Vietnam Insurance Market Outlook to 2030

Region:Vietnam

Author(s):Mukul

Product Code:KROD3400

Region:Vietnam

Author(s):Mukul

Product Code:KROD3400

October 2024

89

The Vietnam insurance market is dominated by a mix of local and international players, with companies like Prudential Vietnam, Bao Viet Insurance, and AIA Vietnam leading the way. These firms have established themselves through comprehensive product offerings, strategic partnerships, and extensive distribution networks. As digital insurance platforms continue to grow, newer players are entering the market, but traditional players retain a significant share due to their established presence and trust among consumers.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (USD bn) |

Market Share (%) |

No. of Employees |

Product Range |

Geographic Reach |

Digital Platform |

|

Prudential Vietnam |

1999 |

Ho Chi Minh City |

||||||

|

Bao Viet Insurance |

1965 |

Hanoi |

||||||

|

AIA Vietnam |

2000 |

Ho Chi Minh City |

||||||

|

Manulife Vietnam |

1999 |

Ho Chi Minh City |

||||||

|

Dai-ichi Life Vietnam |

2007 |

Ho Chi Minh City |

Vietnam Insurance Market Growth Drivers

Vietnam Insurance Market Restraints

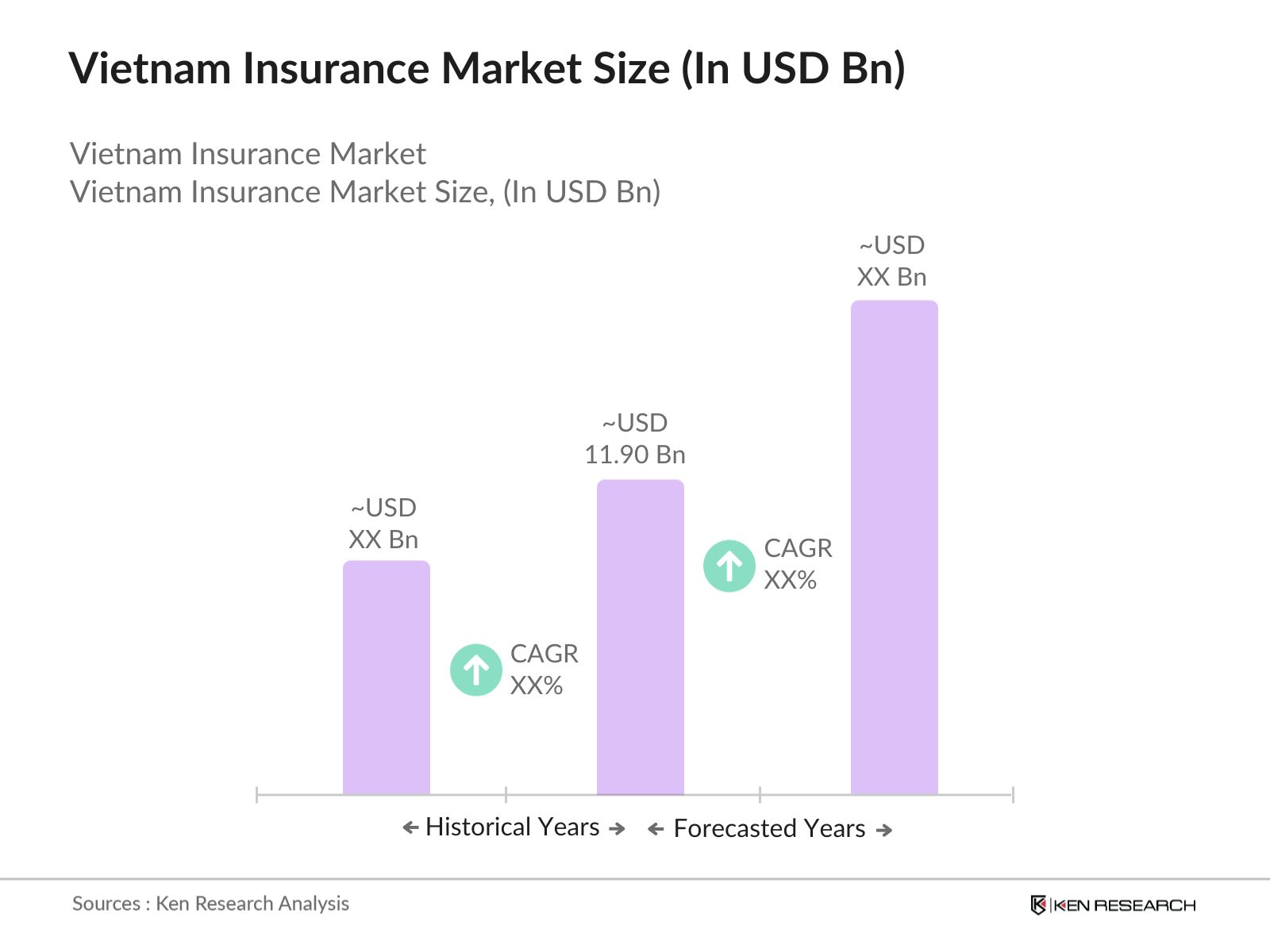

Over the next five years, the Vietnam insurance market is expected to experience significant growth driven by continued economic expansion, rising disposable income, and a shift toward digital insurance platforms. Additionally, the governments supportive regulatory framework, coupled with increasing foreign investment, will help propel the market forward. Health and life insurance products, in particular, are anticipated to witness substantial growth as awareness of financial security and healthcare needs increases.

Market Opportunities

|

By Insurance Type |

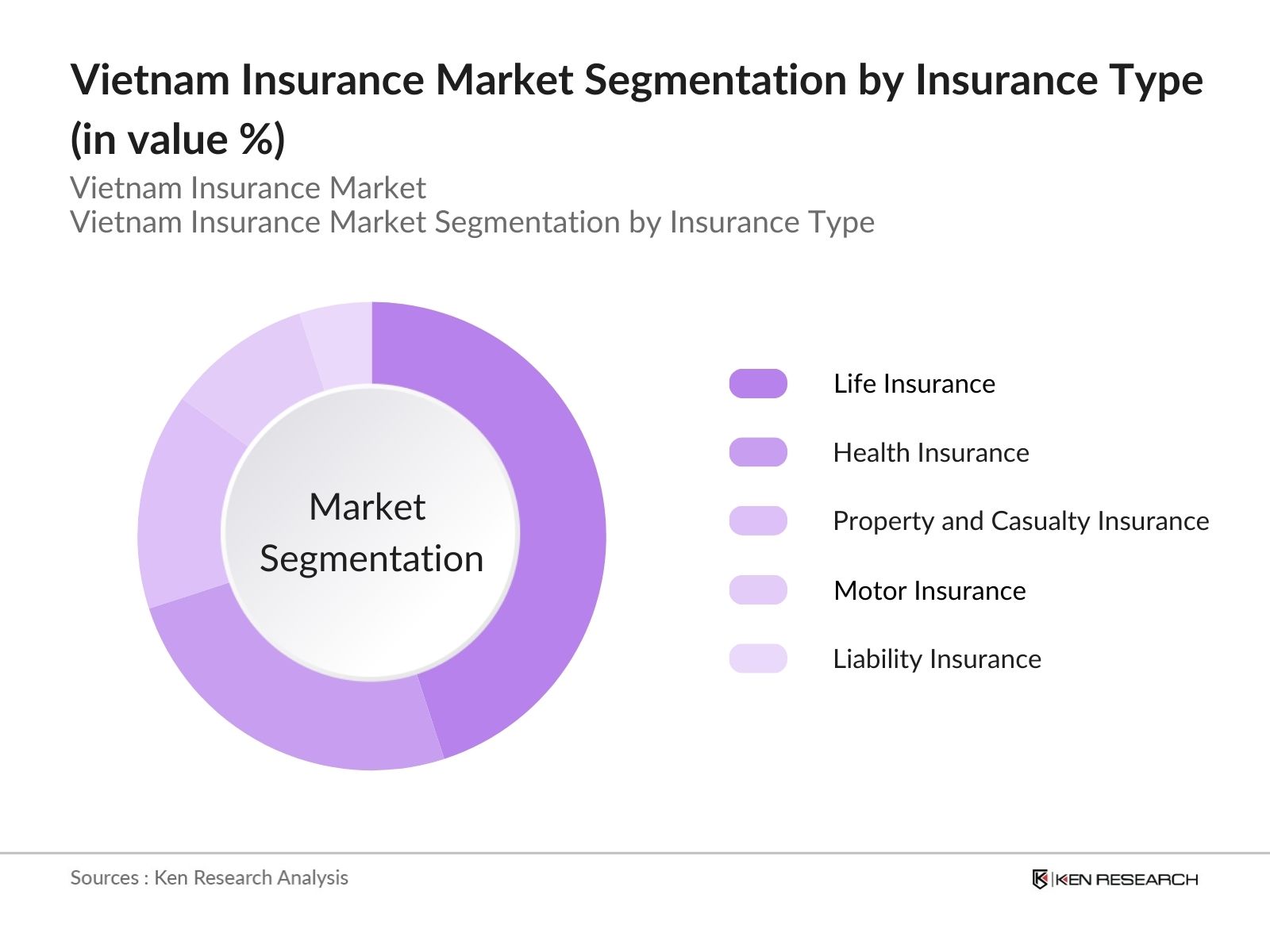

Life Insurance Health Insurance Property & Casualty Insurance Motor Insurance Liability Insurance |

