Vietnam Photovoltaics Market Outlook to 2030

Region:Asia

Author(s):Sanjeev

Product Code:KROD8539

December 2024

82

About the Report

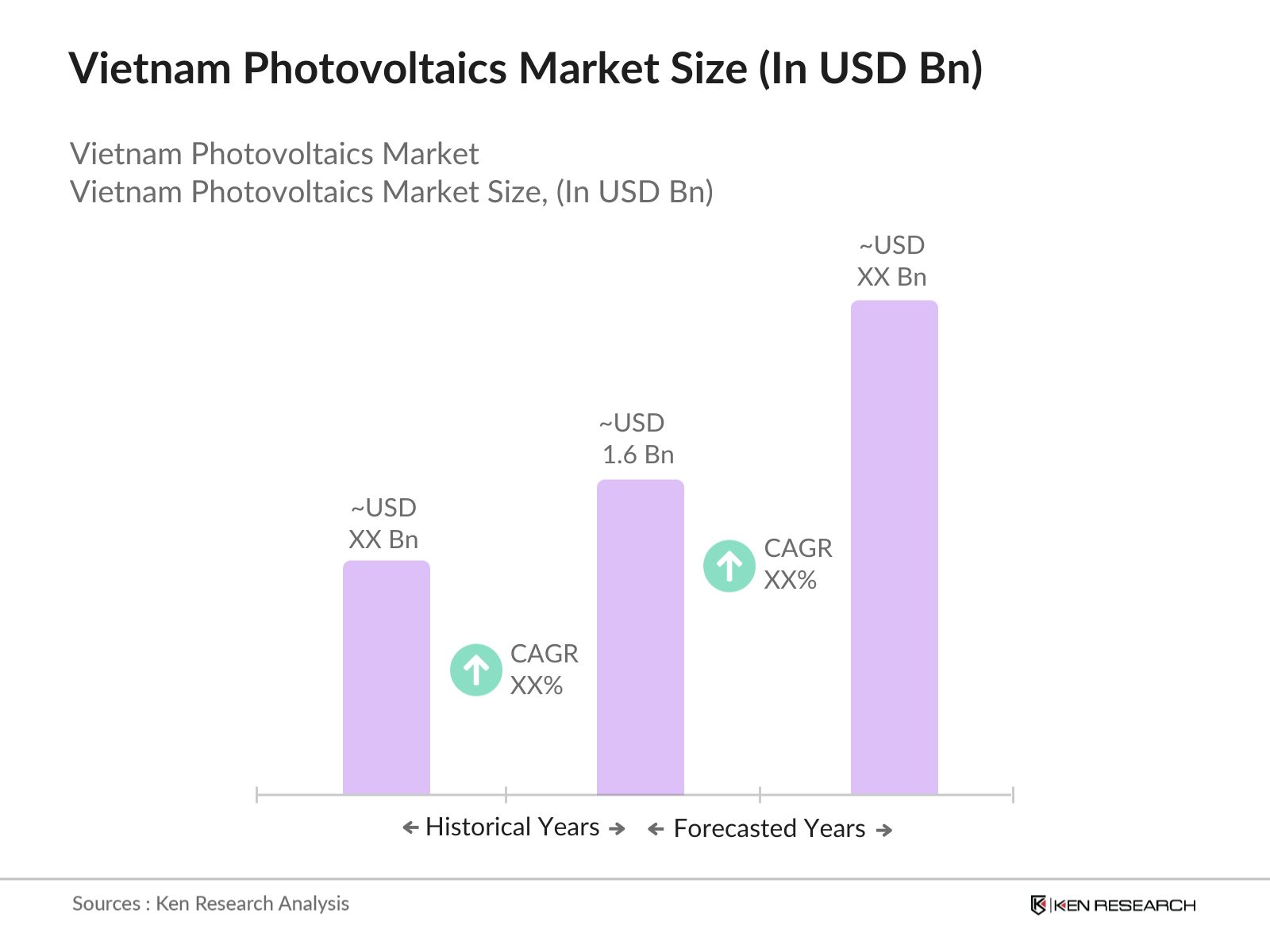

Vietnam Photovoltaics Market Overview

- The Vietnam photovoltaics market is valued at USD 1.6 billion, driven by the country's strong push for renewable energy adoption. Vietnams solar market has seen exponential growth over recent years, fueled by declining costs of solar technology, government incentives like feed-in tariffs (FiTs), and a growing need for energy security amidst rising electricity demand. The market has benefitted from policies aiming to diversify energy sources and reduce dependency on traditional fossil fuels, which has led to widespread adoption of solar energy systems in both urban and rural regions.

- Ho Chi Minh City and Binh Thuan province dominate the solar market due to their favorable geographic locations with high solar irradiance and large tracts of land available for utility-scale solar farms. These regions also benefit from strong government backing for infrastructure development, making them ideal for large-scale photovoltaic installations. Additionally, areas in Southern Vietnam, where sunlight is more abundant, are emerging as key hubs for photovoltaic projects.

- Power Purchase Agreements (PPAs) are a critical component of Vietnams solar energy regulation framework. In 2023, Vietnam Electricity (EVN) began implementing direct PPAs, allowing corporate buyers to purchase power directly from solar developers at negotiated prices, independent of government tariffs. This move is expected to drive private sector investment in solar energy projects. The Ministry of Industry and Trade projects that direct PPAs will contribute over 5 GW of solar power by 2025, improving financial flexibility for solar developers.

