USA Orthopedic Devices Industry Outlook to 2030

Region:North America

Author(s):Sanjeev

Product Code:KROD2684

November 2024

87

About the Report

USA Orthopedic Devices Market Overview

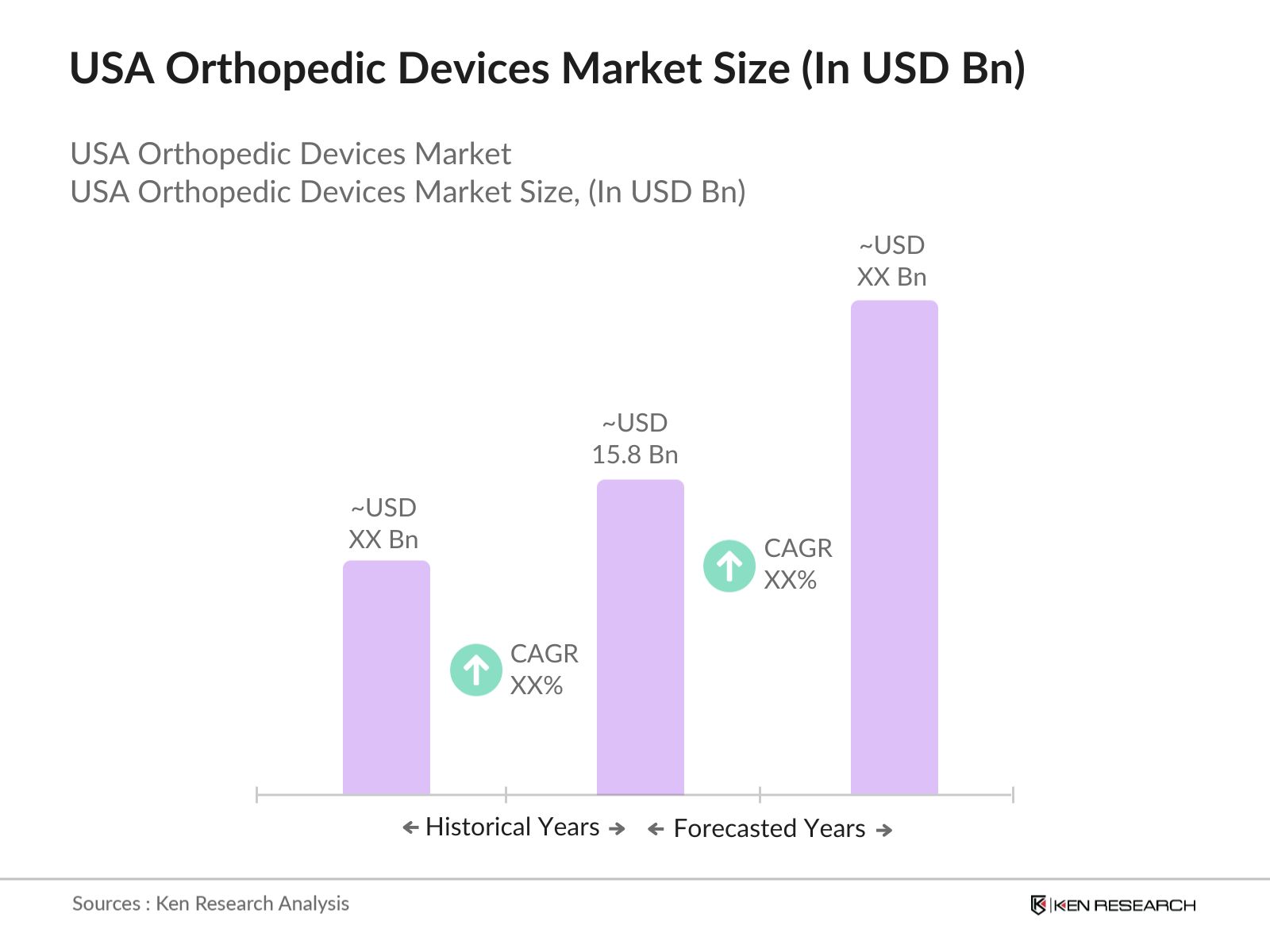

- The USA Orthopedic Devices Market is valued at USD 15.08 billion, driven by the increasing prevalence of orthopedic disorders and advancements in surgical technology. The market growth is supported by a rise in the aging population, a growing emphasis on minimally invasive procedures, and the integration of advanced materials in orthopedic devices. Additionally, investments in healthcare infrastructure and innovative product development by key players further stimulate the market. Sources such as the American Academy of Orthopaedic Surgeons (AAOS) highlight the critical role of these factors in expanding the orthopedic device sector.

- Major cities such as New York, Los Angeles, and Chicago dominate the USA Orthopedic Devices Market due to their robust healthcare ecosystems, which include leading hospitals and research institutions specializing in orthopedic care. New York serves as a hub for medical innovations and access to cutting-edge treatments, while California's vast population and high healthcare expenditure contribute to demand. Chicago's strong presence of orthopedic specialists and surgical centers further enhances its market dominance. According to sources like the Centers for Disease Control and Prevention (CDC), these cities are pivotal in advancing orthopedic healthcare initiatives.

- The FDA plays a crucial role in ensuring the safety and efficacy of orthopedic devices. As of 2024, the agency has introduced stricter guidelines for device approval, with a focus on post-market surveillance. This regulatory framework is essential for maintaining high safety standards and instilling confidence among healthcare providers and patients in the use of orthopedic devices.

