Vietnam Diagnostic Imaging Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD3410

November 2024

86

About the Report

Vietnam Diagnostic Imaging Market Overview

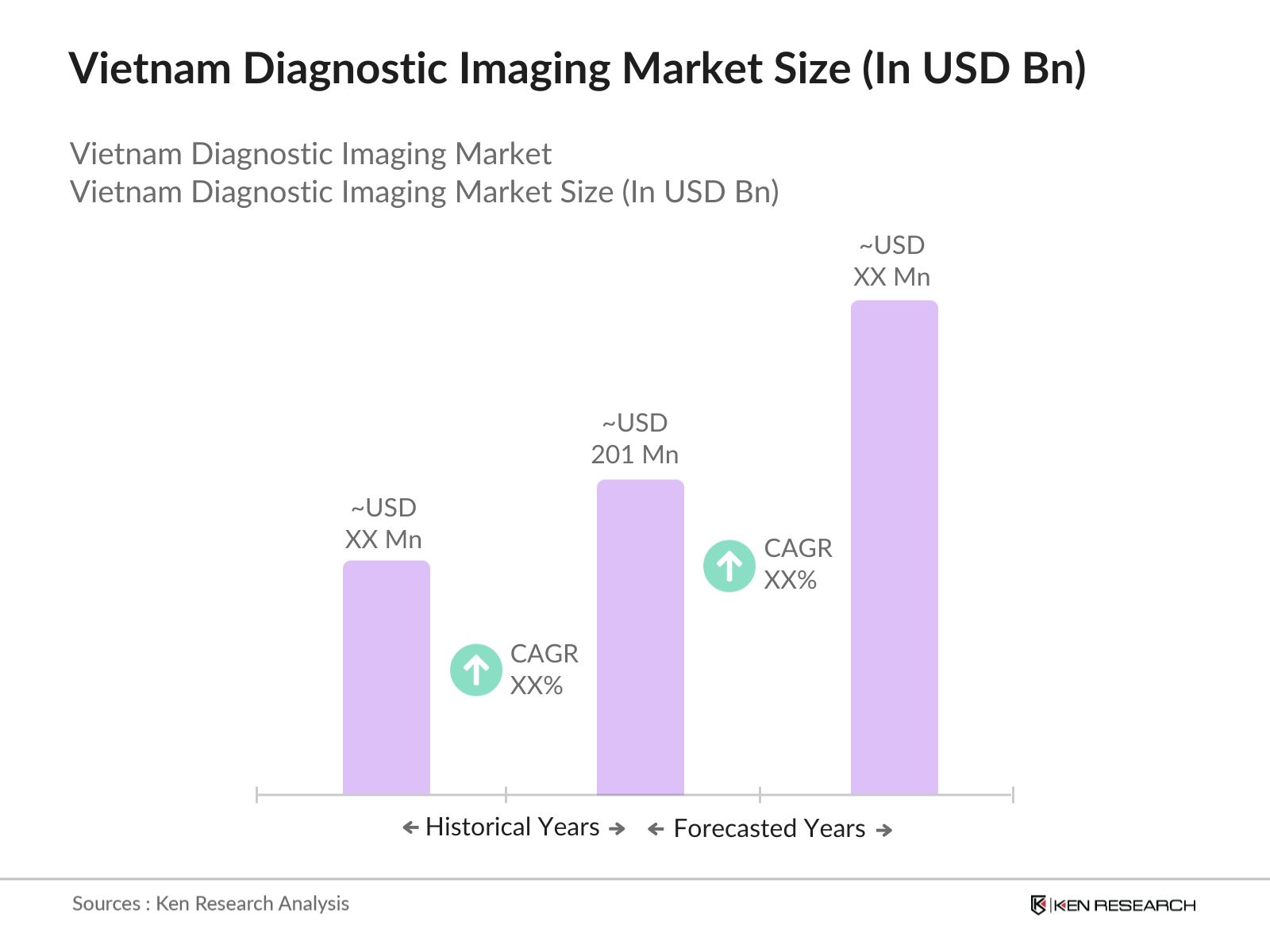

- The Vietnam Diagnostic Imaging market is valued at USD 201 million, based on a five-year historical analysis. This market is driven by the growing prevalence of chronic diseases, such as cancer and cardiovascular conditions, that require advanced diagnostic tools for early detection. The increasing demand for non-invasive procedures, coupled with rising healthcare expenditure, has further fueled the market's growth. Additionally, technological advancements in imaging systems, such as AI-based imaging solutions, are contributing to the rising adoption of diagnostic tools in hospitals and clinics across Vietnam.