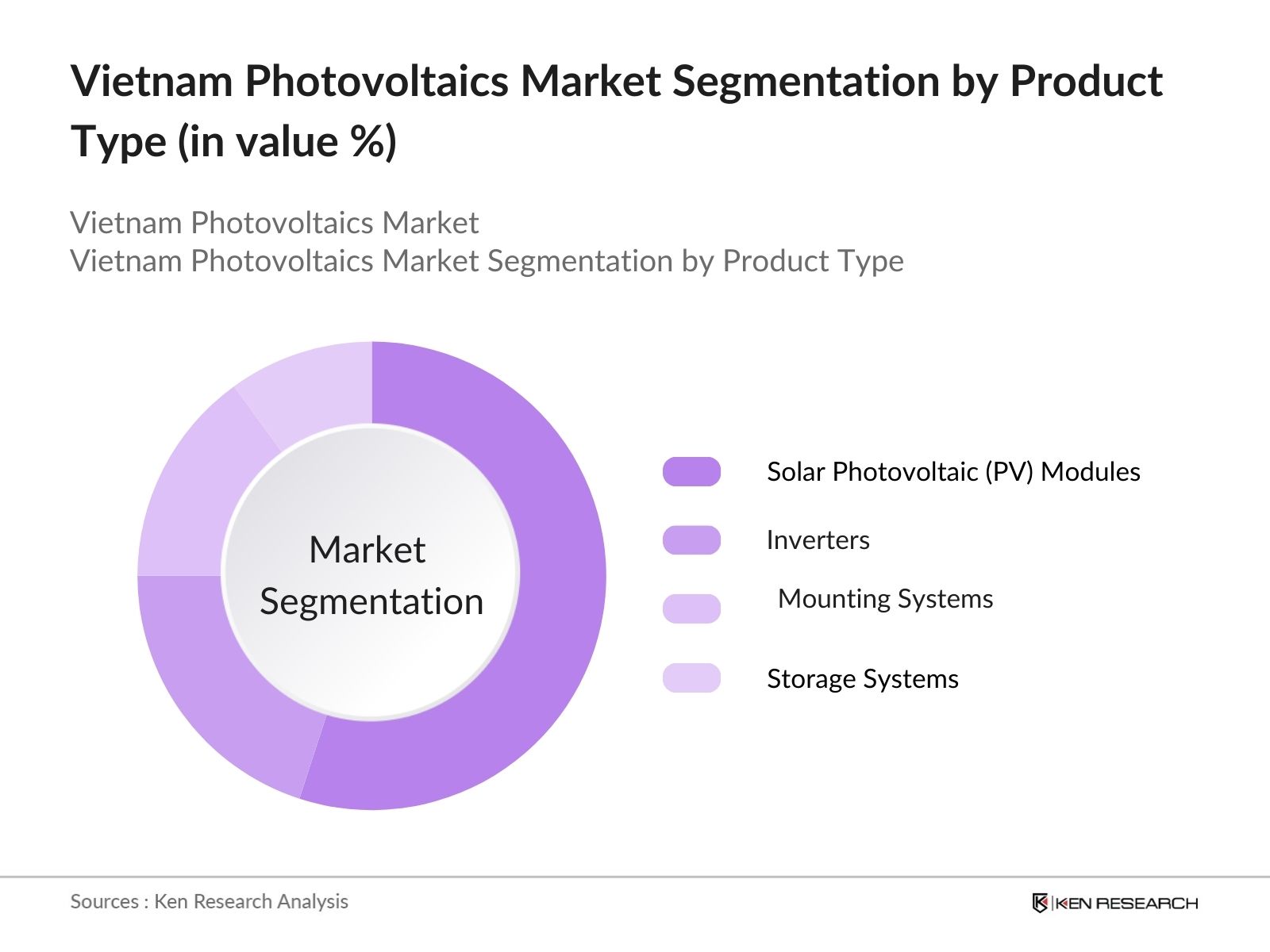

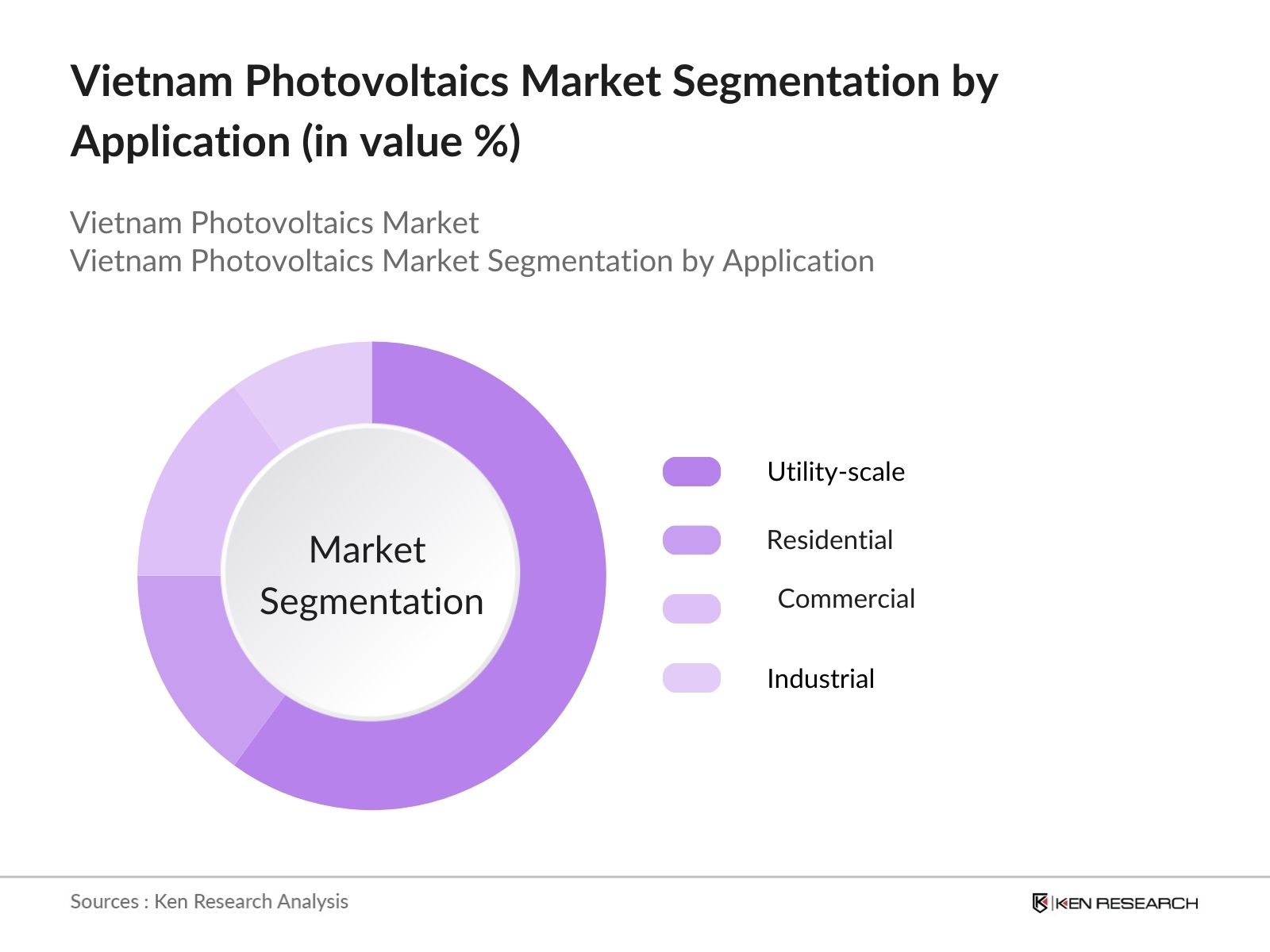

Vietnam Photovoltaics Market Segmentation

The Vietnam photovoltaics market is segmented by product type and by application.

- By Product Type: The market is segmented by product type into solar photovoltaic (PV) modules, inverters, mounting systems, and storage systems. Recently, solar photovoltaic (PV) modules hold the dominant market share under this segmentation. This is due to the continuous decline in the cost of solar PV modules, making them more accessible to both residential and commercial consumers. Additionally, technological advancements in module efficiency, such as bifacial and monocrystalline panels, have contributed to their dominance. In contrast, storage systems are gaining traction, but their high cost has limited widespread adoption so far.

- By Application: The market is further segmented by application into residential, commercial, utility-scale, and industrial. The utility-scale segment dominates the market, driven by large solar farms developed to meet the country's increasing energy demands. The Vietnamese