USA Soldier Systems Market Outlook to 2030

Region:North America

Author(s):Sanjna

Product Code:KROD2158

December 2024

84

About the Report

USA Soldier Systems Market Overview

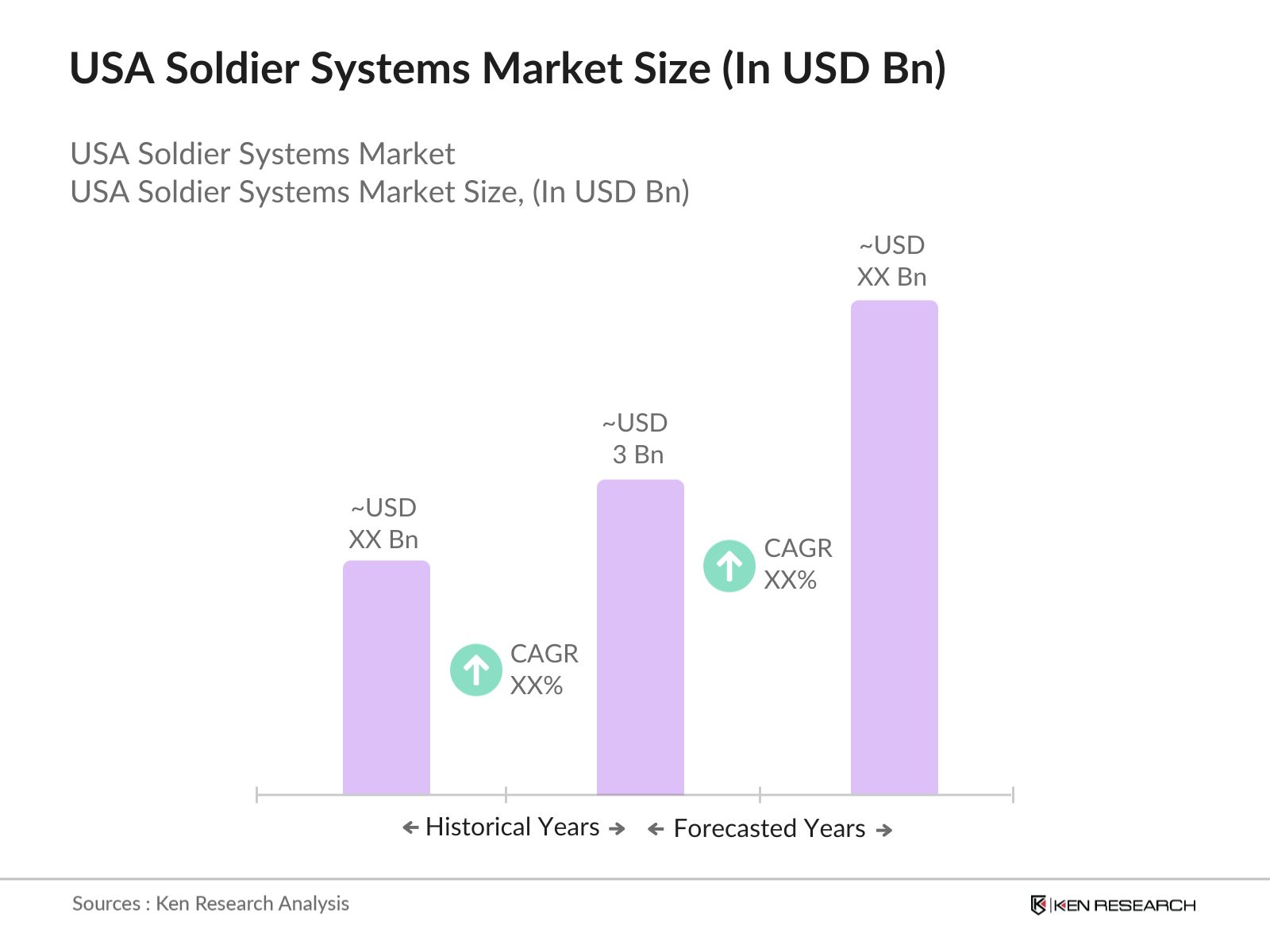

- The USA Soldier Systems Market is valued at USD 3 billion in 2023, driven by increasing defense budgets, the rising need for advanced personal protection, and the integration of sophisticated communication and navigation systems. Investments in research and development of technologies like augmented reality, exoskeletons, and wearable sensors are also propelling market growth.