USA Orthopedic Devices Market Segmentation

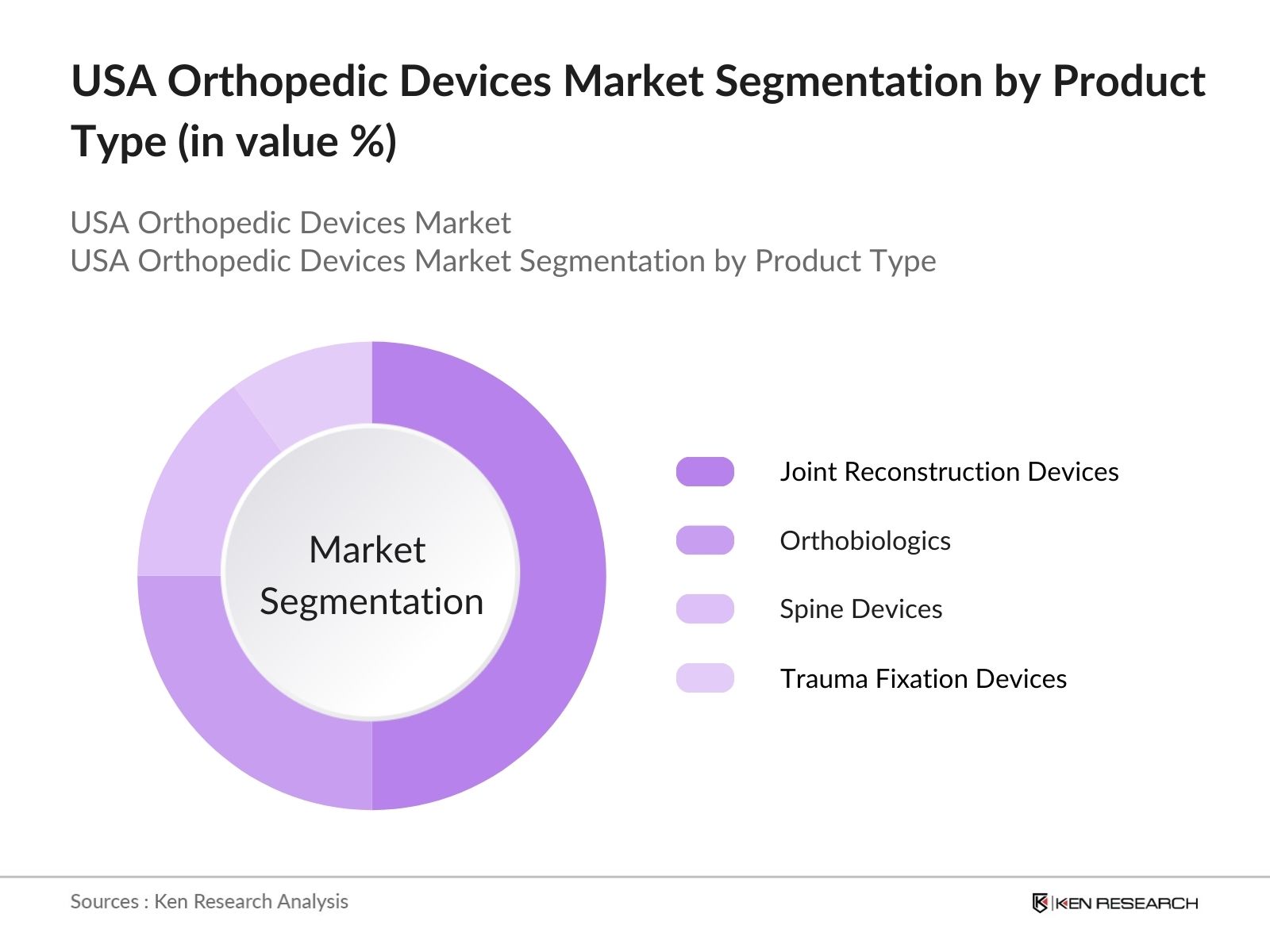

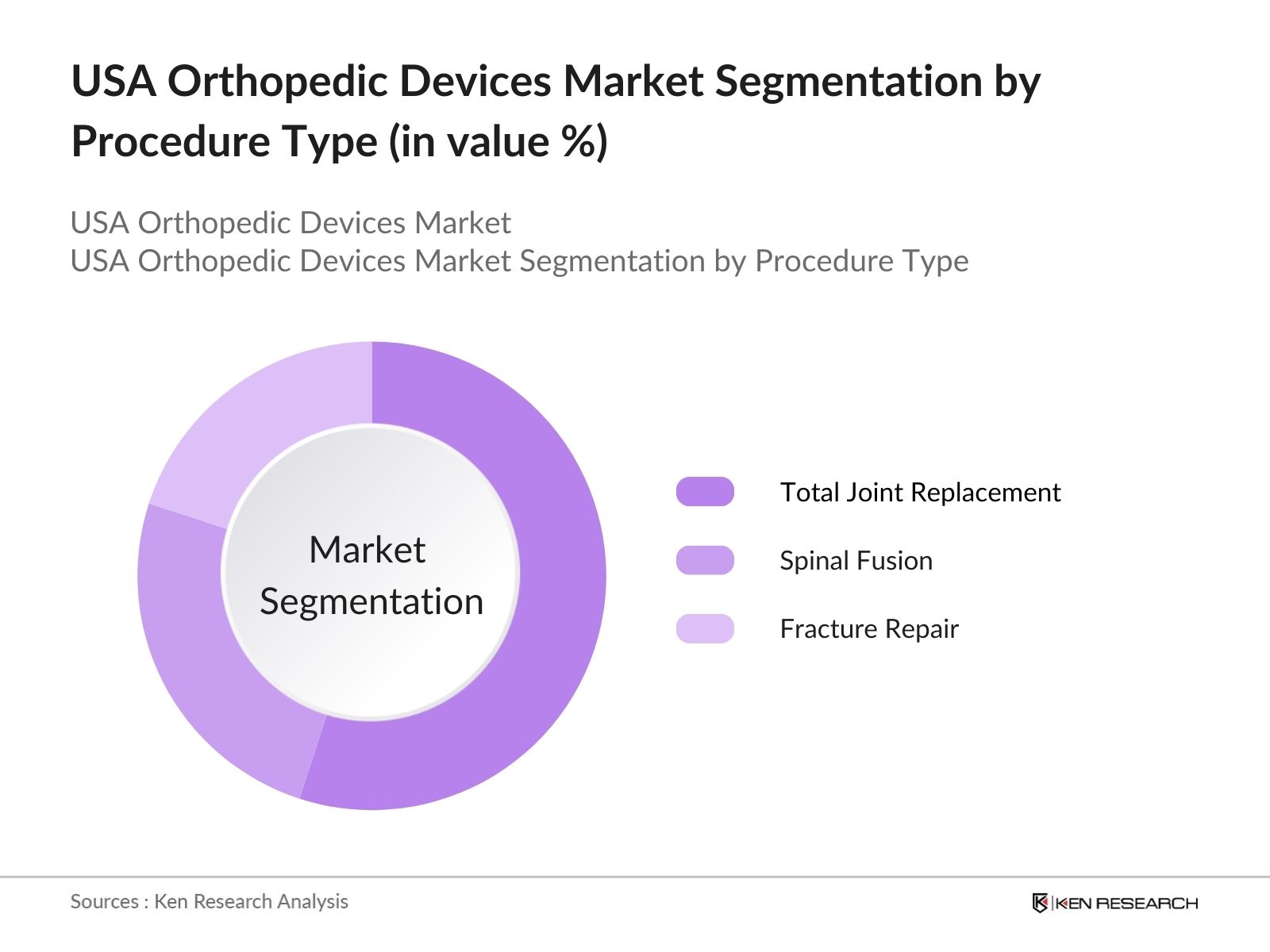

The USA Orthopedic Devices Market can be segmented into product and procedure.

- By Product Type: The market is segmented by product type into joint reconstruction devices, orthobiologics, spine devices, and trauma fixation devices. Currently, joint reconstruction devices hold a dominant market share due to the rising number of knee and hip replacement surgeries driven by an aging population. The increasing prevalence of osteoarthritis and other joint-related conditions necessitates these procedures, resulting in a high demand for advanced joint reconstruction solutions. Companies such as Zimmer Biomet and Stryker are continuously innovating in this area, further solidifying the market position of joint reconstruction devices.

