USA Self-Checkout System Market Outlook to 2030

Region:North America

Author(s):Naman Rohilla

Product Code:KROD6242

December 2024

99

About the Report

USA Self-Checkout System Market Overview

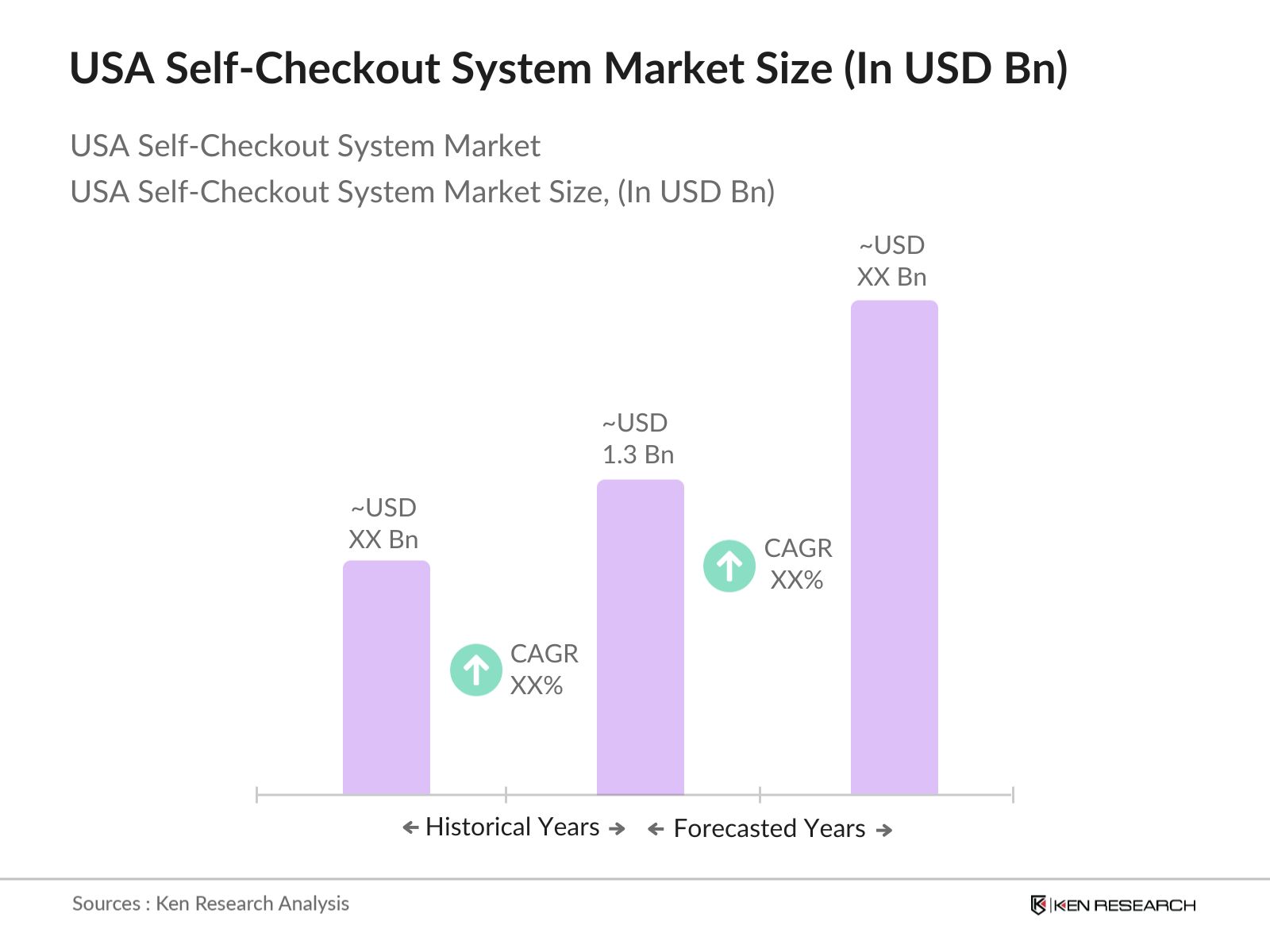

- The USA Self-Checkout System market is valued at USD 1.3 billion, based on a five-year historical analysis. This market is driven by increasing demand for efficient retail operations, a focus on reducing labor costs, and consumer preference for faster, contactless payment methods. The adoption of self-checkout technology has accelerated in recent years due to the retail industrys push for automation, coupled with changing consumer behaviour driven by the rise of e-commerce and cashless transactions.