- Ho Chi Minh City and Hanoi are dominant cities in the Vietnam Diagnostic Imaging market due to their advanced healthcare infrastructure, higher availability of specialized healthcare professionals, and large patient pool. The concentration of high-quality diagnostic centers and the presence of major hospitals in these cities has enabled them to lead the market. Both cities attract investments from the public and private sectors, further strengthening their role in Vietnam's healthcare industry.

- Vietnam's national health policies are actively supporting the expansion of diagnostic imaging services. Under the "National Strategy for Health Protection, Care, and Promotion," the government has allocated some fundings towards improving diagnostic services in public hospitals. As of 2023, $800 million was directed towards upgrading imaging facilities in provincial hospitals, with a focus on MRI and CT scan technologies. This policy aims to improve healthcare accessibility and reduce the diagnostic gap between urban and rural populations.

Vietnam Diagnostic Imaging Market Segmentation

By Modality: Vietnam's Diagnostic Imaging market is segmented by modality into X-ray Imaging, Computed Tomography (CT), Magnetic Resonance Imaging (MRI), Ultrasound Imaging, and Nuclear Imaging. In recent years, X-ray imaging has maintained a dominant market share under this segmentation due to its widespread use in diagnosing bone fractures, chest infections, and other conditions. X-ray machines are relatively affordable and can be found in most public hospitals and private clinics. Furthermore, the increasing focus on portable and digital X-ray systems has contributed to the continuous dominance of this segment.