governments FiT program has attracted numerous investors to build large solar farms, leading to rapid growth in this segment. Furthermore, utility-scale installations benefit from economies of scale, which reduce costs compared to smaller residential or commercial projects, making them more financially viable.

Vietnam Photovoltaics Market Competitive Landscape

The Vietnam photovoltaics market is dominated by key local and international players. Major companies include First Solar, JA Solar Technology, and Trina Solar, which have strong market positions due to their technological innovation and cost-efficient solutions. These companies dominate the market with high-efficiency solar modules and have established long-term partnerships with project developers across Vietnam. This market consolidation highlights the significant influence of these firms, although local companies like SolarBK are starting to make notable contributions by focusing on rooftop installations and smaller-scale projects.

|

Company Name |

Establishment Year |

Headquarters |

Manufacturing Capacity |

R&D Investments |

Market Penetration |

ESG Initiatives |

Global Reach |

Key Projects |

|

First Solar |

1999 |

Tempe, USA |

||||||

|

JA Solar Technology Co., Ltd. |

2005 |

Beijing, China |

||||||

|

Trina Solar Limited |

1997 |

Changzhou, China |

||||||

|

Sungrow Power Supply Co., Ltd. |

1997 |

Hefei, China |

||||||

|

SolarBK |

2006 |

Ho Chi Minh City, VN |

Vietnam Photovoltaics Industry Analysis

Growth Drivers

- Renewable Energy Policies (Governmental Support, PPA mechanisms): Vietnam's renewable energy policies have been pivotal in driving the photovoltaic (PV) market growth. The government's commitment to achieving 21% renewable energy in total energy consumption by 2030 has translated into robust support mechanisms, such as the feed-in-tariff (FiT) for solar projects and Power Purchase Agreements (PPAs). The FiT for solar power in Vietnam was set at VND 2,086/kWh ($0.09/kWh) for ground-mounted projects until the end of 2020, and extensions for new projects continue to encourage investment. Additionally, the Ministry of Industry and Trade (MoIT) forecasts that solar capacity will increase to 20 GW by 2030.

