KSA Carbon Black Market Outlook to 2030

Region:Saudi Arabia

Author(s):Vijay Kumar

Product Code:KROD3373

Region:Saudi Arabia

Author(s):Vijay Kumar

Product Code:KROD3373

December 2024

88

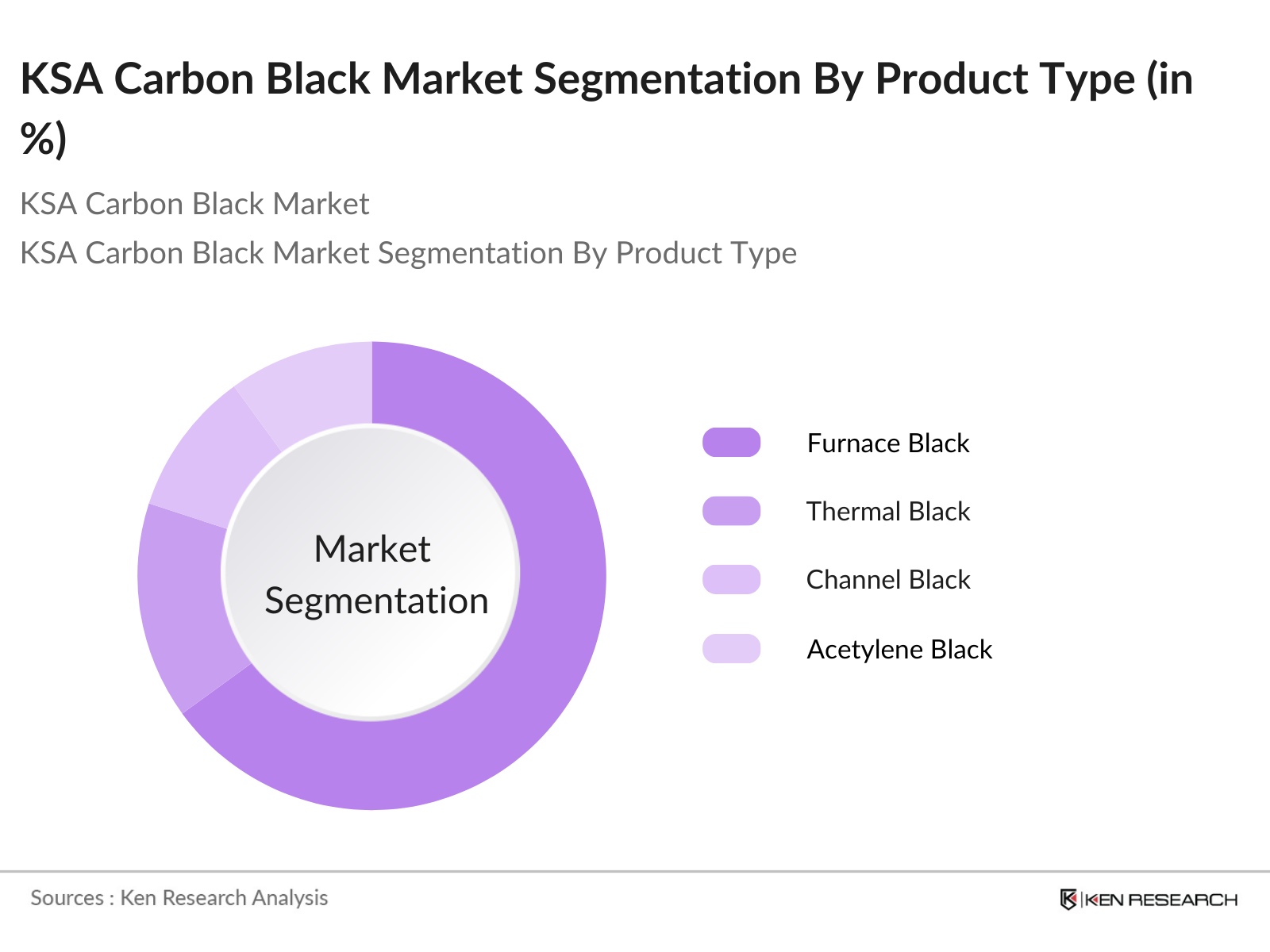

By Product Type: The KSA Carbon Black market is segmented by product type into furnace black, thermal black, channel black, and acetylene black. Furnace black currently holds the dominant market share, due to its extensive application in tire manufacturing and rubber products. This dominance is driven by the cost-effectiveness of the furnace process, which produces carbon black suitable for a wide range of industrial applications, including the automotive and plastics sectors.

