USA Scrap Metal Recycling Market Outlook to 2030

Region:North America

Author(s):Vijay Kumar

Product Code:KROD7544

November 2024

96

About the Report

USA Scrap Metal Recycling Market Overview

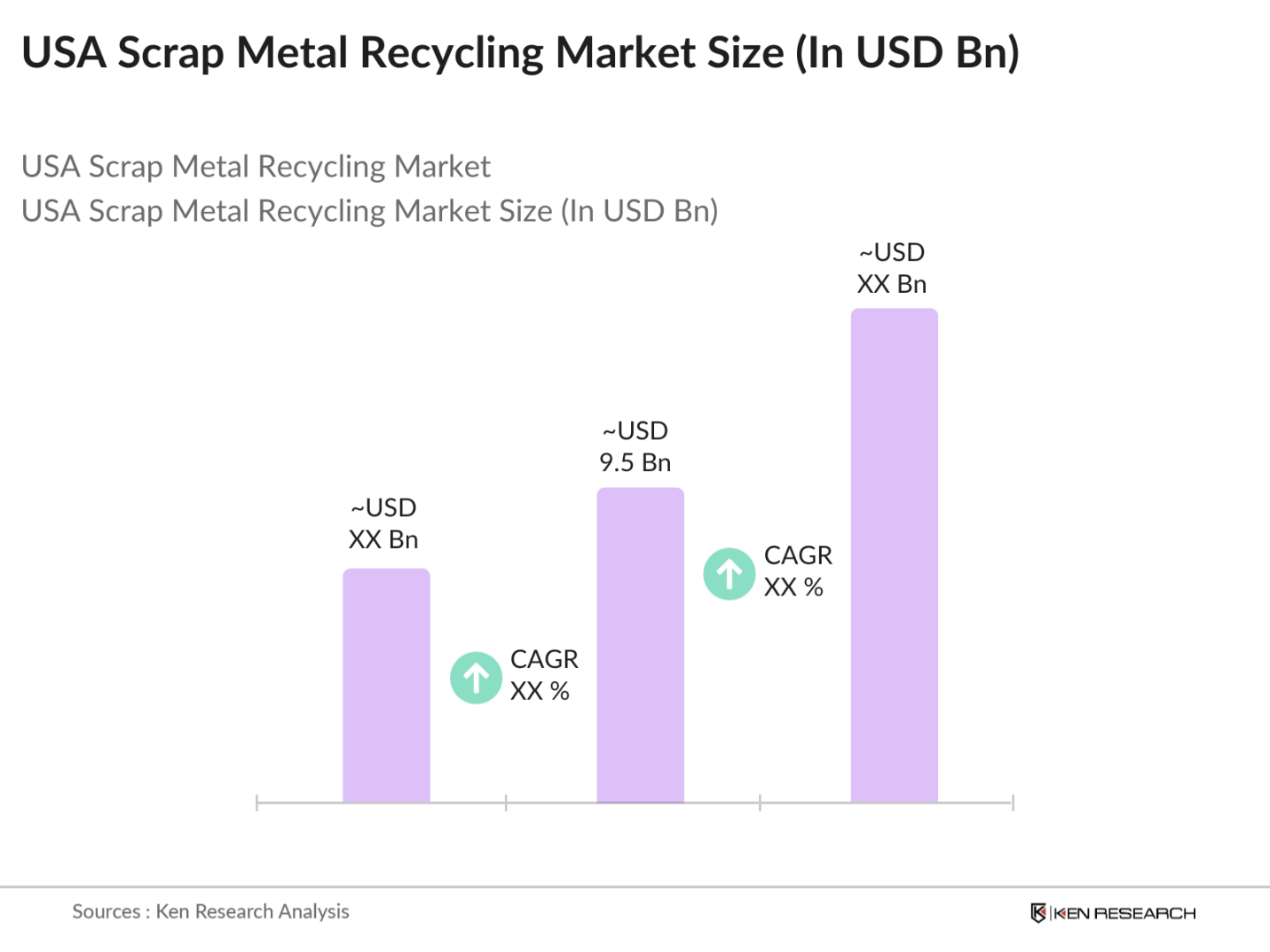

- The USA Scrap Metal Recycling market is valued at USD 9.5 billion, based on a five-year historical analysis. This market is primarily driven by the rising demand for sustainable raw materials across industries such as automotive, construction, and electronics, which increasingly prioritize cost-effective and eco-friendly materials. With the focus on environmental regulations and corporate sustainability initiatives, scrap metal recycling plays a crucial role in reducing waste and conserving natural resources. Advanced recycling technologies, including automation and AI-driven sorting systems, further enhance market efficiency and profitability, making recycled metals a preferred choice in industrial applications.

