Vietnam Diabetes Care Drugs Market Outlook to 2030

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD5667

November 2024

83

About the Report

Vietnam Diabetes Care Drugs Market Overview

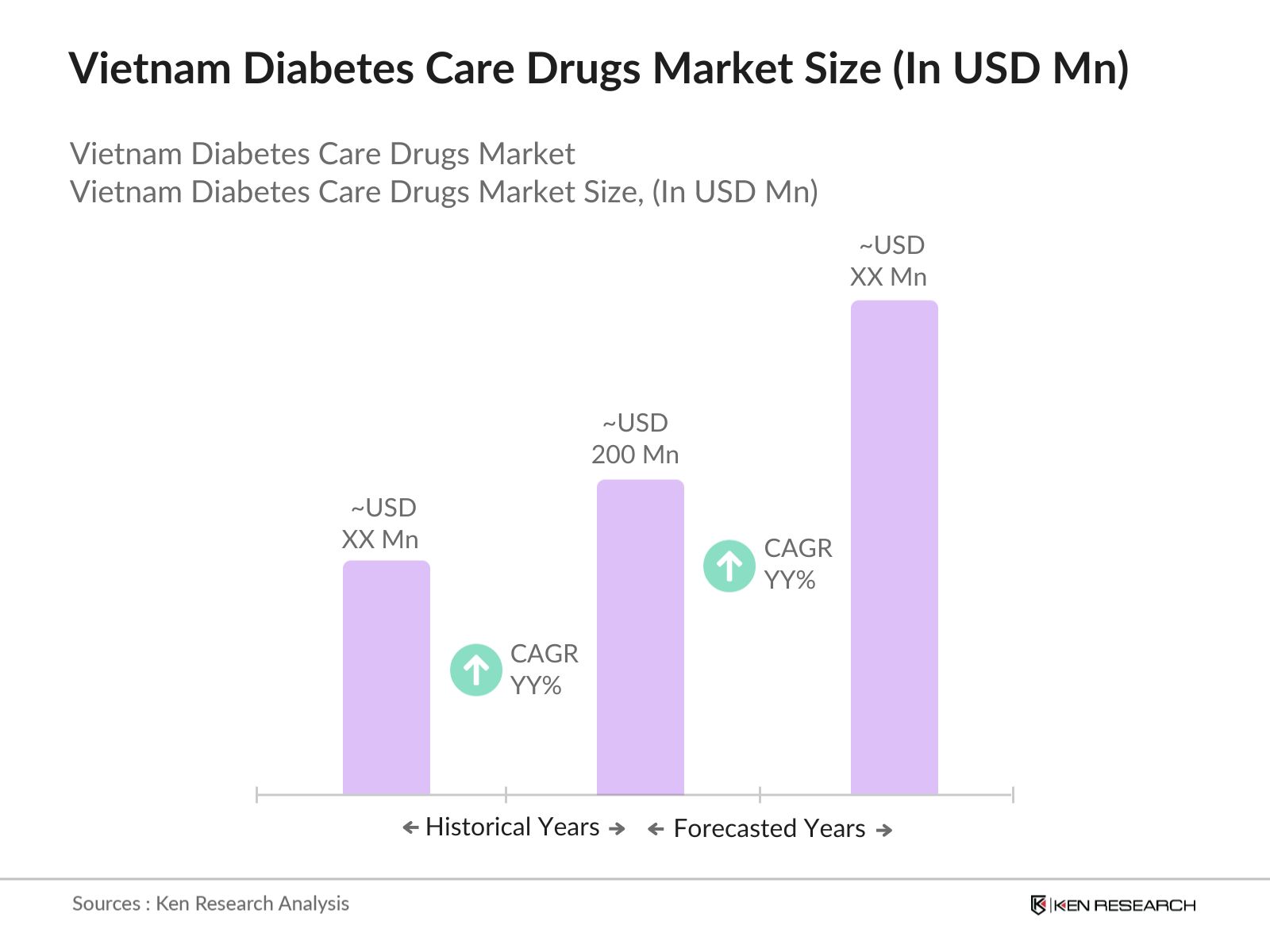

- The Vietnam Diabetes Care Drugs Market is valued at USD 200 million, based on a five-year historical analysis. This market is primarily driven by the rising prevalence of diabetes in both urban and rural populations, increased healthcare expenditure, and the governments efforts to enhance diabetes care. The country has seen a surge in demand for both insulin and oral anti-diabetic drugs, particularly with the growing availability of biosimilar drugs that help meet the demand in low-income groups.