- Major cities such as Washington, D.C., and San Diego, along with countries like the United States, dominate this market due to their heavy investments in defense R&D and the presence of major defense contractors. Washington, D.C., is home to numerous defense agencies and contractors, while San Diego serves as a hub for the U.S. Navy and defense manufacturers. These cities benefit from proximity to government funding, military installations, and a strong industrial base in soldier systems technologies.

- The International Traffic in Arms Regulations (ITAR) controls the export of U.S. military technologies. In 2023, updates were made which reflect a recognition of the rapid evolution of military technology and the need for the U.S. defense industry to adapt. By streamlining processes related to the export of AI and autonomous systems, these changes aim to reduce bureaucratic delays that have historically hindered timely access to critical technologies for both U.S. companies and allied nations.

USA Soldier Systems Market Segmentation

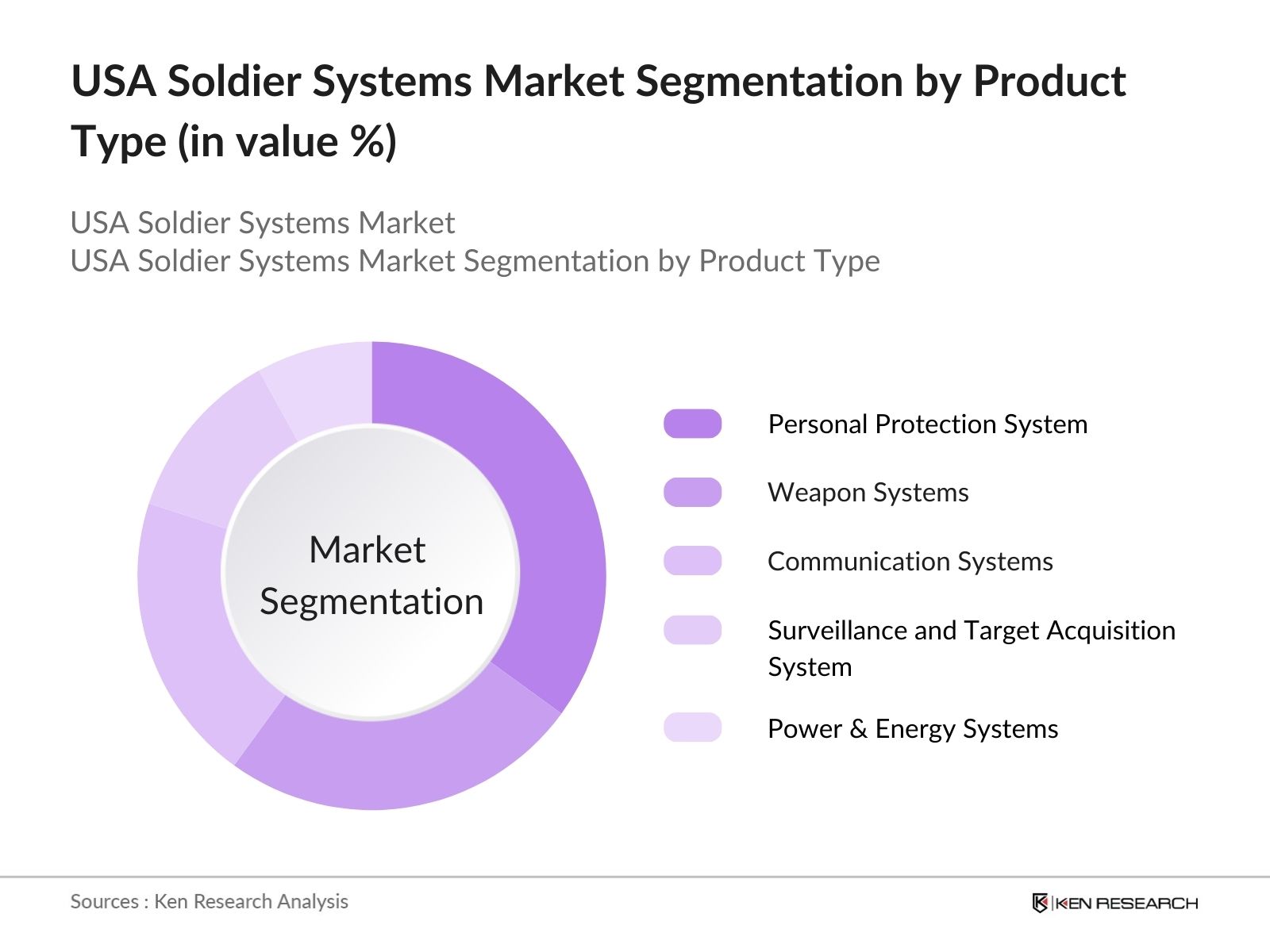

By Product Type: The USA soldier systems market is segmented by product type into personal protection systems, weapon systems, communication systems, surveillance and target acquisition systems, and power and energy systems. Personal protection systems dominate the market share. The dominance of this sub-segment is attributed to the continuous development and procurement of advanced body armor, helmets, and tactical vests. The growing focus on improving soldier survivability, coupled with the adoption of smart textiles and lightweight materials, reinforces the need for cutting-edge protection equipment.