- The dominant cities in this market include New York, Los Angeles, and Chicago, primarily due to their large retail footprints and highly developed infrastructure. Retail chains in these cities are more likely to adopt advanced self-checkout systems due to higher consumer traffic, the need for efficiency, and their role as early adopters of technology. Moreover, tech-driven retail giants like Walmart and Amazon have large operations in these cities, which boosts the demand for innovative checkout systems.

- Retailers deploying self-checkout systems must comply with stringent consumer protection laws. The U.S. Federal Trade Commission (FTC) has implemented policies to ensure that self-checkout systems are fair, transparent, and accessible to all consumers. As of 2024, retailers face fines for non-compliance, with penalties reaching up to $5,000 per violation. These regulations encourage retailers to provide clear instructions, accessible interfaces, and customer support to prevent unfair practices and improve the consumer experience.

USA Self-Checkout System Market Segmentation

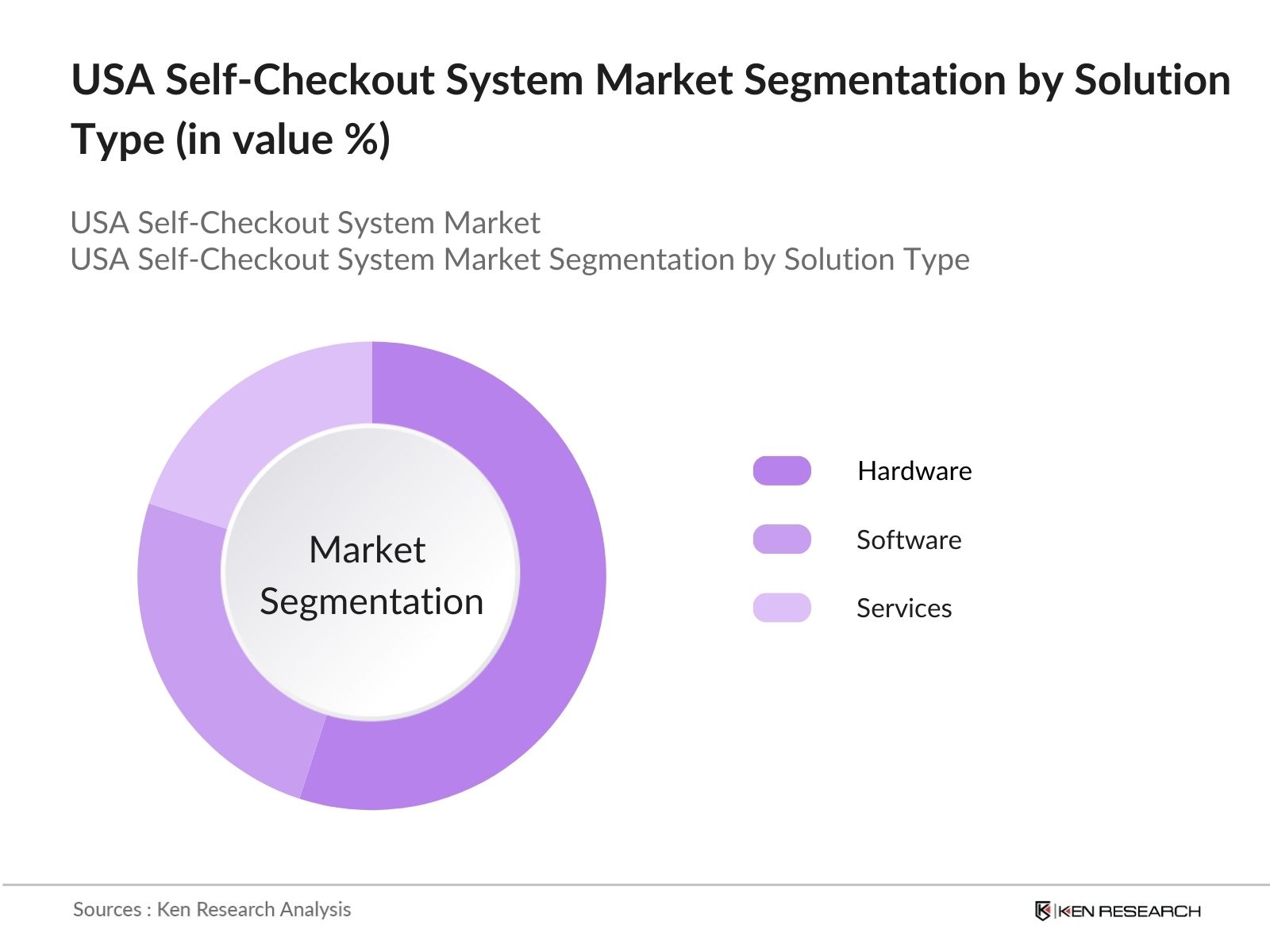

- By Solution Type: The market is segmented by solution type into hardware, software, and services. Hardware solutions, including kiosks and barcode scanners, hold a dominant market share due to their critical role in enabling self-service transactions. Retailers are investing in advanced hardware to provide a seamless customer experience and reduce transaction times. Hardware like hybrid checkout kiosks is particularly prevalent in high-traffic stores, where speed and customer satisfaction are essential.

