KSA Red Meat Market Outlook to 2030

Region:Middle East

Author(s):Shubham Kashyap

Product Code:KROD3080

November 2024

88

About the Report

KSA Red Meat Market Overview

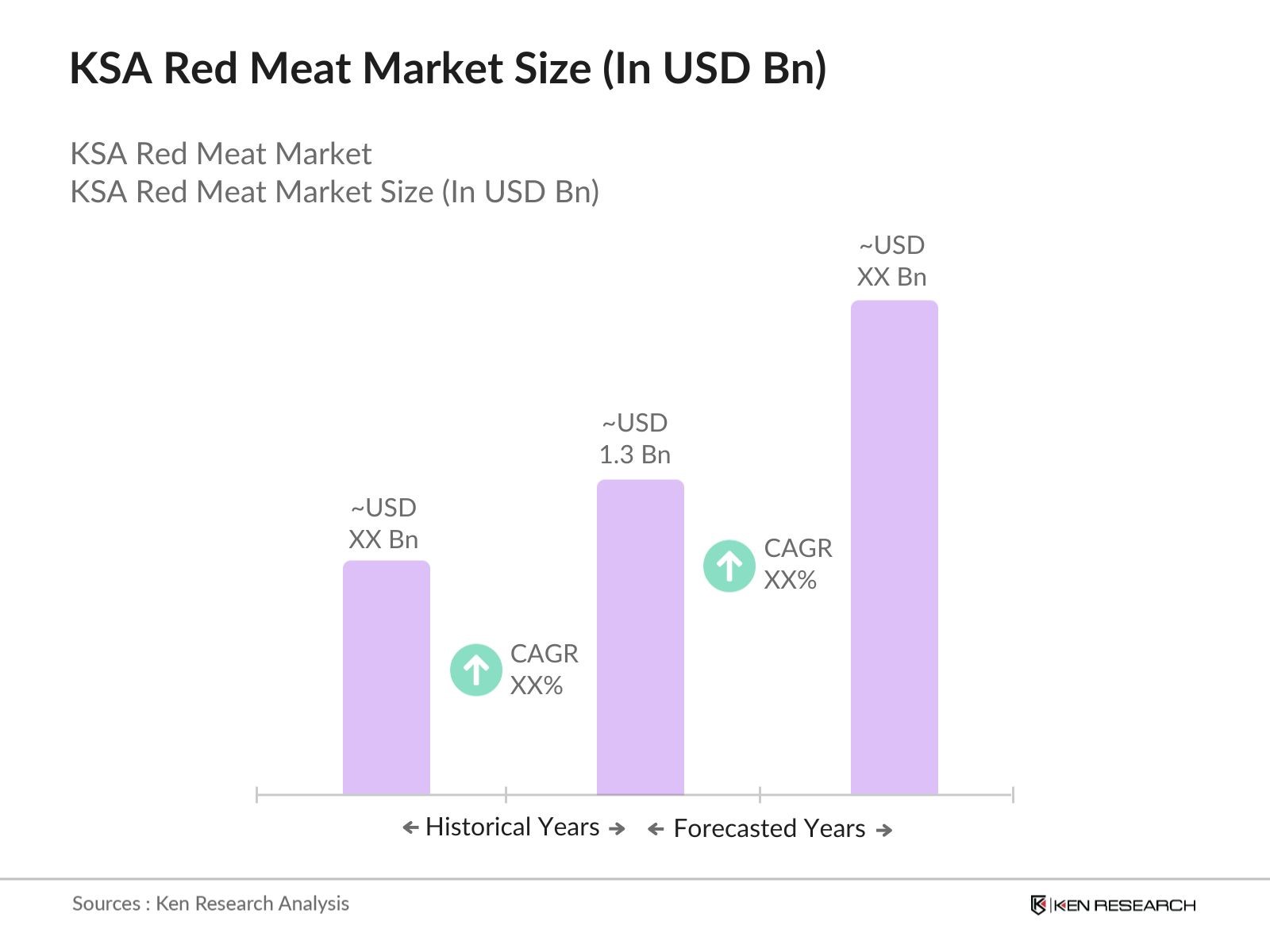

- The KSA red meat market is valued at USD 1.3 billion, based on a five-year historical analysis, supported by increasing demand for protein-rich diets, population growth, and government-led initiatives to enhance domestic meat production. The market is witnessing growth driven by changing consumer preferences for higher-quality meat, coupled with rising disposable incomes. The demand for red meat, including beef, lamb, and mutton, is surging as the Kingdom seeks to reduce its reliance on imported meat products.

