USA Organic Food Market Outlook to 2030

Region:United States

Author(s):Samanyu

Product Code:KROD4483

Region:United States

Author(s):Samanyu

Product Code:KROD4483

November 2024

81

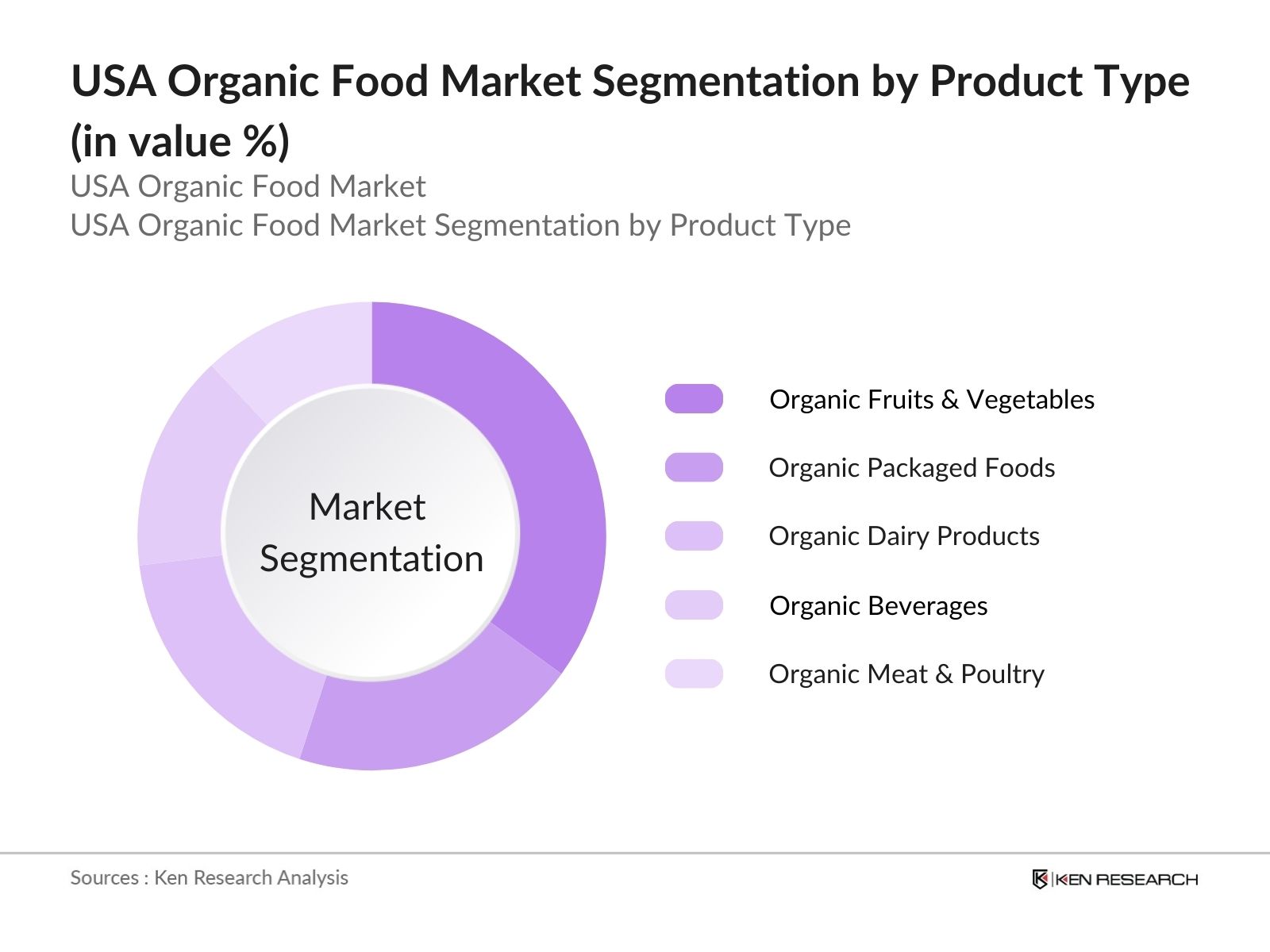

By Product Type: The market is segmented by product type into organic fruits & vegetables, organic dairy products, organic packaged foods, organic meat & poultry, and organic beverages. Recently, organic fruits & vegetables have maintained a dominant market share in the USA due to their perceived health benefits and a surge in demand for fresh, non-GMO produce. Consumers prefer organic produce for its lack of pesticides and chemicals, particularly following increased public awareness campaigns around food safety and sustainability.