- Declining Costs of Solar Technology (Cost-competitiveness, Module Prices): The declining costs of solar technology have accelerated the adoption of photovoltaics in Vietnam. In 2022, the cost of photovoltaic modules dropped globally by over 85% since 2010, making solar energy more cost-competitive than conventional power sources. Vietnam benefits from lower import tariffs on solar modules, making large-scale adoption economically feasible. According to the International Renewable Energy Agency (IRENA), the levelized cost of electricity (LCOE) for solar PV in Vietnam has reached $0.066/kWh, significantly lower than coal-fired generation.

- Rising Demand for Energy Independence (Energy Security): Energy independence is a critical priority for Vietnam, as it seeks to reduce reliance on fossil fuel imports and ensure energy security amid growing electricity demand. In 2022, Vietnam's electricity consumption reached 234 TWh, with demand expected to grow annually by 10%. The national energy security plan aims to diversify energy sources, including increasing solar capacity to mitigate risks associated with import dependency. Vietnams coal imports, for example, rose to 56 million tons in 2022, underscoring the need for energy diversification through renewables like solar.

Market Challenges

- Regulatory Hurdles (Permitting Delays, Grid Capacity Constraints): Regulatory hurdles, including prolonged permitting processes and grid capacity limitations, continue to challenge the PV market. Vietnams National Load Dispatch Center (NLDC) reported that by the end of 2022, nearly 20% of installed solar capacity faced curtailment due to grid congestion. The delays in project approvals from the Ministry of Planning and Investment (MPI) further exacerbate project timelines. Additionally, Vietnam's grid infrastructure requires an estimated $15 billion investment by 2030 to handle new renewable capacities, including solar.

- High Initial Investment (Capital Costs, ROI Period): While solar technology costs have decreased, the high initial capital outlay remains a challenge, especially for utility-scale projects. The average cost to develop 1 MW of solar capacity in Vietnam is approximately $700,000, according to MoIT. Furthermore, the return on investment (ROI) period for photovoltaic systems, though reduced, still spans over 10 years for many projects, depending on FiT rates and other incentives. These financial burdens are particularly significant for smaller developers and individual investors.

Vietnam Photovoltaics Market Future Outlook

Over the next five years, the Vietnam photovoltaics market is expected to witness continued robust growth. This growth will be driven by ongoing government support through incentives like power purchase agreements (PPAs) and updated feed-in tariffs, alongside declining solar technology costs. Moreover, increasing corporate demand for renewable energy, advancements in storage technologies, and integration with grid modernization projects are expected to enhance market performance. The focus will likely shift towards rooftop solar and hybrid systems, with emerging trends pointing to higher adoption of energy storage solutions and AI-based solar management systems.

Future Market Opportunities

- Technological Innovations (High-Efficiency Solar Panels, Bifacial Technology): Technological advancements, particularly in high-efficiency solar panels and bifacial technology, present significant growth opportunities for Vietnams PV market. The International Energy Agency (IEA) reported in 2023 that bifacial solar modules, which generate power from both sides, offer up to 30% more efficiency compared to traditional modules. In Vietnam, the adoption of such technologies is projected to increase by 15% annually as developers seek to maximize power output in limited spaces, particularly in regions like Ninh Thuan and Binh Thuan provinces.

- Cross-border Power Trade (Energy Export Opportunities): Vietnam is exploring cross-border power trade opportunities, particularly with neighboring countries like Laos and Cambodia, where energy demand is growing rapidly. In 2022, Vietnam signed agreements to export 3,000 MW of electricity to Laos by 2030. Solar energy will play a pivotal role in these export strategies, given its abundance and cost-competitiveness. Expanding solar capacity in border regions can allow Vietnam to meet domestic needs while tapping into the lucrative cross-border energy markets.

