USA Video Surveillance Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD9167

December 2024

90

About the Report

USA Video Surveillance Market Overview

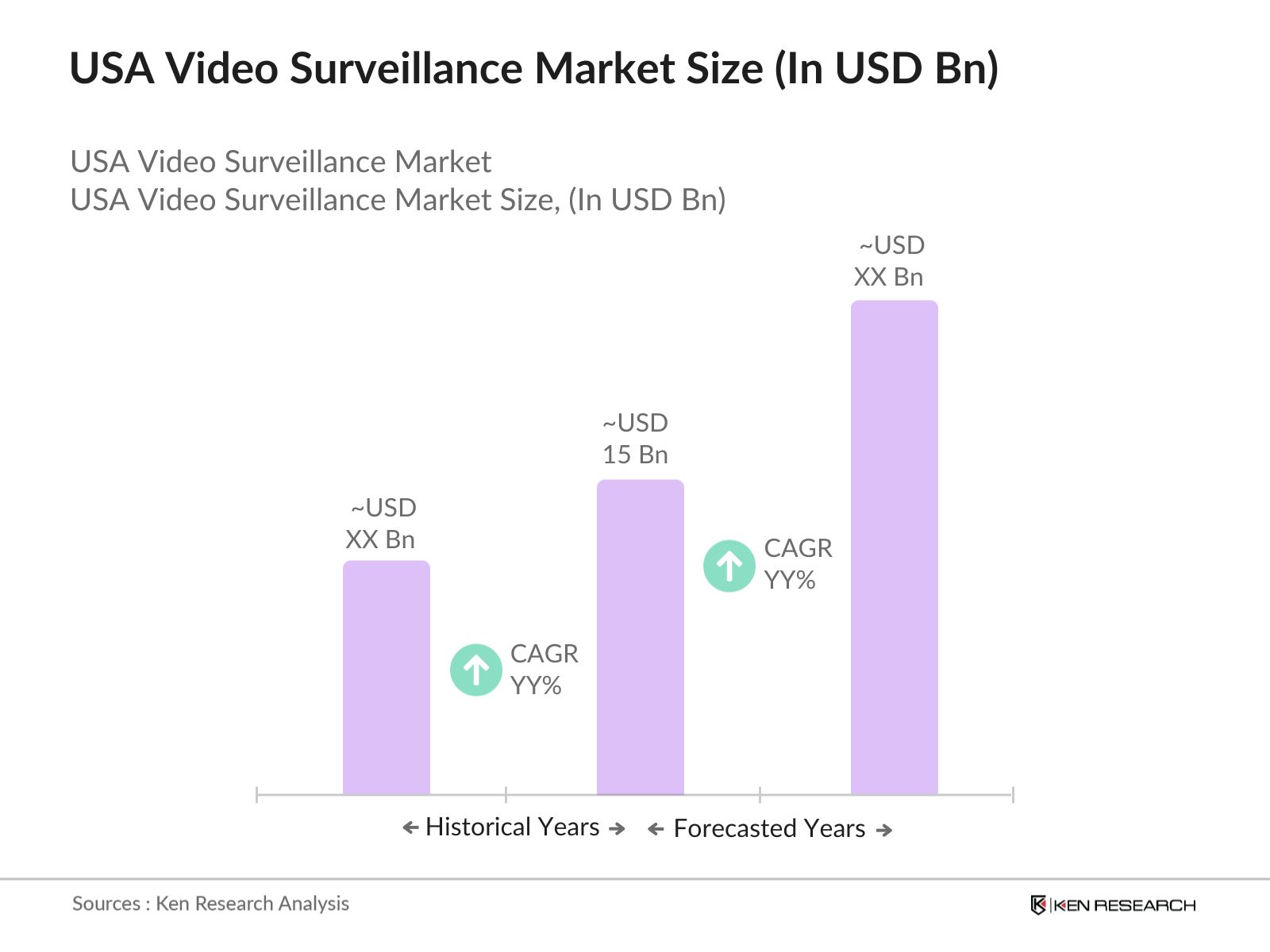

- The USA Video Surveillance market is valued at USD 15 billion, and it is driven primarily by advancements in IP-based camera technologies and a growing emphasis on public safety and security. Over the last five years, there has been significant investment in video analytics, cloud-based storage, and AI-driven surveillance solutions, boosting the market.

