Vietnam Refrigerants Market Outlook to 2030

Region:Asia

Author(s):Mukul

Product Code:KROD3920

October 2024

80

About the Report

Vietnam Refrigerants Market Overview

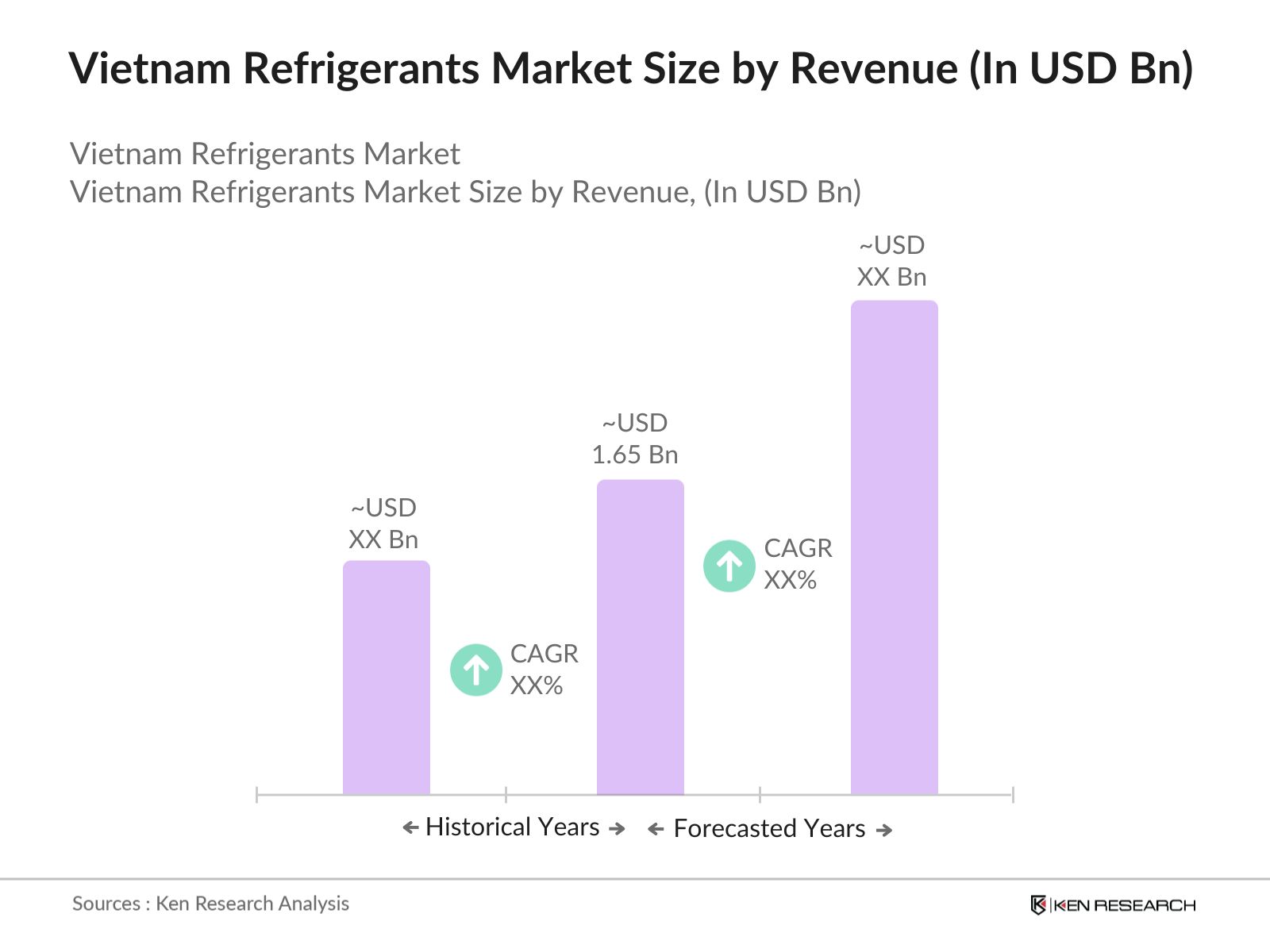

The Vietnam refrigerants market size by revenue USD 1.65 billion, based on a five-year historical analysis. This market is driven by the increasing demand for efficient cooling systems in residential, commercial, and industrial applications. As Vietnam experiences growth in infrastructure development, the need for HVAC systems and refrigeration solutions continues to rise, pushing the demand for both traditional and eco-friendly refrigerants. Additionally, government regulations favoring the phase-out of harmful refrigerants like HCFCs contribute to market expansion.

Key cities such as Ho Chi Minh City and Hanoi dominate the Vietnam refrigerants market due to their rapid urbanization and growing commercial sectors. These cities have witnessed a boom in commercial real estate, hospitality, and retail sectors, which are highly dependent on advanced cooling systems. Moreover, industrial hubs like Haiphong are becoming central to Vietnams growth, requiring significant refrigeration solutions for logistics, food processing, and manufacturing.

Vietnam is actively phasing out HCFCs as part of its HCFC Phase-out Management Plan, in accordance with the Montreal Protocol. The Ministry of Natural Resources and Environment reported that Vietnam had successfully reduced HCFC consumption by 35% by 2023 and aims to completely phase out these refrigerants by 2025. This program is creating new opportunities for low-GWP refrigerant suppliers, as businesses are compelled to adopt eco-friendly alternatives to meet regulatory requirements.

Vietnam Refrigerants Market Segmentation

By Product Type: The Vietnam refrigerants market is segmented by product type into fluorocarbons, inorganics, and hydrocarbons. Fluorocarbons hold a dominant market share under the segmentation by product type, largely due to their wide applications in air conditioning and refrigeration systems. Fluorocarbon-based refrigerants, such as HFCs and HCFCs, are well-established in Vietnams HVAC industry. Despite global regulations to phase out harmful refrigerants, their cost-effectiveness and efficiency continue to make them a favored choice for both residential and commercial cooling systems.