- In terms of geographic dominance, major cities like Ho Chi Minh City and Hanoi lead the market due to their well-established healthcare infrastructure, higher urbanization rates, and better access to modern healthcare services. Additionally, these cities have a higher concentration of diabetes centers and healthcare professionals, allowing for better diagnosis and treatment of diabetes compared to rural areas.

- The Vietnamese government has implemented the National Diabetes Program, which, by 2024, has screened over 10 million individuals for diabetes and pre-diabetes. This initiative has led to earlier diagnosis and a higher number of patients receiving timely medication, thus driving demand for diabetes care drugs. The program also includes public health campaigns aimed at increasing awareness of diabetes management, further boosting market growth.

Vietnam Diabetes Care Drugs Market Segmentation

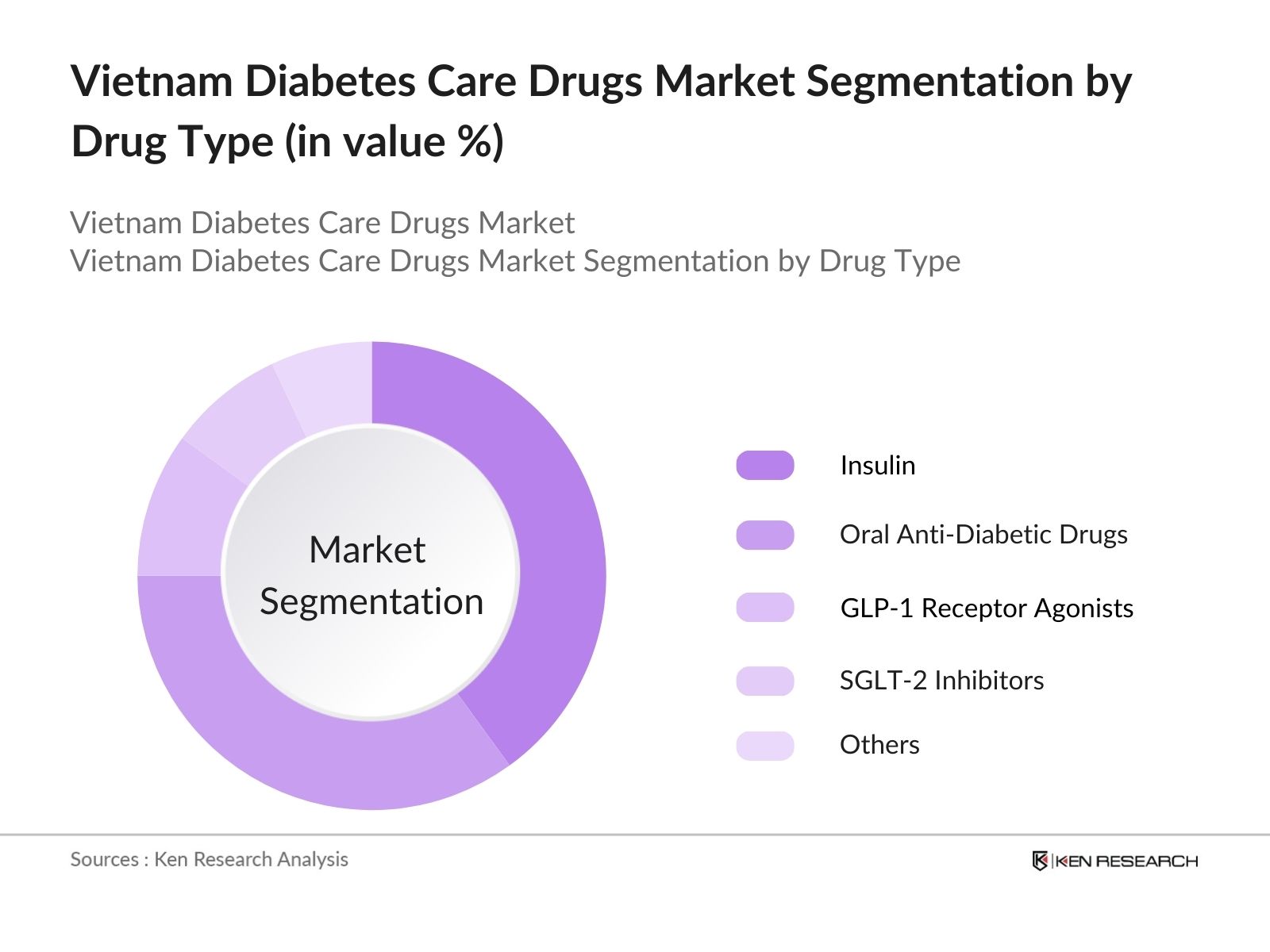

By Drug Type: The market is segmented by drug type into insulin, oral anti-diabetic drugs, GLP-1 receptor agonists, SGLT-2 inhibitors, and others (including alpha-glucosidase inhibitors and amylinomimetics). Insulin currently holds the dominant market share due to its widespread necessity for type 1 diabetic patients and its increasing use in type 2 diabetes patients who fail to control blood sugar with oral medications alone. Furthermore, advancements in insulin delivery methods, such as prefilled insulin pens and insulin pumps, have made it easier for patients to administer their doses, contributing to the dominance of this sub-segment.