- Certain regions within the USA, like New York and Los Angeles, lead the video surveillance market due to their high crime rates and densely populated urban environments, which create a demand for extensive surveillance networks. Additionally, major government initiatives aimed at enhancing public safety in these metropolitan areas and across vital infrastructure drive the market further. Large-scale investment in public and private security systems ensures these cities remain dominant players.

- In 2024, the US government allocated over $5 billion in its budget towards improving national security through surveillance technologies, specifically targeting border regions. This initiative includes the deployment of video surveillance systems along key border checkpoints and in critical infrastructure zones, including airports, seaports, and power stations.

USA Video Surveillance Market Segmentation

By Offering: The market is segmented into hardware, software, and services. In 2023, hardware, especially IP-based cameras, holds a dominant share. This dominance is attributed to the transition from analog to IP systems, which offer better scalability, higher resolution, and real-time monitoring capabilities. IP cameras are increasingly favored by large businesses, government entities, and residential users for their ease of installation and integration into existing IT networks.

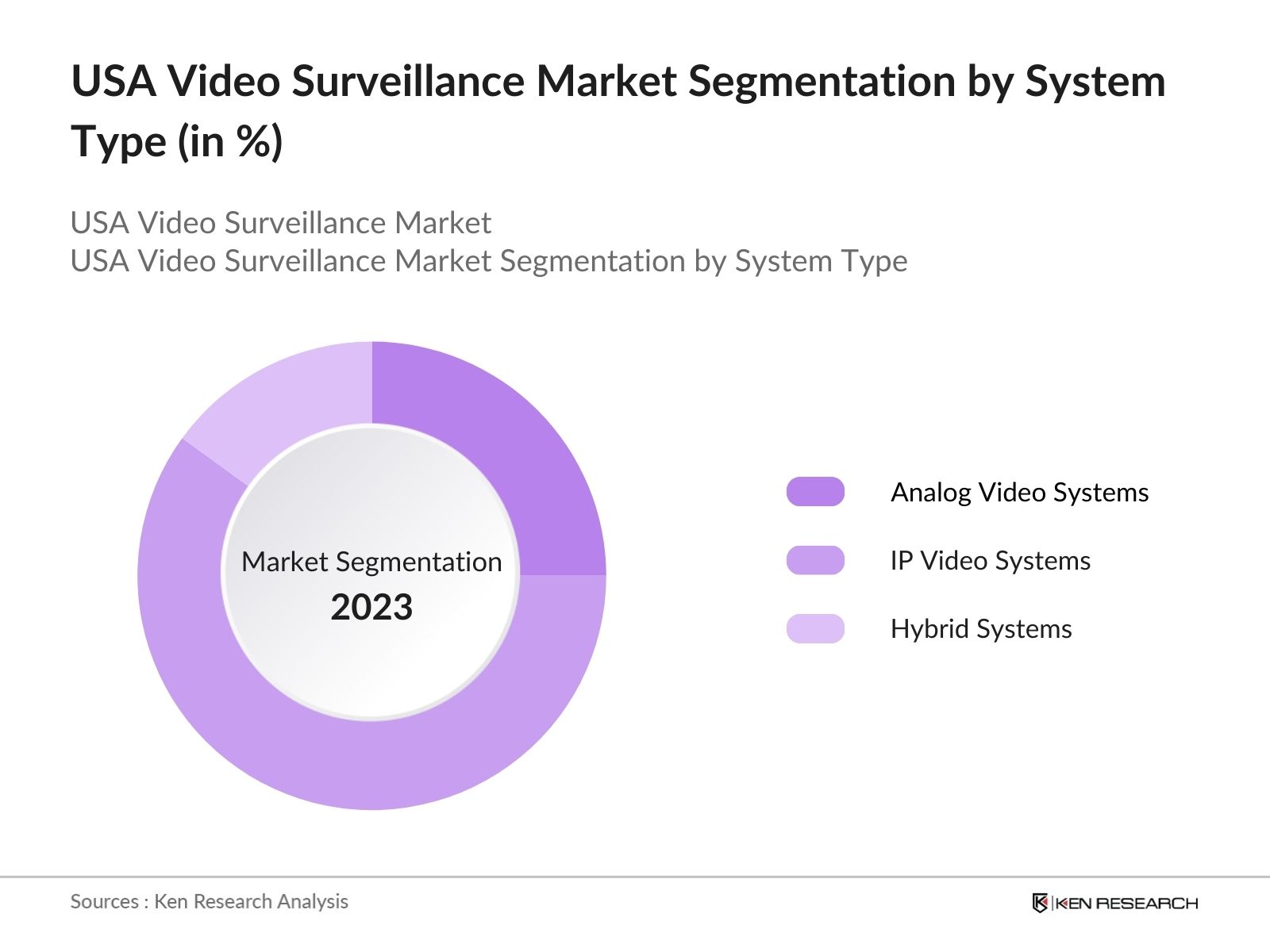

By System Type: The market is also categorized into analog video systems, IP video systems, and hybrid systems. Among these, IP video surveillance systems dominate the market due to their superior features, such as real-time surveillance, remote access, and better scalability. IP systems are particularly favored by the government and large commercial setups for their ability to handle higher data loads and enhanced integration with cloud storage. Hybrid systems, which combine analog and IP technologies, are gaining traction in businesses seeking to upgrade their surveillance infrastructure gradually.

USA Video Surveillance Market Competitive Landscape