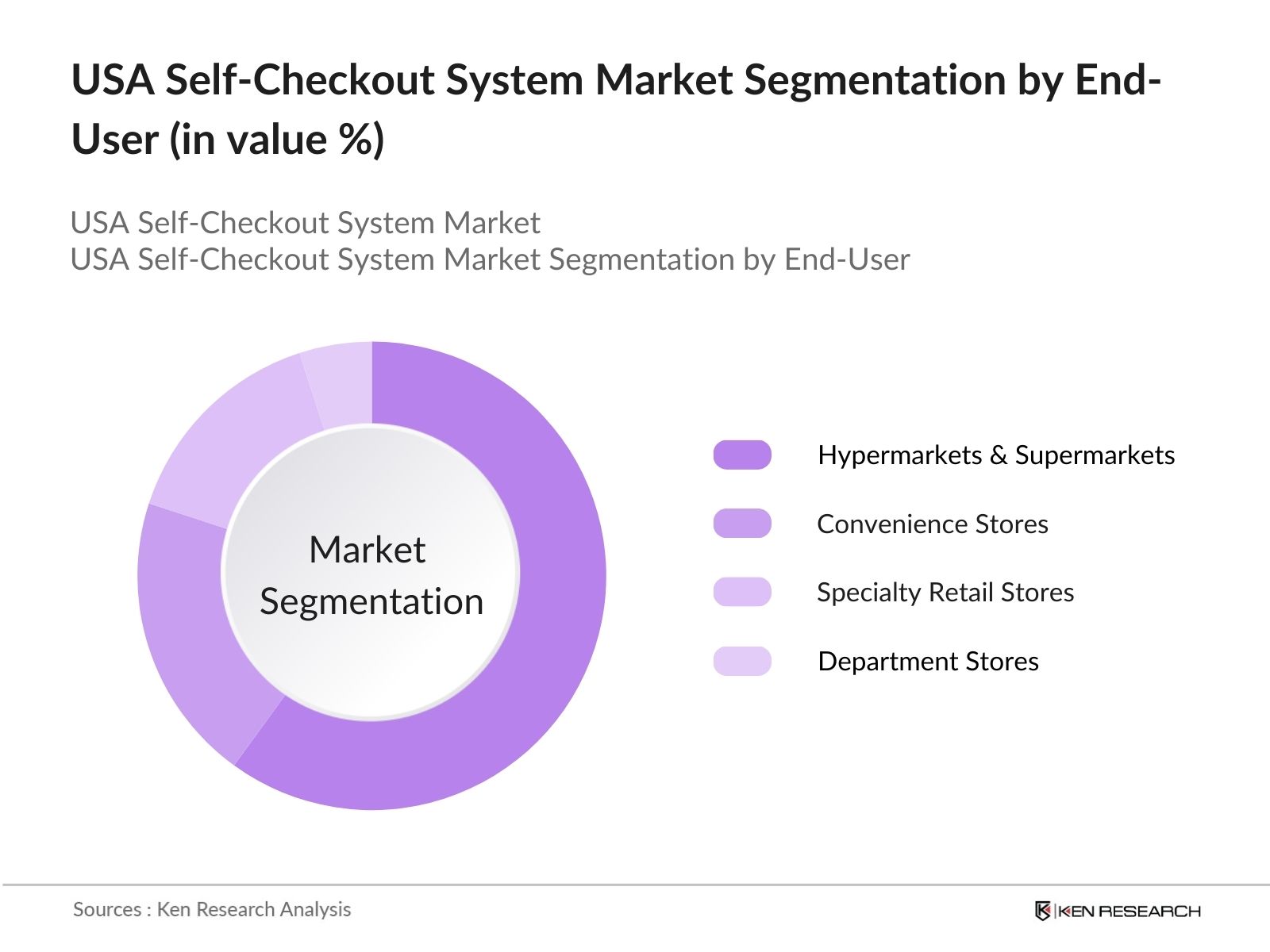

- By End-User: The market is further segmented by end-user into hypermarkets and supermarkets, convenience stores, specialty retail stores, and department stores. Hypermarkets and supermarkets dominate the market share under the end-user segment. This is because large retail chains like Walmart and Costco are implementing self-checkout systems extensively across their stores to streamline the checkout process, minimize staffing costs, and handle high transaction volumes. Their expansive presence and investment in technology drive the dominance of this segment.

USA Self-Checkout System Market Competitive Landscape

The USA Self-Checkout System market is dominated by several key players. These companies are industry leaders due to their innovation, product offerings, and market reach. The market is characterized by a few major players, including NCR Corporation and Diebold Nixdorf, which are prominent in developing self-checkout technologies. Companies like Toshiba and Fujitsu play a vital role in offering customized solutions that cater to different retail environments. The market remains competitive, with investments in R&D to enhance system capabilities, including artificial intelligence and mobile payment integration.

|

Company Name |

Establishment Year |

Headquarters |

Patents |

R&D Spending |

Employee Count |

Partnerships |

Revenue |

Product Portfolio |

Technology Innovations |

|

NCR Corporation |

1884 |

Atlanta, USA |

- |

- |

- |

- |

- |

- |

- |

|

Diebold Nixdorf |

1859 |

North Canton, USA |

- |

- |

- |

- |

- |

- |

- |

|

Toshiba Global Commerce |

1939 |

Tokyo, Japan |

- |

- |

- |

- |

- |

- |

- |

|

Fujitsu Limited |

1935 |

Tokyo, Japan |

- |

- |

- |

- |

- |

- |

- |

|

ITAB Group |

1987 |

Jnkping, Sweden |

- |

- |

- |

- |

- |

- |

- |