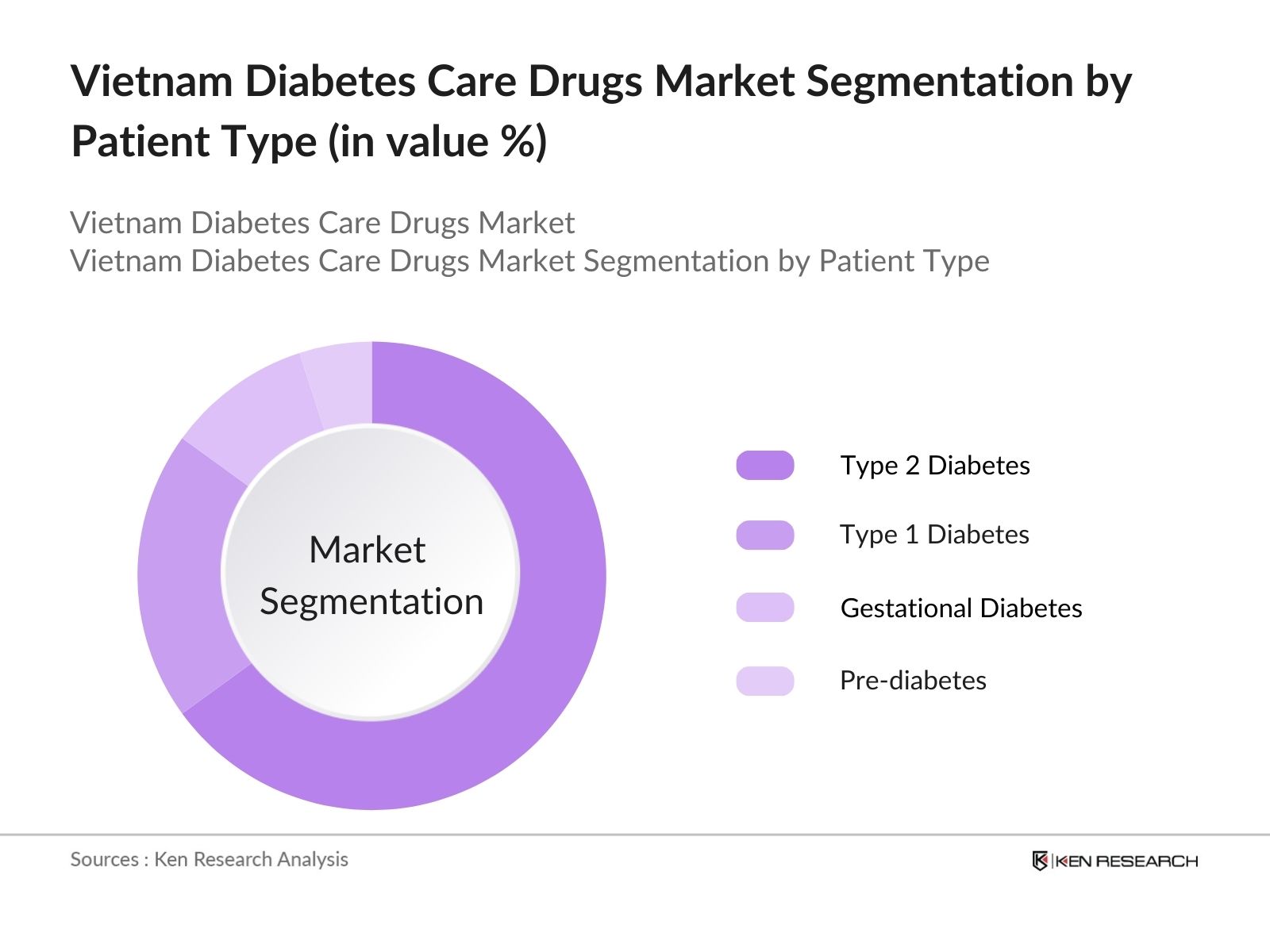

By Patient Type: The market is also segmented by patient type, which includes Type 1 diabetes, Type 2 diabetes, gestational diabetes, and pre-diabetes. Type 2 diabetes represents the largest share of the market due to the growing aging population, unhealthy dietary patterns, and a rise in sedentary lifestyles in urban areas. Moreover, government campaigns aimed at diabetes awareness and early diagnosis have further elevated the number of diagnosed Type 2 diabetic patients, boosting the demand for anti-diabetic drugs in this sub-segment.

Vietnam Diabetes Care Drugs Market Competitive Landscape

The market is dominated by key global and local players who have a influence on market dynamics. The market sees a high level of consolidation, with several major companies like Sanofi, Novo Nordisk, and Eli Lilly having a large presence in insulin and other diabetes care drugs. Additionally, local manufacturers like Vinphaco are also playing a pivotal role in catering to domestic demand, especially in rural areas where affordability is a concern.

|

Company |

Establishment Year |

Headquarters |

Revenue |

No. of Products |

R&D Investment |

Market Penetration |

Distribution Network |

Strategic Partnerships |

Key Therapeutic Areas |

|

Sanofi |

1973 |

Paris, France |

|||||||

|

Novo Nordisk |

1923 |

Bagsvrd, Denmark |

|||||||

|

Eli Lilly |

1876 |

Indianapolis, USA |

|||||||

|

Merck & Co. |

1891 |

Kenilworth, USA |

|||||||

|

Vinphaco |

1958 |

Phu Tho, Vietnam |

Vietnam Diabetes Care Drugs Market Analysis

Market Growth Drivers

- Rising Prevalence of Diabetes in Vietnam: Vietnam has been witnessing an alarming rise in the number of diabetes cases, with over 5.4 million individuals diagnosed in 2024. This has led to an increasing demand for diabetes care drugs in the country. According to government health records, the diabetic population in Vietnam has been growing steadily, driven by changing lifestyles and dietary habits, particularly in urban areas. These factors are directly contributing to higher drug consumption for diabetes management.