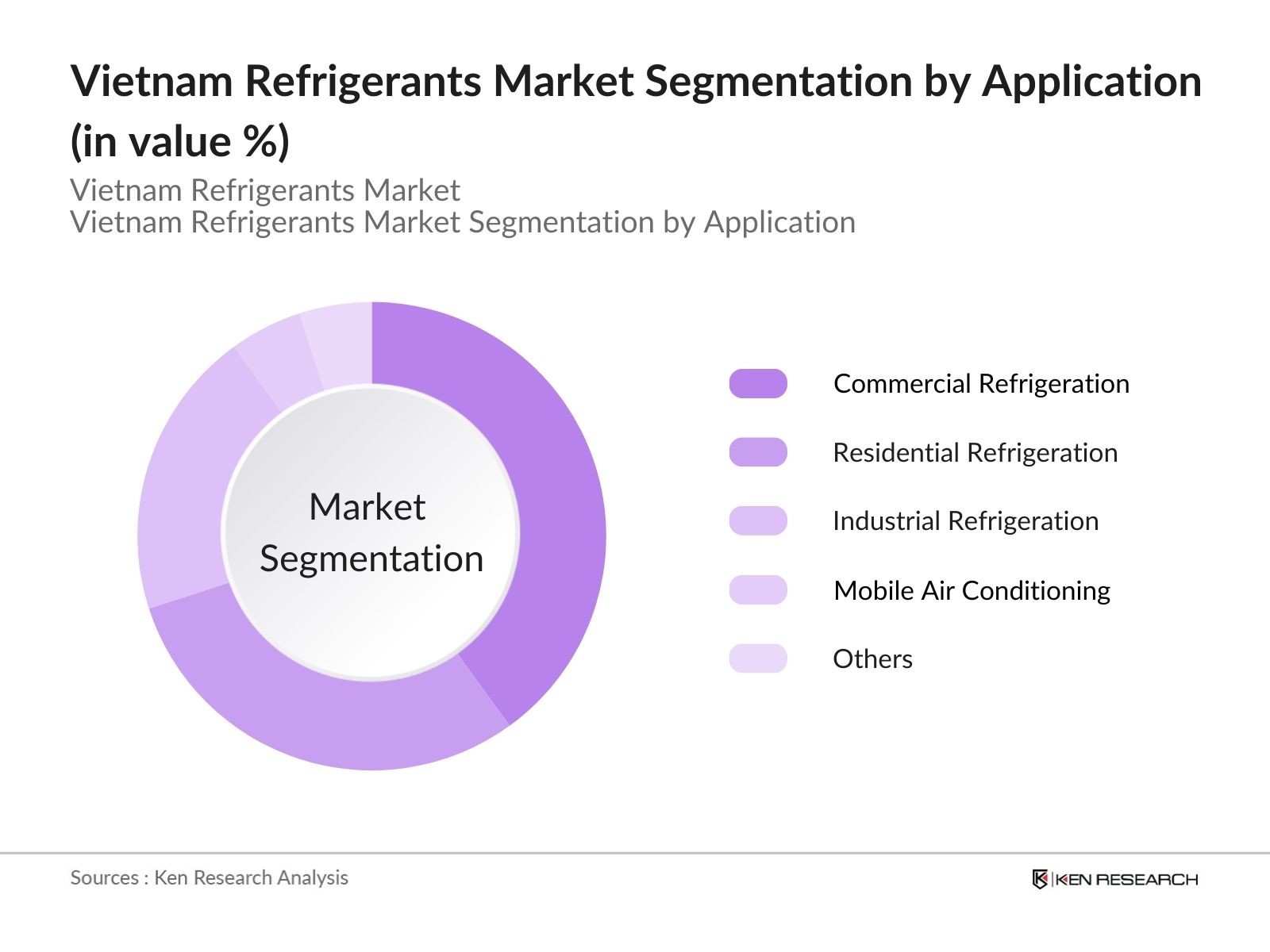

By Application: The Vietnam refrigerants market is also segmented by application into residential refrigeration, commercial refrigeration, industrial refrigeration, mobile air conditioning, and others (transport refrigeration, data centers). Commercial refrigeration holds a dominant market share in this segment due to the expanding retail and foodservice industries in Vietnam. As supermarkets, hypermarkets, and food delivery services grow across urban and suburban areas, the need for efficient and reliable refrigeration systems intensifies.

Vietnam Refrigerants Market Competitive Landscape

The Vietnam refrigerants market is characterized by a mix of global and local players, each contributing to the evolving competitive landscape. The market is dominated by international brands such as Honeywell and Daikin, who have established strong footholds with eco-friendly refrigerants and extensive distribution networks. Meanwhile, domestic manufacturers are rising due to their localized solutions, tailored for Vietnams specific climatic and regulatory conditions.

|

Company |

Year Established |

Headquarters |

Revenue (USD Mn) |

APAC Market Presence |

Employees |

Key Services |

Recent Developments |

API Integration |

Cloud-Based Solutions |

|

Honeywell International Inc. |

1906 |

Charlotte, USA |

|||||||

|

Daikin Industries, Ltd. |

1924 |

Osaka, Japan |

|||||||

|

The Chemours Company |

2015 |

Wilmington, USA |

|||||||

|

Dongyue Group Co., Ltd. |

1987 |

Zibo, China |

|||||||

|

Sinochem Group Co., Ltd. |

1950 |

Beijing, China |

Vietnam Refrigerants Industry Analysis

Vietnam Refrigerants Market Growth Drivers

- Increasing Demand in HVAC Systems: The growing industrial sector in Vietnam is driving the demand for HVAC systems, with a significant rise in commercial real estate projects. The HVAC market, particularly in urban areas like Ho Chi Minh City and Hanoi, is experiencing growth due to rising construction activities. According to the General Statistics Office of Vietnam, the country's construction sector grew by 9.6% in 2023. This has led to increased demand for refrigerants, particularly in large-scale HVAC systems for industrial and commercial buildings, contributing to the growth of the refrigerants market. Source: General Statistics Office of Vietnam

