KSA Orthopedic Devices Market Outlook to 2030

Region:Saudi Arabia

Author(s):Yogita Sahu

Product Code:KROD6787

Region:Saudi Arabia

Author(s):Yogita Sahu

Product Code:KROD6787

November 2024

96

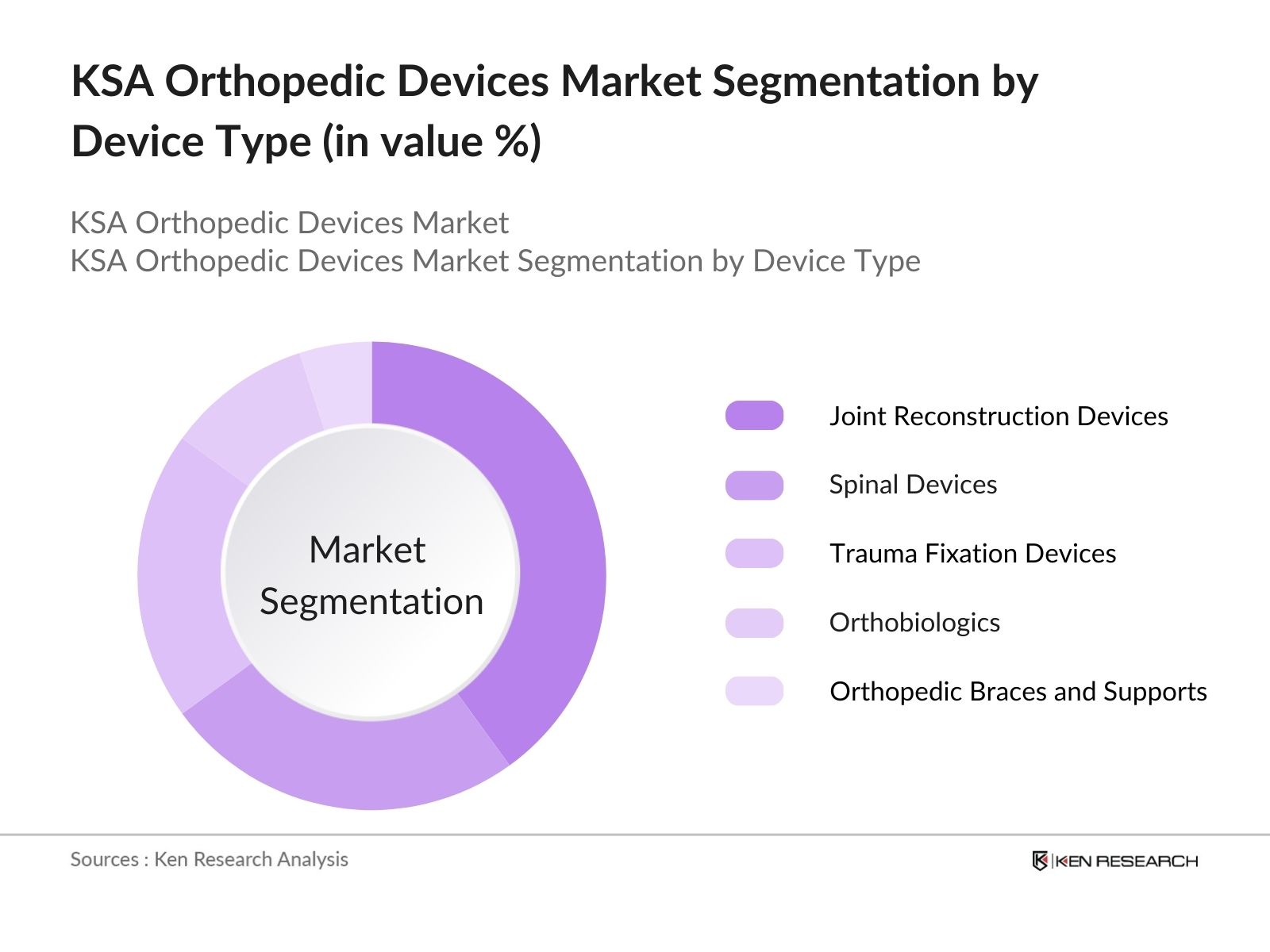

By Device Type: The market is segmented by device type into joint reconstruction devices, spinal devices, trauma fixation devices, orthobiologics, and orthopedic braces and supports. Recently, joint reconstruction devices have emerged as the dominant sub-segment, particularly due to the rising cases of knee and hip replacements in the elderly population. With advancements in prosthetic technologies, the demand for these devices continues to grow, especially as more patients seek minimally invasive surgeries for joint reconstruction.

