USA Student Information Systems Market Outlook to 2030

Region:North America

Author(s):Shubham Kashyap

Product Code:KROD9252

December 2024

87

About the Report

USA Student Information Systems Market Overview

The USA Student Information Systems (SIS) market is valued at around USD 2.2 billion, a figure reflecting the nationwide push toward digital transformation across educational institutions. Schools and universities are increasingly adopting SIS to meet the growing demands for streamlined administrative processes, efficient data management, and improved communication among students, parents, and faculty. The shift is particularly driven by the rising adoption of cloud-based solutions, which offer scalability and ease of access, alongside the integration of advanced technologies such as artificial intelligence and data analytics.

- Major urban centers like New York, California, and Texas lead the SIS market, propelled by their large student populations and significant investments in educational technology. These states are home to some of the nations most populous school districts and universities, creating a high demand for efficient SIS solutions. New York City alone oversees over a million students, while California and Texas each manage millions across extensive networks of K-12 schools and higher education institutions.

- The Family Educational Rights and Privacy Act (FERPA) governs the handling of student data, requiring U.S. educational institutions to implement strict data privacy measures. FERPA compliance has led to millions in cybersecurity investments by educational institutions in 2023, as schools adapt to evolving privacy standards and ensure SIS solutions meet compliance requirements.