- Government Regulations on Eco-Friendly Refrigerants: Vietnam is increasingly enforcing regulations to reduce its carbon footprint, in line with its National Action Plan on Climate Change. The government's commitment to phasing out ozone-depleting substances has led to restrictions on the use of hydrofluorocarbons (HFCs), encouraging the adoption of low-GWP (Global Warming Potential) refrigerants. Vietnams HCFC Phase-out Management Plan aims to reduce consumption by 35% in 2025, which is driving the adoption of eco-friendly alternatives such as CO2 and ammonia. This regulatory push is essential in transitioning to more sustainable refrigerant solutions.

- Expansion of Cold Chain Logistics: Vietnam's cold chain logistics sector is rapidly expanding due to increased demand for frozen and refrigerated food products, driven by the growth in urbanization and the foodservice industry. With approximately 75% of Vietnam's population living in urban areas, demand for cold storage solutions has surged. The market for refrigerated transport has grown alongside, necessitating advanced refrigerants for cooling systems. According to the Vietnam Logistics Business Association, the cold storage capacity grew by 12% in 2023, further amplifying the need for reliable and efficient refrigerants.

Vietnam Refrigerants Market Restraints

-

Environmental Concerns Regarding HFCs: Vietnam's reliance on HFCs for refrigeration systems is becoming increasingly problematic due to their high GWP and harmful environmental impacts. HFC emissions are a significant concern, contributing to global warming and violating international agreements like the Kigali Amendment. The Ministry of Natural Resources and Environment reported that Vietnam emitted 2.7 million tons of CO2 equivalent through HFCs in 2023. This poses a challenge for businesses that need to comply with both domestic and international environmental regulations, pushing them toward alternative refrigerants.

- Lack of Skilled Workforce in Sustainable Refrigeration: Vietnam is facing a shortage of skilled workers knowledgeable in sustainable refrigeration technologies. According to the Ministry of Labor, Invalids, and Social Affairs, Vietnams technical workforce, particularly in the refrigeration sector, lacks adequate training in handling advanced refrigerants like ammonia and CO2. This gap in expertise limits the country's ability to fully transition to eco-friendly refrigerants, as businesses struggle to find qualified technicians for system installations and maintenance. The Ministry is launching vocational training programs to address this issue, but the shortage remains a challenge.

Vietnam Refrigerants Market Future Outlook

Over the next five years, the Vietnam refrigerants market is expected to show significant growth driven by government initiatives toward eco-friendly refrigerants, increased demand for cooling solutions in the commercial and industrial sectors, and advancements in refrigerant technology. As urbanization continues, along with the expansion of cold chain logistics and data centers, the demand for refrigerants will experience sustained growth. Furthermore, rising environmental awareness and the regulatory push for phasing out HCFCs and HFCs will accelerate the adoption of low-GWP and natural refrigerants.

Market Opportunities

Growing Adoption of Low-GWP Refrigerants: The transition to low-GWP refrigerants presents a substantial opportunity for growth in Vietnam's refrigerants market. Low-GWP options like ammonia and CO2 are gaining popularity, especially in large-scale industrial applications such as cold storage and processing facilities. The Ministry of Industry and Trade reported that, as of 2023, over 40% of new refrigeration systems in industrial sectors are utilizing low-GWP refrigerants, which presents a lucrative opportunity for manufacturers and suppliers in this space.