|

By Distribution Channel |

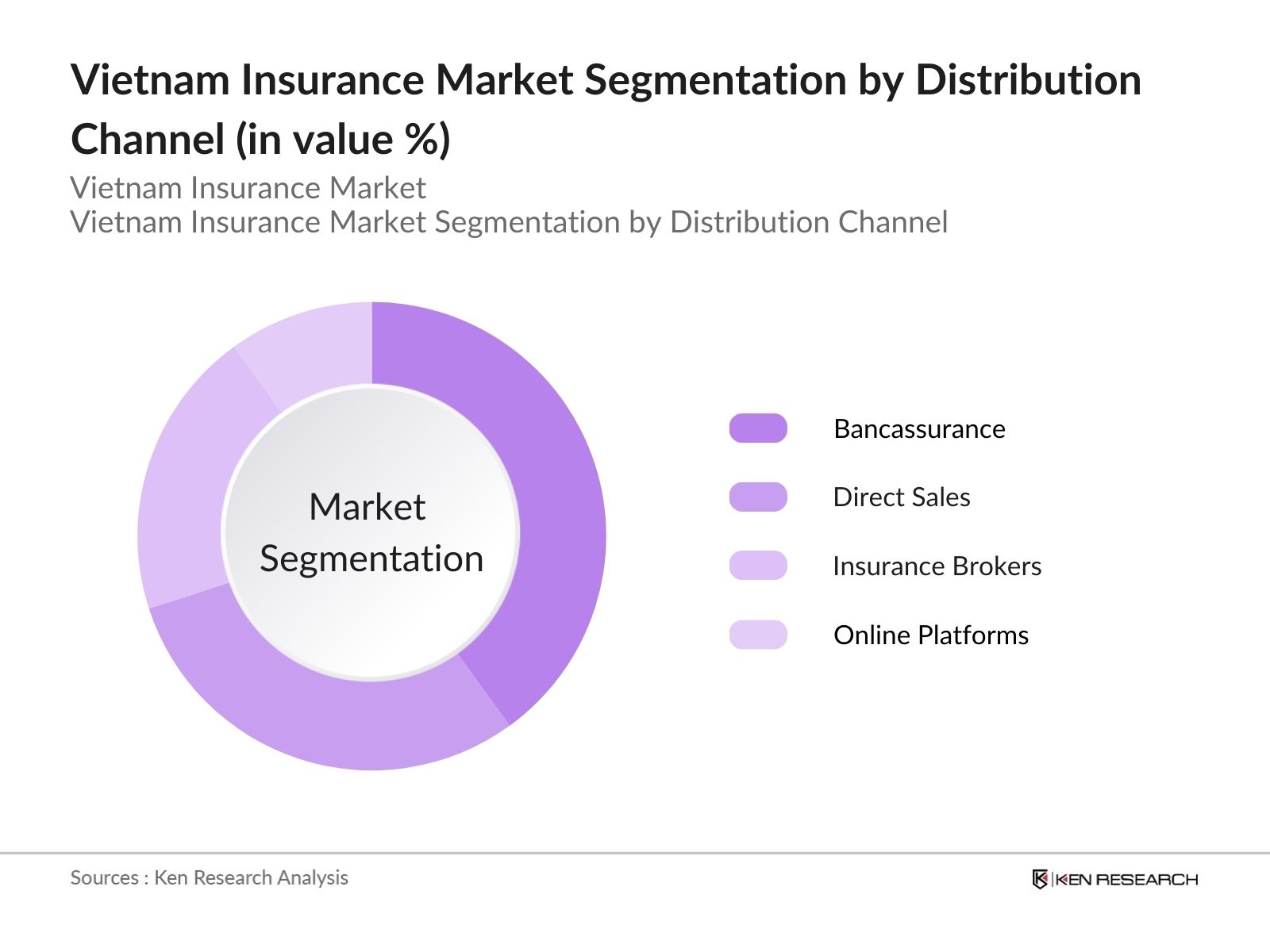

Direct Sales Bancassurance Insurance Brokers Online Platforms |

|

By Customer Type |

Individual Corporate |

|

By Region |

Northern Vietnam Central Vietnam Southern Vietnam |

|

By Premium Type |

Regular Premium Single Premium |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1.Growth Drivers