- Major urban areas such as Riyadh, Jeddah, and Dammam are leading the growth of this market due to higher population density, increased disposable incomes, and a growing preference for premium meat cuts. In contrast, rural areas are showing steady growth in demand for affordable meat products as the government promotes self-sufficiency and supports local meat producers.

- The Saudi Arabian government, under Vision 2030, has implemented initiatives to increase domestic meat production and reduce import dependency. In 2024, the Ministry of Environment, Water, and Agriculture launched programs to support local farmers, providing subsidies and improved breeding techniques to enhance livestock quality. These programs are expected to boost local red meat production by over 20% by 2028.

KSA Red Meat Market Segmentation

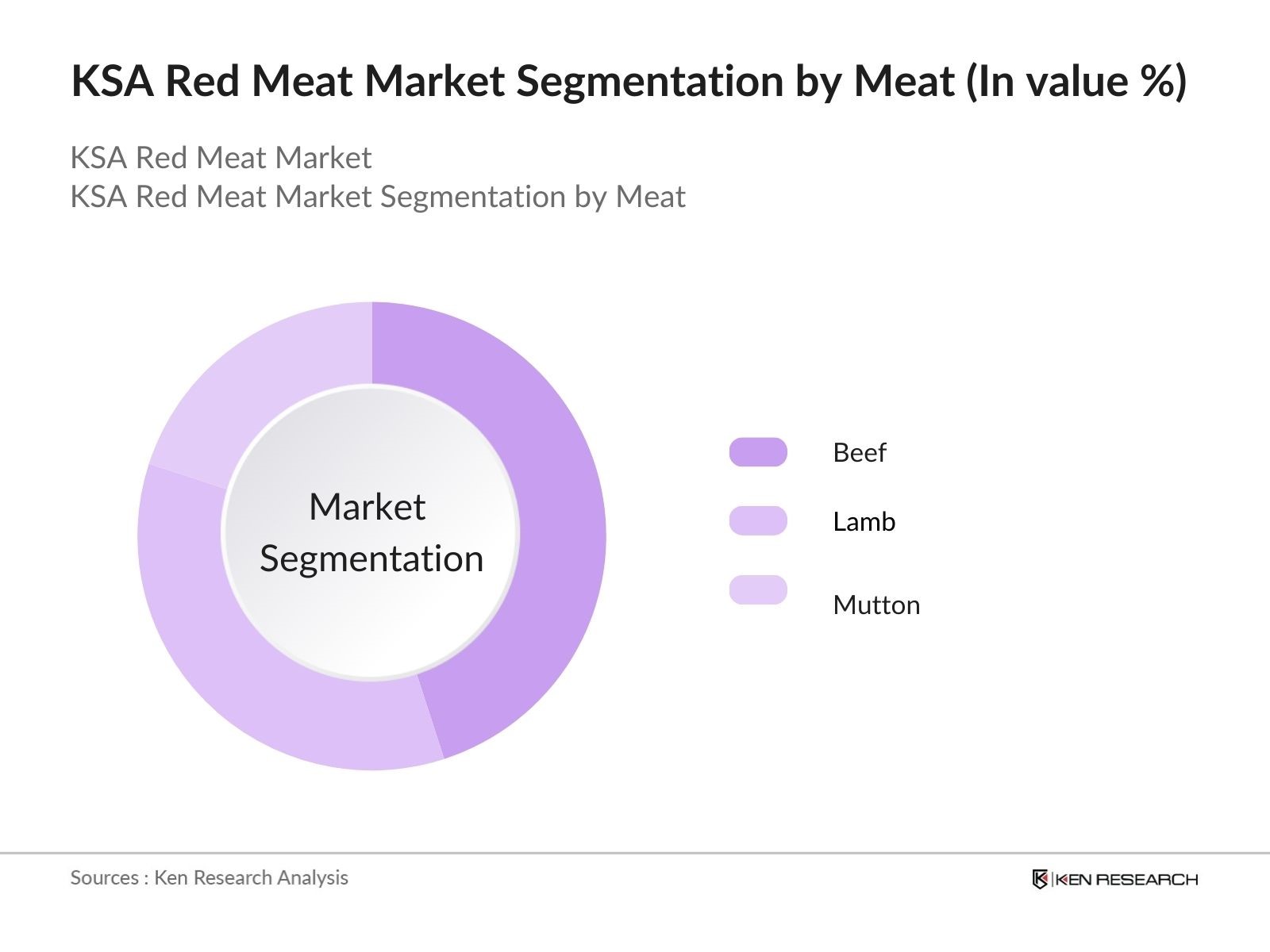

- By Meat Type: The market is segmented by type of meat into beef, lamb, and mutton. Beef dominates the market due to its popularity among consumers and increasing demand in urban areas. Lamb and mutton are also significant contributors, particularly in traditional meals and during religious festivities like Eid. The demand for premium beef cuts is on the rise, especially among the upper-middle-class population, while lamb and mutton consumption remains strong in rural regions.