- By Procedure Type: The market is also segmented by procedure type, which includes total joint replacement, spinal fusion, and fracture repair. Total joint replacement is the leading procedure type, largely attributed to the increasing number of elective surgeries aimed at improving mobility and quality of life for patients. The growing incidence of joint disorders among the elderly population emphasizes the need for effective surgical interventions. This segments dominance is supported by advancements in surgical techniques and materials, ensuring better outcomes for patients.

USA Orthopedic Devices Competitive Landscape

The USA Orthopedic Devices Market is highly competitive, with key players focusing on technological advancements, strategic collaborations, and expanding their product portfolios. Dominant companies such as Johnson & Johnson, Medtronic, and Stryker benefit from their strong brand presence and extensive distribution networks, which enhance their market influence.

|

Company |

Establishment Year |

Headquarters |

Number of Employees |

Revenue (USD Bn) |

Market Focus |

R&D Investment (USD Mn) |

|

Johnson & Johnson |

1886 |

New Brunswick, NJ |

||||

|

Medtronic |

1949 |

Minneapolis, MN |

||||

|

Stryker Corporation |

1941 |

Kalamazoo, MI |

||||

|

Zimmer Biomet |

1927 |

Warsaw, IN |

||||

|

Smith & Nephew |

1856 |

London, UK |

USA Orthopedic Devices Industry Analysis

Growth Drivers

- Increasing Incidence of Orthopedic Disorders: The prevalence of orthopedic disorders has been rising significantly, driven by factors such as increased physical activity and aging. In the U.S., approximately 50 million adults are affected by arthritis alone, a primary contributor to orthopedic issues. The World Health Organization reported that musculoskeletal disorders are expected to increase by 25% by 2025, necessitating advanced orthopedic interventions. This trend highlights the urgent demand for orthopedic devices to manage these conditions effectively.