3.1.1. Increased Disposable Income

3.1.2. Regulatory Changes Favoring Private Insurance

3.1.3. Rise of Digital Insurance Platforms

3.1.4. Aging Population and Healthcare Awareness

3.2.Market Challenges

3.2.1. Low Insurance Penetration in Rural Areas

3.2.2. Regulatory and Compliance Burdens

3.2.3. Lack of Financial Literacy and Awareness

3.3.Opportunities

3.3.1. Adoption of InsurTech Solutions

3.3.2. Microinsurance Growth in Underserved Markets

3.3.3. Expansion of Health and Life Insurance Products

3.4.Trends

3.4.1. Digital Transformation and AI-Powered Solutions

3.4.2. Customization of Insurance Policies

3.4.3. Increasing Partnership Between Banks and Insurers (Bancassurance)

3.5.Government Regulation

3.5.1. Vietnam Insurance Law Amendments

3.5.2. Foreign Direct Investment (FDI) Regulations

3.5.3. Financial Stability and Supervisory Framework

3.6.SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1.By Insurance Type (In Value %)

4.1.1. Life Insurance

4.1.2. Health Insurance

4.1.3. Property & Casualty Insurance

4.1.4. Motor Insurance

4.1.5. Liability Insurance

4.2.By Distribution Channel (In Value %)

4.2.1. Direct Sales

4.2.2. Bancassurance

4.2.3. Insurance Brokers

4.2.4. Online Platforms

4.3.By Customer Type (In Value %)

4.3.1. Individual

4.3.2. Corporate

4.4.By Region (In Value %)

4.4.1. Northern Vietnam

4.4.2. Central Vietnam

4.4.3. Southern Vietnam

4.5.By Premium Type (In Value %)

4.5.1. Regular Premium

4.5.2. Single Premium

5.1.Detailed Profiles of Major Companies

5.1.1. Prudential Vietnam Assurance

5.1.2. Bao Viet Insurance

5.1.3. AIA Vietnam

5.1.4. Manulife Vietnam

5.1.5. Dai-ichi Life Vietnam

5.1.6. Chubb Life Vietnam

5.1.7. Sun Life Vietnam

5.1.8. PVI Insurance

5.1.9. Generali Vietnam

5.1.10. MB Ageas Life

5.1.11. Cathay Life Insurance Vietnam

5.1.12. Liberty Insurance

5.1.13. PTI Insurance

5.1.14. Samsung Vina Insurance

5.1.15. BIDV Insurance

5.2.Cross Comparison Parameters

Market Share

Revenue

Number of Employees

Geographical Reach

Product Portfolio

Customer Base

Market Penetration Rate

Strategic Initiatives

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Insurance Supervisory Authority Regulations

6.2. Solvency and Risk-Based Capital Requirements

6.3. Compliance and Reporting Guidelines

6.4. Tax Regulations on Insurance Premiums

6.5. Liberalization Policies for Foreign Insurers

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Insurance Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By Customer Type (In Value %)

8.4. By Region (In Value %)

8.5. By Premium Type (In Value %)

9.1. Customer Acquisition and Retention Strategies

9.2. Digital Marketing Initiatives

9.3. White Space Opportunities in Rural Markets

9.4. Product Diversification Strategies

The first step involves mapping the key stakeholders in the Vietnam insurance market. Extensive desk research was carried out using secondary and proprietary data sources to identify critical variables affecting market dynamics, including regulatory changes, consumer preferences, and distribution channels.

This step focuses on analyzing historical data related to insurance products, distribution channels, and consumer demographics. We also assessed the market penetration of various insurance types and distribution methods, leading to accurate revenue estimations.

Market hypotheses were validated through interviews with industry experts from major insurance companies, including both local and international firms. This provided insights into operational trends, challenges, and opportunities that refined the market analysis.

The final stage involved synthesizing data from multiple sources and consultations to ensure comprehensive and validated insights into the Vietnam insurance market. This included bottom-up and top-down approaches to cross-check market size, segmentation, and competitive landscape findings.

The Vietnam insurance market is valued at USD 11.90 billion, driven by rising disposable income, regulatory reforms, and increased awareness of insurance products among consumers.

Challenges include low penetration in rural areas, regulatory compliance issues, and a lack of financial literacy, which limits the uptake of insurance products, especially in the health and life insurance segments.

Key players include Prudential Vietnam, Bao Viet Insurance, AIA Vietnam, Manulife Vietnam, and Dai-ichi Life Vietnam, all of which dominate due to their extensive product portfolios, distribution networks, and strong brand presence.

Key drivers include economic growth, rising disposable incomes, and government policies promoting the insurance sector. Increased digitalization and partnerships between banks and insurers (bancassurance) also play a pivotal role.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.