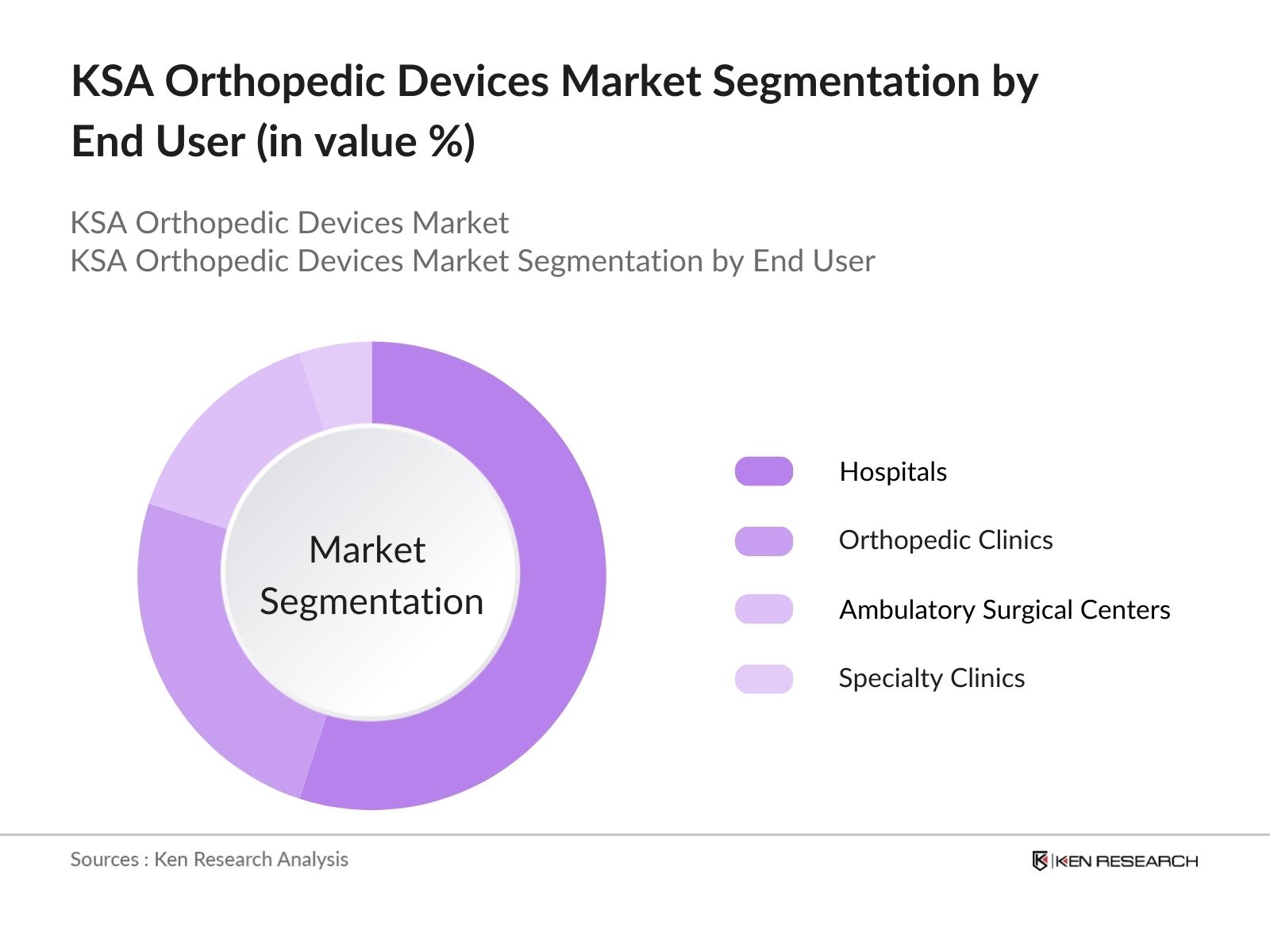

By End User: The market is also segmented by end user into hospitals, orthopedic clinics, ambulatory surgical centers, and specialty clinics. Hospitals are currently leading this segment due to their large patient inflow and superior medical facilities. As government funding increases and more hospitals are equipped with state-of-the-art technology, they continue to serve as the primary setting for complex orthopedic procedures such as joint replacements and spinal surgeries.

The market is dominated by a mix of global and local players. The presence of established international companies and local manufacturers has led to intense competition. Notably, foreign companies dominate the high-end device segment, while local firms are gaining traction in cost-sensitive segments such as orthopedic braces and supports.

|

Company Name |

Established |

Headquarters |

No. of Employees |

R&D Expenditure |

Product Range |

Revenue (SAR Bn) |

Partnerships |

Mergers/Acquisitions |

|

Zimmer Biomet |

1927 |

USA |

||||||

|

Stryker Corporation |

1941 |

USA |

||||||

|

Medtronic |

1949 |

Ireland |

||||||

|

DePuy Synthes |

1895 |

USA |

||||||

|

Arthrex, Inc. |

1981 |

USA |

Over the next five years, the KSA orthopedic devices industry is expected to exhibit growth due to increasing healthcare spending, the rise in chronic conditions like arthritis, and the high demand for advanced medical procedures. Government efforts under Vision 2030 to enhance healthcare services and encourage medical tourism will continue to drive investments in orthopedic care.

