USA Steel Slag Market Outlook to 2030

Region:North America

Author(s):Naman Rohilla

Product Code:KROD9200

Region:North America

Author(s):Naman Rohilla

Product Code:KROD9200

December 2024

86

The USA steel slag market is dominated by major steel companies and dedicated slag processing firms. These players leverage advanced technologies for slag processing and recycling, contributing to the markets competitive nature.

The USA steel slag market is set to expand as industries increasingly prioritize sustainable construction and waste management practices. Federal infrastructure investment programs and rising environmental awareness are expected to encourage higher steel slag utilization across road construction, cement production, and even agricultural applications. The sector is also likely to benefit from emerging technologies aimed at improving the recycling and processing efficiency of steel slag, creating potential for cost savings and broader adoption across industries.

|

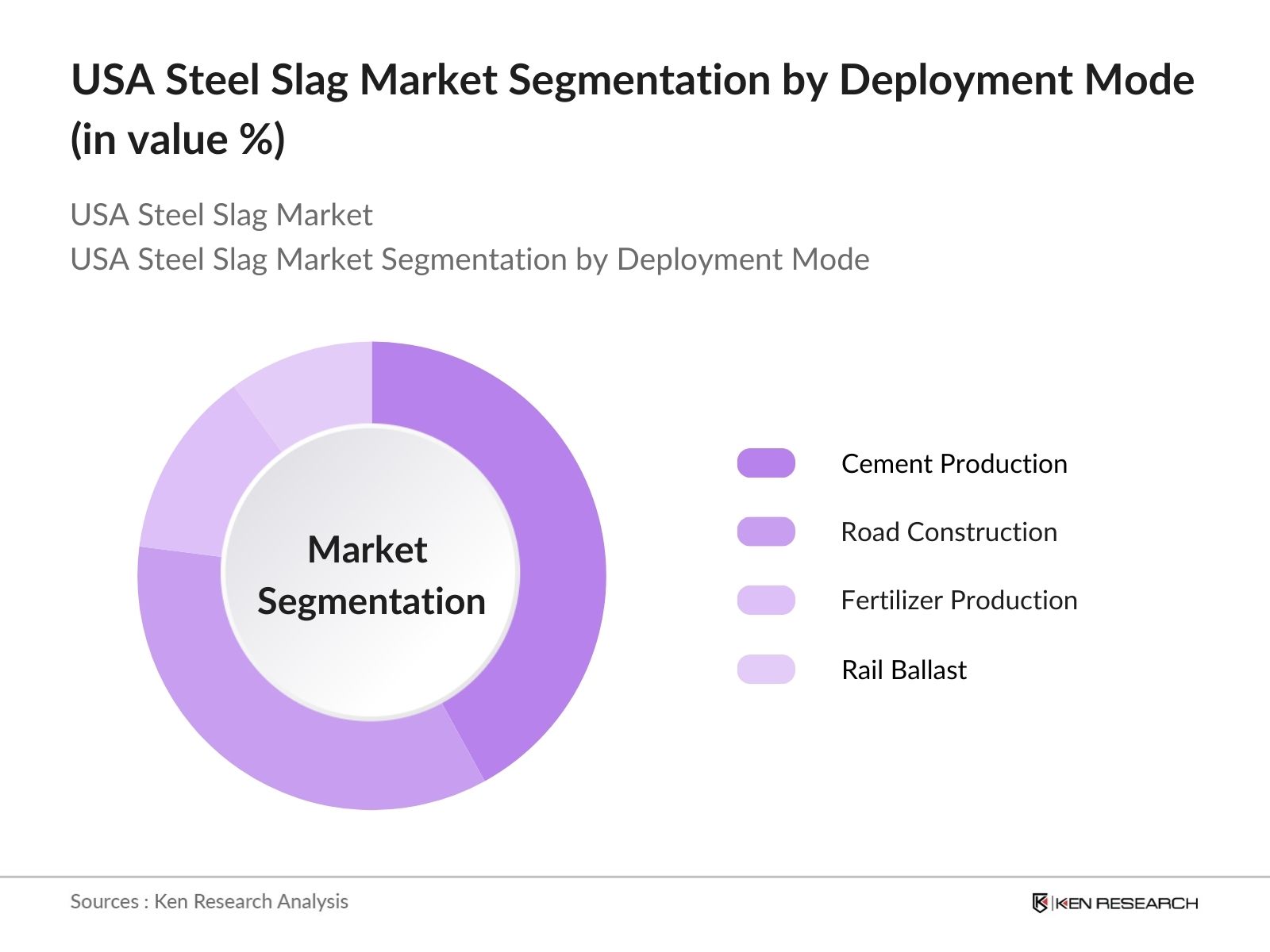

Application |

Cement Production Road Construction Fertilizer Production Rail Ballast |

|

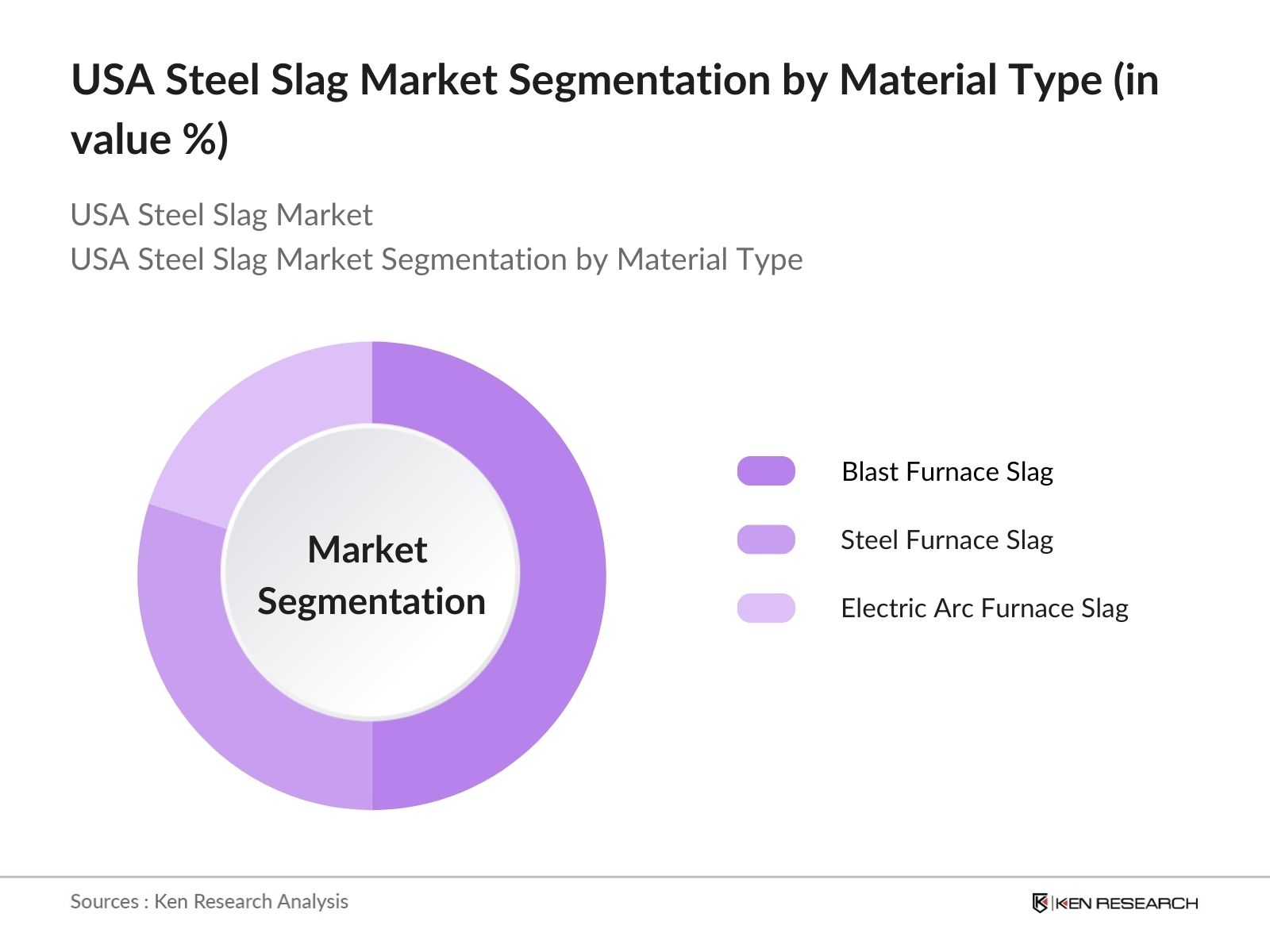

Material Type |

Blast Furnace Slag Steel Furnace Slag Electric Arc Furnace Slag |

|

End-user Industry |

Construction Agriculture Industrial Waste Management |

|

Geography |

Northeast USA Midwest USA Southern USA Western USA |

|

Processing Method |

Crushing and Grinding Screening and Magnetic Separation Leaching and Chemical Treatment |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Material Composition