- The market is dominated by regions with significant industrial activities, such as California, Texas, and New York. These areas have large industrial bases and high population densities, generating substantial amounts of scrap metal. Additionally, their well-established recycling infrastructures, government support, and accessibility to global trade routes through major ports contribute to their dominance. These states serve as the primary hubs for scrap collection, sorting, and distribution across the USA.

- The U.S. scrap metal recycling industry is significantly affected by export regulations, including tariffs and duties on exported metals. In 2022, tariffs imposed on steel and aluminum under Section 232 of the Trade Expansion Act remained in effect, impacting the export of over 6 million tons of ferrous scrap. These regulations aim to protect domestic industries but have also created challenges for U.S. exporters. The U.S. Census Bureau reported that the value of exported scrap metal dropped by 15% in 2023 due to these trade barriers.

USA Scrap Metal Recycling Market Segmentation

By Type of Metal: The USA scrap metal recycling market is segmented by metal type into ferrous and non-ferrous metals. Ferrous metals, including steel and iron, dominate the market due to their extensive usage in key industries like construction and automotive manufacturing. Ferrous metals hold the majority share because of the ease of recycling, high recovery rates, and strong demand from the steelmaking industry, which relies heavily on recycled steel to lower production costs and meet sustainability goals.

By Source: The USA Scrap Metal Recycling market is also segmented by source into industrial scrap, construction and demolition scrap, automotive scrap, and consumer goods scrap. Automotive scrap dominates this segment, driven by the growing volume of end-of-life vehicles (ELVs). The demand for recycled metal from ELVs has surged as manufacturers shift towards lightweight materials, such as aluminum and high-strength steel, to meet fuel efficiency and emission standards.

USA Scrap Metal Recycling Market Competitive Landscape

The USA scrap metal recycling market is highly competitive, with several major players driving innovation and operational efficiency. The competition is led by both regional and national recycling firms that have established their presence across the country. The USA scrap metal recycling market is consolidated with a few key players such as Schnitzer Steel Industries, Sims Metal Management, OmniSource Corporation, Nucor Corporation, and SA Recycling.

USA Scrap Metal Recycling Industry Analysis

Growth Drivers

- Rising Demand from the Construction Industry: The demand for scrap metal recycling in the USA is increasingly driven by the construction industry's need for sustainable materials. In 2023, the U.S. construction sector consumed approximately 106 million tons of raw materials, a substantial portion of which was sourced from recycled metals, as companies shifted toward more environmentally friendly practices. This trend is encouraged by government infrastructure initiatives, which promote the use of recycled materials.

- Increasing Government Regulations on Waste Management: Government regulations aimed at reducing landfill waste are pushing for higher rates of scrap metal recycling. The Resource Conservation and Recovery Act (RCRA) mandates stricter waste management policies, which directly affect how scrap metals are handled and recycled. In 2023, the U.S. Environmental Protection Agency (EPA) reported that metal recycling accounted for nearly 33% of the total municipal waste recycling efforts.

- Expansion of Circular Economy Practices: Circular economy principles, which promote recycling and reusing materials, are gaining traction in the U.S. scrap metal recycling market. The U.S. Department of Energy reported in 2023 that industries such as automotive and manufacturing reused 95 million tons of scrap metal to minimize waste and reduce energy consumption. These practices have received a significant boost from government incentives, such as the Infrastructure Investment and Jobs Act, which allocates $17 billion for sustainable infrastructure projects that integrate recycling solutions.

Market Challenges

- Fluctuating Scrap Metal Prices: Price volatility remains a major challenge for the scrap metal recycling market. In 2023, U.S. scrap steel prices fluctuated between $270 and $430 per ton due to global economic uncertainties, including trade restrictions and changing demand from key export markets. The Bureau of Labor Statistics highlighted how fluctuating raw material prices directly impact the profitability of recycling operations, as well as their ability to invest in new technologies.

