preventing financial mismanagement. These systems are continuously evolving to handle crises, such as the COVID-19 pandemic, which exposed weaknesses in risk management practices across many sectors, including healthcare.

- Technological Integration in Revenue Cycle Management (RCM): Technological advancements are transforming Revenue Cycle Management (RCM) by integrating automation and AI to optimize billing processes, reduce claim denials, and enhance cash flow. The IMF reports that the integration of these technologies is critical in addressing inefficiencies and high operational costs within the healthcare system, which saw labor costs for healthcare practitioners rise by 2-3% more in Medicaid expansion states over a five-year period.

- Cost Containment Strategies: The high cost of healthcare in the U.S., which stood at $3.8 trillion or $11,000 per person in 2019, has led to the adoption of outsourcing as a cost-containment strategy. Outsourcing helps healthcare providers manage administrative expenses and focus on core clinical activities. Given that the share of healthcare costs in the GDP rose from 5% in 1960 to about 18% in recent years, outsourcing RCM functions is seen as a viable strategy to control rising costs and improve financial management.

Market Challenges

- Data Breaches and Privacy Issues: The digital transformation of the healthcare industry has heightened the risk of data breaches and privacy violations. The U.S. healthcare sector is frequently targeted for cyberattacks, leading to significant financial and reputational damage. Managing this risk is crucial, as the healthcare industry deals with sensitive personal data and must comply with stringent data protection regulations such as HIPAA, which adds complexity to outsourcing relationships.

- High Costs of Technology Adoption: While technological integration is a driver for market growth, the initial investment required for adopting advanced RCM technologies is a barrier for many healthcare providers, especially smaller practices. This financial burden may limit the adoption of these technologies, despite their long-term benefits in reducing costs and improving operational efficiency.

USA Medical Billing Outsourcing Market Future Outlook

Over the next five years, the USA Medical Billing Outsourcing Market is expected to exhibit significant growth, driven by the ongoing digital transformation in healthcare, rising adoption of cloud-based billing solutions, and increasing complexities in healthcare regulations. The demand for outsourcing services is likely to be bolstered by the shift toward value-based care models, compelling healthcare providers to optimize their billing processes and reduce administrative burdens.

Market Opportunities

- Growth in Adoption of Telehealth and Remote Billing: The adoption of telehealth services has accelerated, especially following the COVID-19 pandemic. This shift has created opportunities for medical billing outsourcing firms to offer specialized services for remote billing and coding. As telehealth becomes a mainstay in healthcare delivery, there is a rising demand for billing services that can handle the unique coding and reimbursement challenges associated with virtual care.

- Expansion of Services to Small and Medium Practices: Smaller healthcare practices often struggle with maintaining in-house billing teams due to financial constraints and lack of expertise. The market is seeing an increase in outsourcing services tailored to these smaller practices, allowing them to access specialized billing services without the high overhead costs. This expansion is supported by the increased focus on efficiency and cost reduction in the healthcare sector.

Scope of the Report

|

Component |

In-house Outsourced |

|

Service |

Front-End Services Middle-End Services Back-End Services |

|

End-User |

Hospitals Physician Offices Independent Practices |

|

Service Provider |

Small and Medium Enterprises (SMEs) Large Enterprises |

|

Region |

Northeast Midwest South West |

Products

Key Target Audience

Healthcare Providers (Hospitals, Clinics, Independent Practices)

Healthcare IT Vendors

Healthcare Insurance Companies

Medical Billing Service Providers

Government and Regulatory Bodies (Department of Health and Human Services, Centers for Medicare & Medicaid Services)

Venture Capital and Investment Firms

Health Information Management (HIM) Companies

Healthcare Consulting and Advisory Firms

Companies

Players Mentioned in the Report

R1RCM Inc.

Veradigm LLC (Allscripts Healthcare)

Oracle (Cerner Corporation)

eClinicalWorks

Kareo, Inc.

McKesson Corporation

Quest Diagnostics Incorporated

Promantra Inc.

AdvancedMD, Inc.