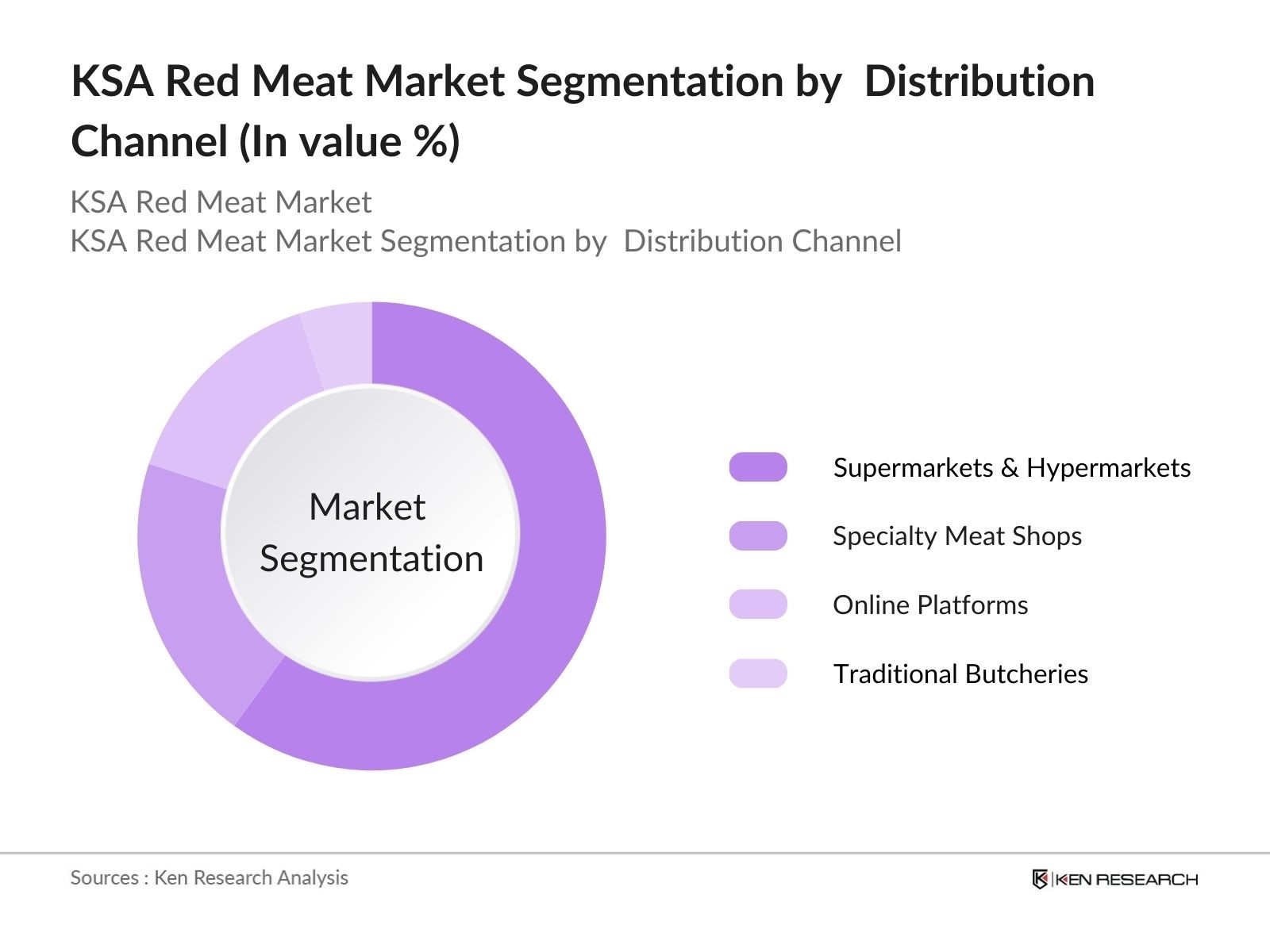

- By Distribution Channel: The market is segmented by distribution channel into supermarkets & hypermarkets, specialty meat shops, online platforms, and traditional butcheries. Supermarkets & hypermarkets are the largest distribution channel, with chains like Carrefour and Lulu Hypermarket offering a wide variety of imported and domestic red meat products. Online platforms are gaining traction, especially in urban areas, as consumers shift towards e-commerce for convenience and a wider selection of meat products.

KSA Red Meat Market Competitive Landscape

The KSA red meat market is highly competitive, with several domestic and international players providing a wide range of meat products. Key players include Almarai, National Agricultural Development Company (NADEC), and Almunajem Foods. These companies are continuously expanding their product portfolios to meet the growing demand for both fresh and processed meat products in the Kingdom. Investments in modern slaughterhouses, sustainable farming practices, and partnerships with international suppliers are common strategies employed by these players to strengthen their market presence.

|

Company Name |

Establishment Year |

Headquarters |

Meat Processing Capacity (Tons) |

Revenue (USD Mn) |

No. of Employees |

Livestock Population |

Sustainability Initiatives |

Cold Chain Logistics |

Market Share (2023, %) |

|

Almarai |

1977 |

Riyadh |

|||||||

|

