KSA Commercial Vehicle Market Outlook to 2030

Region:Saudi Arabia

Author(s):Shubham Kashyap

Product Code:KROD3418

Region:Saudi Arabia

Author(s):Shubham Kashyap

Product Code:KROD3418

November 2024

92

The KSA Commercial Vehicle market is moderately competitive, with both global and regional players operating in the market. Major international manufacturers like Toyota, Isuzu, and Volvo dominate the heavy commercial vehicle segment, offering a range of high-performance trucks and buses. These companies focus on product innovation, technology integration, and strategic partnerships to maintain their competitive edge.

Local players such as Haji Husein Alireza & Co. and Zahid Tractor are also key participants, leveraging their strong distribution networks and service capabilities. These companies provide tailored commercial vehicle solutions to meet the needs of Saudi Arabian industries, with a particular focus on after-sales service and maintenance, which is a critical aspect for customers in the commercial vehicle space.

|

Company Name |

Establishment Year |

Headquarters |

Production Capacity (Units/Year) |

Revenue (2023) |

Key Products |

Market Presence |

Sustainability Initiatives |

R&D Investment |

Distribution Network |

|

Toyota Motor Corporation |

1937 |

Japan |

|||||||

|

Volvo Group |

1927 |

Sweden |

|||||||

|

Isuzu Motors |

1916 |

Japan |

|||||||

|

Zahid Tractor & Heavy Machinery |

1950 |

Saudi Arabia |

|||||||

|

Hino Motors |

1942 |

Japan |

The KSA Commercial Vehicle market is expected to maintain steady growth, driven by continuous investment in infrastructure, logistics, and public transport projects. The government's Vision 2030 initiative, which aims to diversify the economy and develop non-oil sectors, will create opportunities for commercial vehicle manufacturers and suppliers. Additionally, the growing demand for eco-friendly and technologically advanced vehicles will shape the future of the market.

|

By Vehicle Type |

Heavy Commercial Vehicles Medium Commercial Vehicles Light Commercial Vehicles |

|

By End-User Industry |

Construction Logistics Public Transportation Mining Others (Utilities, Emergency Services) |

|

By Fuel Type |

Diesel Electric Hybrid Natural Gas |

|

By Transmission Type |

Automatic Manual |

|

By Region |

Riyadh Jeddah Dammam Makkah Medina |

1.1 Definition and Scope

1.2 Market Taxonomy (Vehicle Type, End-User Industry, Fuel Type, Region, Transmission Type)

1.3 Market Growth Rate

1.4 Market Segmentation Overview (Heavy Commercial Vehicles, Light Commercial Vehicles, Medium Commercial Vehicles)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Government Infrastructure Investment (Vision 2030 Projects)