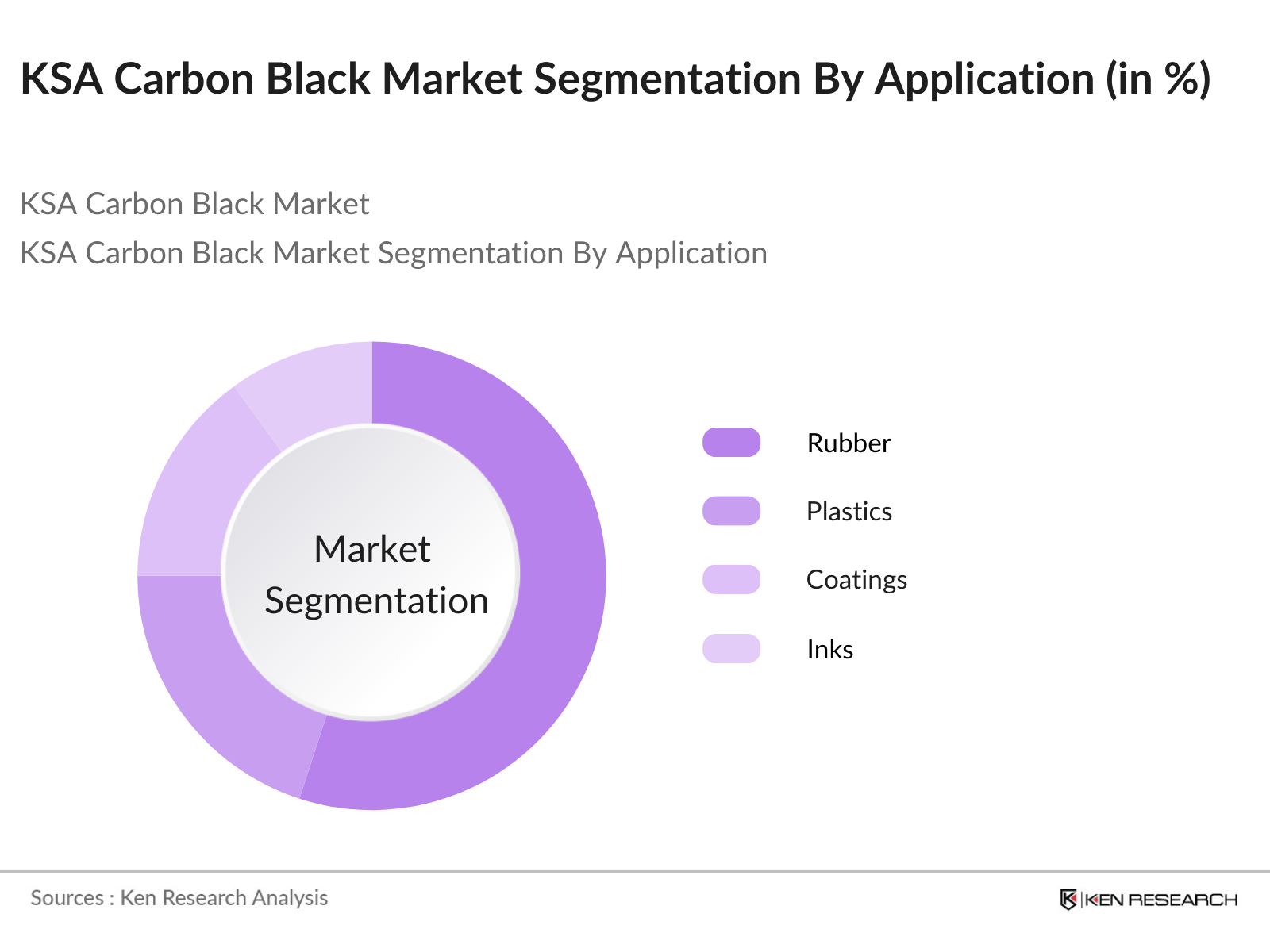

By Application: The KSA Carbon Black market is segmented by application into rubber, plastics, coatings, inks, and batteries. Rubber, particularly in the tire manufacturing sector, has a dominant share in the market. The increasing demand for both passenger and commercial vehicles in the region has significantly boosted the consumption of carbon black in tire production.

The KSA Carbon Black market is dominated by a few key players, with both local manufacturers and global companies holding significant market positions. Local players such as Saudi Carbon Black Company, supported by government initiatives, have a strong presence in the market. At the same time, global giants like Cabot Corporation and Birla Carbon continue to expand their operations in the region due to the increasing demand for high-quality carbon black products.

