Vietnam Mobile Payments Market Outlook to 2029

Region:Asia

Author(s):Anmol, Chirag

Product Code:KR1503

We use cookies and similar technologies to improve your experience, analyze website traffic, and personalize content. By clicking Accept All, you consent to our use of cookies and analytics tracking.

Privacy PolicyRegion:Asia

Author(s):Anmol, Chirag

Product Code:KR1503

April 2025

80-100

The Vietnam Mobile Payments market is valued at USD 40 billion, based on a five-year historical analysis. The rapid surge is driven by a strong increase in smartphone penetration, which reached 84 million users, and internet usage, with over 78.9 million active users. The market is also fueled by rising contactless transaction adoption and robust government support for digital financial inclusion, particularly among underserved communities.

Hanoi and Ho Chi Minh City dominate the Vietnam Mobile Payments landscape due to their high urbanization, advanced digital infrastructure, and concentrated presence of fintech startups and banking institutions. These cities also benefit from QR code transaction booms and government-led initiatives, such as smart city programs and financial technology zones, creating an ideal ecosystem for rapid mobile payments adoption and usage at scale.

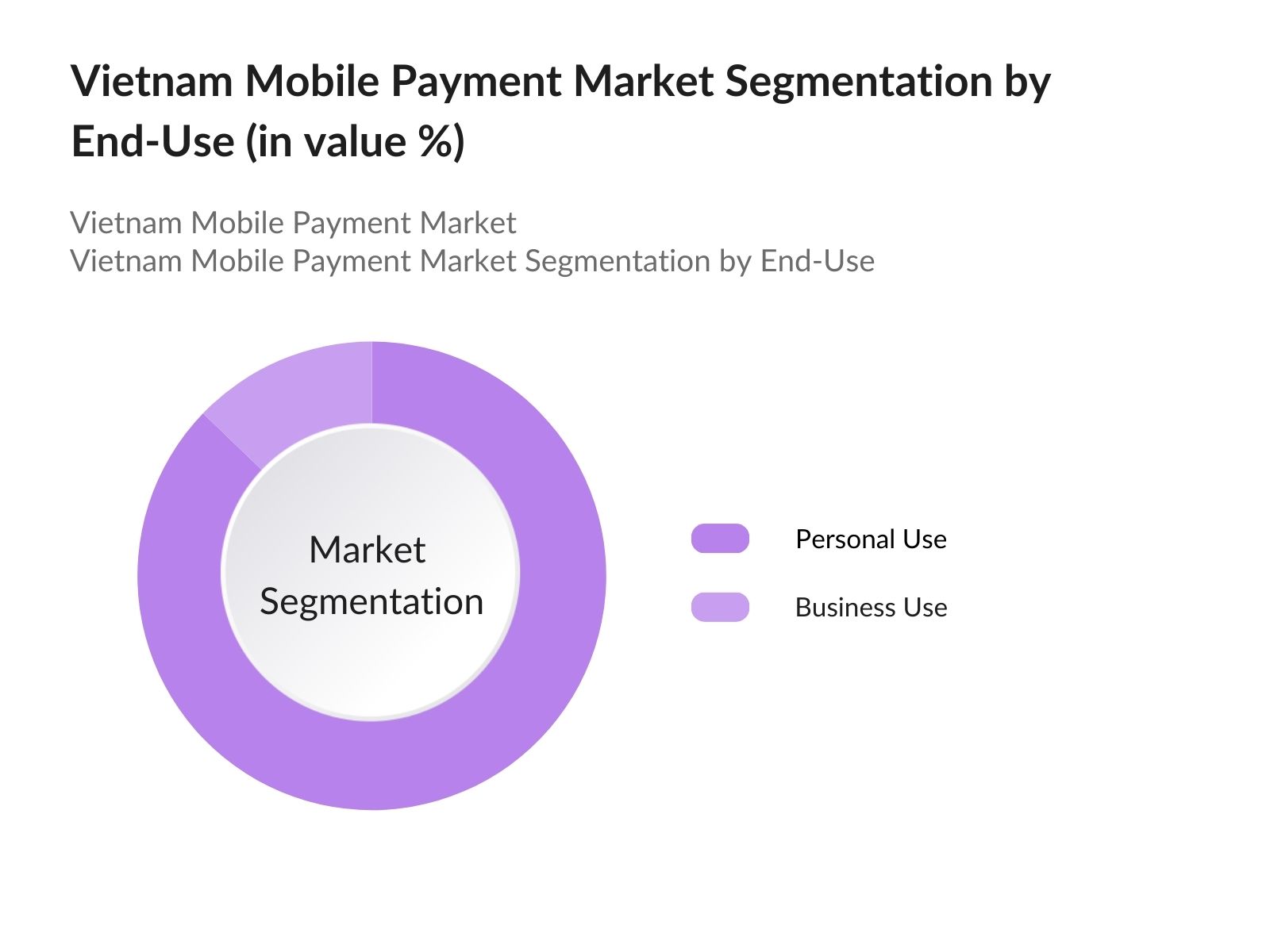

By End Use: The Vietnam mobile payments market is segmented by end use into Personal Use and Business Use. The market under the end-use segment is heavily dominated by personal usage. The personal use segment holds the largest market share due to widespread e-wallet adoption, peer-to-peer payments, and retail digital transactions. This growth is catalyzed by smartphone ubiquity, low transaction limits, and ease of app integration across the retail and service ecosystems.