International Collaborations and Joint Ventures: International partnerships are becoming a key growth driver for the refrigerants market in Vietnam. Collaborations with global companies specializing in eco-friendly refrigeration technologies are on the rise. For instance, Japans Ministry of Economy, Trade, and Industry has initiated multiple joint ventures in Vietnam to develop sustainable refrigerant solutions. These partnerships provide Vietnam access to cutting-edge technology and expertise, which will boost domestic production and adoption of advanced refrigerants. In 2023, foreign investments in Vietnams refrigeration sector reached $500 million, highlighting the market potential for such collaborations. Source: Japans Ministry of Economy, Trade, and Industry

Scope of the Report

|

By Product Type |

Fluorocarbons (HFCs, HCFCs) |

|

Inorganics (CO2, Ammonia) |

|

|

Hydrocarbons (Propane, Isobutane) |

|

|

Other Types (HFOs, Blends) |

|

|

By Application |

Residential Refrigeration |

|

Commercial Refrigeration |

|

|

Industrial Refrigeration |

|

|

Mobile Air Conditioning |

|

|

Others (Transport Refrigeration, Data Centers) |

|

|

By End-user |

HVAC |

|

Automotive |

|

|

Food and Beverage |

|

|

Healthcare |

|

|

Cold Chain Logistics |

|

|

By Environmental Impact |

Low GWP (Global Warming Potential) |

|

Zero ODP (Ozone Depletion Potential) |

|

|

By Region |

North Vietnam |

|

Central Vietnam |

|

|

South Vietnam |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

HVAC Manufacturers

Refrigeration System Providers

Automotive Manufacturers

Food and Beverage Processing Companies

Cold Chain Logistics Companies

Data Center Operators

Government and Regulatory Bodies (Vietnam Ministry of Natural Resources and Environment, Vietnam Ministry of Industry and Trade)

Investments and Venture Capitalist Firms

Time Period Captured in the Report:

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

Honeywell International Inc.

Daikin Industries, Ltd.

The Chemours Company

Dongyue Group Co., Ltd.

Sinochem Group Co., Ltd.

Arkema S.A.

Gujarat Fluorochemicals Limited

Tazzetti S.p.A.

Harp International Ltd.

Zhejiang Juhua Co., Ltd.

SRF Limited

Asahi Glass Company (AGC)

Orbia (Formerly Mexichem)

The Linde Group

A-Gas International

Table of Contents

Vietnam Refrigerants Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

Vietnam Refrigerants Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

Vietnam Refrigerants Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Demand in HVAC Systems

3.1.2. Government Regulations on Eco-Friendly Refrigerants

3.1.3. Expansion of Cold Chain Logistics

3.1.4. Technological Innovations in Refrigerant Systems

3.2. Market Challenges

3.2.1. High Costs of Advanced Refrigerants

3.2.2. Environmental Concerns Regarding HFCs

3.2.3. Lack of Skilled Workforce in Sustainable Refrigeration

3.3. Opportunities

3.3.1. Growing Adoption of Low-GWP Refrigerants

3.3.2. International Collaborations and Joint Ventures

3.3.3. Rising Refrigerant Demand in Data Centers

3.4. Trends

3.4.1. Shift Towards Natural Refrigerants (CO2, Ammonia, Hydrocarbons)

3.4.2. Growth of IoT-Integrated Refrigerant Management Systems

3.4.3. Development of Non-Flammable Refrigerants

3.5. Government Regulation

3.5.1. Vietnams National Action Plan on Climate Change

3.5.2. Refrigerant Phase-out Programs (HCFC Phase-out Management Plan)

3.5.3. Import/Export Regulations for Refrigerants

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Manufacturers, Distributors, End-users)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

Vietnam Refrigerants Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Fluorocarbons (HFCs, HCFCs)

4.1.2. Inorganics (CO2, Ammonia)

4.1.3. Hydrocarbons (Propane, Isobutane)

4.1.4. Other Types (HFOs, Blends)

4.2. By Application (In Value %)

4.2.1. Residential Refrigeration

4.2.2. Commercial Refrigeration

4.2.3. Industrial Refrigeration

4.2.4. Mobile Air Conditioning

4.2.5. Others (Transport Refrigeration, Data Centers)

4.3. By End-user (In Value %)

4.3.1. HVAC

4.3.2. Automotive

4.3.3. Food and Beverage

4.3.4. Healthcare

4.3.5. Cold Chain Logistics

4.4. By Environmental Impact (In Value %)

4.4.1. Low GWP (Global Warming Potential)

4.4.2. Zero ODP (Ozone Depletion Potential)

4.5. By Region (In Value %)

4.5.1. North Vietnam

4.5.2. Central Vietnam

4.5.3. South Vietnam

Vietnam Refrigerants Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. The Chemours Company