- High Energy Costs: The scrap metal recycling process is energy-intensive, and rising energy prices have significantly impacted operational costs. In 2023, the U.S. Energy Information Administration (EIA) reported that industrial electricity rates increased to an average of 8.06 cents per kilowatt-hour, up from 7.3 cents in 2022. This rise in energy costs has forced many recycling facilities to seek more energy-efficient technologies or reduce production capacity to manage expenses, especially since energy accounts for nearly 20% of total operating costs in scrap metal recycling.

USA Scrap Metal Recycling Future Outlook

Over the next five years, the USA Scrap Metal Recycling market is poised for substantial growth, driven by a combination of environmental regulations, rising raw material costs, and the increasing adoption of green manufacturing practices. The demand for recycled metals is expected to surge as industries such as automotive, construction, and electronics seek sustainable alternatives to virgin materials.

Market Opportunities

- Growth in E-Waste Recycling: E-waste recycling presents a growing opportunity for the U.S. scrap metal market. In 2022, the U.S. generated approximately 6.92 million tons of e-waste, according to the United Nations University. With metals such as copper, aluminum, and gold being integral components of electronic waste, their recovery has become a priority for both environmental and economic reasons.

- Increased Adoption of Sustainable Manufacturing: Sustainable manufacturing practices are driving increased demand for recycled metals. In 2023, the U.S. Environmental Protection Agency highlighted that over 45 million tons of scrap metal were reused in manufacturing, especially in the automotive and electronics sectors. Companies are adopting recycled materials to meet sustainability goals and comply with government regulations that incentivize eco-friendly practices.

Scope of the Report

|

By Type of Metal |

Ferrous Metals Non-Ferrous Metals |

|

By Source |

Industrial Scrap Construction Scrap Automotive Scrap Consumer Goods Scrap |

|

By End-Use Industry |

Construction Automotive Manufacturing Electrical & Electronics Others |

|

By Recycling Process |

Collection Sorting Shredding Melting Final Product Manufacturing |

|

By Region |

Northeast Midwest South West |

Products

Key Target Audience

Steel Manufacturers

Automotive Manufacturers

Construction Firms

Government & Regulatory Bodies (EPA, DOE)

Waste Management Companies

Electric Arc Furnace Operators

Investments and Venture Capitalist Firms

End-of-Life Vehicle (ELV) Processors

Companies

Players Mentioned in the Report

Schnitzer Steel Industries

Sims Metal Management

OmniSource Corporation

Nucor Corporation

SA Recycling

PSC Metals

Alter Trading Corporation

Metalico Inc.

Ferrous Processing & Trading Company

Gerdau Ameristeel Corporation

Table of Contents

1. USA Scrap Metal Recycling Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. USA Scrap Metal Recycling Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. USA Scrap Metal Recycling Market Analysis

3.1. Growth Drivers

3.1.1. Rising Demand from the Construction Industry

3.1.2. Increasing Government Regulations on Waste Management

3.1.3. Expansion of Circular Economy Practices

3.1.4. Technological Advancements in Recycling Techniques

3.2. Market Challenges

3.2.1. Fluctuating Scrap Metal Prices

3.2.2. High Energy Costs

3.2.3. Lack of Infrastructure in Rural Areas

3.3. Opportunities

3.3.1. Growth in E-Waste Recycling

3.3.2. Increased Adoption of Sustainable Manufacturing

3.3.3. Strategic Public-Private Partnerships

3.4. Trends

3.4.1. Adoption of Automation and AI in Recycling

3.4.2. Increasing Focus on Closed-Loop Recycling Systems

3.4.3. Growing Role of Export Markets

3.5. Government Regulations

3.5.1. Scrap Metal Export Regulations (Including Tariffs and Duties)

3.5.2. Environmental Protection Agency (EPA) Guidelines

3.5.3. Tax Incentives for Recycling Facilities

3.5.4. End-of-Life Vehicle Recycling Standards

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.8.1. Bargaining Power of Suppliers