- Advancements in Technology: Technological innovations in orthopedic devices are transforming treatment methodologies. For instance, advancements in robotics and artificial intelligence are enhancing surgical precision. According to the National Institutes of Health, the integration of technology has led to a 30% increase in surgical success rates from 2022 to 2024. Furthermore, smart implants equipped with sensors are providing real-time data to healthcare providers, improving patient outcomes significantly.

Market Challenges

- High Cost of Devices: The high cost of orthopedic devices poses a significant challenge to market growth. The expense associated with orthopedic implants limits access for many patients, creating financial burdens related to orthopedic surgeries. This situation necessitates innovative pricing strategies to enhance accessibility and ensure that more patients can receive the necessary treatments.

- Stringent Regulatory Approvals: Navigating the regulatory landscape for orthopedic devices can be daunting due to stringent FDA approval processes. The time required for device approval can lead to delays in market entry and innovation. Many new orthopedic devices face regulatory challenges, hindering the rapid introduction of new technologies to the market and impacting the overall growth of the industry.

USA Orthopedic Devices Market Future Outlook

Over the next five years, the USA Orthopedic Devices Market is expected to exhibit substantial growth, driven by continuous advancements in orthopedic technology and a rising demand for effective surgical solutions. The integration of artificial intelligence (AI) and robotics in orthopedic surgeries is anticipated to enhance surgical precision and recovery times. Additionally, the growing emphasis on preventive healthcare and lifestyle management will contribute to the markets expansion.

Future Market Opportunities

- Technological Advancements in Orthopedic Devices: Innovations such as 3D printing and personalized implants are transforming the landscape of orthopedic surgeries. By the end of 2024, the utilization of 3D printing technology in manufacturing orthopedic devices is projected to increase significantly, leading to customized solutions that meet specific patient needs.

- Collaboration between Healthcare Providers and Technology Firms: The collaboration between healthcare providers and technology companies is expected to enhance the development of advanced orthopedic solutions. Initiatives like the integration of telemedicine and digital health platforms are paving the way for improved patient monitoring and post-operative care, ensuring better outcomes.

Scope of the Report

|

By Product Type |

Joint Reconstruction Devices Orthobiologics Spine Devices Trauma Fixation Devices |

|

By Procedure Type |

Total Joint Replacement Spinal Fusion Fracture Repair |

|

By Region |

North East West South |

|

By End-User |

Hospitals Ambulatory Surgical Centers Rehabilitation Centers |

Products

Key Target Audience

Government and Regulatory Bodies (FDA, CMS)

Healthcare Firms

Hospitals and Surgical Centers

Orthopedic Surgeons

Medical Device Distributors

Rehabilitation Centers

Investments and Venture Capitalist Firms

Banks and Financial Institue

Insurance Companies

Companies

List of Major Players in the USA Orthopedic Devices Market

Johnson & Johnson

Medtronic

Stryker Corporation

Zimmer Biomet

Smith & Nephew

DePuy Synthes

NuVasive

Amedica Corporation

Orthofix Medical

Conmed Corporation

Wright Medical Group

Globus Medical

SeaSpine Holdings Corporation

Aesculap Implant Systems

Arthrex

Table of Contents

1. USA Orthopedic Devices Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics

1.4. Market Segmentation Overview

2. USA Orthopedic Devices Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. USA Orthopedic Devices Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Incidence of Orthopedic Disorders

3.1.2. Advancements in Technology

3.1.3. Aging Population

3.1.4. Rising Demand for Minimally Invasive Procedures

3.2. Market Challenges

3.2.1. High Cost of Devices

3.2.2. Stringent Regulatory Approvals

3.2.3. Limited Reimbursement Policies

3.3. Opportunities

3.3.1. Emerging Markets

3.3.2. Technological Innovations

3.3.3. Strategic Collaborations

3.4. Trends

3.4.1. Growth of 3D Printing Technology

3.4.2. Telemedicine in Orthopedic Care

3.4.3. Personalized Medicine

3.5. Government Regulation

3.5.1. FDA Regulations

3.5.2. Product Safety Standards

3.5.3. Compliance Guidelines

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. USA Orthopedic Devices Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Joint Reconstruction Devices