USA Student Information Systems Market Segmentation

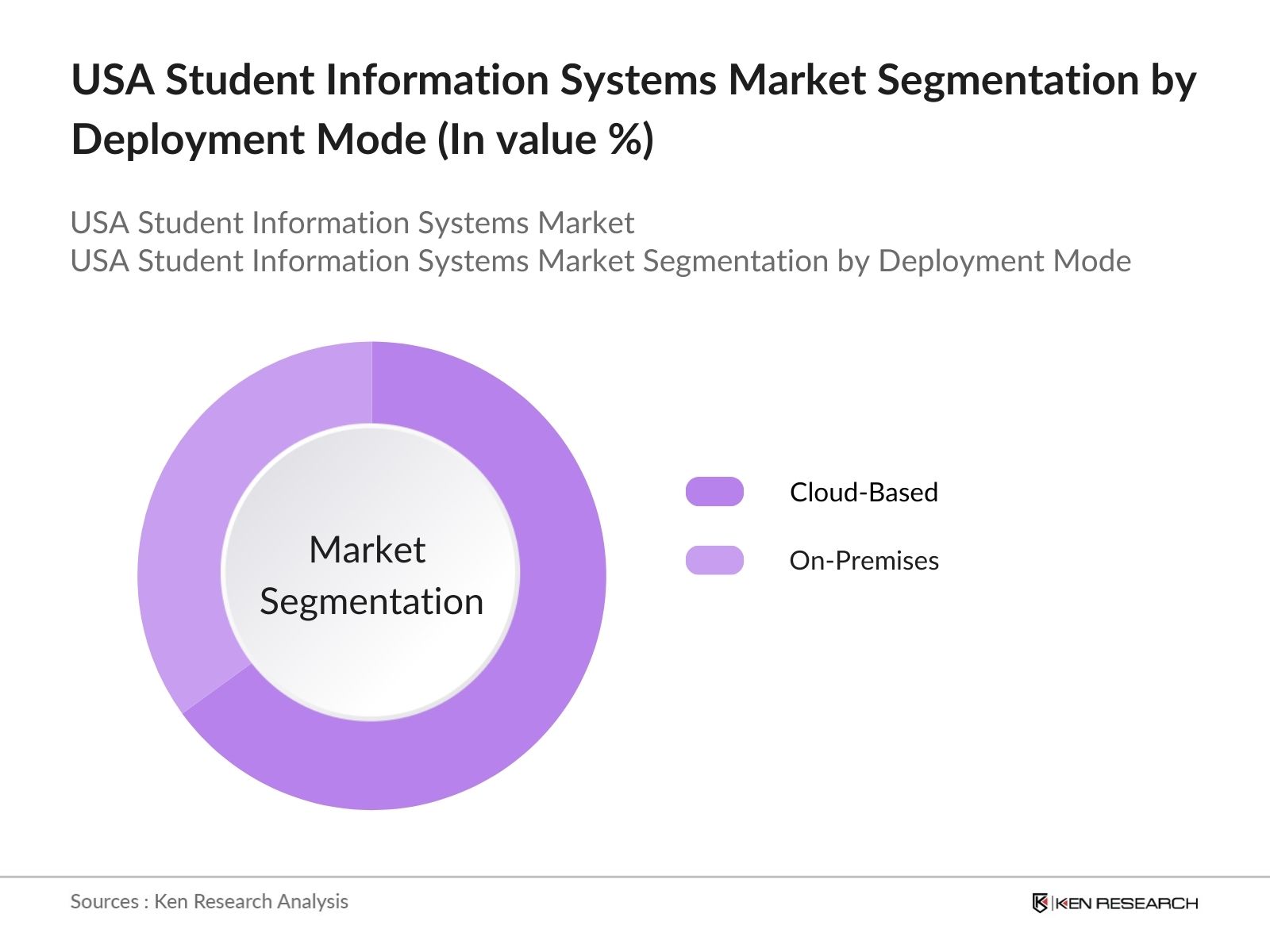

- By Deployment Mode: The market is segmented by deployment mode into on-premises and cloud-based solutions. Cloud-based SIS solutions have a dominant market share in the USA under the deployment mode segmentation. This is attributed to their scalability, cost-effectiveness, and ease of access, which are particularly beneficial for institutions seeking to modernize their administrative processes without significant upfront investments. The flexibility offered by cloud-based systems allows for seamless updates and integration with other educational technologies, further enhancing their appeal.