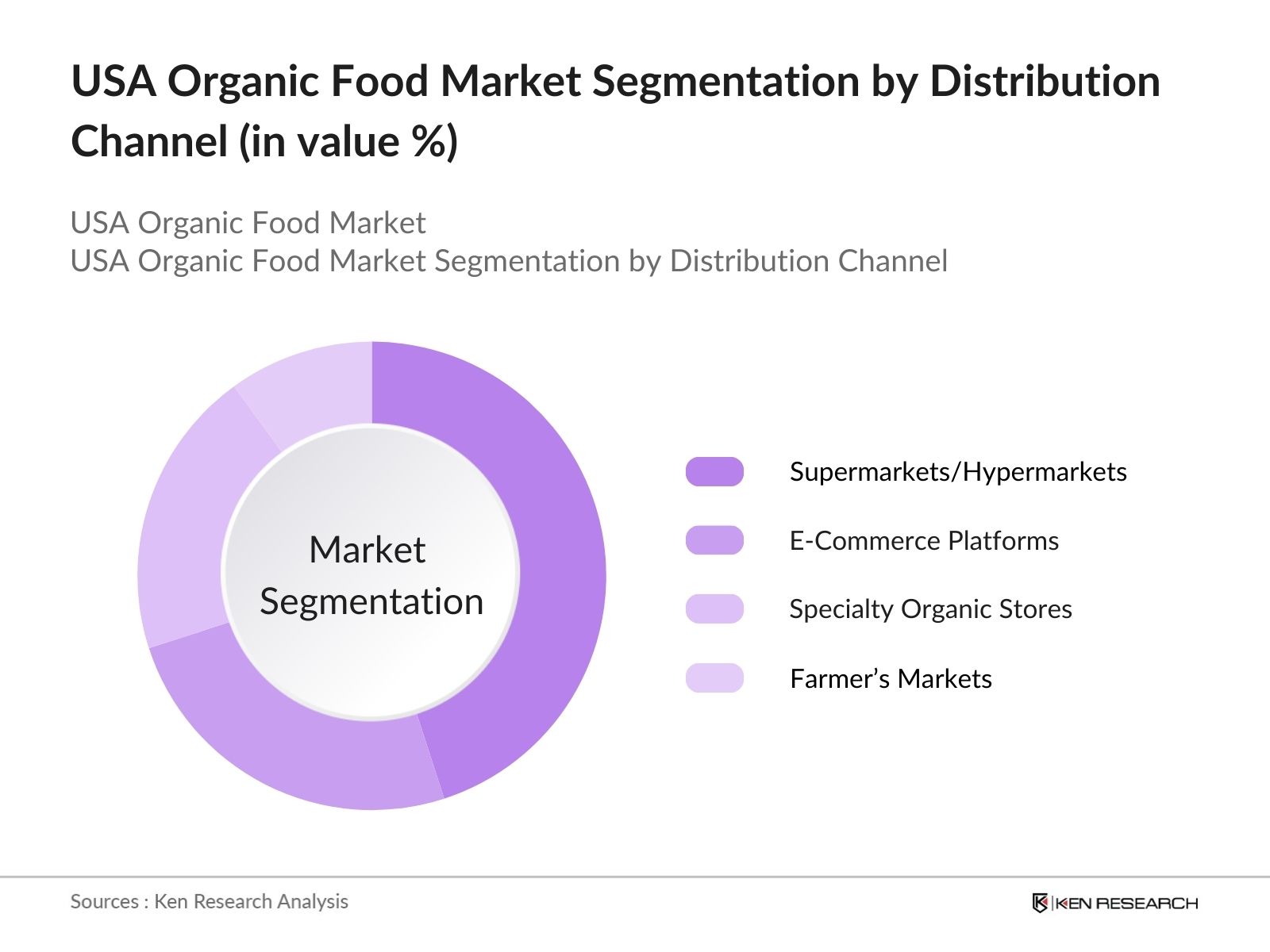

By Distribution Channel: The market is segmented by distribution channel into supermarkets/hypermarkets, specialty organic stores, e-commerce platforms, and farmers markets. Supermarkets and hypermarkets are the most dominant in this category, as they provide consumers with convenient access to a wide variety of organic products. These retailers often engage in promotional activities and offer discounts on organic products, contributing to their widespread reach among urban and suburban consumers.