- Government Policies Supporting Diabetes Treatment: The Vietnamese government, through the Ministry of Health, has introduced various diabetes management programs aimed at improving the accessibility and affordability of diabetes care drugs. By 2024, over 800,000 individuals are benefiting from government-funded initiatives that subsidize insulin and other diabetes-related medications. These initiatives focus on both prevention and treatment, contributing to market growth by making essential drugs more affordable and widely available.

- Growing Demand for Advanced Treatment Options: The demand for newer, more advanced diabetes medications, such as GLP-1 receptor agonists and SGLT2 inhibitors, has been rising. In 2024, an estimated 1.2 million Vietnamese patients have shifted to advanced treatment options, seeking better glycemic control and fewer side effects. This growing preference for innovative drugs has resulted in increased sales of branded diabetes medications in Vietnam.

Market Challenges

- Limited Access to Healthcare in Rural Areas: Vietnam's rural population, which accounts for approximately 60 million people in 2024, continues to face limited access to healthcare facilities and diabetes medications. Many rural areas lack sufficient healthcare infrastructure, resulting in delayed diagnosis and inadequate treatment of diabetes. This urban-rural healthcare gap hinders the market growth for diabetes care drugs, as a large portion of the population remains underserved.

- Low Awareness of Diabetes Management: Despite the increasing prevalence of diabetes, awareness of proper diabetes management remains low in Vietnam. Surveys conducted in 2024 indicate that nearly 35% of diabetic patients in rural areas are unaware of proper treatment protocols, leading to underutilization of prescribed drugs. This lack of awareness limits the demand for diabetes care drugs, as many patients remain untreated or are not compliant with their medication regimens.