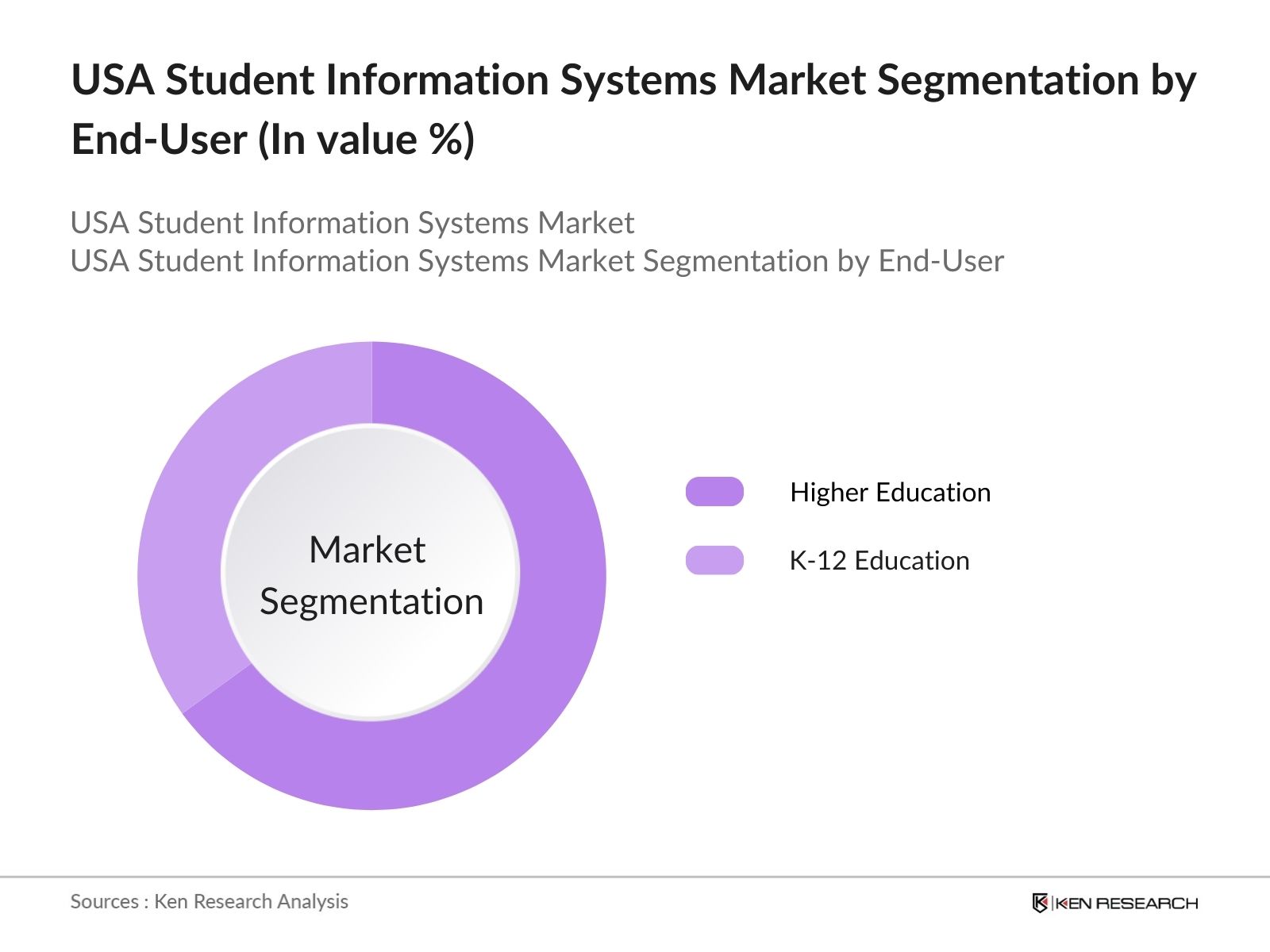

- By End-User: The market is also segmented by end-user into K-12 education and higher education institutions. Higher education institutions hold a dominant market share in the USA under the end-user segmentation. This dominance is due to the complex administrative needs of universities and colleges, which require comprehensive SIS solutions to manage student records, course registrations, financial aid, and compliance with accreditation standards. The emphasis on data-driven decision-making and the need to enhance student engagement and retention rates further drive the adoption of SIS in higher education.

USA Student Information Systems Market Competitive Landscape

The USA Student Information Systems market is characterized by the presence of several key players offering a range of solutions tailored to the diverse needs of educational institutions. These companies leverage technological advancements and strategic partnerships to maintain their competitive edge.

USA Student Information Systems Market Analysis

Growth Drivers

- Digital Transformation in Education: Digital transformation in the U.S. education sector has been significantly propelled by investments in technology infrastructure, particularly to enhance Student Information Systems (SIS). In 2024, U.S. federal funding allocated USD 20 billion to K-12 institutions, aiming to bolster digital adoption and infrastructure enhancements across educational facilities, aligning with the Department of Educations goals. As of 2023, 70 million students are enrolled in K-12 and higher education, with an increasing demand for digital resources to improve student management and data analytics.

- Increasing Adoption of E-Learning Platforms: The rapid integration of e-learning platforms in U.S. educational institutions has expanded, with over majority of universities implementing digital platforms to support remote and hybrid learning as of 2023. Supported by government incentives, the adoption of e-learning has proven critical in managing educational data and improving accessibility, with the U.S. governments 2024 budget prioritizing technology advancements across public education. This adoption fosters a seamless SIS experience, empowering institutions to maintain comprehensive records and track student progress.

- Demand for Efficient Administrative Processes: U.S. schools have seen a substantial increase in administrative tasks since 2022, particularly in data management and record-keeping. As education institutions face mounting pressure to streamline operations, SIS solutions are seen as essential to automating processes like enrollment and attendance tracking. Administrative spending by U.S. educational institutions topped billions in 2023, illustrating the need for digital systems that support cost-effective, efficient management across both K-12 and higher education.