Over the next five years, the KSA Carbon Black market is expected to experience steady growth, driven by increasing demand across sectors such as automotive, construction, and electronics. The government's focus on industrialization and local manufacturing, combined with the rising demand for specialty carbon black in emerging sectors like batteries and electronics, will further propel the market.

|

By Product Type |

Furnace Black Thermal Black Channel Black Acetylene Black |

|

By Application |

Rubber Plastics Coatings Inks Batteries |

|

By Manufacturing Process |

Furnace Process Thermal Process Channel Process |

|

By End-Use Industry |

Automotive Construction Electronics Industrial Goods Textile |

|

By Region |

Riyadh Jeddah Dammam Makkah Madinah |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Automotive Industry Demand (Rubber, Tyres)

3.1.2. Infrastructure and Construction Growth (Coatings, Asphalt)

3.1.3. Increased Demand in Plastic and Polymer Industry (Plastics, Compounds)

3.1.4. Government Focus on Industrialization (Local Production Initiatives)

3.2. Market Challenges

3.2.1. Volatile Raw Material Prices (Crude Oil, Carbonaceous Materials)

3.2.2. Environmental Regulations (Carbon Emission Norms)

3.2.3. High Production Costs (Energy-Intensive Processes)

3.3. Opportunities

3.3.1. Technological Advancements in Manufacturing Process (Furnace Black, Thermal Black)

3.3.2. Shift Toward Specialty Carbon Black (Pigments, Conductive Carbon Black)

3.3.3. Expansion in Emerging Industries (Textiles, Batteries)

3.4. Trends

3.4.1. Use of Recovered Carbon Black (Sustainability, Circular Economy)

3.4.2. Adoption of Advanced Manufacturing Technologies (Automation, AI Integration)

3.4.3. Localization of Supply Chains (Self-Sufficiency in KSA)

3.5. Government Regulation

3.5.1. KSA Environmental Protection Initiatives (Sustainable Production)

3.5.2. Carbon Management Programs (Carbon Capture and Storage)

3.5.3. Public-Private Partnerships (Industrial Sector Support Programs)

3.6. SWOT Analysis

3.7. Stake Ecosystem (Suppliers, Distributors, End-Users)

3.8. Porters Five Forces Analysis (Competitive Landscape, Supplier Power, Buyer Power, Substitutes)

3.9. Competition Ecosystem (Local vs International Players, Market Penetration)

4.1. By Product Type (In Value %)

4.1.1. Furnace Black

4.1.2. Thermal Black

4.1.3. Channel Black

4.1.4. Acetylene Black

4.2. By Application (In Value %)

4.2.1. Rubber

4.2.2. Plastics

4.2.3. Coatings

4.2.4. Inks

4.2.5. Batteries

4.3. By Manufacturing Process (In Value %)

4.3.1. Furnace Process

4.3.2. Thermal Process

4.3.3. Channel Process

4.4. By End-Use Industry (In Value %)

4.4.1. Automotive (Tyres, Rubber Components)

4.4.2. Construction (Asphalt, Concrete Additives)

4.4.3. Electronics (Conductive Additives, Batteries)

4.4.4. Industrial Goods (Coatings, Plastics)

4.4.5. Textiles

4.5. By Region (In Value %)

4.5.1. Riyadh

4.5.2. Jeddah

4.5.3. Dammam

4.5.4. Makkah

4.5.5. Madinah

5.1. Detailed Profiles of Major Companies

5.1.1. Saudi Carbon Black Company

5.1.2. SABIC

5.1.3. Continental Carbon

5.1.4. Cabot Corporation

5.1.5. Birla Carbon

5.1.6. Orion Engineered Carbons

5.1.7. Mitsubishi Chemical

5.1.8. Phillips Carbon Black

5.1.9. Tokai Carbon

5.1.10. Black Bear Carbon

5.1.11. Himadri Speciality Chemicals

5.1.12. Longxing Chemical

5.1.13. China Synthetic Rubber Corporation (CSRC)

5.1.14. Jiangxi Black Cat Carbon Black Inc.

5.1.15. Shandong Huadong Rubber Materials

5.2. Cross Comparison Parameters (Product Portfolio, Production Capacity, Market Share, R&D Investments, Regional Presence, Sustainability Initiatives, Strategic Partnerships, Financial Performance)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Joint Ventures and Collaborations

5.8. Government Grants

5.9. Private Equity Investments

6.1. Environmental Regulations (Emissions Control, Waste Management)

6.2. Industry Compliance Standards (ISO Standards, Safety Norms)

6.3. Certification Processes (Quality, Environmental)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Manufacturing Process (In Value %)

8.4. By End-Use Industry (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

We then conducted a detailed analysis of historical data, focusing on production capacity, consumption patterns, and the supply-demand balance in the KSA Carbon Black market. Data from industry reports and local market insights were used to build reliable market forecasts.

Our market hypotheses were further refined through expert consultations. Industry professionals were interviewed through Computer-Assisted Telephone Interviews (CATIs) to validate the assumptions made regarding market dynamics, price trends, and competitive positioning.