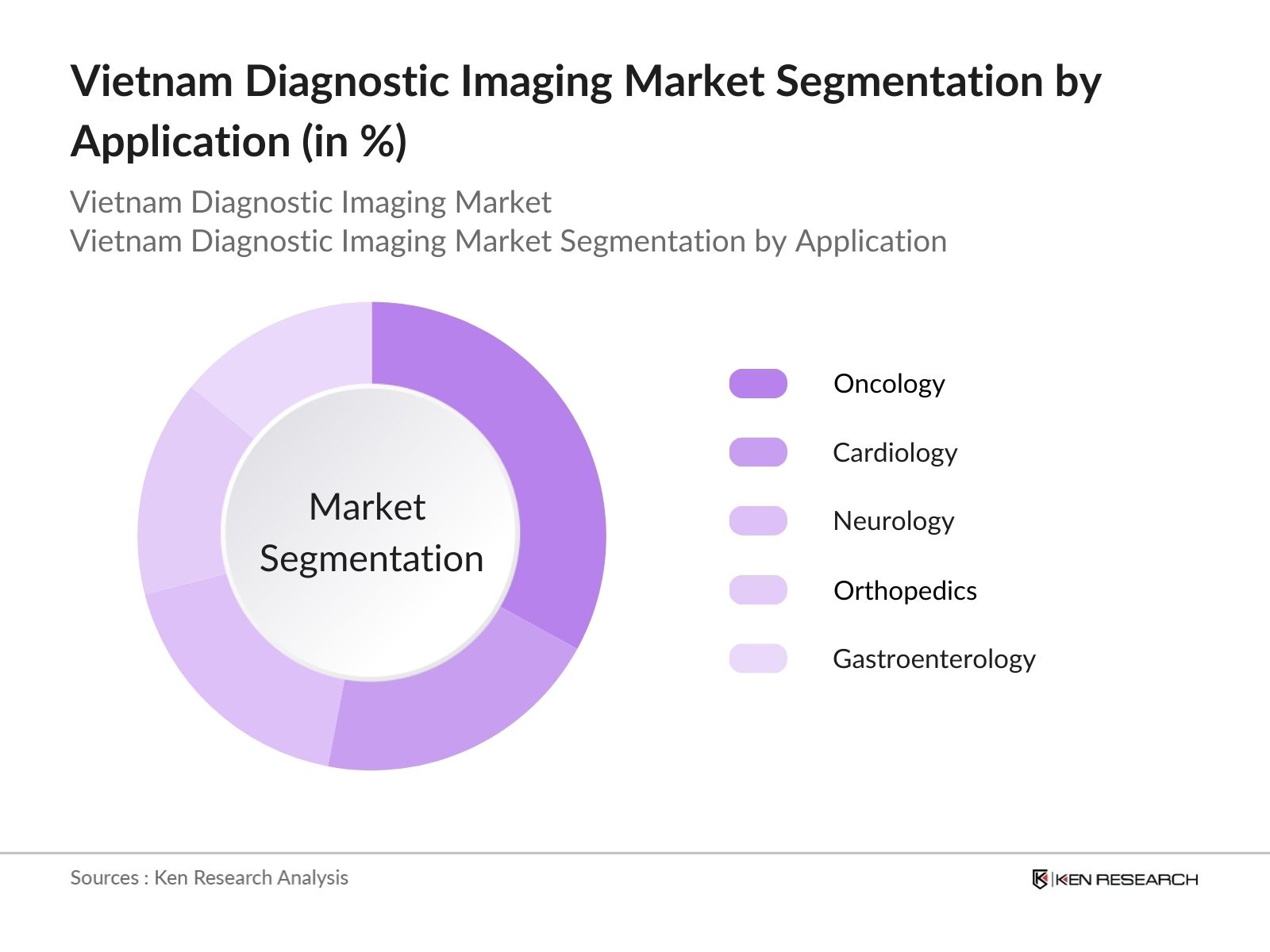

By Application: The Vietnam Diagnostic Imaging market is segmented by application into Oncology, Cardiology, Neurology, Orthopedics, and Gastroenterology. Oncology dominates this segmentation with the largest market share due to the rising incidence of cancer in Vietnam. Diagnostic imaging is critical in the detection and staging of cancer, making it a crucial tool in treatment planning. As cancer awareness and screening programs increase, the demand for advanced imaging techniques such as PET-CT and MRI has risen, cementing the dominance of oncology as a leading application.

Vietnam Diagnostic Imaging Market Competitive Landscape

The Vietnam Diagnostic Imaging market is highly competitive, with a few key players dominating the market. These companies are continuously innovating, leveraging AI, and expanding their digital imaging solutions to cater to the evolving needs of healthcare providers. The market is dominated by global leaders like Siemens Healthineers, GE Healthcare, and Philips Healthcare, with a strong presence of domestic companies focusing on localized needs. These companies have strong brand recognition and have established extensive distribution channels across the country.

|

Company Name |

Establishment Year |

Headquarters |

No. of Employees |

Revenue (USD Bn) |

R&D Investment |

Market Penetration |

Product Innovation |

|

Siemens Healthineers |

1847 |

Erlangen, Germany |

- |

- |

- |

- |

- |

|

GE Healthcare |

1892 |

Chicago, USA |

- |

- |

- |

- |

- |

|

Philips Healthcare |

1891 |

Amsterdam, Netherlands |

- |

- |

- |

- |

- |

|

Canon Medical Systems |

1930 |

Tokyo, Japan |

- |

- |

- |

- |

- |

|

Mindray Medical International |

1991 |

Shenzhen, China |

- |

- |

- |

- |

- |

Vietnam Diagnostic Imaging Market Analysis

Vietnam Diagnostic Imaging Market Growth Drivers:

- Rising Prevalence of Chronic Diseases: The growing prevalence of chronic diseases like diabetes, cardiovascular diseases, and cancer is majorly driving the demand for diagnostic imaging services in Vietnam. According to the World Health Organization (WHO), non-communicable diseases (NCDs) accounted for around 77% of all deaths in Vietnam in 2023. This rising burden of chronic diseases, particularly in urban areas, necessitates early detection and ongoing monitoring, making diagnostic imaging crucial in the healthcare system. Vietnam's population of 99 million further stresses the need for enhanced imaging services to address health challenges associated with an aging population and lifestyle changes.

- Expansion of Healthcare Infrastructure: Vietnam's healthcare infrastructure has expanded in response to economic growth and government investment. In 2023, the Ministry of Health of Vietnam allocated $2.8 billion for healthcare infrastructure improvements, focusing on modernizing hospitals and expanding diagnostic capabilities. The country has been increasing the number of public and private diagnostic centers, with an estimated 1,450 hospitals nationwide, including a growing number of specialized diagnostic centers. This growth enables wider access to advanced imaging services, particularly in rural areas, and supports the overall growth of the diagnostic imaging market.

- Increased Focus on Early Diagnosis and Preventive Healthcare: Vietnam is witnessing a shift towards preventive healthcare, with an increasing emphasis on early diagnosis. The country's National Cancer Control Program focuses on early detection of cancers like breast, cervical, and colorectal, utilizing advanced imaging techniques. In 2023, the Ministry of Health screened over 12 million individuals for cancer-related diseases through national programs. Early diagnosis through imaging not only improves patient outcomes but also reduces long-term healthcare costs, making it a vital component of Vietnams healthcare strategy.