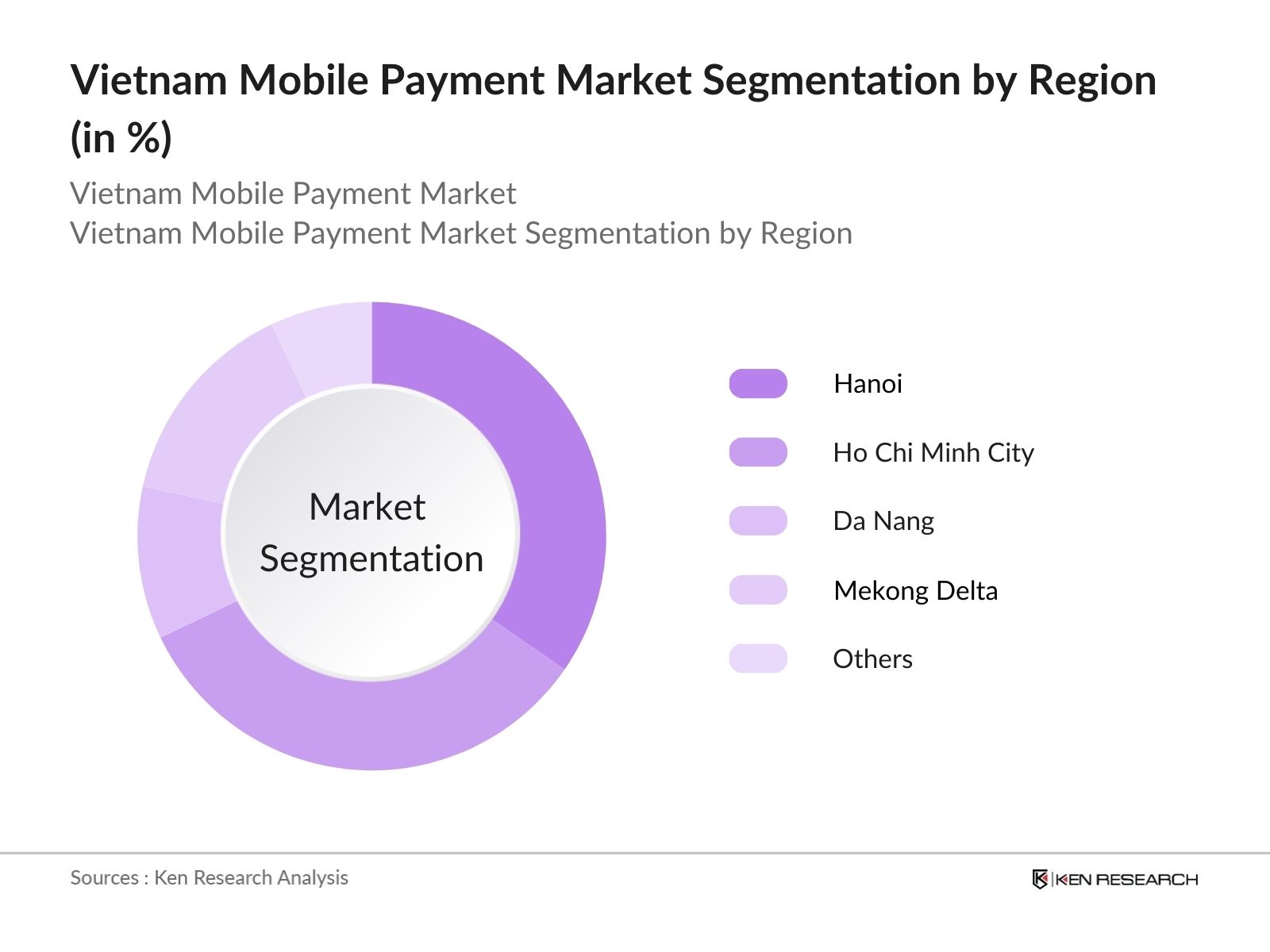

By Region: The Vietnam mobile payments market is segmented by region into Hanoi, Ho Chi Minh City, Da Nang, Mekong Delta, and Others. Hanoi holds the largest regional share due to its lead in QR-based transaction volume and value, driven by higher merchant adoption and early government investment in fintech infrastructure. Ho Chi Minh City follows closely due to its robust startup ecosystem and dense user base. Da Nang and the Mekong Delta are emerging through mobile money drives and rural inclusion programs.

By Region: The Vietnam mobile payments market is segmented by region into Hanoi, Ho Chi Minh City, Da Nang, Mekong Delta, and Others. Hanoi holds the largest regional share due to its lead in QR-based transaction volume and value, driven by higher merchant adoption and early government investment in fintech infrastructure. Ho Chi Minh City follows closely due to its robust startup ecosystem and dense user base. Da Nang and the Mekong Delta are emerging through mobile money drives and rural inclusion programs.

Vietnam Mobile Payments Market Competitive Landscape

Vietnam Mobile Payments Market Competitive LandscapeThe Vietnam Mobile Payments market is dominated by strong local e-wallet providers backed by retail integrations, digital loyalty features, and robust consumer adoption. Players like MoMo, ZaloPay, and VNPay lead in transaction volumes and user base, driven by their intuitive user experience and strategic partnerships with merchants. With over 40 active e-wallet platforms operating, the market remains highly competitive, reinforced by cashback incentives, QR-based payments, and integration across super-app ecosystems.

Mobile Penetration and Internet Connectivity: Vietnam's digital ecosystem is advancing rapidly. As of 2024, the country has 84 million smartphone users and 79.8 million internet users. Mobile broadband access is expanding, particularly in rural areas, improving access to digital services. This widespread smartphone usage is fueling mobile wallet adoption. The government plans 100% 5G mobile coverage to enhance financial access and close the urban-rural digital divide, as per Vietnam's Digital Infrastructure Master Plan.

Surge in Contactless and Cashless Payments: The value of domestic credit transfers reached 48 quadrillion VND in a single quarter. Contactless card usage now accounts for 75% of Visa transactions. The younger population leads this transformation, with 88% of Gen Z and Gen Y users preferring cashless transactions. QR code adoption saw a 106.7% surge in transaction volumes, streamlining merchant operations and enhancing transaction speed and transparency.

Government Support for Digital Economy and Inclusion: The Vietnamese government's National Digital Transformation Programme and Financial Inclusion Strategy are boosting mobile payment infrastructure. High-speed internet and 5G will cover 99% of the population. Initiatives like financial inclusion for women entrepreneurs are improving access to mobile banking and creating a wider consumer base for digital payment platforms, ensuring long-term growth in the sector.