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Milestones and Industry Benchmarks

3.1. Growth Drivers (Policy Incentives, Industry Demand)

3.1.1. Industrial Demand for Slag as Cement Substitute

3.1.2. Environmental Regulations Promoting Recycling

3.1.3. Technological Advancements in Processing

3.1.4. Urbanization and Infrastructure Projects

3.2. Market Challenges (Logistics, Competition, and Sustainability)

3.2.1. High Processing and Transport Costs

3.2.2. Competition from Natural Aggregates

3.2.3. Environmental Sustainability Challenges

3.3. Opportunities (Innovative Applications and Green Initiatives)

3.3.1. Carbon-Neutral Construction Initiatives

3.3.2. Expansion in the Cement and Asphalt Industries

3.3.3. Rising Demand for Eco-friendly Materials

3.4. Trends (Technology Integration, Market Preferences)

3.4.1. Smart Production Techniques in Steel Slag Processing

3.4.2. Adoption of Slag in Asphalt Roads

3.4.3. Steel Slag in Carbon-Sequestration Efforts

3.5. Regulatory Framework (Environmental Standards and Compliance)

3.5.1. Clean Air Act and Impacts on Production Standards

3.5.2. Waste Management Compliance and Certification

3.5.3. State-Level Regulations on Industrial By-products

3.6. Stakeholder Ecosystem (Key Market Players and Influencers)

3.7. Porters Five Forces Analysis

3.8. SWOT Analysis

4.1. By Application (In Value %)

4.1.1. Cement Production

4.1.2. Road Construction

4.1.3. Fertilizer Production

4.1.4. Rail Ballast

4.2. By Material Type (In Value %)

4.2.1. Blast Furnace Slag

4.2.2. Steel Furnace Slag

4.2.3. Electric Arc Furnace Slag

4.3. By End-user Industry (In Value %)

4.3.1. Construction

4.3.2. Agriculture

4.3.3. Industrial Waste Management

4.4. By Geography (In Value %)

4.4.1. Northeast USA

4.4.2. Midwest USA

4.4.3. Southern USA

4.4.4. Western USA

4.5. By Processing Method (In Value %)

4.5.1. Crushing and Grinding

4.5.2. Screening and Magnetic Separation

4.5.3. Leaching and Chemical Treatment

5.1. Detailed Profiles of Major Companies

5.1.1. ArcelorMittal

5.1.2. Nucor Corporation

5.1.3. Tata Steel USA

5.1.4. Steel Dynamics Inc.

5.1.5. Schnitzer Steel

5.1.6. Phoenix Services LLC

5.1.7. Harsco Corporation

5.1.8. Levy Company

5.1.9. TMS International

5.1.10. Sims Metal Management

5.1.11. Gerdau

5.1.12. CRH

5.1.13. SSAB

5.1.14. Lafarge North America

5.1.15. AK Steel Corporation

5.2. Cross Comparison Parameters (Revenue, Production Capacity, Slag Processing Technology, Market Reach, Environmental Certifications, Key Product Lines, R&D Investment, Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Venture Capital and Private Equity Investments

5.7. Government Funding and Incentives

6.1. Environmental Standards for Slag Recycling

6.2. Compliance and Licensing Requirements

6.3. Certification Processes in the Steel Slag Market

7.1. Market Potential Assessment

7.2. Key Factors Impacting Future Market Growth

7.3. Emerging Applications of Steel Slag

8.1. By Application (In Value %)

8.2. By Material Type (In Value %)

8.3. By End-user Industry (In Value %)

8.4. By Region (In Value %)

8.5. By Processing Method (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Cost Optimization Opportunities

9.3. Product Diversification Strategy

9.4. Market Penetration Strategies

Disclaimer Contact UsThis phase focuses on mapping the ecosystem of the USA Steel Slag Market, identifying key stakeholders across the production, consumption, and recycling spectrums. A combination of secondary and proprietary sources is employed to define critical market variables influencing growth.

Historical data from industry sources is compiled to analyze trends in the steel slag market, covering production volumes, applications, and usage patterns. This includes data verification to ensure comprehensive, industry-relevant insights.

Expert consultations are conducted with market participants to validate the findings and assumptions. Insights gathered from these consultations offer real-time perspectives on market shifts and operational trends.

All insights are synthesized to prepare a final report, verified through cross-referencing with industry publications and proprietary databases, ensuring accuracy and reliability for business professionals.

