Vietnam Consumer Electronics Market Outlook to 2030

Region:Asia

Author(s):Sanjeev

Product Code:KROD4670

October 2024

90

About the Report

Vietnam Consumer Electronics Market Overview

-

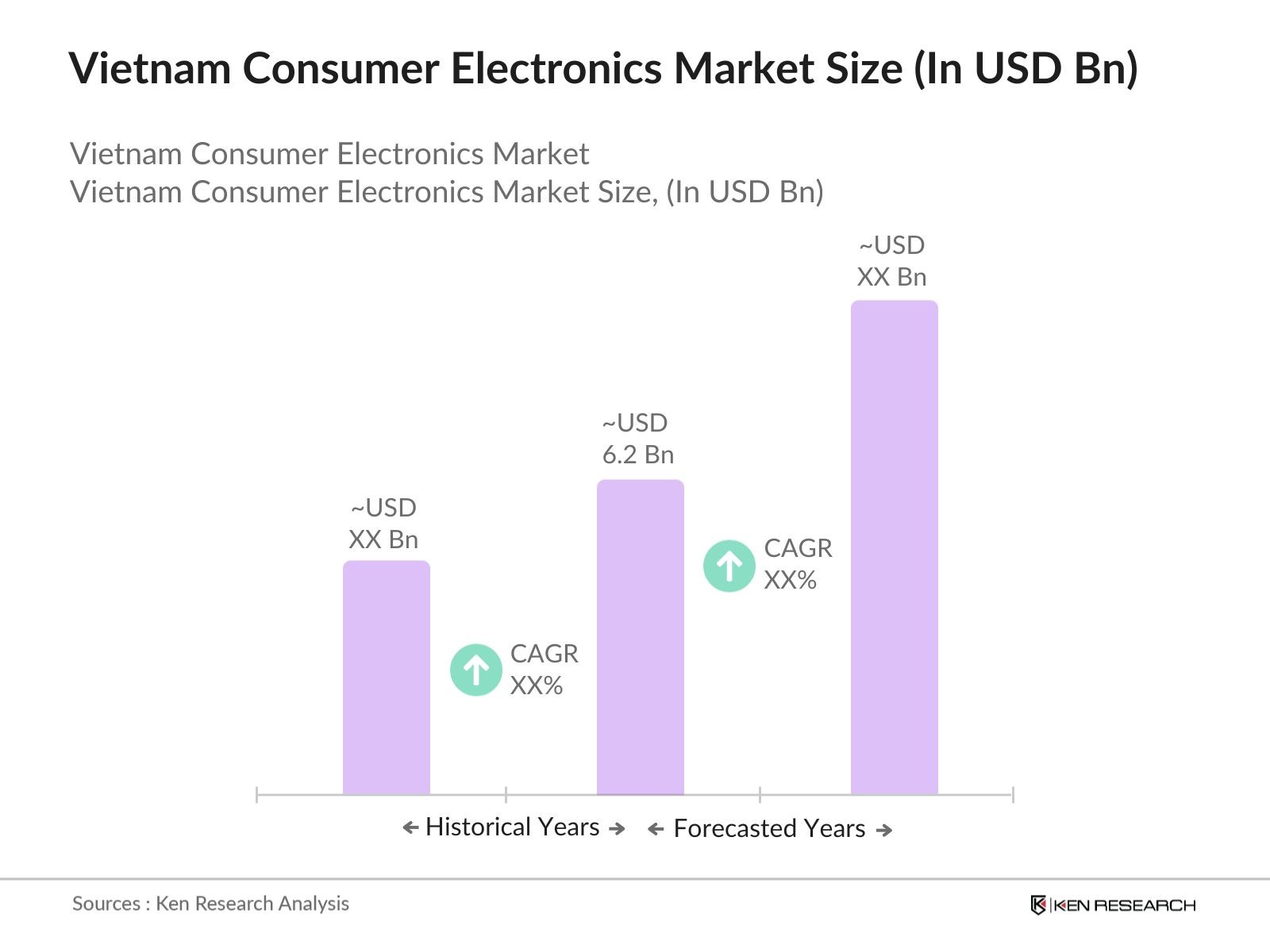

The Vietnam consumer electronics market is valued at USD 6.2 billion. This figure is driven primarily by increased disposable income, urbanization, and strong demand for smartphones, smart home devices, and laptops. E-commerce has been pivotal, enabling easier access to these electronics, especially in urban areas. Government initiatives focused on technology advancement and digital transformation have also played a crucial role in accelerating market growth. Furthermore, the expanding middle-class population in Vietnam has amplified demand for high-tech consumer goods, contributing significantly to the market size.