The market is dominated by a few major players who have established themselves through continuous innovation and a broad portfolio of products. Companies like Hikvision, Dahua Technology, and Bosch Security Systems lead the market due to their advanced product offerings and extensive global reach.

|

Company |

Establishment Year |

Headquarters |

Revenue |

Product Portfolio |

R&D Spend |

Global Presence |

Customer Base |

Technological Advancements |

|

Hikvision |

2001 |

Hangzhou, China |

||||||

|

Dahua Technology |

2001 |

Hangzhou, China |

||||||

|

Bosch Security Systems |

1921 |

Gerlingen, Germany |

||||||

|

Axis Communications AB |

1984 |

Lund, Sweden |

||||||

|

Honeywell International |

1906 |

Charlotte, USA |

USA Video Surveillance Market Analysis

Market Growth Drivers

- Increasing Demand for Enhanced Security in Public and Private Sectors: The growing concern over safety and security in public spaces and private enterprises has driven the demand for video surveillance systems in the USA. According to recent data from 2024, over 1,200 municipalities have implemented video surveillance in public transportation systems, airports, and schools.

- Growing Investment in Infrastructure and Smart Cities Initiatives: The USA governments push towards smart city developments is driving the video surveillance market. By 2024, approximately 500 cities have begun implementing smart city technologies, with an emphasis on surveillance for traffic management, public safety, and law enforcement.

- Increase in Corporate and Retail Security Requirements: The corporate sector, especially in industries like retail, banking, and manufacturing, has seen heightened security concerns due to theft, fraud, and employee monitoring needs. By 2024, nearly 80,000 retail stores across the USA have installed advanced surveillance systems, especially in areas prone to high shrinkage or theft incidents.

Market Challenges

- Data Privacy Concerns and Regulations: Data privacy concerns, particularly around facial recognition and the storage of personal information, have posed challenges to the adoption of video surveillance systems. In 2024, over 25 states have enacted stricter regulations around the use of video surveillance in public spaces, making it harder for companies to deploy facial recognition technology without proper consent.