National Agricultural Development Company |

1981 |

Riyadh |

|||||||

|

Almunajem Foods |

1950 |

Riyadh |

|||||||

|

Tanmiah Food Company |

1962 |

Jeddah |

|||||||

|

Aseer Agricultural Company |

1981 |

Abha |

KSA Red Meat Industry Analysis

Growth Drivers

- Rise in Disposable Income and Changing Consumption Patterns: The Kingdom of Saudi Arabia (KSA) has witnessed a steady rise in disposable income, reaching SAR 85,000 per household annually in 2023, according to the Saudi General Authority for Statistics. This increase, alongside changing dietary preferences, has led to a higher per capita meat consumption rate of 52 kilograms per year in 2024, showing a growing demand for red meat. Saudi Arabias shift towards a more urban lifestyle is driving these consumption changes, with urban areas like Riyadh and Jeddah experiencing particularly high demand for premium meat products.

- Government Support for Local Meat Production: The Saudi government has made substantial efforts to boost local meat production as part of its Vision 2030 plan. This includes SAR 6.3 billion in subsidies for livestock breeding programs aimed at increasing self-sufficiency in red meat production. Initiatives under the Agricultural Development Fund (ADF) have supported the establishment of 50+ breeding facilities across the country. Additionally, Vision 2030's emphasis on food security is pushing the development of modern farms and breeding technologies to reduce dependence on meat imports.