-

Ho Chi Minh City and Hanoi lead the Vietnamese consumer electronics market. These cities have strong digital infrastructures, higher consumer spending power, and greater access to international brands. The urban population in these regions is highly tech-savvy, with substantial interest in smart home technologies and personal electronics, making them the key consumption hubs. The dominance of these cities is attributed to their role as economic centers, where consumer spending on electronics outpaces rural areas due to higher income levels and access to modern retail channels.

-

National digital transformation programs Vietnam's National Digital Transformation Program is a government initiative aimed at fostering the development of a digital economy. By 2023, the government had invested over USD 400 million in programs targeting the digital transformation of various industries, including consumer electronics. This includes incentives for the adoption of digital platforms and technologies, thereby boosting demand for tech products.

Vietnam Consumer Electronics Market Segmentation

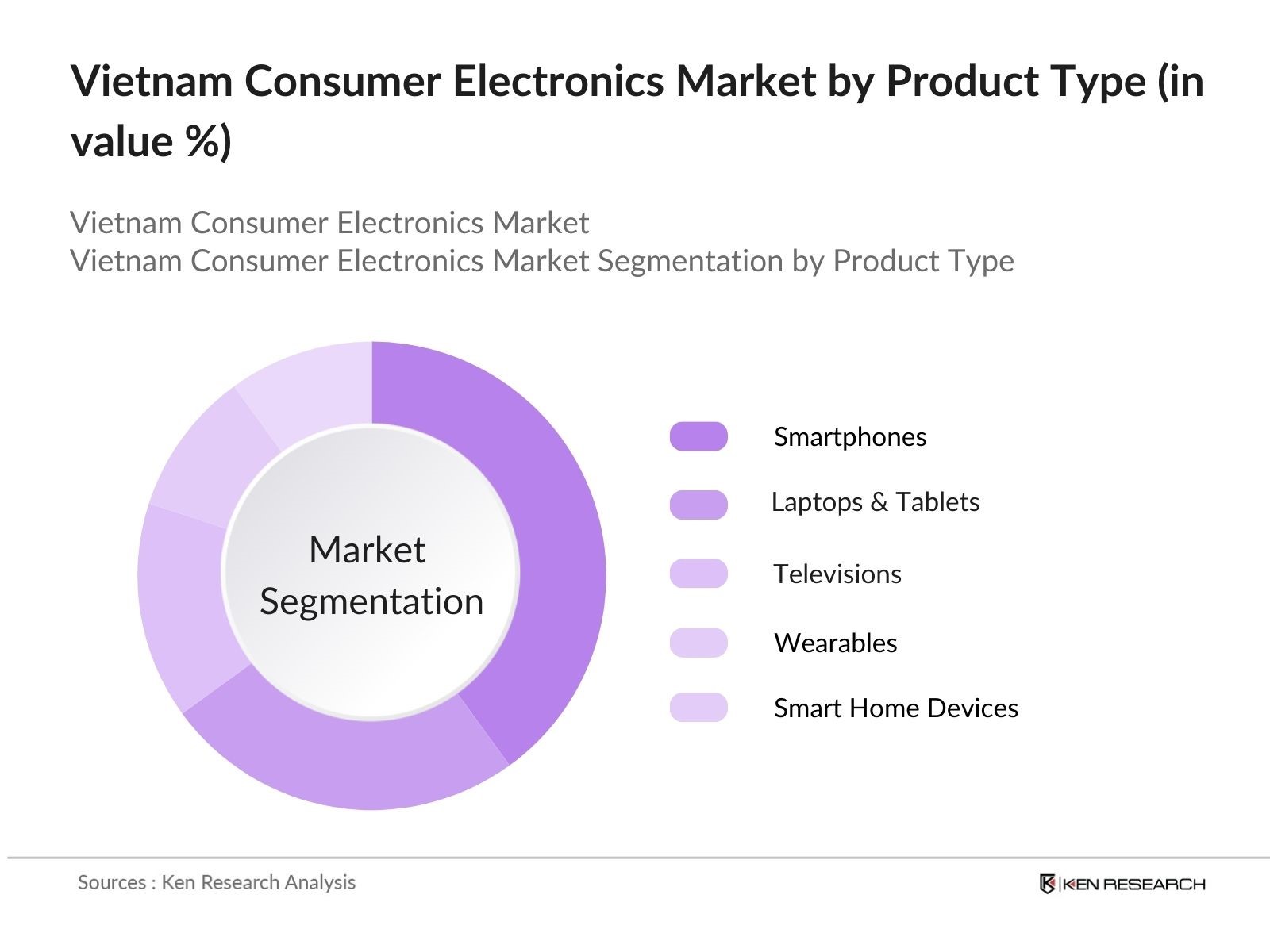

- By Product Type: The market is segmented by product type into smartphones, laptops & tablets, televisions, wearables, and smart home devices. Among these, smartphones currently dominate the market share, driven by the increasing consumer preference for internet connectivity and multifunctional devices. Brands like Samsung, Apple, and Xiaomi have significant brand loyalty, helping maintain dominance in this category. The growing availability of affordable smartphones has also boosted demand, especially among younger consumers who use them for social media, entertainment, and mobile gaming.