|

By Device Type |

Joint Reconstruction Devices Spinal Devices Trauma Fixation Devices Ortho biologics Orthopedic Braces and Supports |

|

By End User |

Hospitals Orthopedic Clinics Ambulatory Surgical Centers Specialty Clinics |

|

By Application |

Knee Replacement Hip Replacement Spine Surgery Sports Medicine Trauma |

|

By Technology |

Conventional Orthopedic Devices Robotic-Assisted Devices Computer-Assisted Surgery Devices 3D Printed Orthopedic Devices |

|

By Region |

North West East South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (Orthopedic Procedures, Aging Population, Healthcare Infrastructure, Medical Tourism)

3.2. Market Challenges (High Cost of Advanced Devices, Reimbursement Policies, Regulatory Barriers, Low Healthcare Penetration in Rural Areas)

3.3. Opportunities (3D Printing, Robotic-Assisted Surgeries, Public-Private Partnerships, Healthcare Reforms)

3.4. Trends (Increased Adoption of Minimally Invasive Surgery, Usage of Smart Orthopedic Implants, Outpatient Surgeries Growth, Telehealth Integration)

3.5. Government Regulations (SFDA Medical Device Regulation, Public Healthcare Spending Initiatives, Local Manufacturing Incentives, Import Tariffs)

3.6. SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7. Stakeholder Ecosystem (Hospitals, Clinics, Distributors, Manufacturers, Insurance Providers)

3.8. Porters Five Forces (Bargaining Power of Suppliers, Bargaining Power of Buyers, Threat of New Entrants, Threat of Substitutes, Industry Rivalry)