Challenges

- Data Privacy and Security Concerns: Data privacy and security concerns are significant for educational institutions implementing Student Information Systems (SIS) as these systems manage sensitive student data. The Family Educational Rights and Privacy Act (FERPA) requires educational institutions to uphold stringent data protection practices, which can present challenges for schools adopting SIS solutions. Government regulations mandate regular security audits and ongoing upgrades to meet compliance standards, pushing institutions to prioritize cybersecurity measures to protect student information. These requirements underscore the importance of robust data privacy protocols in the SIS market to maintain trust and compliance.

- High Implementation Costs: The cost of implementing SIS solutions can be a substantial barrier, particularly for public schools with limited budgets. The setup process involves expenses for hardware, software, and comprehensive training programs, making SIS adoption challenging for institutions without adequate funding. Smaller schools, in particular, face financial constraints, which restrict their ability to invest in SIS solutions without state or federal support. This cost challenge highlights the need for additional funding within the educational technology sector to ensure equitable access to SIS across all types of educational institutions.

USA Student Information Systems Market Future Outlook

The USA Student Information Systems market is projected to experience robust growth, driven by the ongoing demand for sustainable and innovative nonwoven solutions. With increased investments in R&D and a strong focus on eco-friendly materials, manufacturers are likely to introduce advanced products that cater to evolving consumer preferences. Furthermore, the rise in automation and digitalization within manufacturing processes is expected to enhance operational efficiency, solidifying the markets growth trajectory.

Future Market Opportunities

- Integration with Advanced Technologies: AI and Machine Learning (ML) technologies are increasingly integrated with SIS, supporting data-driven decision-making for student performance and administrative tasks. In 2023, U.S. schools spent a substantial amount on AI-based solutions, with SIS vendors enhancing predictive analytics to support educational success metrics. The integration of IoT in campuses, like connected devices for attendance and security, further augments data collection capabilities, fostering efficient student information management.

- Expansion of Cloud-Based Solutions: Cloud-based SIS adoption in the U.S. has grown, with majority of educational institutions adopting cloud infrastructure as of 2023, driven by demand for scalable and secure data solutions. With an estimated over a billion investment in cloud technologies across K-12 and higher education sectors, cloud-based SIS provides schools with flexibility in managing data access, security, and storage solutions, while meeting FERPA compliance requirements.

Scope of the Report

|

By Component |

Software |

|

By Deployment Mode |

On-Premises |

|

By Application |

Student Management |

|

By End-User |

K-12 Education |

|

By Region |

Northeast |

Products

Key Target Audience

Educational Institutions (K-12 and Higher Education)

Educational Technology Providers

Investors and Venture Capitalist Firms

Banks and Financial Institutions

Government and Regulatory Bodies (e.g., U.S. Department of Education)

IT and Software Development Companies

Data Security and Compliance Firms

Professional Development and Training Organizations

Companies

Players Mentioned in the Report

Oracle Corporation

Workday, Inc.

Ellucian Company L.P.

Jenzabar, Inc.

PowerSchool Holdings Inc.

SAP SE

Skyward, Inc.

Illuminate Education

Campus Management Corp. (Anthology Inc.)

Foradian Technologies

Beehively

Infinite Campus, Inc.

Gradelink Corporation

Blackbaud, Inc.

Unit4

Table of Contents

1. USA Student Information Systems Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. USA Student Information Systems Market Size (USD Million)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. USA Student Information Systems Market Analysis

3.1 Growth Drivers

3.1.1 Digital Transformation in Education

3.1.2 Increasing Adoption of E-Learning Platforms

3.1.3 Demand for Efficient Administrative Processes

3.1.4 Government Initiatives and Funding

3.2 Market Challenges

3.2.1 Data Privacy and Security Concerns

3.2.2 High Implementation Costs

3.2.3 Resistance to Change in Educational Institutions

3.3 Opportunities

3.3.1 Integration with Advanced Technologies (AI, ML, IoT)

3.3.2 Expansion of Cloud-Based Solutions

3.3.3 Rising Demand for Mobile Access and Remote Learning

3.4 Trends

3.4.1 Adoption of Analytics for Student Performance Tracking

3.4.2 Emphasis on Personalized Learning Experiences

3.4.3 Growth of SaaS-Based SIS Solutions

3.5 Government Regulations

3.5.1 FERPA Compliance

3.5.2 Data Protection and Privacy Laws

3.5.3 Funding Programs for Educational Technology

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porter’s Five Forces Analysis