Vietnam Diagnostic Imaging Market Challenges:

- High Equipment Costs: The cost of advanced diagnostic imaging equipment remains a barrier in Vietnam, particularly in rural areas. A standard MRI machine costs about $1.5 million, making it challenging for smaller hospitals and clinics to afford this technology. In 2023, Vietnam's per capita healthcare expenditure was only $170, limiting the budget available for such high-cost equipment. As a result, public healthcare facilities are often reliant on outdated or basic imaging technologies, which impacts the quality of diagnostics in less developed regions.

- Shortage of Skilled Radiologists: Vietnam faces a critical shortage of skilled radiologists, which hinders the optimal use of diagnostic imaging equipment. The country has approximately 4 radiologists per 100,000 people, far below the global average of 12 per 100,000. This shortage is more acute in rural areas, where the deployment of advanced imaging technologies is limited due to the lack of skilled professionals to operate and interpret results. As a result, there is a growing demand for educational programs to address this skill gap and improve diagnostic accuracy.

Vietnam Diagnostic Imaging Future Market Outlook

Over the next five years, the Vietnam Diagnostic Imaging market is expected to show major growth driven by rising healthcare infrastructure development, increasing awareness about early diagnosis, and the government's push to improve healthcare accessibility in rural areas. With continuous technological advancements in imaging systems, such as the integration of artificial intelligence and machine learning, the demand for precision imaging tools will further expand. Growing investments in healthcare digitization and the expansion of diagnostic centers in underserved regions will also contribute to market growth.

Vietnam Diagnostic Imaging Market Opportunities:

- Increased Adoption of Portable Imaging Devices: Portable imaging devices are gaining traction in Vietnam due to their affordability and ease of use in remote areas. As of 2023, more than 500 portable ultrasound machines were deployed in rural health clinics, allowing immediate imaging in areas with limited access to full-scale diagnostic facilities. These devices provide essential services, such as maternal and fetal health monitoring, where immediate imaging is critical. The adoption of portable devices is expected to expand, driven by government incentives aimed at improving healthcare access in underserved regions.

- Expansion of Diagnostic Centers in Rural Areas: There has been a concerted effort to establish diagnostic centers in rural regions of Vietnam. As of 2023, over 300 new diagnostic centers were operational in rural areas, serving over 40 million residents who previously lacked access to advanced healthcare services. These centers are part of Vietnams broader healthcare reform to decentralize medical services and reduce the patient load on urban hospitals. The establishment of these centers presents an opportunity for the diagnostic imaging market to grow, particularly in underserved regions.

Scope of the Report

|

Modality |

X-Ray Imaging CT MRI Ultrasound Nuclear Imaging |

|

End-User |

Hospitals Diagnostic Centers Ambulatory Care Centers |

|

Application |

Oncology Cardiology Neurology Orthopedics Gastroenterology |

|

Technology |

Analog Imaging Digital Imaging |

|

Region |

Northern Vietnam, Central Vietnam, Southern Vietnam |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Government and Regulatory Bodies

Banks and Financial Institutes

Investors and Venture Capitalists

Hospitals and Diagnostic Centers

Radiology Departments

Imaging Equipment Manufacturers

Health Insurance Providers

Companies

Players Mentioned in the Report:

Siemens Healthineers

GE Healthcare

Philips Healthcare

Canon Medical Systems Corporation

Mindray Medical International

Hitachi Medical Corporation

Fujifilm Holdings Corporation

Samsung Medison

Carestream Health

Shimadzu Corporation

Esaote SpA

Hologic Inc.

Planmed Oy

Agfa-Gevaert Group

Medtronic

Table of Contents

1. Vietnam Diagnostic Imaging Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Vietnam Diagnostic Imaging Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Vietnam Diagnostic Imaging Market Analysis

3.1. Growth Drivers

3.1.1. Rising Prevalence of Chronic Diseases

3.1.2. Expansion of Healthcare Infrastructure

3.1.3. Government Healthcare Initiatives

3.1.4. Increased Focus on Early Diagnosis and Preventive Healthcare

3.2. Market Challenges

3.2.1. High Equipment Costs

3.2.2. Shortage of Skilled Radiologists

3.2.3. Limited Reimbursement Coverage

3.3. Opportunities

3.3.1. Technological Advancements (AI, Machine Learning)

3.3.2. Increased Adoption of Portable Imaging Devices

3.3.3. Expansion of Diagnostic Centers in Rural Areas

3.4. Trends

3.4.1. Adoption of 3D and 4D Imaging Technology

3.4.2. Integration of Cloud-Based Imaging Solutions

3.4.3. Increased Focus on Radiation Safety

3.5. Government Regulations

3.5.1. National Health Policies Supporting Diagnostic Imaging

3.5.2. Import Regulations for Medical Devices

3.5.3. Healthcare Standards Compliance

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Vietnam Diagnostic Imaging Market Segmentation