Scope of the Report

|

Solar Photovoltaic (PV) Modules Inverters Mounting Systems Storage Systems |

|

|

By Application |

Residential Commercial Utility-scale Industrial |

|

By Technology |

Crystalline Silicon Thin Film Concentrated Photovoltaics |

|

By Grid Connectivity |

On-grid Off-grid |

|

By Region |

North East West South |

Products

Key Target Audience

Independent Power Producers (IPPs)

Renewable Energy Investors and Venture Capitalist Firms

Government and Regulatory Bodies (Vietnam Ministry of Industry and Trade, EVN - Electricity of Vietnam)

Photovoltaic Module Manufacturers

Energy Storage System Providers

Solar Farm Developers

Rooftop Solar Installation Companies

Energy Infrastructure Developers and Grid Operators

Banks and Financial Institutes

Companies

Players Mention in the Report:

First Solar

JA Solar Technology Co., Ltd.

Trina Solar Limited

SunPower Corporation

Canadian Solar Inc.

Jinko Solar Holding Co., Ltd.

LONGi Green Energy Technology Co., Ltd.

Sungrow Power Supply Co., Ltd.

Hanwha Q CELLS

GCL-Poly Energy Holdings Limited

ABB Ltd.

Sharp Corporation

Solaria Corporation

Tesla, Inc.

Huawei Technologies Co., Ltd.

Table of Contents

1. Vietnam Photovoltaics Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Vietnam Photovoltaics Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Vietnam Photovoltaics Market Analysis

3.1. Growth Drivers

3.1.1. Renewable Energy Policies (Governmental Support, PPA mechanisms)

3.1.2. Declining Costs of Solar Technology (Cost-competitiveness, Module Prices)

3.1.3. Rising Demand for Energy Independence (Energy Security)

3.1.4. Corporate Sustainability Goals (Decarbonization)

3.2. Market Challenges

3.2.1. Regulatory Hurdles (Permitting Delays, Grid Capacity Constraints)

3.2.2. High Initial Investment (Capital Costs, ROI Period)

3.2.3. Land Availability and Competition (Land-use conflicts)

3.3. Opportunities

3.3.1. Technological Innovations (High-Efficiency Solar Panels, Bifacial Technology)

3.3.2. Cross-border Power Trade (Energy Export Opportunities)

3.3.3. Floating Solar Installations (Reservoir Usage, Water Bodies)

3.4. Trends

3.4.1. Adoption of Battery Storage Systems (Energy Storage Solutions)

3.4.2. Integration of AI and IoT in Solar Monitoring (Predictive Maintenance)

3.4.3. Hybrid Renewable Energy Systems (Solar + Wind, Solar + Hydro)

3.5. Government Regulation

3.5.1. Solar Power Purchase Agreements (PPA Models, Contract Structures)

3.5.2. Feed-in Tariff (FiT) Adjustments (FiT Levels, Expiry and Changes)

3.5.3. Incentives for Rooftop Solar Installations (Tax Breaks, Subsidies)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Developers, Investors, EPC Contractors)