USA Self-Checkout System Market Analysis

USA Self-Checkout System Market Growth Drivers

- Labor Shortages: The USA is currently experiencing labor shortages, which impacts the retail sector. According to data from the U.S. Bureau of Labor Statistics, there were over 9 million job openings across various sectors in 2023, with the retail industry among the hardest hit. This shortage has driven retailers to adopt self-checkout systems to reduce dependency on human labor and increase operational efficiency. With a notable gap between job openings and the number of unemployed individuals, automating retail processes has become essential to maintain service levels in high-traffic retail outlets.

- Retail Automation Trends: The USA retail sector is heavily investing in automation. According to the International Federation of Robotics, over 33,000 robots were installed in North American retail outlets in 2023 to assist with customer-facing and back-end operations, including self-checkout systems. This trend has been accelerated by the growing need for efficiency and speed in the retail environment. Automation helps retailers save time, minimize errors, and enhance customer experience, all of which drive the adoption of self-checkout systems in both large and mid-sized retail chains.

- Consumer Preference for Contactless Payments: Contactless payment methods have seen growth, with over 175 million Americans using contactless payment methods at least once a week by 2023, according to data from the U.S. Federal Reserve. This shift toward digital and touchless payment systems is driving the need for self-checkout systems, as they provide a convenient, hygienic, and fast option for consumers. This preference is particularly strong in urban areas, where the density of retail outlets is higher, leading to increased demand for self-checkout solutions that support contactless payments.