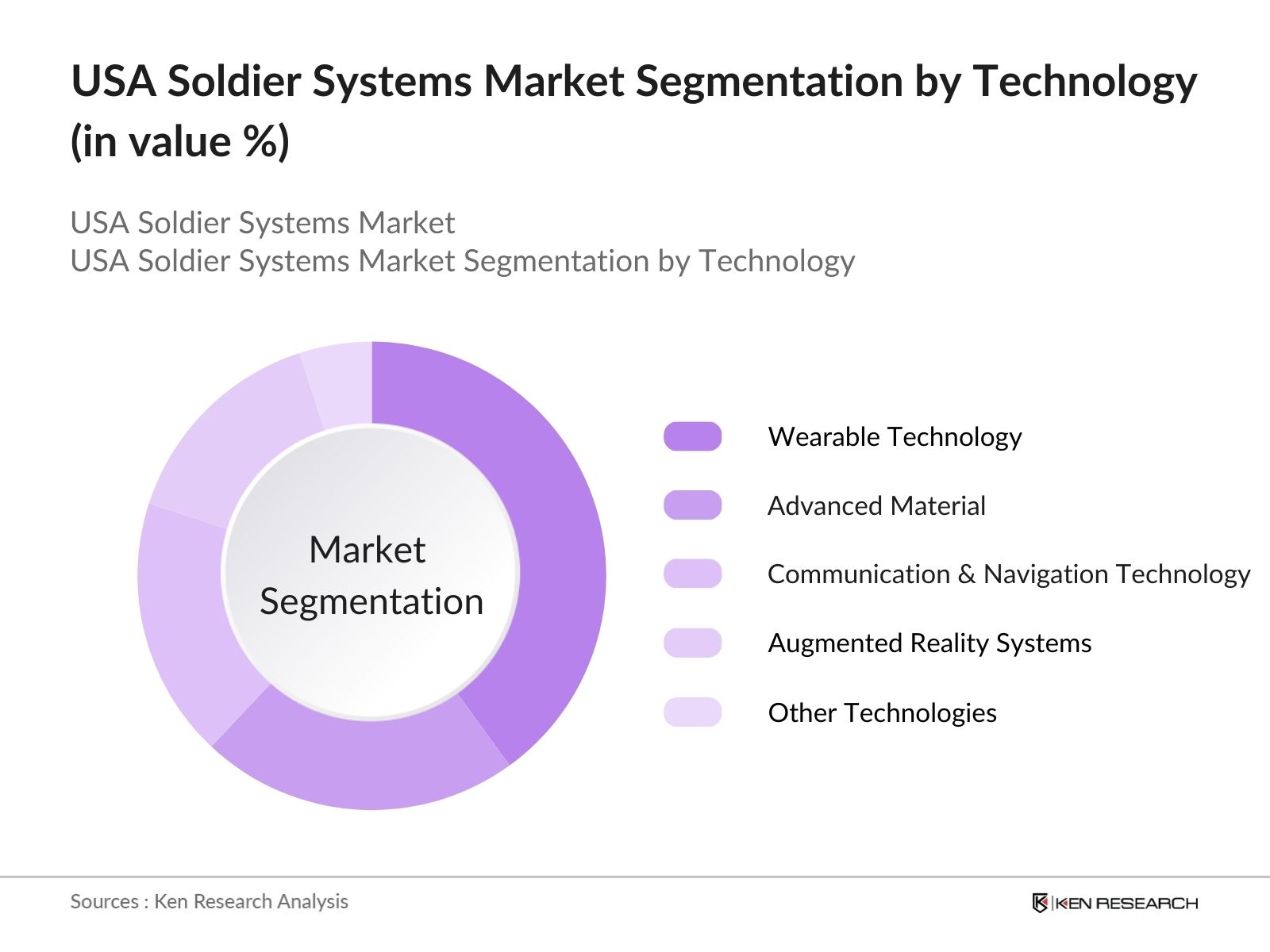

By Technology: The market is segmented by technology into wearable technology, advanced materials, communication and navigation technology, and augmented reality systems. Wearable technology leads the market driven by the increasing adoption of health monitoring systems, smart helmets, and integrated communication systems. These technologies enhance situational awareness and provide real-time data to soldiers in the field, contributing to improved operational efficiency and safety.

USA Soldier Systems Market Competitive Landscape

The USA soldier systems market is dominated by a few key players that contribute to the majority of market revenue. These companies benefit from longstanding relationships with the U.S. Department of Defense and have built comprehensive product portfolios catering to various aspects of soldier systems. Companies like BAE Systems, General Dynamics, and Lockheed Martin continue to lead in innovation and technological advancements.

|

Company Name |

Establishment Year |

Headquarters |

Defense Contracts |

Key product Portfolio |

R&D Spending (USD Mn) |

No. of Employees |

Strategic Initiatives |

|

|

Farnborough, UK |

|||||

|

General Dynamics |

1952 |

Reston, VA, USA |

|||||

|

Lockheed Martin |

1995 |

Bethesda, MD, USA |

|||||

|

Northrop Grumman |

1939 |

Falls Church, VA, USA |

|||||

|

L3Harris Technologies |

2019 |

Melbourne, FL, USA |

USA Soldier Systems Market Analysis

Growth Drivers

- Increased Defense Budget: In FY24, the United States Department of Defense (DoD) budget increased to $886 billion, with a significant allocation directed toward modernizing soldier systems. The budget emphasizes the development of advanced soldier protection, communication, and surveillance systems, reflecting the U.S. government's commitment to enhancing soldier capabilities. This funding supports the procurement of advanced infantry equipment, directly boosting the soldier systems market. These investments aim to ensure operational superiority and preparedness amid growing geopolitical tensions.