The USA organic food market is dominated by a mixture of established multinational corporations and key domestic players. The competitive landscape highlights the consolidation of the market, where companies are continuously expanding their product portfolios and leveraging sustainability trends to gain a competitive edge. Major players are also focusing on strategic mergers and acquisitions to increase market presence.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (2023) |

Employees |

Product Portfolio |

R&D Investment |

Global Presence |

Distribution Network |

|

General Mills Inc. |

1928 |

Minneapolis, Minnesota |

||||||

|

Hain Celestial Group |

1993 |

Lake Success, New York |

||||||

|

Organic Valley |

1988 |

La Farge, Wisconsin |

||||||

|

WhiteWave Foods |

1977 |

Broomfield, Colorado |

||||||

|

Amy's Kitchen |

1987 |

Petaluma, California |

Over the next five years, the USA organic food market is expected to experience robust growth driven by rising consumer preference for natural and chemical-free products, as well as advancements in organic farming techniques. Increasing government support through subsidies for organic farming and new USDA certification programs will likely contribute to market expansion. Furthermore, consumer demand for transparency in food sourcing and ethical practices, such as fair-trade and non-GMO certifications, is expected to play a pivotal role in market dynamics.

|

By Product Type |

Organic Fruits & Vegetables Organic Dairy Organic Packaged Foods Organic Meat & Poultry Organic Beverages |

|

By Distribution Channel |

Supermarkets/Hypermarkets Specialty Stores E-Commerce Farmers Markets |

|

By Consumer Segment |

Health-Conscious Consumers Ethical Consumers Millennials/Gen Z Premium Buyers |

|

By Certification Type |

USDA Organic Non-GMO Verified Fair Trade Kosher/Halal Certified |

|

By Region |

Northeast Midwest South West Pacific Northwest |

1.1. Definition and Scope (Market Definition, Scope, Certification Standards)

1.2. Market Taxonomy (Organic Food Types, Market Distribution Channels, Certification Categories)

1.3. Market Growth Rate (Volume, Value Growth, Market Penetration)

1.4. Market Segmentation Overview (Product Types, Distribution Channels, Consumer Segments)

2.1. Historical Market Size (Market Size in USD, Growth Rate, Volume of Organic Sales)

2.2. Year-On-Year Growth Analysis (Annual Growth, Market Acceleration Factors)

2.3. Key Market Developments and Milestones (New Certifications, Policy Changes, New Entrants)

3.1. Growth Drivers (Consumer Demand, Health Awareness, Regulatory Push, Technological Advancements)

3.1.1. Consumer Preference Shift Towards Organic Products

3.1.2. Health-Conscious Consumer Demographics

3.1.3. Federal and State-Level Organic Regulations (USDA Organic Program)

3.1.4. Technological Innovations in Organic Farming

3.2. Restraints (High Price Points, Supply Chain Challenges, Organic Product Availability)

3.2.1. Premium Pricing and Cost Structure

3.2.2. Limited Organic Supply Chain Networks

3.2.3. Certification and Compliance Costs

3.3. Opportunities (E-commerce Expansion, Export Markets, Organic Private Labels)

3.3.1. Growth in Organic E-Commerce Platforms

3.3.2. Increasing Demand from Export Markets

3.3.3. Introduction of Private Labels in Organic Food

3.4. Trends (Sustainability Movements, Organic Convenience Foods, Locally Sourced Organic)

3.4.1. Growth in Sustainability and Regenerative Agriculture

3.4.2. Emergence of Organic Ready-to-Eat Foods

3.4.3. Locally Sourced Organic Products

3.5. Government Regulations (USDA Organic Guidelines, Non-GMO Standards, Organic Trade Agreements)

3.5.1. USDA National Organic Program (NOP) Compliance

3.5.2. Organic Import Compliance Regulations

3.5.3. Organic Food Labeling Standards

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Farmers, Distributors, Retailers, Consumers)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Organic Fruits & Vegetables