USA Self-Checkout System Market Challenges

- High Initial Setup Costs: The cost of implementing self-checkout systems can be prohibitive for smaller retailers. Based on data from the U.S. Small Business Administration, setting up a single self-checkout terminal can cost anywhere from $15,000 to $40,000, depending on the complexity of the system and additional hardware requirements. For small businesses, this can be a upfront investment that may not provide immediate returns. This is a major barrier to adoption, particularly for independent retail outlets that operate on thinner margins compared to large chains.

- Security Concerns and Theft: Self-checkout systems are often vulnerable to theft, with retail shrinkage costing U.S. retailers around $100 billion in 2023, according to the National Association for Shoplifting Prevention. While these systems offer convenience, they also open up opportunities for shoplifting and fraud, such as item swapping or scanning fewer items. Retailers must invest in advanced security features, such as AI-powered loss prevention systems, which increases the overall cost and complexity of maintaining these systems.

USA Self-Checkout System Market Future Outlook

Over the next five years, the USA Self-Checkout System market is expected to experience growth, driven by continuous technological advancements and retailers push to automate and streamline the checkout process. Retailers are expected to increase investments in artificial intelligence and machine learning to improve system accuracy and speed. In addition, the rise of contactless payments and consumer preference for reduced human interaction at checkout will further boost the market. The integration of mobile payments and enhanced security features will also contribute to market expansion.

USA Self-Checkout System Market Opportunities

- Advancements in AI and Machine Learning for Checkout Optimization: The integration of AI and machine learning technologies into self-checkout systems is creating new opportunities for retailers. These technologies can reduce transaction times by up to 25%, according to data from the U.S. Department of Commerce. AI-powered systems can also enhance loss prevention measures by analyzing customer behavior and detecting suspicious activities in real-time. As these technologies become more affordable and widely available, the adoption of self-checkout systems is expected to rise, providing retailers with a competitive edge in optimizing checkout efficiency.

- Integration with Mobile Payment Systems: Mobile payment systems are becoming increasingly integrated with self-checkout solutions. Data from the Federal Reserve shows that over 80 million U.S. consumers used mobile payment apps in 2023, a figure that is expected to grow as more retailers adopt self-checkout systems that support these technologies. Mobile payments provide a seamless, fast, and secure transaction process, which aligns with consumer preferences for convenience and security. Retailers are leveraging this integration to attract tech-savvy customers and streamline their checkout processes.

Scope of the Report

|

Solution Type |

Hardware Software Services |

|

End-User |

Hypermarkets Convenience Stores Specialty Stores |

|

Payment Mode |

Cash Card Payments Mobile Wallets |

|

Component |

Scanners Displays Receipt Printers Payment Terminals |

|

Region |

Northeast Midwest South West |

Products

Key Target Audience

Retail Chains (Walmart, Target, etc.)

Hypermarkets and Supermarkets

Convenience Stores and Specialty Retailers

Banks and Financial Institutions

Self-Checkout Solution Providers

System Integrators and Technology Providers

Investor and Venture Capitalist Firms

Government and Regulatory Bodies (FTC, US Department of Commerce)

Retail Automation and AI Companies

Companies

Players Mentioned in the Report

NCR Corporation

Diebold Nixdorf

Toshiba Global Commerce Solutions

Fujitsu Limited

ITAB Group

ECRS Corporation

IBM Corporation

HP Inc.

Pan-Oston Co.

Zebra Technologies

Table of Contents

1. USA Self-Checkout System Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. USA Self-Checkout System Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. USA Self-Checkout System Market Analysis

3.1. Growth Drivers

3.1.1. Labor Shortages

3.1.2. Retail Automation Trends

3.1.3. Consumer Preference for Contactless Payments

3.1.4. Retail Store Expansions

3.2. Market Challenges

3.2.1. High Initial Setup Costs

3.2.2. Security Concerns and Theft

3.2.3. Limited Adoption in Smaller Retail Outlets

3.3. Opportunities

3.3.1. Advancements in AI and Machine Learning for Checkout Optimization

3.3.2. Integration with Mobile Payment Systems

3.3.3. Growth of Omnichannel Retailing

3.4. Trends

3.4.1. Customizable Self-Checkout Solutions

3.4.2. Integration of Biometric Payments

3.4.3. Modular and Scalable System Deployments

3.5. Government Regulation

3.5.1. Retail and Consumer Protection Laws

3.5.2. Data Privacy Regulations

3.5.3. Local State-Level Security Mandates for Self-Checkout

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. USA Self-Checkout System Market Segmentation