4.1.2. Orthobiologics

4.1.3. Spine Devices

4.1.4. Trauma Fixation Devices

4.1.5. Others

4.2. By Procedure Type (In Value %)

4.2.1. Total Joint Replacement

4.2.2. Spinal Fusion

4.2.3. Fracture Repair

4.3. By End-User (In Value %)

4.3.1. Hospitals

4.3.2. Ambulatory Surgical Centers

4.3.3. Rehabilitation Centers

4.4. By Region (In Value %)

4.4.1. North

4.4.2. East

4.4.3. South

4.4.4. West

5. USA Orthopedic Devices Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Johnson & Johnson

5.1.2. Medtronic

5.1.3. Stryker Corporation

5.1.4. Zimmer Biomet

5.1.5. Smith & Nephew

5.1.6. DePuy Synthes

5.1.7. NuVasive

5.1.8. Amedica Corporation

5.1.9. Orthofix Medical

5.1.10. Conmed Corporation

5.1.11. Wright Medical Group

5.1.12. Globus Medical

5.1.13. SeaSpine Holdings Corporation

5.1.14. Aesculap Implant Systems

5.1.15. Arthrex

5.2. Cross Comparison Parameters (Market Share, Revenue, Geographic Presence, Product Portfolio, R&D Investment, Key Partnerships, Manufacturing Capabilities, Innovation Rate)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants

5.8. Private Equity Investments

6. USA Orthopedic Devices Market Regulatory Framework

6.1. FDA Guidelines

6.2. Quality Management Systems

6.3. Post-Market Surveillance

7. USA Orthopedic Devices Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Orthopedic Devices Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Procedure Type (In Value %)

8.3. By End-User (In Value %)

8.4. By Region (In Value %)

9. USA Orthopedic Devices Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The research begins with identifying key variables that influence the USA Orthopedic Devices Market, such as technological advancements, regulatory requirements, and consumer trends. Extensive desk research, coupled with analysis of government and industry reports, is conducted to map these variables.

Step 2: Market Analysis and Construction

In this step, historical data is analyzed to evaluate the market's growth trajectory. Market penetration and the ratio of orthopedic devices to surgical procedures are assessed. Data from authoritative sources, including industry reports and academic journals, is used to ensure the accuracy of revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

To validate market assumptions, expert interviews are conducted with orthopedic device manufacturers, healthcare professionals, and regulatory officials. These consultations provide insights into operational challenges and market dynamics.

Step 4: Research Synthesis and Final Output

The final synthesis involves consolidating insights from multiple stakeholders, including industry experts and practitioners. This ensures that the final market analysis is accurate, comprehensive, and aligned with current trends in the USA Orthopedic Devices Market.

Frequently Asked Questions

01. How big is the USA Orthopedic Devices Market?

The USA Orthopedic Devices Market is valued at USD 15.8 billion, driven by advancements in surgical technology and the rising prevalence of orthopedic disorders.

02. What are the challenges in the USA Orthopedic Devices Market?

Key challenges include high implementation costs for new devices, stringent regulatory requirements, and competition among established players, which can hinder market growth.

03. Who are the major players in the USA Orthopedic Devices Market?

Major players include Johnson & Johnson, Medtronic, Stryker Corporation, and Zimmer Biomet, which dominate the market through innovation and extensive distribution networks.

04. What are the growth drivers of the USA Orthopedic Devices Market?

The market is driven by the aging population, increasing incidence of joint disorders, and advancements in technology that enhance surgical outcomes.

05. Which product type dominates the USA Orthopedic Devices Market?

Joint reconstruction devices dominate the market, primarily due to the high demand for knee and hip replacement surgeries, driven by an aging population and increased physical activity.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.