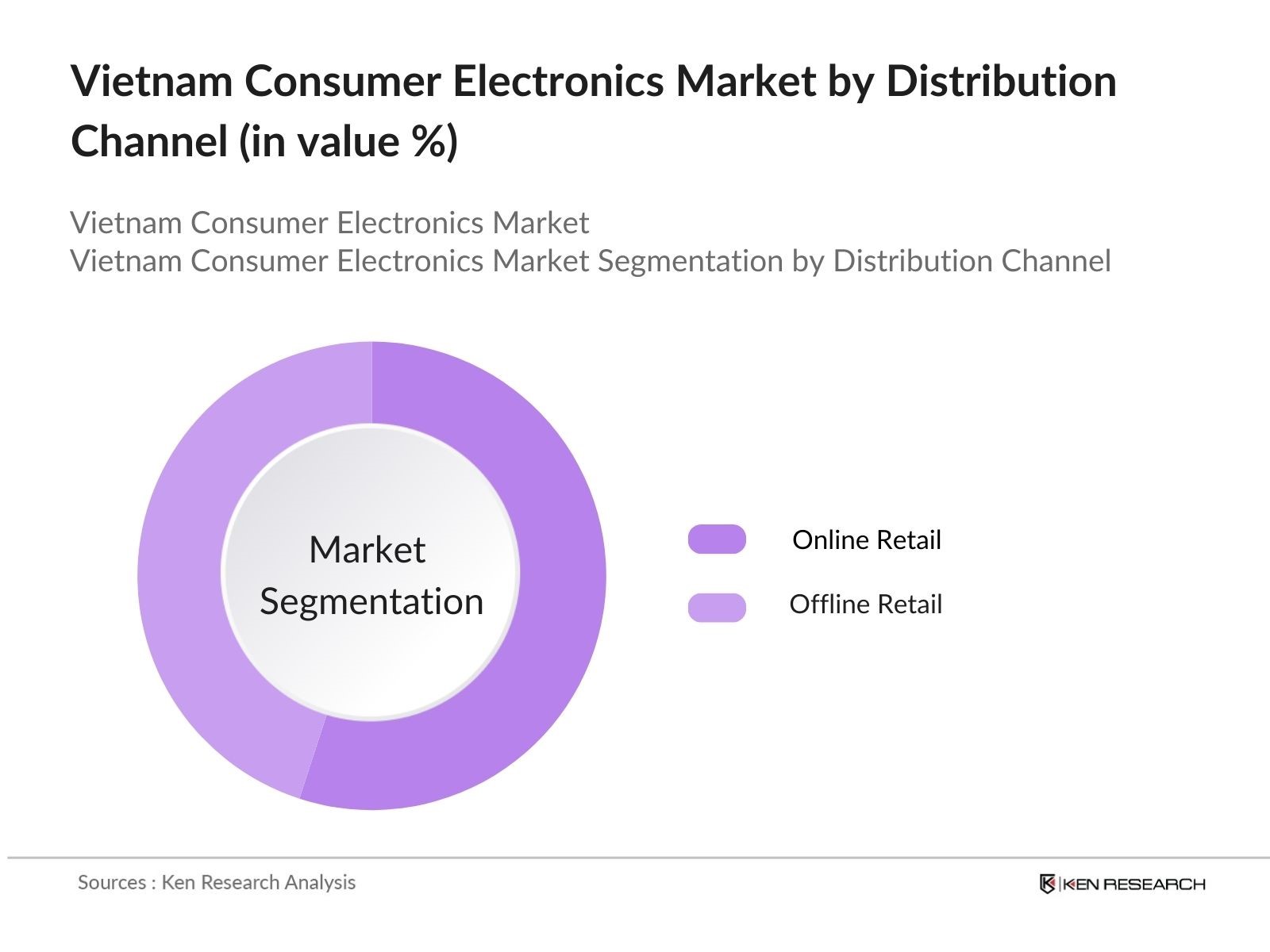

- By Distribution Channel: In terms of distribution channels, the market is divided into online retail and offline retail. Online retail holds the dominant market share due to the convenience and accessibility it offers to consumers. The rise of major e-commerce platforms such as Shopee, Lazada, and Tiki has made online shopping more convenient and affordable. The online channel also appeals to tech-savvy younger generations, who prefer purchasing gadgets through mobile apps. Offline retail remains important, especially for older generations, but online channels are becoming the preferred mode due to wide product variety and competitive pricing.

Vietnam Consumer Electronics Market Competitive Landscape

The Vietnam consumer electronics market is highly competitive, with a mix of local and international players. Key companies dominate the market by offering a wide range of products, cutting-edge technology, and extensive distribution networks. These players have a significant influence over market trends and consumer preferences. The Vietnam consumer electronics market is dominated by global giants such as Samsung, Apple, and LG, alongside emerging local players like VinSmart. These companies maintain their dominance by continuously innovating and releasing products that resonate with consumer needs, such as 5G-enabled smartphones and smart home devices. Their strong presence in both offline and online retail channels further reinforces their market leadership.

|

Company |

Established |

Headquarters |

Product Range |

Revenue (2023) |

No. of Employees |

Global Reach |

Local Market Share |

Distribution Network |

|

Samsung |

1938 |

South Korea |

- |

- |

- |

- |

- |

- |

|

Apple |

1976 |

USA |

- |

- |

- |

- |

- |

- |

|

LG |

1947 |

South Korea |

- |

- |

- |

- |

- |

- |

|

VinSmart |

2018 |

Vietnam |

- |

- |

- |

- |

- |

- |

|

Xiaomi |

2010 |

China |

- |

- |

- |

- |

- |

- |