5.1.2. Honeywell International Inc.

5.1.3. Daikin Industries, Ltd.

5.1.4. Arkema S.A.

5.1.5. Dongyue Group Co., Ltd.

5.1.6. Orbia (Formerly Mexichem)

5.1.7. Sinochem Group Co., Ltd.

5.1.8. The Linde Group

5.1.9. Asahi Glass Company (AGC)

5.1.10. Zhejiang Juhua Co., Ltd.

5.1.11. Gujarat Fluorochemicals Limited

5.1.12. Harp International Ltd.

5.1.13. SRF Limited

5.1.14. Tazzetti S.p.A.

5.1.15. A-Gas International

5.2. Cross Comparison Parameters (Revenue, Product Portfolio, Innovation Index, Market Presence, Green Certifications, Partnerships, Number of Employees, Headquarters)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

Vietnam Refrigerants Market Regulatory Framework

6.1. Environmental Standards (Montreal Protocol, Kigali Amendment Compliance)

6.2. Compliance Requirements (Safety Standards, Energy Efficiency)

6.3. Certification Processes (Green Certifications for Low GWP Refrigerants)

Vietnam Refrigerants Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

Vietnam Refrigerants Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-user (In Value %)

8.4. By Environmental Impact (In Value %)

8.5. By Region (In Value %)

Vietnam Refrigerants Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

In this phase, we map out the entire stakeholder ecosystem within the Vietnam refrigerants market. This involves conducting thorough desk research utilizing proprietary and secondary databases to gather comprehensive information. The primary objective is to identify key market drivers, inhibitors, and other variables influencing market growth.

Step 2: Market Analysis and Construction

We then assess historical data, focusing on market penetration rates and refrigerant consumption across sectors such as residential, commercial, and industrial. Data on refrigerant production and imports will be cross-referenced with local regulatory standards to ensure consistency and accuracy in market sizing.

Step 3: Hypothesis Validation and Expert Consultation

To validate our market insights, we consult industry experts through computer-assisted telephone interviews (CATIs). These consultations provide crucial on-ground perspectives from key players in the refrigerants market, enhancing our understanding of operational and financial dynamics.

Step 4: Research Synthesis and Final Output

Finally, we synthesize the collected data, combining quantitative and qualitative insights to form a comprehensive overview of the market. This final output is cross-validated with primary sources such as manufacturers, distributors, and regulatory bodies to ensure the highest level of accuracy and reliability.

Frequently Asked Questions

01. How big is the Vietnam Refrigerants Market?

The Vietnam refrigerants market size by revenue USD 1.65 billion, is driven by increasing demand for HVAC systems and the rise in industrial refrigeration solutions, particularly in commercial and retail sectors.

02. What are the challenges in the Vietnam Refrigerants Market?

Challenges include the high cost of eco-friendly refrigerants, lack of skilled technicians for managing new refrigerant technologies, and stringent environmental regulations regarding HFCs and HCFCs.

03. Who are the major players in the Vietnam Refrigerants Market?

Key players include Honeywell International Inc., Daikin Industries, Ltd., The Chemours Company, Dongyue Group Co., Ltd., and Sinochem Group Co., Ltd. These companies dominate the market due to their technological innovations and extensive product portfolios.

04. What are the growth drivers of the Vietnam Refrigerants Market?

The market is propelled by factors such as government regulations on eco-friendly refrigerants, growing demand for cooling solutions in residential and commercial sectors, and the expansion of cold chain logistics in Vietnam.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.