Uneven Digital Infrastructure in Remote Regions: Despite national plans, some rural regions still lack consistent mobile connectivity. This digital divide limits the reach of mobile payment services in less urbanized provinces, impacting merchant onboarding and financial inclusivity in remote economies.

Cybersecurity and Consumer Trust Issues: Vietnam's cybersecurity authority recorded a rise in financial fraud cases related to digital payments. Many consumers remain skeptical of mobile wallets due to phishing, SMS fraud, and a lack of strong consumer protection laws. This skepticism is particularly prevalent among older demographics and low-income groups who are less digitally literate.

Over the next 5 years, the Vietnam mobile payments market is expected to witness exponential growth driven by a tech-savvy population, expanding digital infrastructure, and targeted government policies. With active support from the State Bank and implementation of Decree 52, the regulatory environment is now aligned to support e-wallet innovation and intermediary payment service expansion. Regions like Hanoi and Ho Chi Minh City will continue to lead, while rural zones see higher uptake through mobile money services.

Integration with Public Services and Micro-Merchant Ecosystem: Vietnam has 5.5 million SMEs and informal retailers, many of whom remain unbanked. With growing QR code acceptance and API integration, mobile wallets can expand to tax payments, ticketing, and municipal services. Public-private partnerships could facilitate wallet interoperability and create new revenue streams via government service digitization.

Cross-Border and Remittance-Linked Wallet Expansion: With over 5.3 million overseas Vietnamese and growing inbound tourism, cross-border wallet functionality presents a major opportunity. Supporting FX conversion, inbound QR acceptance, and remittance disbursement could strengthen platforms like MoMo and ZaloPay. Backed by improvements in digital identity (DID) and e-KYC, this trend is shaping the next wave of mobile wallet use cases.

|

By Platform |

Android |

|

By Payment Type |

Peer-to-Peer (P2P) |

|

By End User |

Retail & E-Commerce |

|

By Region |

Northern |

|

By Transaction Mode |

QR Code |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Volume of Mobile Transactions, Daily Average Transactions, Urban-Rural Distribution)

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Digital Banking Adoption, Mobile Wallet Penetration, Infrastructure Rollout)

3.1. Growth Drivers

3.1.1. Smartphone Penetration

3.1.2. Government Push for Cashless Economy

3.1.3. Urban Youth and Digital Consumption Behavior

3.1.4. FinTech Ecosystem Maturity

3.2. Restraints

3.2.1. Rural Access and Connectivity Gaps

3.2.2. Cybersecurity and Fraud Concerns

3.2.3. User Trust and Financial Literacy

3.3. Opportunities

3.3.1. Expansion into Rural Districts

3.3.2. Integration with Public Utility and Transport Systems

3.3.3. Interoperability of Wallets and Bank-Linked Platforms

3.4. Trends

3.4.1. Surge in QR Code-based Transactions

3.4.2. Embedded Payments in Super Apps

3.4.3. AI-Powered Fraud Detection Integration

3.5. Government Regulation

3.5.1. SBVs Mobile Money Licensing Framework

3.5.2. National Digital Transformation Roadmap

3.5.3. E-KYC Mandates and Biometric Integration

3.5.4. Data Localization and Compliance Guidelines

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Wallet Providers, Banks, Telcos, Consumers, Regulators)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Platform (In Volume %)