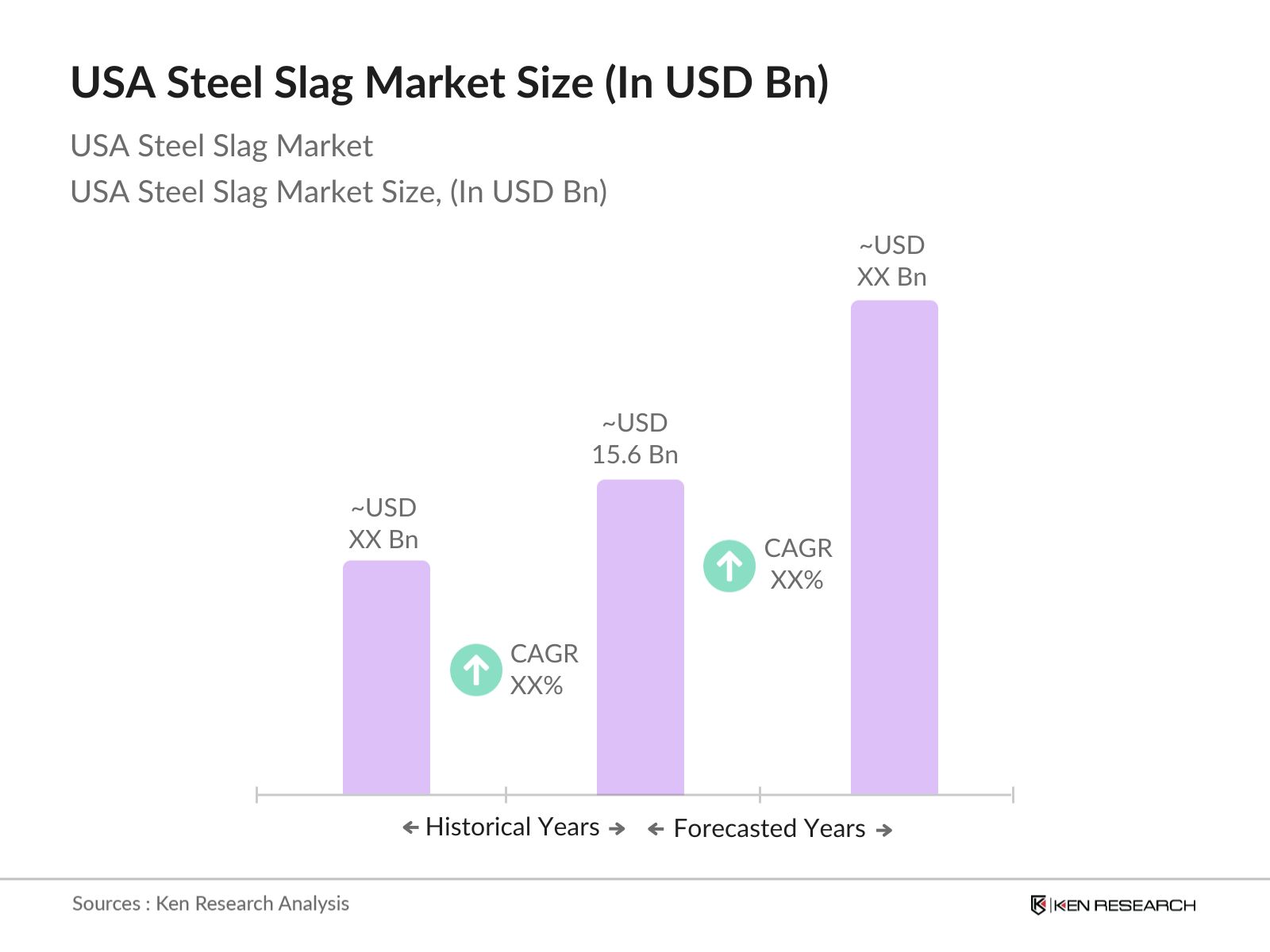

The USA steel slag market is valued at USD 15.6 billion, driven by its diverse applications in construction and sustainable materials, particularly in road construction and cement production.

Key players include ArcelorMittal, Nucor Corporation, Tata Steel USA, Harsco Corporation, and Sims Metal Management, each leveraging advanced slag processing technologies to cater to regional and national demands.

The market is driven by sustainable construction practices, government infrastructure projects, and environmental mandates encouraging the recycling and reuse of industrial by-products like steel slag.

Challenges include high transportation and processing costs, competition from natural aggregates, and the need for sustainable practices to reduce the environmental impact associated with slag production.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.