4.1. By Modality (In Value %)

4.1.1. X-Ray Imaging

4.1.2. Computed Tomography (CT)

4.1.3. Magnetic Resonance Imaging (MRI)

4.1.4. Ultrasound Imaging

4.1.5. Nuclear Imaging

4.2. By End-User (In Value %)

4.2.1. Hospitals

4.2.2. Diagnostic Centers

4.2.3. Ambulatory Care Centers

4.3. By Application (In Value %)

4.3.1. Oncology

4.3.2. Cardiology

4.3.3. Neurology

4.3.4. Orthopedics

4.3.5. Gastroenterology

4.4. By Technology (In Value %)

4.4.1. Analog Imaging

4.4.2. Digital Imaging

4.5. By Region (In Value %)

4.5.1. Northern Vietnam

4.5.2. Central Vietnam

4.5.3. Southern Vietnam

5. Vietnam Diagnostic Imaging Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Siemens Healthineers

5.1.2. GE Healthcare

5.1.3. Philips Healthcare

5.1.4. Canon Medical Systems Corporation

5.1.5. Hitachi Medical Corporation

5.1.6. Mindray Medical International

5.1.7. Samsung Medison

5.1.8. Fujifilm Holdings Corporation

5.1.9. Carestream Health

5.1.10. Shimadzu Corporation

5.1.11. Esaote SpA

5.1.12. Hologic Inc.

5.1.13. Planmed Oy

5.1.14. Agfa-Gevaert Group

5.1.15. Medtronic

5.2 Cross Comparison Parameters (R&D Investment, Market Penetration, Product Offerings, Innovation Capabilities, Customer Support)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. Vietnam Diagnostic Imaging Market Regulatory Framework

6.1. Medical Device Registration Process

6.2. Licensing and Compliance Requirements

6.3. Radiation Safety Standards

7. Vietnam Diagnostic Imaging Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Vietnam Diagnostic Imaging Future Market Segmentation

8.1. By Modality (In Value %)

8.2. By End-User (In Value %)

8.3. By Application (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9. Vietnam Diagnostic Imaging Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. White Space Opportunity Analysis

9.3. Customer Cohort Analysis

9.4. Marketing Initiatives

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

In the first phase, we identified and mapped out all stakeholders within the Vietnam Diagnostic Imaging market. Our comprehensive research included both public and proprietary databases to gather relevant industry information, with a focus on identifying crucial variables that drive market trends and dynamics.

Step 2: Market Analysis and Construction

We analyzed historical data related to the penetration of diagnostic imaging equipment, assessing revenue generation and service quality across different regions. The analysis of technological adoption rates and healthcare expenditure further strengthened our findings and allowed us to estimate market size with precision.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were formulated and validated through consultations with industry experts from leading healthcare providers and imaging equipment manufacturers. We conducted in-depth interviews to gain operational insights, ensuring the accuracy of our market forecasts and data.

Step 4: Research Synthesis and Final Output

In this final phase, we synthesized the research data collected from manufacturers, hospitals, and diagnostic centers to present a holistic view of the Vietnam Diagnostic Imaging market. The reports findings were corroborated with real-world sales figures, product performance data, and consumer preferences.

Frequently Asked Questions

01. How big is the Vietnam Diagnostic Imaging Market?

The Vietnam Diagnostic Imaging market is valued at USD 201 million, driven by advancements in imaging technologies and increasing healthcare expenditure.

02. What are the challenges in the Vietnam Diagnostic Imaging Market?

Challenges include high costs of advanced imaging equipment, limited access to imaging services in rural areas, and the shortage of trained radiologists.

03. Who are the major players in the Vietnam Diagnostic Imaging Market?

Key players include Siemens Healthineers, GE Healthcare, Philips Healthcare, Canon Medical Systems Corporation, and Mindray Medical International.

04. What are the growth drivers of the Vietnam Diagnostic Imaging Market?

The market is propelled by rising healthcare spending, increasing demand for early disease diagnosis, and advancements in imaging technology, such as AI-based systems.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.