- Population Growth and Increased Demand for Protein-Rich Diets: Saudi Arabias population is expected to grow to 37.2 million by the end of 2024, according to the World Bank, with urbanization rates exceeding 84%. This growth, combined with a demand for protein-rich diets, is a major driver of the red meat market in KSA. The nation's urban population, which forms 80% of the total, has shifted towards a protein-heavy diet, further bolstering red meat consumption. These demographic changes contribute to a steadily growing demand for meat, particularly among younger populations.

Market Challenges

- High Dependence on Meat Imports: Despite government efforts to boost local production, Saudi Arabia remains highly dependent on imported red meat, with nearly 70% of beef and lamb imported from countries like Australia, Brazil, and India. Fluctuations in global meat prices and supply chain disruptions pose significant challenges to market stability. The government is working to reduce this dependency through investments in local production, but significant gaps remain.

- Environmental Concerns and Sustainability Issues: The livestock industry in Saudi Arabia faces criticism for its environmental impact, particularly in terms of water consumption and greenhouse gas emissions. Addressing these concerns is crucial, as the government pushes for more sustainable farming practices. The implementation of stricter environmental regulations is expected to increase operational costs for local producers. The Ministry of Environment, Water, and Agriculture is implementing stricter regulations to mitigate these environmental impacts, particularly concerning water use and emissions control.

KSA Red Meat Market Future Outlook

The KSA red meat market is expected to experience robust growth over the next five years, driven by increasing consumer demand for premium meat products, government initiatives to boost local production, and the growing middle-class population. The adoption of sustainable farming practices and technological advancements in meat processing are expected to further enhance market growth.

Future Market Opportunities

- Growth in Online Meat Sales: The rise of e-commerce in Saudi Arabia is presenting new opportunities for meat producers and distributors. In 2024, online platforms accounted for a major portion of total meat sales, and this figure is expected to grow as consumers increasingly turn to digital channels for grocery shopping. Online meat delivery services are particularly popular among younger consumers in urban areas, providing a convenient way to purchase fresh and frozen meat products.

- Expansion of Organic and Halal Meat Products: There is growing consumer interest in organic and Halal-certified meat products, particularly among health-conscious individuals and religiously observant consumers. In 2024, sales of organic red meat grew substantially with increasing demand for products that meet strict Halal and organic farming standards. This presents a significant opportunity for producers to cater to a niche but expanding market segment.

Scope of the Report

|

By Meat |

Beef Lamb Mutton |

|

By Distribution Channel |

Supermarkets & Hypermarkets Specialty Meat Shops Online Platforms Traditional Butcheries |

|

By End User |

Construction Companies Architects & Designers Government Infrastructure Projects Retail & Wholesale Distributors |

|

By Color |

Households Restaurants Catering Services |

|

By Meat Processing |

Fresh Frozen Processed |

|

By Region |

Riyadh Jeddah Eastern Province Rest of Saudi Arabia |

Products

Key Target Audience

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (Ministry of Environment, Water, and Agriculture, Saudi Food & Drug Authority)

Local Meat Producers

Banks and Financial Institutes

Supermarket and Hypermarket Chains

Online Retailers

Meat Processing Companies

Cold Chain Logistics Providers

Premium Restaurant Chains

Companies

Major Players Mentioned in the Report

Almarai

National Agricultural Development Company (NADEC)

Almunajem Foods

Tanmiah Food Company

Aseer Agricultural Company

Al Safi Danone

Savola Group

Al Watania Agriculture

Mazraah Meat

Al Kabeer Group

Global Food Industries

Fonterra Co-operative Group

Sadia (BRF)

Tyson Foods

JBS S.A.