- Adoption of Advanced Technologies: The U.S. Army is incorporating cutting-edge technologies such as AI-integrated helmets, smart textiles, and wearable sensors to improve soldier performance and safety. A smart helmet prototype developed by researchers features an infrared camera, power source, processing hub, and augmented reality display to enhance soldier situational awareness. This adoption is vital for enhancing situational awareness and minimizing casualties, especially in unpredictable conflict environments.

- Rising Geopolitical Tensions: Rising geopolitical tensions, particularly in Eastern Europe and the Indo-Pacific, have accelerated defense spending in the U.S. and prompted investment in advanced soldier systems. For FY24, the U.S. Army has requested $27.7 million for the Soldier Systems - Advanced Development program, which focuses on enhancing combat effectiveness through advanced technologies, fostering the expansion of the soldier systems market.

Challenges

- Budget Constraints for Small-Scale Contracts: Despite a robust defense budget, small-scale suppliers in the soldier systems market face challenges in securing contracts. In 2023, the allocation for large defense contractors dwarfed the budget for smaller suppliers, limiting their participation in procurement. This disparity constrains innovation from smaller firms, which struggle to compete for resources and contracts against larger defense companies.

- Technological Integration with Legacy Systems: In 2023, the U.S. military significantly increased its budget to address the growing compatibility challenges between advanced AI-driven systems and legacy communications platforms. These systems, designed to enhance real-time decision-making and situational awareness for soldiers, often rely on high-speed data processing, advanced sensors, and integrated communication networks.