Vietnam Consumer Electronics Industry Analysis

Market Growth Drivers

-

Consumer demand for smart home devices: The demand for smart home devices in Vietnam is rising, with the country's urban population projected to grow to 44 million by 2025. This urbanization, combined with a tech-savvy middle class, has fueled demand for smart products such as smart speakers, thermostats, and security systems. As of 2023, Vietnam’s household internet penetration reached over 75%, fostering the adoption of smart home solutions. The Vietnamese government’s digital transformation plan has accelerated the adoption of digital devices within households, driving further market growth.

-

Government support for digital transformation: Vietnam’s government has shown strong support for digital transformation through initiatives such as the National Digital Transformation Program. The plan targets a fully digital government by 2030, further accelerating electronics demand, including computers, smartphones, and digital services. The government has allocated over USD 434 million to digital transformation projects in 2023, enhancing the development and integration of technology in both public and private sectors.

-

Increasing urbanization and tech-savvy population: By 2023, around 37.6% of Vietnam's population lived in urban areas, a figure expected to increase to 45% by 2030. With urbanization, a tech-savvy younger generation is driving the demand for consumer electronics. The median age in Vietnam is 32, with increasing disposable income contributing to tech product purchases.

Market Challenges

-

Logistics and supply chain inefficiencies: Vietnam’s logistics infrastructure faces significant challenges, with inadequate road networks and port congestion affecting the efficiency of supply chains. In 2023, logistics costs represented about 20% of the national GDP, higher than in neighboring countries. These inefficiencies impact the cost of consumer electronics, contributing to higher prices and delays in product availability.

