Vietnam Vaccine Market Outlook to 2029

Region:Asia

Author(s):Shashank, Kartika

Product Code:KR1493

April 2025

80-100

About the Report

Listen to the audio summary

Vietnam Vaccine Market Overview

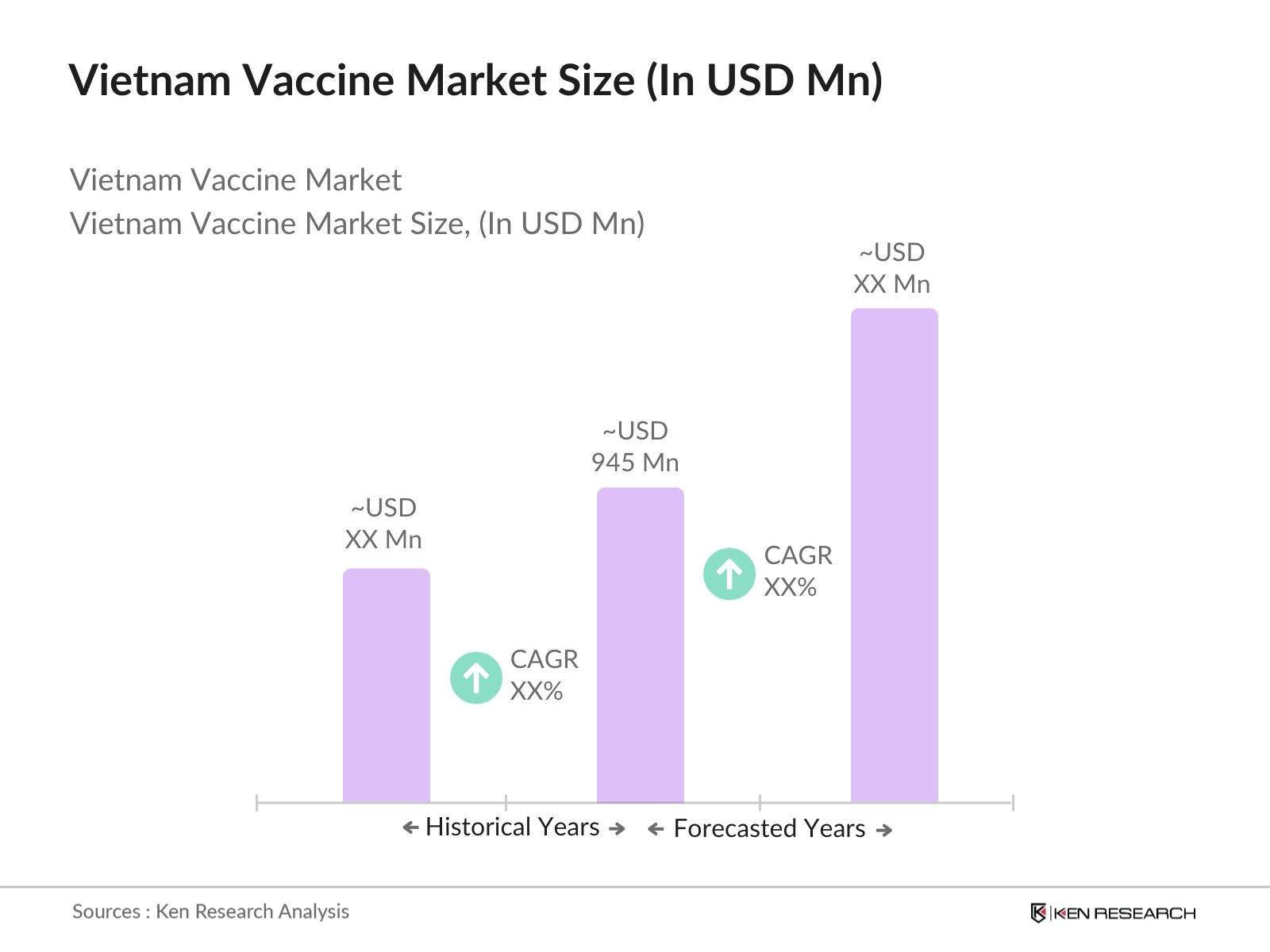

The Vietnam Vaccine Market is valued at USD 945 million, based on a five-year historical analysis. The market has shown consistent growth due to increased government funding under the Expanded Program on Immunization (EPI), rising private sector participation, and growing demand for life-course immunization across adult and geriatric populations. With higher awareness and income levels, the demand for paid vaccines outside EPI, such as HPV and influenza, has surged, supported by improved domestic production capacity and expanded public-private distribution networks.