USA Soldier Systems Future Market Outlook

Over the next five years, the USA soldier systems market is expected to exhibit robust growth, driven by continued defense budget allocations, technological advancements, and the U.S. militarys emphasis on modernizing soldier equipment. The increasing incorporation of augmented reality, artificial intelligence, and wearable technologies into soldier systems will further enhance operational capabilities.

Market Opportunities

- Integration of AR/VR in Training Modules: Augmented Reality (AR) and Virtual Reality (VR) are becoming pivotal in training U.S. soldiers. The Army has allocated $255 million for 2025 to enhance its Integrated Visual Augmentation System (IVAS), which uses AR to simulate combat scenarios and improve training outcomes. This technological advancement offers soldiers an immersive training experience, improving preparedness without the risks of physical drills. The demand for AR/VR systems opens significant opportunities for vendors in the soldier systems market.

- Development of Lightweight Body Armor and Exoskeletons: The development of lightweight body armor and exoskeletons is a major opportunity in the U.S. soldier systems market. In 2024, the U.S. military invested into research and development for these technologies, which aim to reduce the burden on soldiers while enhancing their physical capabilities. These innovations are expected to significantly improve mobility, endurance, and injury prevention in combat zones, making them essential for future battlefield operations

Scope of the Report

|

By Product Type |

Personal Protection Systems |

|

Weapon Systems |

|

|

Communication Systems |

|

|

Surveillance and Target Acquisition Systems |

|

|

Power and Energy Systems |

|

|

By Application |

Army |

|

Navy |

|

|

Air Force |

|

|

Special Forces |

|

|

Marine Corps |

|

|

By Technology |

Wearable Technology |

|

Advanced Materials |

|

|

Communication and Navigation Technology |

|

|

Augmented Reality Systems |

|

|

By Soldier Type |

Frontline Soldiers |

|

Support Personnel |

|

|

Special Operations Forces |

|

|

By Region |

North |

|

South |

|

|

East |

|

|

West |

Products

Key Target Audience: Organisations & Entities who can benefit from Subscribing this Report

Defense Contractors & Suppliers

Military Research Laboratories (e.g., U.S. Army Research Laboratory)

Technology Integrators for Defense Systems

Procurement Managers for Defense Agencies

Logistics and Procurement Companies

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., Defense Acquisition University)

Companies

Major Players Mentioned in the Report

BAE Systems

General Dynamics Corporation

Lockheed Martin Corporation

Northrop Grumman

L3Harris Technologies

Raytheon Technologies

Rheinmetall AG

FLIR Systems, Inc.

Leonardo S.p.A.

Thales Group

Oshkosh Defense

Elbit Systems Ltd.

Kongsberg Gruppen

Saab AB

Safran Group

Table of Contents

1. USA Soldier Systems Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Number of Active Systems, Growth in Soldier Deployments, Modernization Initiatives)

1.4. Market Segmentation Overview

2. USA Soldier Systems Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis (Units of Soldier Systems Procured)

2.3. Key Market Developments and Milestones (Defense Spending, Major Contracts)

3. USA Soldier Systems Market Analysis

3.1. Growth Drivers

3.1.1. Increased Defense Budget

3.1.2. Adoption of Advanced Technologies

3.1.3. Modernization of Infantry Equipment

3.1.4. Rising Geopolitical Tensions

3.2. Market Challenges

3.2.1. Budget Constraints for Small-Scale Contracts

3.2.2. Technological Integration with Legacy Systems

3.2.3. Compliance with Defense Regulations

3.3. Opportunities

3.3.1. Integration of AR/VR in Training Modules

3.3.2. Development of Lightweight Body Armor and Exoskeletons

3.3.3. Adoption of AI and Robotics in Soldier Systems

3.4. Trends

3.4.1. Increased Focus on Soldier Health Monitoring Systems

3.4.2. Miniaturization of Communication Devices

3.4.3. Augmented Reality (AR) Integration in Soldier Helmets

3.5. Government Regulation

3.5.1. Military Standards (MIL-STD)

3.5.2. Procurement Laws and Framework

3.5.3. Export Control Regulations (ITAR)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. USA Soldier Systems Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Personal Protection Systems