3.9. Competition Ecosystem

4.1. By Device Type

4.1.1. Joint Reconstruction Devices

4.1.2. Spinal Devices

4.1.3. Trauma Fixation Devices

4.1.4. Orthobiologics

4.1.5. Orthopedic Braces and Supports

4.2. By End User

4.2.1. Hospitals

4.2.2. Orthopedic Clinics

4.2.3. Ambulatory Surgical Centers

4.2.4. Specialty Clinics

4.3. By Application

4.3.1. Knee Replacement

4.3.2. Hip Replacement

4.3.3. Spine Surgery

4.3.4. Sports Medicine

4.3.5. Trauma

4.4. By Technology

4.4.1. Conventional Orthopedic Devices

4.4.2. Robotic-Assisted Devices

4.4.3. Computer-Assisted Surgery Devices

4.4.4. 3D Printed Orthopedic Devices

4.5. By Region

4.5.1. Central Province

4.5.2. Western Province

4.5.3. Eastern Province

4.5.4. Northern Province

5.1. Detailed Profiles of Major Companies

5.1.1. Zimmer Biomet

5.1.2. DePuy Synthes

5.1.3. Stryker Corporation

5.1.4. Smith & Nephew

5.1.5. Medtronic

5.1.6. NuVasive, Inc.

5.1.7. DJO Global

5.1.8. B. Braun Melsungen AG

5.1.9. Aesculap Implant Systems

5.1.10. Arthrex, Inc.

5.1.11. Globus Medical

5.1.12. Wright Medical Group N.V.

5.1.13. ConMed Corporation

5.1.14. Orthofix International

5.1.15. Exactech, Inc.

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Revenue, Market Share, Key Partnerships, Research and Development Expenditure, Product Launches, Innovation Strategy)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Mergers & Acquisitions, Partnerships, Collaborations, Licensing)

5.5. Investment Analysis

5.6. Venture Capital Funding

5.7. Government Grants

5.8. Private Equity Investments

6.1. Compliance with SFDA Standards

6.2. Import Regulations and Local Manufacturing Policies

6.3. Certification Processes

6.4. Medical Device Registration Requirements

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Device Type

8.2. By End User

8.3. By Application

8.4. By Technology

8.5. By Region

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The first step involves mapping the entire orthopedic devices ecosystem in Saudi Arabia. This includes identifying key stakeholders such as manufacturers, suppliers, hospitals, clinics, and regulatory bodies. Extensive desk research using proprietary databases and government reports was undertaken to establish critical market variables, including device types and usage trends.

Historical data from the last five years was analyzed, focusing on market penetration, hospital usage rates, and revenue generation. An evaluation of healthcare infrastructure and the increasing adoption of robotic-assisted surgeries was conducted to ensure the accuracy of future market projections.

Hypotheses related to the growth of the orthopedic devices market were validated through structured interviews with experts from leading orthopedic device companies and healthcare professionals in Saudi Arabia. These consultations provided essential insights into market trends and operational challenges.

The final phase involved a synthesis of research findings, complemented by interactions with healthcare providers and orthopedic specialists. This helped to validate key data points and refine the final market estimates, ensuring an accurate and comprehensive market analysis.