The Vietnam Vaccine Market is geographically concentrated in regions like the Red River Delta and the North Central & Central Coast, driven by their large urban populations and medical infrastructure. These two regions collectively house over 5,600 healthcare facilities and account for 47% of Vietnams medical infrastructure. Major cities such as Hanoi, Hai Phong, and Da Nang act as immunization hubs due to high disease awareness, consistent public health outreach, and better access to routine and paid vaccination programs. The presence of medical universities, regulatory bodies, and supply chain readiness further reinforces their dominance in the national vaccine landscape.

The Vietnamese government has reinforced vaccine regulations under the Expanded Program on Immunization (EPI) by enhancing domestic capabilities. In 2023, the Ministry of Health committed to producing at least 20 types of vaccines through local manufacturers using 30 production technologies. Additionally, Vietnam maintains strict oversight through provincial CDCs and mandates licensing for all private and public vaccination centers, ensuring compliance with safety and quality norms across the ecosystem.

Vietnam Vaccine Market Segmentation

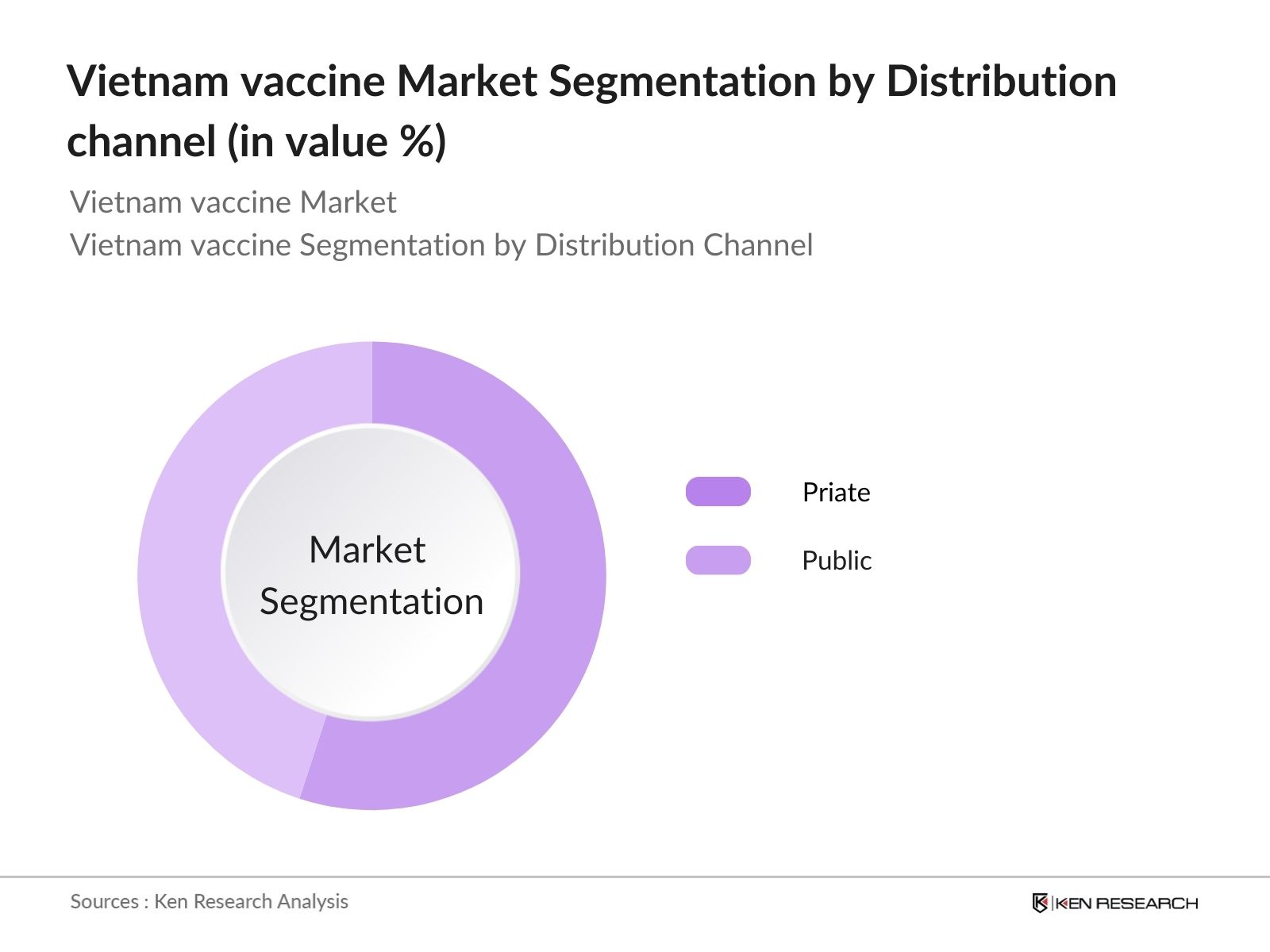

By Distribution Channel: Vietnam Vaccine Market is segmented by distribution channel into Public Sector and Private Sector. The public sector dominates due to the national EPI network covering all 63 provinces. Over 14,000 government-linked vaccination sites operate under CDC supervision. However, the private sector is rapidly expanding in urban areas, offering paid vaccines through hospitals and retail chains, meeting rising consumer demand for premium immunization services.

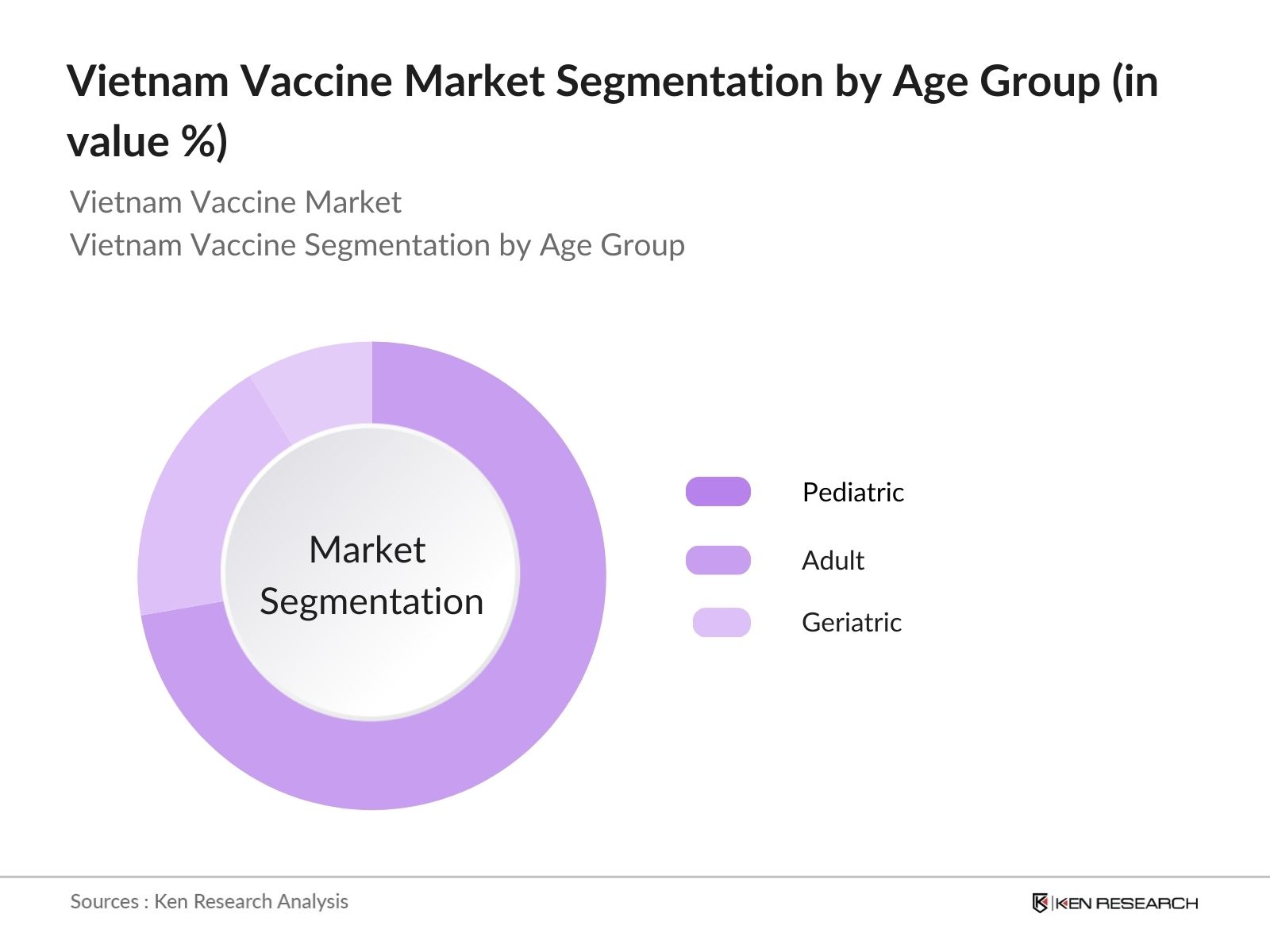

By Age Group: Vietnam Vaccine Market is segmented by age group into Pediatric, Adult, and Geriatric categories. Pediatric vaccines dominate due to high birth cohorts and mandatory early-life immunizations. Over 1.4 million births annually ensure strong recurring demand for BCG, DTP, and polio vaccines. School-based delivery programs and public campaigns further consolidate pediatric dominance, making this the most consistent segment across Vietnams immunization landscape.