The final phase of the research involved integrating insights gathered from primary and secondary sources. The synthesis of data included a detailed analysis of product segments, competitive landscape, and market forecasts, ensuring a holistic view of the market dynamics.

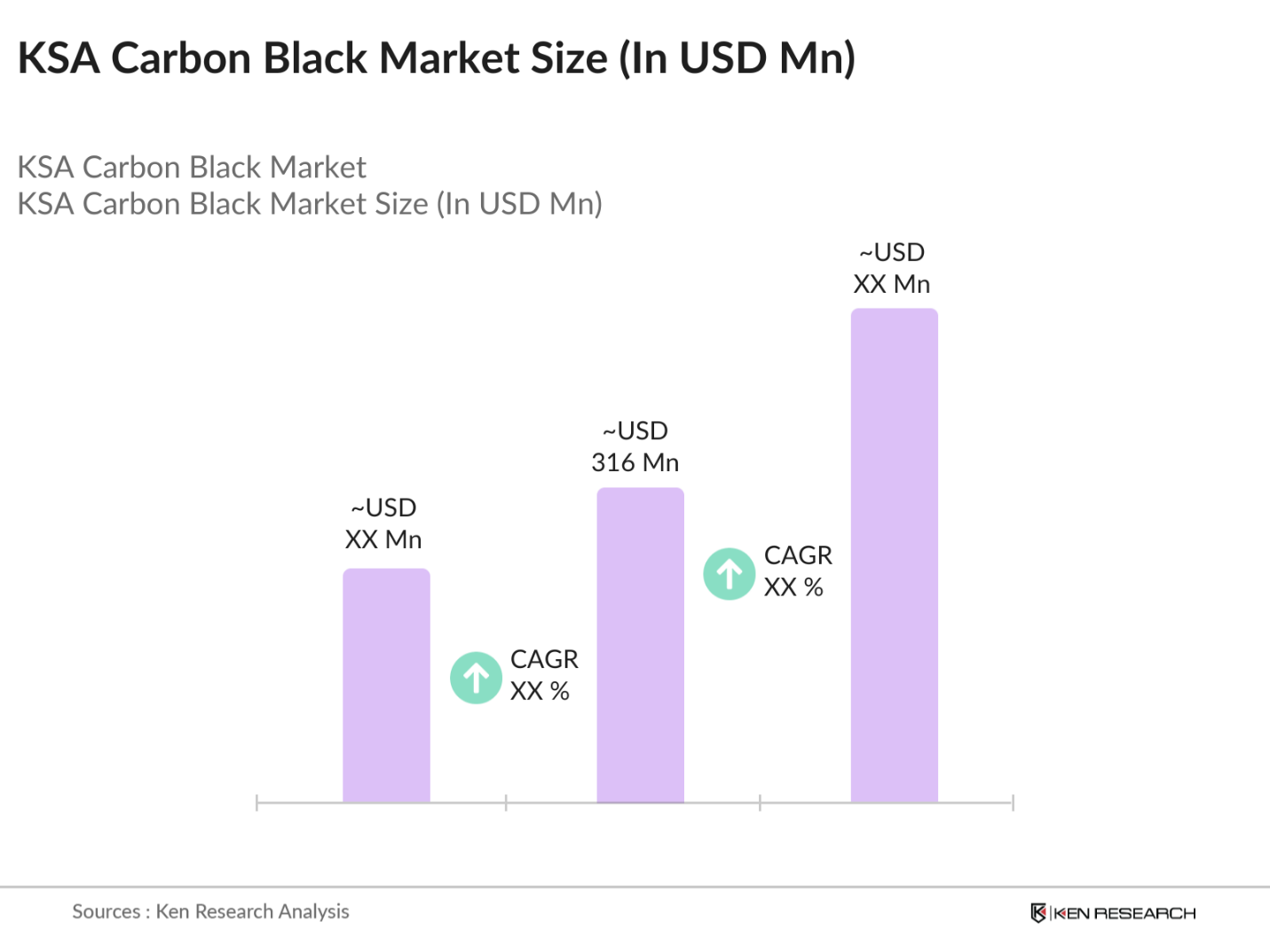

The KSA Carbon Black Market is valued at USD 316 million, driven primarily by the automotive and construction sectors. The demand for carbon black in tire production and plastic manufacturing is bolstering market growth.

Challenges include fluctuating raw material prices and environmental regulations regarding carbon emissions. Additionally, the high energy consumption involved in carbon black production increases operational costs, affecting profitability.

Key players in the market include Saudi Carbon Black Company, Cabot Corporation, Birla Carbon, and Continental Carbon. These companies dominate due to their advanced production technologies, local manufacturing capabilities, and global supply chains.

The market is primarily driven by demand from the automotive and construction sectors. The rising need for tires and rubber products in KSAs growing automobile industry and government-backed infrastructure projects is fueling the market.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.