4.1.2. Organic Dairy Products

4.1.3. Organic Packaged Foods

4.1.4. Organic Meat & Poultry

4.1.5. Organic Beverages

4.2. By Distribution Channel (In Value %)

4.2.1. Supermarkets/Hypermarkets

4.2.2. Specialty Organic Stores

4.2.3. E-Commerce

4.2.4. Farmers Markets

4.3. By Consumer Segment (In Value %)

4.3.1. Health-Conscious Consumers

4.3.2. Ethical Consumers (Sustainability-Oriented)

4.3.3. Millennial and Gen Z Consumers

4.3.4. Premium Product Buyers

4.4. By Certification Type (In Value %)

4.4.1. USDA Certified Organic

4.4.2. Non-GMO Verified

4.4.3. Fair Trade Certified

4.4.4. Organic Kosher and Halal Certified

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

4.5.5. Pacific Northwest

5.1. Detailed Profiles of Major Companies

5.1.1. General Mills Inc.

5.1.2. Hain Celestial Group

5.1.3. Organic Valley

5.1.4. WhiteWave Foods

5.1.5. Earthbound Farm

5.1.6. Amy's Kitchen

5.1.7. Stonyfield Organic

5.1.8. SunOpta Inc.

5.1.9. Eden Foods Inc.

5.1.10. Whole Foods Market

5.1.11. Sprouts Farmers Market

5.1.12. United Natural Foods Inc. (UNFI)

5.1.13. Clif Bar & Company

5.1.14. Nature's Path Foods

5.1.15. Natural Grocers

5.2. Cross Comparison Parameters (Product Line, Revenue, Organic Certifications, Market Penetration, Distribution Reach, Supply Chain Integration)

5.3. Market Share Analysis

5.4. Strategic Initiatives (New Product Launches, Marketing Campaigns, Sustainability Commitments)

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Private Equity, Venture Capital, Strategic Investments)

5.7. Government Subsidies

5.8. Organic Farming Grants and Incentives

6.1. USDA National Organic Program

6.2. Organic Certification and Compliance Standards

6.3. Labeling Regulations

6.4. International Organic Trade Agreements

7.1. Market Projections and Future Growth Drivers

7.2. Key Factors Shaping Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By Consumer Segment (In Value %)

8.4. By Certification Type (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives for Organic Brands

9.4. White Space Opportunity Analysis

Disclaimer Contact Us

In this step, we map the entire ecosystem of the USA organic food market, including farmers, distributors, retailers, and consumers. The primary focus is on identifying the critical factors that influence market dynamics, such as pricing, distribution channels, and regulatory influences. This is done using a mix of primary and secondary research data.

This stage involves analyzing historical data on organic food production, consumer trends, and retailer data to establish market size and growth trends. Additional parameters, such as revenue from organic certification programs and market penetration rates, are considered to refine our understanding of the market structure.

Market assumptions are validated by engaging with key stakeholders, including organic food manufacturers and industry experts, through interviews and surveys. This provides insights into operational challenges and opportunities within the organic food sector, refining the final market estimates.

Finally, data from primary and secondary sources are synthesized to provide a validated overview of the USA organic food market. In this stage, detailed segment-level analysis is conducted to ensure accuracy and thoroughness of the report, culminating in a comprehensive market assessment.