Vietnam Vaccine Market Competitive Landscape

The Vietnam Vaccine market is dominated by globally established pharmaceutical companies and a few domestic leaders with state-backed advantages. Players such as MSD, GSK, and Sanofi hold leadership through their extensive vaccine portfolios, global regulatory certifications, and widespread distribution systems. Meanwhile, domestic manufacturer IVAC benefits from government support and public health programs, enhancing its local footprint. Together, these players ensure high coverage through efficient production capabilities and nationwide cold chain-enabled delivery frameworks.

Vietnam Vaccine Market Analysis

Growth Drivers

High Private Sector Involvement: Vietnams vaccine landscape is being reshaped by the emergence of over 2,660 private vaccination sites offering expanded services beyond EPI coverage. These private centers cater to rising consumer preferences for specialized vaccines, thereby broadening market access and improving immunization rates across various income segments.

Expanding Domestic Vaccine Production: The government aims to master 30 vaccine technologies and produce 20 of them domestically by 2030. This push is expected to reduce reliance on imports, stimulate local manufacturing, and meet both domestic and global standards strengthening Vietnams vaccine self-sufficiency.

Increase in Budget for EPI Program: Vietnam has significantly expanded its EPI program from 6 vaccines in 1985 to 14 by 2022. In 2024, the government allocated VND 424.5 Bn to purchase 11 types of vaccines. These initiatives indicate a consistent policy focus on immunization coverage.

Market Challenges

Urban-Rural Disparities in Healthcare Access: Vaccination efforts face a bottleneck in rural Vietnam due to limited access to healthcare professionals and high patient loads in urban hospitals. This disparity leads to lower vaccination rates in remote regions and deepens public health inequalities.

Lack of Cold Chain Facilities: Vietnams vaccine storage capacity particularly in rural areas lags behind demand. With only 16 months of storage coverage and a shortage of ~2,197 required refrigerators, cold chain constraints continue to affect vaccine distribution efficiency and lead to higher wastage.

Vietnam Vaccine Market Future Outlook

Over the next five years, the Vietnam Vaccine market is expected to grow steadily, driven by increasing private sector involvement, ongoing government support for EPI programs, and advancements in domestic vaccine production technologies. Expansion of life-course immunization programs, rising urbanization, and improved healthcare awareness will further fuel demand. Strategic collaborations, local R&D, and mRNA technology transfers are set to enhance vaccine accessibility, especially in underserved regions, ensuring broader national health coverage.

Market Opportunities

Rise in Paid Vaccination Outside EPI: Vietnam is witnessing increasing consumer interest in paid vaccines not included in the EPI. In 2022 alone, over 2,660 private vaccination facilities served rising demand for optional immunizations such as HPV, influenza, and shingles. This trend is amplified by rising income levels and urban health awareness, especially in Hanoi and Ho Chi Minh City. The shift provides long-term expansion for private retail and hospital-based vaccination programs.

Growth in Life-Course Immunization Programs: The Life-Course Immunization initiative is transforming adult vaccine coverage. Vietnams urbanization rate of 45.8%, paired with 4.6% of GDP allocated to healthcare spending in 2023 (GSO), is facilitating vaccine uptake across all age groups. Public and private centers are increasingly offering vaccines for seniors and middle-aged adults to prevent diseases such as hepatitis, pneumonia, and influenza, reflecting a major diversification of the immunization base.