- High Installation and Maintenance Costs: Video surveillance systems, especially those integrated with AI and analytics, are capital intensive. As of 2024, businesses have reported an average upfront cost of $25,000 for large-scale video surveillance installations. Maintenance, which includes software updates and system repairs, adds a further $5,000 annually for enterprises.

USA Video Surveillance Market Future Outlook

The USA Video Surveillance industry is poised for continued growth over the next five years, driven by several factors, including advancements in AI, increasing adoption of Video Surveillance-as-a-Service (VSaaS), and growing demand for public and commercial safety.

Future Market Opportunities

- Widespread Adoption of AI and Machine Learning in Surveillance: Over the next five years, the use of AI and machine learning in video surveillance will increase across industries. By 2028, it is expected that more than 80% of new video surveillance systems in the USA will be AI-integrated, offering capabilities such as facial recognition, automated threat detection, and predictive analytics.

- Increased Government Surveillance in Critical Infrastructure: Government spending on surveillance for critical infrastructure, including power plants, water facilities, and transport networks, is projected to rise sharply. By 2029, federal and state governments are expected to invest an additional $8 billion in advanced surveillance technologies to safeguard these essential services, driven by rising geopolitical tensions and security threats.

Scope of the Report

|

By Offering |

Hardware Software Services |

|

By System Type |

Analog Video Systems IP Video Systems Hybrid Systems |

|

By Application |

Commercial Residential Infrastructure Transportation Defense |

|

By Region |

North South West East |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Government and Regulatory Bodies (Department of Homeland Security, FCC)

Banks and Financial Institution

Video Surveillance Solution Providers

Private Equity Firms

Transportation and Logistics Firms

Investors and Venture Capitalist Firms

Smart City Technology Providers

Companies

Players Mentioned in the Report:

Hikvision Digital Technology Co. Ltd

Dahua Technology Co. Ltd

Bosch Security Systems

Honeywell International Inc.

Axis Communications AB

Avigilon Corporation

FLIR Systems Inc.

Genetec Inc.

Panasonic Corporation

Hanwha Techwin

Table of Contents

USA Video Surveillance Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics (Growth drivers, challenges, and opportunities)

1.4. Market Segmentation Overview

USA Video Surveillance Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones (Transition to IP Cameras, Technological Advancements)

USA Video Surveillance Market Analysis

3.1. Growth Drivers (Factors including demand for public security, smart city integration)

3.1.1. Increasing adoption of IP cameras (Shift from analog to IP-based systems)

3.1.2. Rise of AI and video analytics (Market demand for real-time insights and automation)

3.1.3. Government security mandates (Regulations for public and infrastructure surveillance)

3.2. Market Challenges

3.2.1. Privacy concerns and regulatory constraints

3.2.2. High storage requirements for high-definition videos

3.2.3. Cybersecurity threats in connected surveillance systems

3.3. Opportunities

3.3.1. Video Surveillance-as-a-Service (VSaaS) as a growing model

3.3.2. Integration with IoT (Smart devices and connected infrastructure)

3.3.3. Expansion in commercial sectors (Retail, Transportation, Healthcare)

3.4. Trends

3.4.1. Increasing use of video analytics for retail and law enforcement

3.4.2. Use of cloud-based storage solutions

3.4.3. Growth in thermal cameras and facial recognition systems

3.5. Regulatory Landscape

3.5.1. U.S. federal and state surveillance regulations

3.5.2. GDPR and international privacy laws impact on U.S. players

USA Video Surveillance Market Segmentation

4.1. By Offering (In Value %)

4.1.1. Hardware (Cameras, storage devices)

4.1.2. Software (Video management systems, analytics)

4.1.3. Services (Installation, maintenance, cloud storage)

4.2. By System Type (In Value %)

4.2.1. Analog Video Surveillance Systems

4.2.2. IP Video Surveillance Systems

4.2.3. Hybrid Video Surveillance Systems

4.3. By Application (In Value %)

4.3.1. Commercial

4.3.2. Residential

4.3.3. Infrastructure and Government Facilities

4.3.4. Transportation

4.3.5. Military & Defense

4.4. By Region (In Value %)

4.4.1. North

4.4.2. South

4.4.3. East

4.4.4. West

USA Video Surveillance Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Hikvision Digital Technology Co. Ltd