4.1.1. Android

4.1.2. iOS

4.1.3. Web

4.2. By Payment Type (In Volume %)

4.2.1. Peer-to-Peer (P2P)

4.2.2. Business-to-Business (B2B)

4.2.3. Consumer-to-Business (C2B)

4.3. By End User (In Volume %)

4.3.1. Retail & E-Commerce

4.3.2. Transportation

4.3.3. Utilities & Bill Payments

4.3.4. Hospitality

4.4. By Transaction Mode (In Volume %)

4.4.1. QR Code

4.4.2. NFC

4.4.3. Mobile Wallets

4.4.4. Bank Transfer

4.5. By Region (In Volume %)

4.5.1. Northern Vietnam

4.5.2. Central Vietnam

4.5.3. Southern Vietnam

5.1. Detailed Profiles of Major Companies

5.1.1. MoMo

5.1.2. ZaloPay

5.1.3. VNPay

5.1.4. ShopeePay

5.1.5. Viettel Money

5.1.6. AirPay

5.1.7. Moca (GrabPay)

5.1.8. Payoo

5.1.9. BIDV SmartBanking

5.1.10. TPBank eBanking

5.1.11. Techcombank F@st Mobile

5.1.12. Vietcombank Mobile

5.1.13. MB Bank App

5.1.14. Napas

5.1.15. Agribank E-Mobile

5.2. Cross Comparison Parameters (Transaction Volume, No. of Users, Partner Merchants, Integration Channels, API Compatibility, Interoperability Readiness, Payment Success Rate, Refund Resolution Time)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investors Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. SBV Circulars on E-Money

6.2. Data Privacy & User Consent Norms

6.3. FinTech Sandbox Environment

6.4. KYC/AML Compliance Requirements

7.1. Projected Transaction Volumes

7.2. Key Drivers of Future Growth

8.1. By Platform (In Volume %)

8.2. By Payment Type (In Volume %)

8.3. By End User (In Volume %)

8.4. By Transaction Mode (In Volume %)

8.5. By Region (In Volume %)

9.1. TAM/SAM/SOM Analysis

9.2. White Space Opportunity Mapping

9.3. Partnership Roadmap (Retailers, Super Apps, Government Apps)

9.4. GTM Strategy for Tier-2 Penetration

The research began with the identification of key operational, transactional, and regulatory variables shaping the Vietnam mobile payment ecosystem. This step involved reviewing datasets from the State Bank of Vietnam (SBV), Ministry of Information and Communications, and telecom/digital infrastructure reports to frame the mobile payment landscape.

Historical transaction volumes, platform-specific adoption rates, and merchant integration patterns were mapped using government open data portals and telecom operator releases. This helped construct regional adoption metrics and usage rates across sectors such as retail, transport, and bill payments, validated through monthly mobile wallet transaction reports.

Strategic hypotheses were tested through direct interviews with payment gateway executives, digital wallet providers, and policymakers at SBV. These consultations helped quantify insights on infrastructure challenges, fraud prevention efforts, and technology preferences (NFC, QR code, mobile apps) to finalize user-side metrics and merchant-side data.

All findings were consolidated using a bottom-up and top-down approach, integrating user-level data with bank partnership metrics, telecom-based eKYC initiatives, and SBV licensing mandates. Final report outputs were cross-verified against transaction settlement figures and real-time payment dashboards to ensure accuracy and depth.

The Vietnam mobile payment market registered 40 billion transactions, based on State Bank of Vietnam data. This reflects the expanding digital infrastructure, smartphone adoption, and increased use of e-wallets like MoMo and ZaloPay across both urban and rural regions.

Vietnam Mobile Payment Market Challenges include fragmented merchant acceptance in Tier-2 cities, cash preference in rural markets, and rising data security threats. Many small vendors still lack QR payment infrastructure, and only 22 banks support seamless interoperability with all digital wallets.

Vietnam Mobile Payment Market Major players include MoMo, ZaloPay, VNPay, ShopeePay, Viettel Money, and Moca. These companies lead the market due to their extensive retail partnerships, integration into super apps, and strong collaborations with public services and banking channels.

Vietnam Mobile Payment Market Growth is driven by rapid smartphone penetration (over 96 million mobile connections), SBVs mobile money licensing initiatives, and the integration of digital wallets into transportation, utility payments, and government services. Increasing trust in QR code systems also contributes.

Vietnam Mobile Payment Market Opportunities exist in digitizing public transit ticketing, enabling inter-wallet interoperability, and embedding mobile payments in school fee systems and hospital bills. SBV-backed digital transformation and 5G rollout across 63 provinces support scalable growth of wallet adoption.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.