3.9 Competitive Landscape

4. USA Student Information Systems Market Segmentation

4.1 By Component (Value %)

4.1.1 Software

4.1.2 Services

4.2 By Deployment Mode (Value %)

4.2.1 On-Premises

4.2.2 Cloud-Based

4.3 By Application (Value %)

4.3.1 Student Management

4.3.2 Admission and Recruitment

4.3.3 Financial Management

4.3.4 Student Engagement and Support

4.3.5 Others

4.4 By End-User (Value %)

4.4.1 K-12 Education

4.4.2 Higher Education

4.5 By Region (Value %)

4.5.1 Northeast

4.5.2 Midwest

4.5.3 South

4.5.4 West

5. USA Student Information Systems Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

Oracle Corporation

Workday, Inc.

SAP SE

Jenzabar, Inc.

Skyward, Inc.

Illuminate Education

Ellucian Company L.P.

Campus Management Corp. (Anthology Inc.)

Foradian Technologies

Beehively

PowerSchool Holdings Inc.

Infinite Campus, Inc.

Gradelink Corporation

Blackbaud, Inc.

Unit4

5.2 Cross Comparison Parameters

5.2.1 Number of Employees

5.2.2 Headquarters Location

5.2.3 Year of Establishment

5.2.4 Revenue

5.2.5 Product Offerings

5.2.6 Market Share

5.2.7 Key Clients

5.2.8 Recent Developments

5.2.9 Strategic Initiatives

5.3 Market Share Analysis

5.4 Strategic Initiatives

Mergers and Acquisitions

Investment Analysis

Venture Capital Funding

Government Grants

Private Equity Investments

6. USA Student Information Systems Market Regulatory Framework

6.1 Educational Standards

6.2 Compliance Requirements

6.3 Certification Processes

7. USA Student Information Systems Market Future Projections

7.1 Future Market Size (USD Million)

7.2 Future Market Size Projections

7.3 Key Factors Driving Future Market Growth

8. USA Student Information Systems Market Future Segmentation

8.1 By Component (Value %)

8.2 By Deployment Mode (Value %)

8.3 By Application (Value %)

8.4 By End-User (Value %)

8.5 By Region (Value %)

9. USA Student Information Systems Market Analysts’ Recommendations

9.1 Total Addressable Market (TAM), Serviceable Available Market (SAM), Serviceable Obtainable Market (SOM) Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the USA Student Information Systems Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the USA Student Information Systems Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple Student Information Systems providers to acquire detailed insights into product segments, sales performance, and consumer preferences. This interaction serves to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the USA Student Information Systems market.

Frequently Asked Questions

How big is the USA Student Information Systems Market?

The USA Student Information Systems market is valued at USD 2.2 billion, driven by the growing demand for digital solutions in educational administration and the shift towards cloud-based platforms in the education sector.

What are the primary growth drivers in the USA Student Information Systems Market?

The growth of the USA SIS market is primarily driven by digital transformation in educational institutions, the adoption of data-driven decision-making, and the need for enhanced data security and compliance with regulations.

Which segments dominate the USA Student Information Systems Market?

Cloud-based solutions dominate the USA SIS market due to their scalability and cost-effectiveness, while higher education institutions hold a significant share under the end-user segmentation, owing to their complex administrative needs.

Who are the major players in the USA Student Information Systems Market?

Key players in the USA SIS market include Oracle Corporation, Workday, Ellucian, PowerSchool, and Jenzabar, which lead due to their advanced technological offerings, extensive client bases, and ongoing investments in innovation.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.