5.1.2. Dahua Technology Co. Ltd

5.1.3. Bosch Security Systems

5.1.4. Axis Communications AB (Canon)

5.1.5. Hanwha Techwin

5.1.6. Honeywell International Inc.

5.1.7. Avigilon Corporation

5.1.8. Panasonic Corporation

5.1.9. FLIR Systems Inc.

5.1.10. Cisco Systems Inc.

5.1.11. NEC Corporation

5.1.12. Allied Telesis Inc.

5.1.13. CP Plus International

5.1.14. Palantir Technologies

5.1.15. Genetec Inc.

5.2. Cross Comparison Parameters (Revenue, R&D spend, Market share, Technological expertise, Installed base, Employee size, Product portfolio, Global presence)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Mergers & Acquisitions, Partnerships, Product launches)

USA Video Surveillance Market Future Size (In USD Bn)

6.1. Future Market Size Projections

6.2. Key Factors Driving Future Market Growth

USA Video Surveillance Future Market Segmentation

7.1. By Offering (In Value %)

7.2. By System Type (In Value %)

7.3. By Application (In Value %)

7.4. By Region (In Value %)

USA Video Surveillance Market Analysts' Recommendations

8.1. Technology adoption recommendations (AI, cloud services)

8.2. Growth opportunities in underpenetrated sectors (Education, Healthcare)

8.3. Regulatory compliance insights for market players

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the USA Video Surveillance Market. This step includes extensive desk research using a combination of secondary and proprietary databases to identify key variables, such as market drivers, regulatory environments, and technological trends.

Step 2: Market Analysis and Construction

This phase focuses on analyzing historical data pertaining to the USA Video Surveillance Market, including market penetration rates, system preferences, and the adoption of new technologies. The objective is to map out revenue estimates and future projections by analyzing market trends.

Step 3: Hypothesis Validation and Expert Consultation

Through consultation with industry experts, we validate our hypotheses using computer-assisted telephone interviews (CATIs) to gather operational and financial insights. These inputs help refine our analysis, ensuring it aligns with industry realities.

Step 4: Research Synthesis and Final Output

In this final phase, we engage with video surveillance hardware manufacturers and service providers to collect specific data points on consumer preferences, product sales, and technological innovations. This ensures our analysis is comprehensive and accurately reflects market dynamics.

Frequently Asked Questions

01. How big is the USA Video Surveillance Market?

The USA Video Surveillance Market is valued at USD 15 billion, driven by growing public safety concerns, adoption of IP-based systems, and smart city initiatives.

02. What are the challenges in the USA Video Surveillance Market?

The key challenges in the USA Video Surveillance Market include privacy concerns, high storage requirements for high-definition video, and cybersecurity threats associated with connected systems.

03. Who are the major players in the USA Video Surveillance Market?

Major players in the USA Video Surveillance Market include Hikvision, Dahua Technology, Bosch Security Systems, Axis Communications, and Honeywell International Inc., dominating due to advanced technologies and broad market reach.

04. What are the growth drivers of the USA Video Surveillance Market?

Growth in the USA Video Surveillance Market is propelled by increased adoption of IP-based cameras, advances in AI-driven analytics, and government investments in public security infrastructure.

05. What are the emerging trends in the USA Video Surveillance Market?

Key trends in the USA Video Surveillance Market include the rise of Video Surveillance-as-a-Service (VSaaS), cloud-based storage, and integration of surveillance systems with IoT and smart city technologies.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.