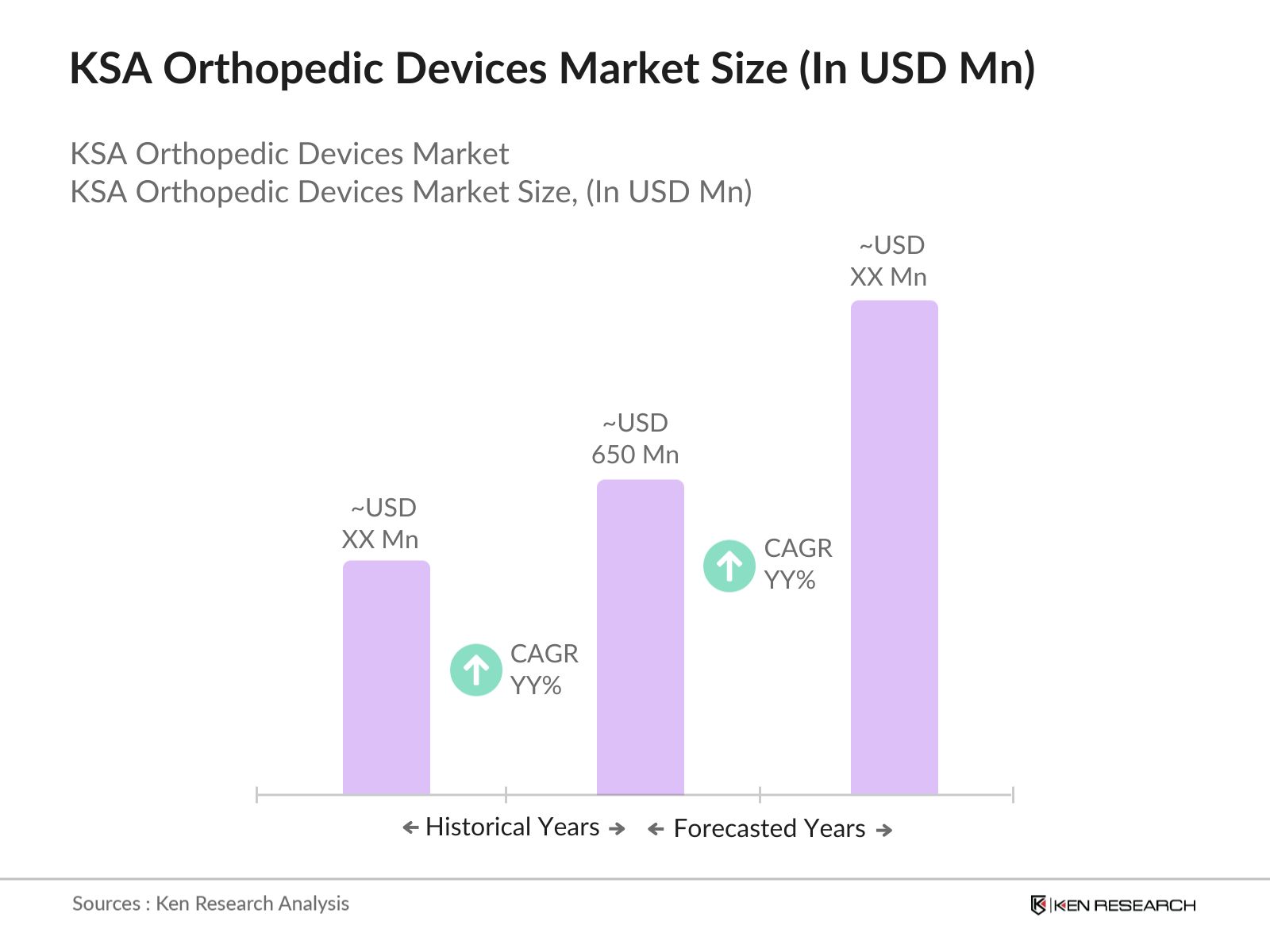

The KSA orthopedic devices market is valued at USD 650 million, driven by the increasing demand for joint reconstruction devices and a growing aging population in the country.

Challenges in the KSA orthopedic devices market include the high cost of advanced devices, complex regulatory procedures, and the limited availability of skilled professionals for robotic-assisted surgeries.

Major players in the KSA orthopedic devices market include Zimmer Biomet, Stryker Corporation, Medtronic, DePuy Synthes, and Arthrex, Inc., dominating due to their advanced product offerings and extensive distribution networks.

Key growth drivers in the KSA orthopedic devices market include government investments in healthcare infrastructure, the rising incidence of joint-related disorders, and the growing demand for minimally invasive surgeries.

The future of the KSA orthopedic devices market will be shaped by technological advancements like 3D printing and robotic surgeries, which offer more precise and customized treatments.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.