4.1.2. Weapon Systems

4.1.3. Communication Systems

4.1.4. Surveillance and Target Acquisition Systems

4.1.5. Power and Energy Systems

4.2. By Application (In Value %)

4.2.1. Army

4.2.2. Navy

4.2.3. Air Force

4.2.4. Special Forces

4.2.5. Marine Corps

4.3. By Technology (In Value %)

4.3.1. Wearable Technology

4.3.2. Advanced Materials

4.3.3. Communication and Navigation Technology

4.3.4. Augmented Reality Systems

4.3.5 Other Technologies

4.4. By Soldier Type (In Value %)

4.4.1. Frontline Soldiers

4.4.2. Support Personnel

4.4.3. Special Operations Forces

4.5. By Region (In Value %)

4.5.1. North

4.5.2. South

4.5.3. East

4.5.4. West

5. USA Soldier Systems Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. BAE Systems

5.1.2. General Dynamics Corporation

5.1.3. Lockheed Martin Corporation

5.1.4. Northrop Grumman

5.1.5. L3Harris Technologies

5.1.6. Thales Group

5.1.7. Rheinmetall AG

5.1.8. FLIR Systems, Inc.

5.1.9. Elbit Systems Ltd.

5.1.10. Leonardo S.p.A.

5.1.11. Safran Group

5.1.12. Oshkosh Defense

5.1.13. Raytheon Technologies

5.1.14. Kongsberg Gruppen

5.1.15. Saab AB

5.2. Cross Comparison Parameters (Revenue, Market Share, Defense Contracts, Technological Innovations, Number of Employees, Inception Year, Headquarters, Market Strategy)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. USA Soldier Systems Market Regulatory Framework

6.1. Military Certification Processes

6.2. Compliance Requirements (ITAR, DFARS)

6.3. Environmental Regulations for Defense Products

7. USA Soldier Systems Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Technological Innovation, Geopolitical Tensions)

8. USA Soldier Systems Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By Soldier Type (In Value %)

8.5. By Region (In Value %)

9. USA Soldier Systems Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

10. Contact Us

11. Disclaimer

Research Methodology

Step 1: Identification of Key Variables

The first step involved developing a comprehensive market ecosystem that includes all major stakeholders in the USA soldier systems market. Extensive desk research, including data from defense industry reports, company filings, and proprietary databases, was conducted to pinpoint the key variables influencing the market.

Step 2: Market Analysis and Construction

In this phase, historical data of the USA soldier systems market was gathered and analyzed. Data related to procurement contracts, technological advancements, and soldier system adoption rates were reviewed. This helped in building an accurate market model to understand revenue generation across different product categories.

Step 3: Hypothesis Validation and Expert Consultation

The market hypotheses were validated by conducting interviews with industry experts from major defense contractors and military officials. These insights provided valuable information on trends, procurement cycles, and technological innovations in soldier systems, ensuring a reliable assessment of the market.

Step 4: Research Synthesis and Final Output

The final step involved synthesizing the data from both top-down and bottom-up approaches to create a well-rounded analysis. Interactions with leading defense companies and technology providers helped to verify the projections and market segmentation, providing a thorough understanding of the USA soldier systems market.

Frequently Asked Questions

01. How big is the USA Soldier Systems Market?

The USA Soldier Systems Market is valued at USD 3 billion in 2023, driven by increasing defense budgets, the rising need for advanced personal protection, and the integration of sophisticated communication and navigation systems.

02. What are the challenges in the USA Soldier Systems Market?

Challenges of USA Soldier Systems Market include budget constraints for smaller defense contractors, integration of new technologies with legacy systems, and compliance with stringent military certification requirements like MIL-STD.

03. Who are the major players in the USA Soldier Systems Market?

Major players of USA Soldier Systems Market include BAE Systems, General Dynamics, Lockheed Martin, Northrop Grumman, and L3Harris Technologies, all of which have strong defense contracts and advanced R&D initiatives.

04. What are the growth drivers of the USA Soldier Systems Market?

Key growth drivers of USA Soldier Systems Market include increasing defense budgets, rising geopolitical tensions, and the demand for advanced technologies like augmented reality and wearable health monitoring systems.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.