4.1. By Solution Type (In Value %)

4.1.1. Hardware (Self-Checkout Kiosks, Hybrid Checkout Systems)

4.1.2. Software (POS Systems, Inventory Management Software)

4.1.3. Services (Installation, Maintenance, Consulting)

4.2. By End-User (In Value %)

4.2.1. Hypermarkets and Supermarkets

4.2.2. Convenience Stores

4.2.3. Specialty Retail Stores

4.2.4. Department Stores

4.3. By Payment Mode (In Value %)

4.3.1. Cash

4.3.2. Card Payments

4.3.3. Mobile Wallets

4.4. By Component (In Value %)

4.4.1. Scanners

4.4.2. Displays

4.4.3. Receipt Printers

4.4.4. Payment Terminals

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

5. USA Self-Checkout System Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. NCR Corporation

5.1.2. Diebold Nixdorf

5.1.3. Fujitsu Limited

5.1.4. Toshiba Global Commerce Solutions

5.1.5. ITAB Group

5.1.6. ECRS Corporation

5.1.7. Pan-Oston Co.

5.1.8. IBM Corporation

5.1.9. HP Inc.

5.1.10. Kiosk Information Systems

5.1.11. Zebra Technologies

5.1.12. IER Group

5.1.13. StrongPoint ASA

5.1.14. UST Global

5.1.15. Avery Dennison

5.2. Cross Comparison Parameters

5.2.1. Number of Employees

5.2.2. Headquarters Location

5.2.3. Founding Year

5.2.4. Revenue

5.2.5. Technology Patents

5.2.6. Market Presence

5.2.7. Product Portfolio Breadth

5.2.8. Key Partnerships and Alliances

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. USA Self-Checkout System Market Regulatory Framework

6.1. Retail Compliance Standards

6.2. PCI Compliance for Payment Systems

6.3. Certification Requirements

7. USA Self-Checkout System Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Self-Checkout System Future Market Segmentation

8.1. By Solution Type

8.2. By End-User

8.3. By Payment Mode

8.4. By Component

8.5. By Region

9. USA Self-Checkout System Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research process begins by identifying the key variables that influence the USA Self-Checkout System market, focusing on stakeholders such as retailers, technology providers, and consumers. Extensive secondary research is conducted using a mix of proprietary databases and publicly available industry reports to map out the market ecosystem.

Step 2: Market Analysis and Construction

The market analysis involves a detailed examination of the historical data to understand market trends, technology adoption, and end-user demand in the USA. Key market ratios, such as the adoption rate of self-checkout systems across different regions, are analyzed to construct accurate market estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through direct interviews and consultations with industry experts from leading self-checkout technology providers and retailers. These consultations provide insights into market dynamics and operational trends that complement the data collected from secondary sources.

Step 4: Research Synthesis and Final Output

In the final stage, data from both primary and secondary research are synthesized into actionable insights. This comprehensive approach ensures that the market analysis is thorough and validated by industry experts, providing accurate and reliable conclusions.

Frequently Asked Questions

How big is the USA Self-Checkout System Market?

The USA Self-Checkout System market is valued at USD 1.3 billion, driven by increasing automation in retail and consumer preference for faster checkout solutions.

What are the challenges in the USA Self-Checkout System Market?

Challenges in the USA Self-Checkout System market include high initial implementation costs for retailers, concerns over system security and theft, and resistance from smaller retail chains to adopt expensive technologies.

Who are the major players in the USA Self-Checkout System Market?

Key players in the USA Self-Checkout System market include NCR Corporation, Diebold Nixdorf, Fujitsu Limited, Toshiba Global Commerce Solutions, and ITAB Group, known for their innovative product offerings and strong market presence.

What are the growth drivers of the USA Self-Checkout System Market?

Growth of the USA Self-Checkout System market is driven by rising consumer demand for faster checkout processes, the retail industry's push towards automation, and the adoption of contactless payment technologies.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.