3.8. Porters Five Forces (Bargaining Power of Suppliers, Threat of Substitutes, etc.)

3.9. Competition Ecosystem

4. Vietnam Photovoltaics Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Solar Photovoltaic (PV) Modules

4.1.2. Inverters

4.1.3. Mounting Systems

4.1.4. Storage Systems

4.2. By Application (In Value %)

4.2.1. Residential

4.2.2. Commercial

4.2.3. Utility-scale

4.2.4. Industrial

4.3. By Technology (In Value %)

4.3.1. Crystalline Silicon (Monocrystalline, Polycrystalline)

4.3.2. Thin Film (Cadmium Telluride, Amorphous Silicon, Copper Indium Gallium Selenide)

4.3.3. Concentrated Photovoltaics (CPV)

4.4. By Grid Connectivity (In Value %)

4.4.1. On-grid

4.4.2. Off-grid

4.5. By Region (In Value %)

4.5.1. North

4.5.2. East

4.5.3. South

4.5.4. West

5. Vietnam Photovoltaics Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. First Solar

5.1.2. JA Solar Technology Co., Ltd.

5.1.3. Trina Solar Limited

5.1.4. SunPower Corporation

5.1.5. Canadian Solar Inc.

5.1.6. Jinko Solar Holding Co., Ltd.

5.1.7. LONGi Green Energy Technology Co., Ltd.

5.1.8. Sungrow Power Supply Co., Ltd.

5.1.9. Hanwha Q CELLS

5.1.10. GCL-Poly Energy Holdings Limited

5.1.11. ABB Ltd.

5.1.12. Sharp Corporation

5.1.13. Solaria Corporation

5.1.14. Tesla, Inc.

5.1.15. Huawei Technologies Co., Ltd.

5.2 Cross Comparison Parameters (Manufacturing Capacity, Global Reach, Technology Partnerships, Cost Competitiveness, Efficiency of Products, Market Penetration, ESG Initiatives, Innovation Pipeline)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Vietnam Photovoltaics Market Regulatory Framework

6.1. Solar Energy Standards (Grid Code Compliance, Technical Standards)

6.2. Compliance Requirements (Environmental Impact Assessments, Licensing)

6.3. Certification Processes (Product Certifications, ISO Standards)

7. Vietnam Photovoltaics Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Vietnam Photovoltaics Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By Grid Connectivity (In Value %)

8.5. By Region (In Value %)

9. Vietnam Photovoltaics Market Analysts Recommendations

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2. Consumer Preference Analysis

9.3. Marketing Initiatives and Strategies

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves the construction of an ecosystem map for the Vietnam photovoltaics market, identifying key stakeholders including energy companies, policymakers, and equipment manufacturers. This step is based on extensive desk research and primary interviews with industry experts, enabling the identification of key market dynamics and drivers.

Step 2: Market Analysis and Construction

In this phase, historical data on market performance and growth trends are collected and analyzed. We also assess solar penetration, energy output statistics, and analyze key challenges such as grid connectivity and land acquisition issues. Detailed analysis of revenue generation across various market segments is also conducted.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses about the market trends and dynamics are developed and validated through interviews with industry insiders, including solar farm developers, regulatory bodies, and technical experts. These consultations provide valuable insights into operational and financial performance, confirming data accuracy and reliability.

Step 4: Research Synthesis and Final Output

This final phase involves direct interaction with solar technology manufacturers and large-scale project developers to collect detailed insights on installation rates, performance metrics, and emerging technologies. The data collected from both bottom-up and top-down approaches are synthesized to provide an accurate and comprehensive view of the market.

Frequently Asked Questions

01. How big is the Vietnam Photovoltaics Market?

The Vietnam photovoltaics market is valued at USD 1.6 billion, driven by supportive government policies, declining solar technology costs, and rising energy demand.

02. What are the key challenges in the Vietnam Photovoltaics Market?

The key challenges in Vietnam photovoltaics market include regulatory hurdles such as grid connectivity issues, land acquisition challenges for large-scale projects, and the high upfront cost of solar installations.

03. Who are the major players in the Vietnam Photovoltaics Market?

The major players in Vietnam photovoltaics market include First Solar, JA Solar, Trina Solar, and local companies like SolarBK. These companies dominate the market due to their advanced technology offerings and extensive project portfolios.

04. What are the growth drivers of the Vietnam Photovoltaics Market?

The Vietnam photovoltaics market is driven by declining solar panel costs, government incentives like feed-in tariffs, and rising demand for energy independence. Corporate sustainability goals and the focus on renewable energy also contribute to market growth.

05. What are the dominant application segments in the Vietnam Photovoltaics Market?

The utility-scale segment dominates due to large solar farm developments supported by government policies, followed by the residential and commercial segments focusing on rooftop installations.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.