3.8.2. Bargaining Power of Buyers

3.8.3. Threat of New Entrants

3.8.4. Threat of Substitutes

3.8.5. Industry Rivalry

3.9. Competition Ecosystem

4. USA Scrap Metal Recycling Market Segmentation

4.1. By Metal Type (In Value %)

4.1.1. Ferrous Metals

4.1.2. Non-Ferrous Metals

4.1.3. E-Waste Metals

4.1.4. Precious Metals

4.1.5. Alloys

4.2. By Source (In Value %)

4.2.1. Construction & Demolition Waste

4.2.2. Industrial Scrap

4.2.3. End-of-Life Vehicles

4.2.4. Consumer Goods

4.2.5. Packaging Waste

4.3. By Processing Method (In Value %)

4.3.1. Shredding

4.3.2. Melting

4.3.3. Baling

4.3.4. Shearing

4.4. By Application (In Value %)

4.4.1. Building & Construction

4.4.2. Automotive

4.4.3. Electronics

4.4.4. Industrial Machinery

4.4.5. Packaging

4.5. By Region (In Value %)

4.5.1. North-East

4.5.2. Midwest

4.5.3. South

4.5.4. West

5. USA Scrap Metal Recycling Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Schnitzer Steel Industries

5.1.2. Commercial Metals Company

5.1.3. Nucor Corporation

5.1.4. Sims Metal Management

5.1.5. Steel Dynamics Inc.

5.1.6. Ferrous Processing & Trading Co.

5.1.7. SA Recycling

5.1.8. Alter Trading Corporation

5.1.9. Metalico Inc.

5.1.10. OmniSource Corporation

5.1.11. David J. Joseph Company

5.1.12. Triple M Metal

5.1.13. PSC Metals

5.1.14. Miller Compressing Company

5.1.15. American Iron & Metal (AIM)

5.2. Cross Comparison Parameters (Headquarters, Number of Recycling Plants, Annual Recycling Capacity, Revenue, Market Share, Number of Employees, Regional Presence, Key Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. USA Scrap Metal Recycling Market Regulatory Framework

6.1. Compliance with Federal and State Regulations

6.2. Scrap Metal Licensing and Permits

6.3. Environmental and Safety Standards

6.4. Certification Processes

7. USA Scrap Metal Recycling Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Scrap Metal Recycling Future Market Segmentation

8.1. By Metal Type (In Value %)

8.2. By Source (In Value %)

8.3. By Processing Method (In Value %)

8.4. By Application (In Value %)

8.5. By Region (In Value %)

9. USA Scrap Metal Recycling Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase focuses on mapping the entire ecosystem of the USA Scrap Metal Recycling Market, incorporating key stakeholders such as metal processors, manufacturers, and government agencies. Extensive desk research is conducted using secondary sources and proprietary databases to define critical variables affecting market dynamics.

Step 2: Market Analysis and Construction

In this step, historical data for the USA Scrap Metal Recycling market is analyzed, focusing on market size, revenue generation from different scrap sources, and scrap metal export volumes. This step is essential for constructing an accurate market model and identifying key trends in the industry.

Step 3: Hypothesis Validation and Expert Consultation

To validate the findings, expert consultations are conducted through computer-assisted telephone interviews (CATIs) with key market participants such as recycling facility operators and scrap metal processors. These discussions provide insights into operational challenges and future growth prospects.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing data from various sources, including direct feedback from industry experts, to provide a comprehensive, validated report. This ensures that all insights are aligned with real-world market dynamics and accurately reflect current and future trends.

Frequently Asked Questions

01. How big is the USA Scrap Metal Recycling Market?

The USA Scrap Metal Recycling market is valued at USD 9.5 billion, based on a five-year historical analysis. This market is primarily driven by the rising demand for sustainable raw materials across industries such as automotive, construction, and electronics, which increasingly prioritize cost-effective and eco-friendly materials.

02. What are the challenges in the USA Scrap Metal Recycling Market?

Key challenges include fluctuating scrap metal prices, outdated recycling technologies, and a fragmented scrap collection system that hampers operational efficiency in certain regions.

03. Who are the major players in the USA Scrap Metal Recycling Market?

The major players include Schnitzer Steel Industries, Sims Metal Management, OmniSource Corporation, Nucor Corporation, and SA Recycling, all of which dominate the market due to their extensive recycling infrastructures and advanced technological capabilities.

04. What are the growth drivers of the USA Scrap Metal Recycling Market?

Growth is driven by increasing demand for sustainable raw materials in manufacturing, government regulations mandating recycling, and technological advancements that enhance the recycling process's efficiency and profitability.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.