Vietnam Diabetes Care Drugs Market Future Outlook

The Vietnam Diabetes Care Drugs industry is expected to experience substantial growth over the next five years, driven by the continuous rise in diabetes prevalence, technological advancements in drug delivery methods, and expanding government programs aimed at improving public health.

Future Market Opportunities

- Increased Adoption of Personalized Diabetes Care: Over the next five years, Vietnam is expected to see a shift toward personalized diabetes care, with more than 2 million patients projected to adopt tailored treatment plans by 2029. This trend will drive the demand for advanced diabetes medications, as patients seek more individualized solutions to manage their condition effectively.

- Expansion of Biosimilar Insulin Availability: Biosimilar insulin products are expected to gain widespread acceptance in Vietnam by 2029, with the number of patients using biosimilar insulins projected to surpass 800,000. These more affordable alternatives will reduce the cost burden on patients and the healthcare system, driving growth in the diabetes care drugs market.

Scope of the Report

|

Drug Type |

Insulin Oral Anti-diabetic Drugs GLP-1 Agonists SGLT-2 Inhibitors Others |

|

Patient Type |

Type 1 Diabetes Type 2 Diabetes Gestational Diabetes Pre-diabetes |

|

Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Pharmacies Clinics |

|

Region |

North East West South |

|

Drug Formulation |

Tablets Injectable Capsules Oral Liquids |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Pharmaceuticals manufacturers and suppliers

Banks and Financial Institution

Government and regulatory bodies (Ministry of Health, Vietnam Social Security)

Health insurance providers

Private Equity Firms

Healthcare Companies

Companies

Players Mentioned in the Report:

Sanofi

Novo Nordisk

Eli Lilly

Merck & Co.

AstraZeneca

Pfizer

Boehringer Ingelheim

Takeda Pharmaceuticals

Novartis

Bayer AG

Cipla

Glenmark Pharmaceuticals

Biocon

Sun Pharma

Abbott Laboratories

Table of Contents

1. Vietnam Diabetes Care Drugs Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Vietnam Diabetes Care Drugs Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Vietnam Diabetes Care Drugs Market Analysis

3.1. Growth Drivers

3.1.1. Rising Diabetes Prevalence (Type 1, Type 2, Gestational Diabetes)

3.1.2. Increased Healthcare Expenditure

3.1.3. Expanding Government Health Programs (e.g., National Target Program on Diabetes)

3.1.4. Growing Awareness of Diabetes Management

3.2. Market Challenges

3.2.1. High Cost of Insulin Therapy

3.2.2. Lack of Healthcare Access in Rural Areas

3.2.3. Regulatory Barriers

3.3. Opportunities

3.3.1. Growth in Biosimilar Drugs

3.3.2. Introduction of Digital Health Solutions

3.3.3. Increasing Penetration of E-commerce Platforms for Drug Delivery

3.4. Trends

3.4.1. Shift Towards Combination Therapies

3.4.2. Adoption of Smart Insulin Pens and Continuous Glucose Monitoring Devices

3.4.3. Expansion of Telemedicine Services

3.5. Government Regulations

3.5.1. Ministry of Health Guidelines for Diabetes Drug Approval

3.5.2. Pricing Control Policies for Essential Drugs

3.5.3. Local Manufacturing Incentives for Pharmaceuticals

3.5.4. National Health Insurance Coverage for Diabetes Medications

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Vietnam Diabetes Care Drugs Market Segmentation