-

High penetration of counterfeit electronics: Vietnam has struggled with counterfeit electronics, which accounted for up to 20% of all electronic goods sold in 2022. This presence of fake products not only harms legitimate businesses but also undermines consumer trust in brands. Efforts by the government to curb this include stricter border controls and intellectual property laws, but enforcement remains inconsistent.

Vietnam Consumer Electronics Market Future Outlook

Over the next five years, the Vietnam consumer electronics market is expected to witness substantial growth driven by rising disposable incomes, the rapid adoption of smart home devices, and 5G technology penetration. As consumers become more tech-savvy, demand for AI-integrated devices and high-performance gadgets will increase. Additionally, e-commerce growth will further expand product accessibility, particularly in rural areas where offline retail is limited.

Fututre Market Opportunities

- Expansion of smart home products’ :The demand for smart home products continues to grow, with over 2 million households using at least one smart home device by 2023. The increasing affordability of these devices, coupled with rising consumer awareness, creates opportunities for further growth. The expansion of IoT networks and government-backed digital infrastructure projects are expected to facilitate the proliferation of these products.

- Adoption of 5G-enabled devices: Vietnam launched commercial 5G services in 2022, and by mid-2023, 5G coverage reached 10 major cities. The adoption of 5G devices is expected to increase sharply as the country aims to cover 25% of the population with 5G networks by 2025. The uptake of 5G smartphones and other connected devices presents an opportunity for consumer electronics manufacturers to introduce a new generation of high-speed devices.

Scope of the Report

|

By Product Type |

Smartphones Laptops and Tablets Televisions Wearables Smart Home Devices |

|

By Distribution Channel |

Online Retail Offline Retail |

|

By End-User |

Individual Consumers Commercial, Industrial |

|

By Technology |

5G Enabled Devices Wi-Fi 6 Compatible Devices AI-Powered Devices IoT-Integrated Devices |

|

By Region |

North East West South |

Products

Key Target Audience

- Consumer Electronics Manufacturers

- E-commerce Platforms

- Retail Chains (Big C, VinMart)

- Banks and FInancial Institutes

- Government and Regulatory Bodies (Ministry of Industry and Trade, Vietnam Electronics and Informatics Corporation)

- Telecommunications Providers (Viettel, VNPT)

- Investments and Venture Capitalist Firms

- Tech Startups and Innovators

- Smart Home Technology Developers

Companies

Major Players in the Vietnam Consumer Electronics Market

- Samsung Electronics

- Apple Inc.

- LG Electronics

- VinSmart

- Xiaomi Corporation

- Oppo

- Panasonic Corporation

- Sony Corporation

- Asus

- Dell Technologies

- HP Inc.

- Huawei Technologies

- TCL Electronics

- Lenovo Group Ltd.

- Canon Inc.

Table of Contents

Vietnam Consumer Electronics Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

Vietnam Consumer Electronics Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

Vietnam Consumer Electronics Market Analysis

3.1. Growth Drivers (e.g., Rising Disposable Income, Increasing Tech Adoption, E-Commerce Growth, Government Policies)

3.1.1. Consumer demand for smart home devices

3.1.2. Government support for digital transformation

3.1.3. Increasing urbanization and tech-savvy population

3.1.4. E-commerce platforms driving online sales

3.2. Market Challenges (e.g., Supply Chain Disruptions, Counterfeit Products, Pricing Competition)

3.2.1. Logistics and supply chain inefficiencies

3.2.2. High penetration of counterfeit electronics

3.2.3. Intense price competition among brands

3.3. Opportunities (e.g., 5G Rollout, Internet of Things, Smart Cities Initiatives)

3.3.1. Expansion of smart home products

3.3.2. Adoption of 5G-enabled devices

3.3.3. Opportunities in rural electrification

3.4. Trends (e.g., Consumer Shift to Smart Devices, Wearables, High-Performance Laptops)

3.4.1. Rise of wearable electronics

3.4.2. Growing demand for high-performance gaming laptops

3.4.3. Integration of voice assistants in consumer electronics

3.5. Government Regulation (e.g., Import Tariffs, Local Manufacturing Incentives, E-waste Management)

3.5.1. National digital transformation programs

3.5.2. Import and export tariffs on electronics

3.5.3. Government incentives for local manufacturing

3.5.4. E-waste management regulations

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porter’s Five Forces Analysis