Experian Health

Table of Contents

1. USA Medical Billing Outsourcing Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. USA Medical Billing Outsourcing Market Size (In USD Billion)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. USA Medical Billing Outsourcing Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Emphasis on Compliance and Risk Management

3.1.2. Technological Integration in Revenue Cycle Management (RCM)

3.1.3. Cost Containment Strategies

3.2. Market Challenges

3.2.1. Data Breaches and Privacy Issues

3.2.2. High Costs of Technology Adoption

3.2.3. Legislative and Regulatory Pressure

3.3. Opportunities

3.3.1. Growth in Adoption of Telehealth and Remote Billing

3.3.2. Expansion of Services to Small and Medium Practices

3.3.3. Mergers and Acquisitions to Broaden Market Reach

3.4. Trends

3.4.1. Automation in Coding and Claims Management

3.4.2. Emergence of Artificial Intelligence in Claims Denial Management

3.4.3. Shift Towards End-to-End Revenue Cycle Solutions

3.5. Government Regulation

3.5.1. Affordable Care Act Impact

3.5.2. Impact of the No Surprises Act

3.5.3. Medicare and Medicaid Compliance Requirements

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem Analysis

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. USA Medical Billing Outsourcing Market Segmentation

4.1. By Component (In Value %)

4.1.1. In-house

4.1.2. Outsourced

4.2. By Service (In Value %)

4.2.1. Front-End Services

4.2.2. Middle-End Services

4.2.3. Back-End Services

4.3. By End-User (In Value %)

4.3.1. Hospitals

4.3.2. Physician Offices

4.3.3. Independent Practices

4.4. By Service Provider (In Value %)

4.4.1. Small and Medium Enterprises (SMEs)

4.4.2. Large Enterprises

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

5. USA Medical Billing Outsourcing Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. R1RCM Inc.

5.1.2. Veradigm LLC (Allscripts Healthcare)

5.1.3. Oracle (Cerner Corporation)

5.1.4. eClinicalWorks

5.1.5. Kareo, Inc.

5.1.6. McKesson Corporation

5.1.7. Quest Diagnostics

5.1.8. Promantra Inc.

5.1.9. AdvancedMD, Inc.

5.1.10. Experian Health

5.1.11. Athenahealth, Inc.

5.1.12. Conduent Incorporated

5.1.13. Genpact

5.1.14. GE Healthcare

5.1.15. The SSI Group

5.2. Cross Comparison Parameters (Number of Employees, Headquarters, Inception Year, Revenue, Client Base, Service Offerings, Technology Platform, Compliance Certifications)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. USA Medical Billing Outsourcing Market Regulatory Framework

6.1. Affordable Care Act (ACA)

6.2. HIPAA Compliance

6.3. Medicare and Medicaid Regulations

6.4. Regulatory Compliance for Revenue Cycle Management

7. USA Medical Billing Outsourcing Market Future Size (In USD Billion)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Medical Billing Outsourcing Market Future Segmentation

8.1. By Component (In Value %)

8.2. By Service (In Value %)

8.3. By End-User (In Value %)

8.4. By Service Provider (In Value %)

8.5. By Region (In Value %)

9. USA Medical Billing Outsourcing Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the USA Medical Billing Outsourcing Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compiled and analyzed historical data pertaining to the USA Medical Billing Outsourcing Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and resultant revenue generation. Furthermore, an evaluation of service quality statistics was conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provided valuable operational and financial insights directly from industry practitioners, which were instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involved direct engagement with multiple medical billing service providers to acquire detailed insights into service segments, sales performance, client satisfaction, and other pertinent factors. This interaction served to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the USA Medical Billing Outsourcing Market.

Frequently Asked Questions

01. How big is the USA Medical Billing Outsourcing Market?

The USA Medical Billing Outsourcing Market is valued at USD 5.6 billion, based on a five-year historical analysis. This market is primarily driven by the increasing complexities of healthcare regulations, such as HIPAA compliance, and the rising adoption of revenue cycle management (RCM) solutions across healthcare providers.

02. What are the growth drivers of the USA Medical Billing Outsourcing Market?

Growth drivers include the rising complexity of healthcare regulations, increased adoption of digital billing platforms, and the need for healthcare providers to reduce costs and improve operational efficiency.

03. Who are the major players in the USA Medical Billing Outsourcing Market?

Key players include R1RCM Inc., Veradigm LLC, Oracle (Cerner Corporation), eClinicalWorks, and McKesson Corporation, dominating due to their comprehensive service offerings and technological expertise.

04. What are the challenges in the USA Medical Billing Outsourcing Market?

Challenges include data breaches and privacy concerns, high implementation costs of advanced IT solutions, and evolving legislative regulations affecting revenue cycle management.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.