4.1. By Drug Type (In Value %)

4.1.1. Insulin

4.1.2. Oral Anti-diabetic Drugs (Metformin, Sulfonylureas, DPP-4 Inhibitors)

4.1.3. GLP-1 Receptor Agonists

4.1.4. SGLT-2 Inhibitors

4.1.5. Others (Amylinomimetics, Alpha-glucosidase Inhibitors)

4.2. By Patient Type (In Value %)

4.2.1. Type 1 Diabetes

4.2.2. Type 2 Diabetes

4.2.3. Gestational Diabetes

4.2.4. Pre-diabetes Patients

4.3. By Distribution Channel (In Value %)

4.3.1. Hospital Pharmacies

4.3.2. Retail Pharmacies

4.3.3. Online Pharmacies

4.3.4. Clinics

4.4. By Region (In Value %)

4.4.1. North

4.4.2. West

4.4.3. South

4.4.4. East

4.5. By Drug Formulation (In Value %)

4.5.1. Tablets

4.5.2. Injectable

4.5.3. Capsules

4.5.4. Oral Liquids

5. Vietnam Diabetes Care Drugs Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Sanofi

5.1.2. Novo Nordisk

5.1.3. Eli Lilly

5.1.4. Merck & Co.

5.1.5. AstraZeneca

5.1.6. Pfizer

5.1.7. Takeda Pharmaceuticals

5.1.8. Novartis

5.1.9. Boehringer Ingelheim

5.1.10. Bayer AG

5.1.11. Cipla

5.1.12. Glenmark Pharmaceuticals

5.1.13. Biocon

5.1.14. Sun Pharma

5.1.15. Abbott Laboratories

5.2. Cross Comparison Parameters (Revenue, Market Share, R&D Investment, Therapeutic Focus, Sales Volume, Drug Pipeline, Market Penetration, Strategic Alliances)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Vietnam Diabetes Care Drugs Market Regulatory Framework

6.1. Pharmaceutical Regulatory Approval Process

6.2. Pricing Control Regulations

6.3. Import and Export Restrictions on Drugs

6.4. GMP Certification Requirements

6.5. Pharmacovigilance Guidelines

7. Vietnam Diabetes Care Drugs Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Vietnam Diabetes Care Drugs Future Market Segmentation

8.1. By Drug Type (In Value %)

8.2. By Patient Type (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By Region (In Value %)

8.5. By Drug Formulation (In Value %)

9. Vietnam Diabetes Care Drugs Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first phase involves defining the key variables influencing the Vietnam Diabetes Care Drugs Market. This includes studying the roles of major stakeholders such as healthcare providers, drug manufacturers, and regulatory bodies. Information is gathered through secondary research and government health databases to provide a foundational understanding of the market.

Step 2: Market Analysis and Construction

In this phase, we analyze historical market trends to identify growth patterns and revenue streams. This includes evaluating the adoption rate of diabetes care drugs across different regions in Vietnam. Various sub-segments such as insulin and oral drugs are assessed in terms of market size and growth potential.

Step 3: Hypothesis Validation and Expert Consultation

Expert interviews are conducted using CATIs (computer-assisted telephone interviews) with industry specialists, healthcare professionals, and key players to validate market hypotheses. These consultations offer insights into operational efficiencies, drug adoption rates, and regional challenges in drug distribution.

Step 4: Research Synthesis and Final Output

In the final phase, the collected data is synthesized to produce a comprehensive market report. The findings from the expert consultations are corroborated with secondary research to ensure accuracy and reliability, providing stakeholders with a precise and validated market analysis.

Frequently Asked Questions

How big is the Vietnam Diabetes Care Drugs Market?

The Vietnam Diabetes Care Drugs Market is valued at USD 200 million, driven by a rising diabetes prevalence, expanding healthcare infrastructure, and government initiatives to improve public access to diabetes treatment.

What are the challenges in the Vietnam Diabetes Care Drugs Market?

Key challenges in the Vietnam Diabetes Care Drugs Market include high costs associated with advanced insulin therapies, regulatory hurdles for drug approvals, and inadequate access to healthcare in rural areas, which limits drug availability and diagnosis rates.

Who are the major players in the Vietnam Diabetes Care Drugs Market?

The major players in the Vietnam Diabetes Care Drugs Market include Sanofi, Novo Nordisk, Eli Lilly, Merck & Co., and AstraZeneca, all of which have extensive portfolios and strong market penetration in the diabetes care sector.

What are the growth drivers of the Vietnam Diabetes Care Drugs Market?

Growth in the Vietnam Diabetes Care Drugs Market is driven by the increasing incidence of diabetes, government health initiatives, and the introduction of innovative therapies like GLP-1 receptor agonists and SGLT-2 inhibitors, which offer superior glycemic control and patient compliance.

How is the Vietnam Diabetes Care Drugs Market expected to grow in the future?

The Vietnam Diabetes Care Drugs Market is expected to grow over the next five years due to the continuous rise in diabetes cases, improved healthcare access, and advancements in drug delivery systems such as smart insulin pens and continuous glucose monitors.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.