3.9. Competition Ecosystem

Vietnam Consumer Electronics Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Smartphones

4.1.2. Laptops and Tablets

4.1.3. Televisions

4.1.4. Wearables (Smartwatches, Fitness Trackers)

4.1.5. Smart Home Devices (Smart Speakers, Cameras, Thermostats)

4.2. By Distribution Channel (In Value %)

4.2.1. Online Retail

4.2.2. Offline Retail (Specialty Stores, Supermarkets, Hypermarkets)

4.3. By End-User (In Value %)

4.3.1. Individual Consumers

4.3.2. Commercial (Business, Offices, Educational Institutions)

4.3.3. Industrial (Factories, Warehouses)

4.4. By Technology (In Value %)

4.4.1. 5G Enabled Devices

4.4.2. Wi-Fi 6 Compatible Devices

4.4.3. AI-Powered Devices

4.4.4. IoT-Integrated Devices

4.5. By Region (In Value %)

4.5.1. North

4.5.2. South

4.5.3. East

4.5.4. West

Vietnam Consumer Electronics Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Samsung Electronics

5.1.2. LG Electronics

5.1.3. Apple Inc.

5.1.4. Sony Corporation

5.1.5. Xiaomi Corporation

5.1.6. Panasonic Corporation

5.1.7. Oppo

5.1.8. Asus

5.1.9. Dell Technologies

5.1.10. HP Inc.

5.1.11. Huawei Technologies

5.1.12. Vsmart (VinSmart)

5.1.13. TCL Electronics

5.1.14. Lenovo Group Ltd.

5.1.15. Canon Inc.

5.2. Cross Comparison Parameters (Market Share, Distribution Networks, Product Portfolio, Market Penetration)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

Vietnam Consumer Electronics Market Regulatory Framework

6.1. Local Manufacturing Regulations

6.2. Import and Export Tariff Policies

6.3. Certifications and Standards Compliance

Vietnam Consumer Electronics Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

Vietnam Consumer Electronics Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By End-User (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

Vietnam Consumer Electronics Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Cohort Analysis

9.3. Market Entry Strategies

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

In the first stage, an in-depth ecosystem map of the Vietnam Consumer Electronics Market was developed. This stage included desk research from government databases, trade reports, and secondary sources, identifying major market drivers, consumer behaviors, and product trends.

Step 2: Market Analysis and Construction

This phase compiled historical data on market penetration, distribution channels, and revenue generation within the Vietnam Consumer Electronics Market. Data from online sales trends and physical retail performance was analyzed to determine the distribution shift.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were formulated and validated through direct interviews with experts from leading electronics companies. These consultations allowed insights into emerging product categories, technological innovation, and consumer preferences.

Step 4: Research Synthesis and Final Output

The final synthesis involved engaging with electronics manufacturers to understand specific product segments' performance, ensuring the accuracy of market forecasts. These engagements ensured a comprehensive and data-backed report.

Frequently Asked Questions

01. How big is the Vietnam Consumer Electronics Market?

The Vietnam consumer electronics market is valued at USD 6.2 billion, driven by rising urbanization, increasing internet penetration, and the growing demand for smartphones and smart home devices.

02. What are the challenges in the Vietnam Consumer Electronics Market?

Challenges include the presence of counterfeit products, pricing competition, and supply chain inefficiencies, particularly in rural areas where logistics and distribution face limitations.

03. Who are the major players in the Vietnam Consumer Electronics Market?

Major players include Samsung Electronics, Apple, LG, VinSmart, and Xiaomi. These companies dominate the market due to their strong brand presence, innovation in product offerings, and wide distribution networks.

04. What are the growth drivers of the Vietnam Consumer Electronics Market?

The market is propelled by increasing disposable incomes, technological advancements in AI and 5G, and the expansion of e-commerce platforms, which facilitate easier access to consumer electronics.

05. What trends are shaping the Vietnam Consumer Electronics Market?

Key trends include the growing adoption of smart home devices, the rise of 5G-enabled smartphones, and the increasing popularity of wearable devices such as fitness trackers and smartwatches.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.