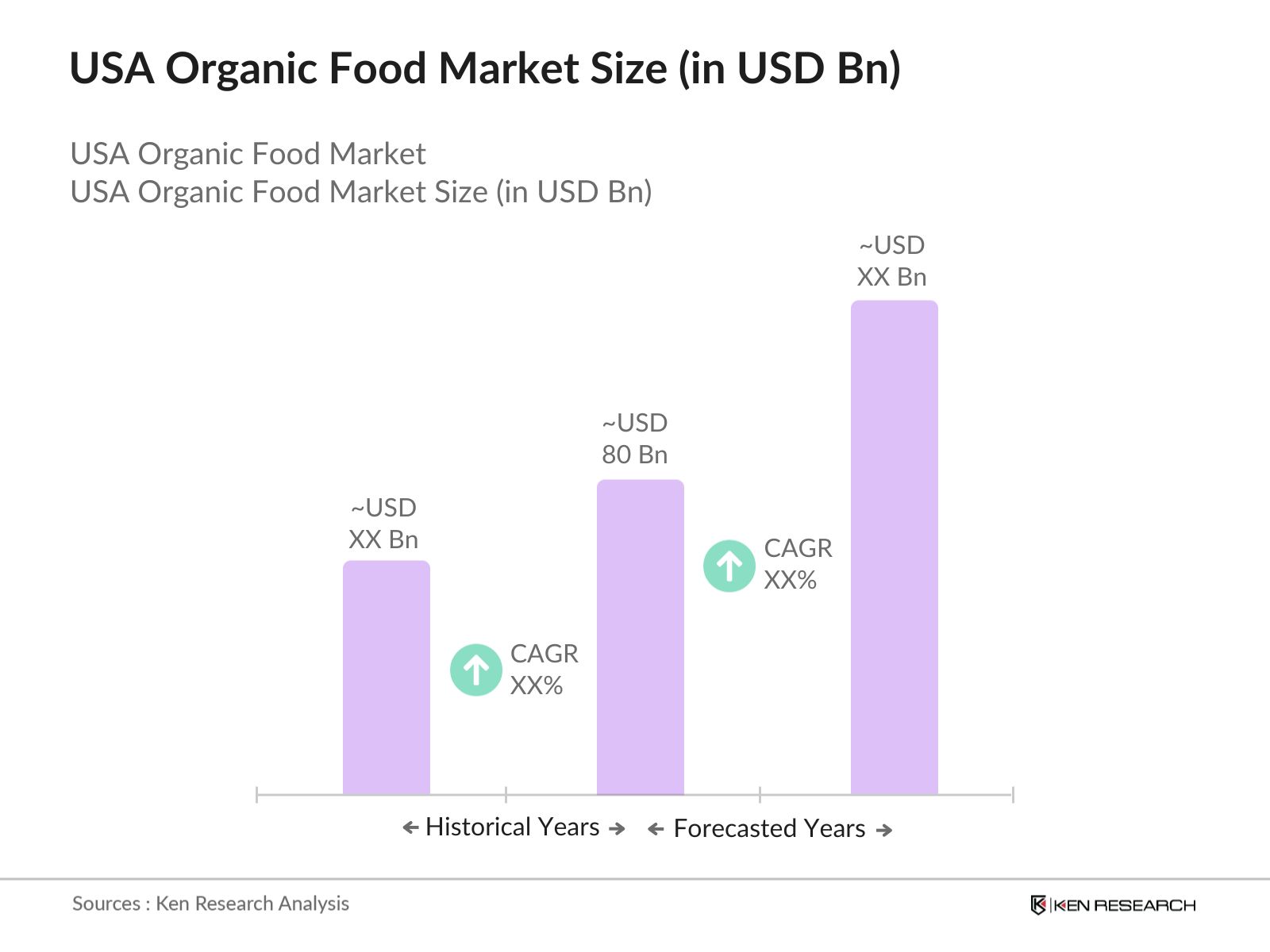

The USA organic food market is valued at USD 80 billion and is driven by increasing consumer demand for health-conscious, chemical-free, and non-GMO food products.

Key challenges in USA organic food market include the high price points of organic products, supply chain inefficiencies, and the rising cost of organic farming inputs, which make scalability a significant issue for smaller producers.

Major players in USA organic food market include General Mills, Hain Celestial Group, Organic Valley, WhiteWave Foods, and Amy's Kitchen, all of which dominate the market through extensive product offerings and strategic acquisitions.

The growth in USA organic food market is driven by consumer awareness of food safety, demand for non-GMO products, and government support through USDA organic certification programs, which incentivize farmers and producers to convert to organic farming practices.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.