3.1.2 Expansion of Logistics & Transportation Sector

3.1.3 Rising Demand for Heavy-Duty Trucks (Construction, Mining Sectors)

3.1.4 Increasing Urbanization & Public Transport Initiatives

3.2 Market Challenges

3.2.1 High Import Dependency on Commercial Vehicles

3.2.2 Fluctuating Oil Prices Impacting Fleet Demand

3.2.3 Regulatory Compliance with Emission Norms

3.2.4 High Maintenance Costs for Commercial Vehicle Fleets

3.3 Opportunities

3.3.1 Adoption of Electric Commercial Vehicles

3.3.2 Localization of Commercial Vehicle Manufacturing

3.3.3 Technological Advancements in Fleet Telematics

3.3.4 Public-Private Partnerships in Public Transport

3.4 Trends

3.4.1 Shift Towards Sustainable Transportation

3.4.2 Integration of Autonomous Driving Technologies

3.4.3 Growth in E-Commerce Accelerating Demand for LCVs

3.4.4 Adoption of Alternative Fuels (Natural Gas, Hydrogen)

3.5 Government Regulations

3.5.1 SASO Commercial Vehicle Emission Standards

3.5.2 Ministry of Transport Vehicle Safety Guidelines

3.5.3 Vision 2030 Industrial Strategy for Local Manufacturing

3.5.4 Policies Supporting the Adoption of Electric Vehicles

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Ecosystem

4.1 By Vehicle Type (In Units/Value %)

4.1.1 Heavy Commercial Vehicles

4.1.2 Medium Commercial Vehicles

4.1.3 Light Commercial Vehicles

4.2 By End-User Industry (In Units/Value %)

4.2.1 Construction

4.2.2 Logistics

4.2.3 Public Transportation

4.2.4 Mining

4.2.5 Others (Utilities, Emergency Services)

4.3 By Fuel Type (In Units/Value %)

4.3.1 Diesel

4.3.2 Electric

4.3.3 Hybrid

4.3.4 Natural Gas

4.4 By Transmission Type (In Units/Value %)

4.4.1 Automatic

4.4.2 Manual

4.5 By Region (In Units/Value %)

4.5.1 Riyadh

4.5.2 Jeddah

4.5.3 Dammam

4.5.4 Makkah

4.5.5 Medina

5.1 Detailed Profiles of Major Competitors

5.1.1 Toyota Motor Corporation

5.1.2 Isuzu Motors Ltd.

5.1.3 Volvo Group

5.1.4 Mercedes-Benz (Daimler AG)

5.1.5 Scania AB

5.1.6 Ford Motor Company

5.1.7 Hyundai Motor Company

5.1.8 Haji Husein Alireza & Co.

5.1.9 Zahid Tractor & Heavy Machinery

5.1.10 Tata Motors Limited

5.1.11 Ashok Leyland

5.1.12 MAN Truck & Bus SE

5.1.13 Navistar International Corporation

5.1.14 FAW Group

5.1.15 Hino Motors Ltd.

5.2 Cross Comparison Parameters (Production Capacity, Headquarters, Inception Year, Revenue, Product Range, Fleet Telematics Integration, R&D Expenditure, Sustainability Initiatives)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Vehicle Emission Standards

6.2 Compliance with Transport Ministry Guidelines

6.3 Import Tariff and Local Manufacturing Incentives

6.4 Certification Processes for Commercial Vehicle Safety

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Vehicle Type (In Units/Value %)

8.2 By End-User Industry (In Units/Value %)

8.3 By Fuel Type (In Units/Value %)

8.4 By Transmission Type (In Units/Value %)

8.5 By Region (In Units/Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

In this phase, a comprehensive ecosystem map of stakeholders in the KSA Commercial Vehicle Market is constructed. Extensive desk research is utilized to gather industry data from government reports, proprietary databases, and other sources. This step focuses on identifying key variables like market demand, production rates, and regulatory influences.

In this step, historical data on vehicle production, imports, and sales are compiled and analyzed. This includes evaluating the ratio of vehicles by type and end-user industry. An assessment of the operational efficiency of commercial vehicle fleets is also conducted to ensure the accuracy of revenue estimates.

Hypotheses based on market trends are developed and validated through interviews with industry experts, including commercial fleet managers, automotive suppliers, and regulatory authorities. These consultations offer valuable insights into current market dynamics, growth drivers, and competitive positioning.

The final phase involves synthesizing the research through direct engagement with manufacturers and fleet operators. These consultations verify the findings and provide additional data on emerging technologies, sustainability practices, and future market opportunities.