Scope of the Report

|

By Age Group |

Pediatric |

|

By Technology Live |

Live Attenuated |

|

By Distribution |

Private |

|

By Purpose |

Routine/Preventive |

|

By Region |

Red River Delta |

Products

Key Target Audience

Pediatric Healthcare Providers

Private Vaccination Centers

Public Health Authorities

Pharmaceutical Distributors

Adult & Geriatric Care Clinics

Government Immunization Program Managers

Cold Chain & Logistics Providers

Companies

Players Mentioned in the Report

MSD

GSK

Sanofi

Pfizer

IVAC

Table of Contents

1. Vietnam Vaccine Market Overview

1.1. Market Taxonomy

2. Vietnam Vaccine Market Size and Segmentation

2.1. Market Size of Vietnam Vaccine Market (2018–2030F)

2.2. Segmentation by Age Group (2024 & 2030F)

2.3. Segmentation by Technology (2024 & 2030F)

2.4. Segmentation by Purpose (2024 & 2030F)

2.5. Segmentation by Region (2024 & 2030F)

2.6. Segmentation by Distribution Channel (2024 & 2030F)

3. Vietnam Vaccine Industry Analysis

3.1. Vaccination Rate by Major Type of Diseases

3.2. Market Trends and Developments

3.3. Market Challenges

3.4. Porter’s Five Forces Analysis

3.5. Relevant Regulations and Standards for Vaccine Market in Vietnam

4. Vietnam Vaccine Market Competitive Landscape

4.1. Ecosystem of Vietnam Vaccine Market

4.2. Market Share of Key Players (2024)

4.3. Cross Comparison of Key Players in Vietnam Vaccine Market

5. Research Methodology

5.1. Market Definitions and Assumptions

5.2. Abbreviations

5.3. Market Sizing Approach

5.4. Consolidated Research Approach

5.5. Primary Research Approach

5.6. Sample Size Inclusion | Market Sizing

5.7. Research Limitations and Conclusion

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The research began with comprehensive mapping of stakeholders involved in the Vietnam Vaccine market, including manufacturers, government authorities, vaccination retail centers, and healthcare facilities. Secondary research was conducted using sources like company profiles, industry articles, WHO databases, and government reports. Key variables such as vaccine type, target population, channel of distribution, and disease-specific usage were identified to build the foundational hypothesis.

Step 2: Market Analysis and Construction

Historical and forecast data for the period 20182030F was analyzed across segmentation axesage group, vaccine technology, purpose, distribution channel, and region. A bottom-up approach was used, aggregating revenues from individual companies and validating estimates through stakeholder interviews. Additionally, macroeconomic indicators such as Vietnams population growth, healthcare spending, urbanization trends, and immunization targets were factored into market sizing and projections.

Step 3: Hypothesis Validation and Expert Consultation

Ken Research conducted structured CATI interviews with over 50 stakeholders, including C-level executives, directors, and health policy experts. The sample size breakdown was: 50% from vaccine manufacturers, 25% from vaccination retail chains, 15% from health ministry and local department experts, and 10% independent consultants. Interviews focused on pricing, supply-side disruptions, cold chain infrastructure, government policies, and product pipelines. This was supplemented by insights from internal databases and proprietary tools.

Step 4: Research Synthesis and Final Output

All data points were synthesized using triangulation of primary insights, proprietary research tools, and external validation sources like WHO, GAVI, and UNICEF reports. A bottom-up model was used for demand-side and supply-side assessment, which was sanity-checked using top-down benchmarks. The final report incorporated CAGR calculations, regulatory impact, private sector participation, and competitive intensity to deliver a forward-looking and actionable market outlook.

Frequently Asked Questions

01. How big is the Vietnam Vaccine Market?

The Vietnam Vaccine market is valued at USD 945 million in 2024, driven by rising private healthcare spending, expansion of the national immunization program, and growing investments in public health infrastructure.

02. What are the challenges in the Vietnam Vaccine Market?

Vietnam Vaccine market Challenges include urban-rural disparities in healthcare access, with rural areas facing staffing shortages and lower vaccination rates. There is also limited cold chain capacity, with ~2,197 additional refrigerators needed, and high import dependence for specialized vaccines due to underdeveloped domestic production.

03. Who are the major players in the Vietnam Vaccine Market?

Major players in the Vietnam Vaccine market include MSD, GSK, Sanofi, Pfizer, and IVAC. These top five companies collectively dominate the market, with MSD leading due to its broad vaccine portfolio and global presence. Domestic manufacturers such as Vabiotech and Polyvac contribute to the remaining market share, supported by local production capabilities and government collaborations.

04. What are the growth drivers of the Vietnam Vaccine Market?

Growth in the Vietnam Vaccine market is propelled by strong private sector participation, expanding local vaccine manufacturing initiatives, and the implementation of life-course immunization programs aligned with urbanization and improved income levels. Additionally, increased government funding for the national immunization agenda continues to strengthen vaccine accessibility and coverage across the country.

05. Which region dominates the Vietnam Vaccine Market?

The Red River Delta region leads the Vietnam Vaccine market, supported by strong healthcare infrastructure and centralized immunization efforts. It is followed closely by the North Central and Central Coast, Southeast, and Mekong River Delta regions, which benefit from expanding healthcare access, regional public health programs, and increasing vaccination awareness.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.