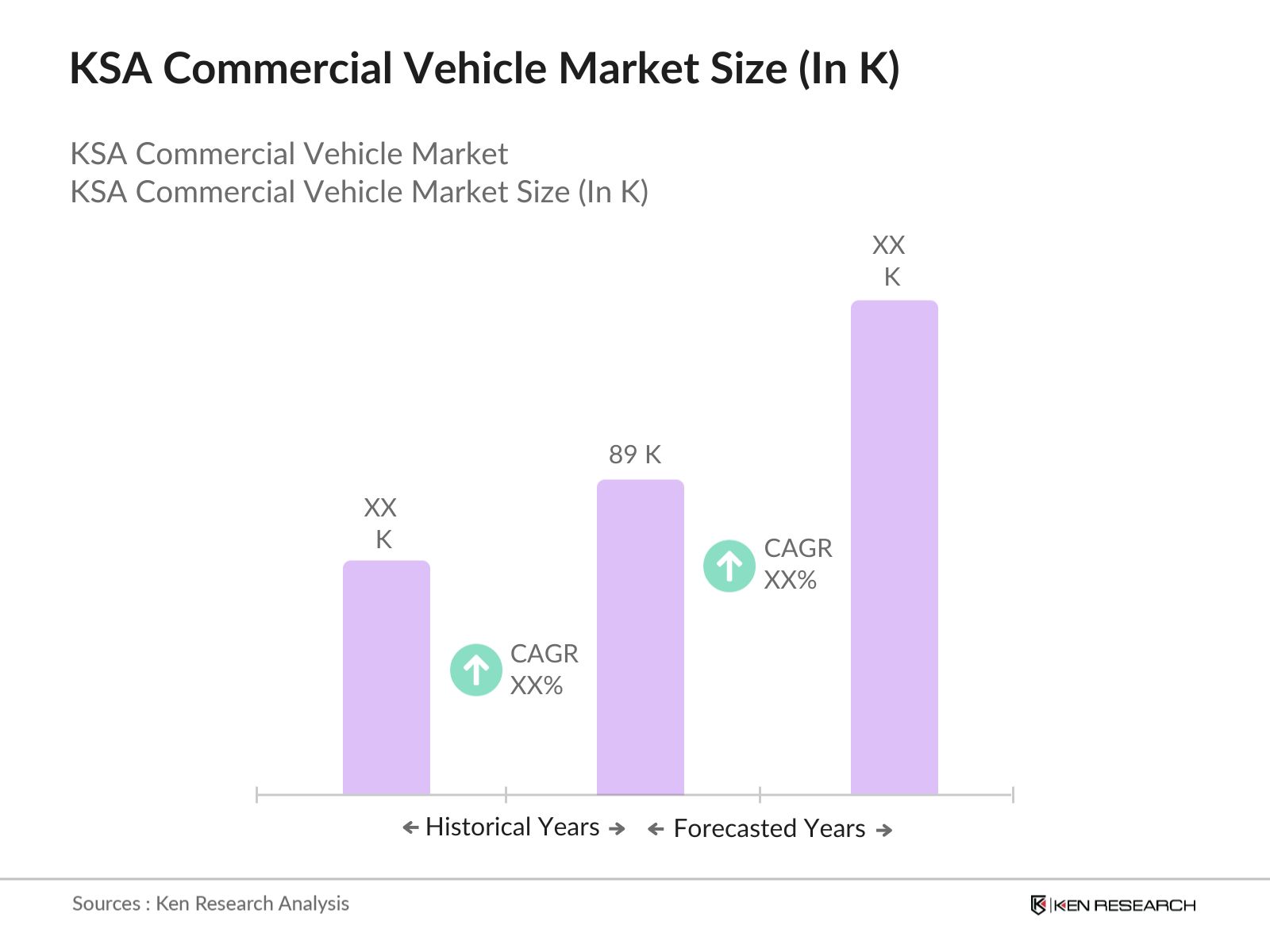

The KSA commercial vehicle market was valued at 89 k vehicles, driven by rising infrastructure projects, logistics, and public transportation investments under Vision 2030.

Challenges in the KSA commercial vehicle market include dependency on vehicle imports, fluctuating oil prices affecting fleet purchases, and the need to comply with increasingly stringent emissions regulations.

Key players in the KSA commercial vehicle market include Toyota Motor Corporation, Volvo Group, Isuzu Motors, Zahid Tractor & Heavy Machinery, and Hino Motors. These companies dominate due to their wide product offerings and extensive distribution networks.

The KSA commercial vehicle market is propelled by government infrastructure projects, the expansion of the logistics sector, and increasing demand for heavy-duty vehicles in construction and mining industries.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.