Table of Contents

1. KSA Red Meat Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. KSA Red Meat Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. KSA Red Meat Market Analysis

3.1 Growth Drivers

3.1.1 Rise in Disposable Income and Changing Consumption Patterns (Per Capita Consumption, Average Disposable Income)

3.1.2 Government Support for Local Meat Production (Government Subsidies, Vision 2030 Initiatives, Breeding Programs)

3.1.3 Population Growth and Increased Demand for Protein-Rich Diets (Population Growth Rate, Urbanization Metrics)

3.1.4 Rising Preference for Premium Meat Products (Segmented Pricing for Premium Meats)

3.2 Market Challenges

3.2.1 High Dependence on Meat Imports (Import Dependency Ratio)

3.2.2 Fluctuations in Global Meat Prices (Global Meat Price Volatility)

3.2.3 Environmental Sustainability Concerns (Water Usage, Greenhouse Gas Emissions)

3.3 Opportunities

3.3.1 Growth in E-commerce Meat Sales (E-commerce Penetration Rate in Meat Sales)

3.3.2 Increasing Demand for Halal-Certified and Organic Meat (Halal Certification, Organic Certification Metrics)

3.3.3 Expansion of Cold Chain Logistics (Cold Chain Infrastructure Investment)

3.4 Trends

3.4.1 Increasing Popularity of Processed Meat Products (Processed Meat Consumption Growth)

3.4.2 Growth of Local Meat Production Facilities (Increase in Local Slaughterhouses)

3.4.3 Adoption of Advanced Livestock Management Practices (Adoption Rate of IoT & Livestock Management Technologies)

3.5 Government Regulation

3.5.1 Vision 2030 and Agriculture Policies (Vision 2030 Goals for Livestock)

3.5.2 Import Tariffs and Trade Regulations (Meat Import Tariffs, Trade Agreements)

3.5.3 Environmental Compliance for Livestock Farming (Water Use Regulations, Emission Standards)

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces

3.9 Competition Ecosystem

4. KSA Red Meat Market Segmentation

4.1 By Meat Type (In Value %)

4.1.1 Beef

4.1.2 Lamb

4.1.3 Mutton

4.2 By Distribution Channel (In Value %)

4.2.1 Supermarkets & Hypermarkets

4.2.2 Specialty Meat Shops

4.2.3 Online Platforms

4.2.4 Traditional Butcheries

4.3 By End-User (In Value %)

4.3.1 Households

4.3.2 Restaurants

4.3.3 Catering Services

4.4 By Region (In Value %)

4.4.1 Riyadh

4.4.2 Jeddah

4.4.3 Eastern Province

4.4.4 Rest of Saudi Arabia

4.5 By Meat Processing Type (In Value %)

4.5.1 Fresh

4.5.2 Frozen

4.5.3 Processed

5. KSA Red Meat Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Almarai

5.1.2 National Agricultural Development Company (NADEC)

5.1.3 Almunajem Foods

5.1.4 Al Safi Danone

5.1.5 Savola Group

5.1.6 Al Watania Agriculture

5.1.7 Tanmiah Food Company

5.1.8 Aseer Agricultural Company

5.1.9 Mazraah Meat

5.1.10 Al Kabeer Group

5.1.11 Global Food Industries

5.1.12 Fonterra Co-operative Group

5.1.13 Sadia (BRF)

5.1.14 Tyson Foods

5.1.15 JBS S.A.

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Livestock Population, Meat Processing Capacity, Sustainability Initiatives, Cold Chain Infrastructure, Market Share)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. KSA Red Meat Market Regulatory Framework

6.1 Livestock Farming Regulations (Health and Safety Standards, Animal Welfare Policies)

6.2 Compliance Requirements for Meat Imports (Halal Certification, Quality Control Regulations)

6.3 Certification Processes (Halal Certification, Organic Certification)

7. KSA Red Meat Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. KSA Red Meat Future Market Segmentation

8.1 By Meat Type (In Value %)

8.2 By Distribution Channel (In Value %)

8.3 By End-User (In Value %)

8.4 By Region (In Value %)

8.5 By Meat Processing Type (In Value %)

9. KSA Red Meat Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping the ecosystem of the KSA Red Meat Market, including key stakeholders such as meat producers, distributors, and government bodies. Extensive desk research was conducted using proprietary databases and secondary sources to identify market dynamics and the variables influencing supply, demand, and pricing.

Step 2: Market Analysis and Construction

In this phase, historical data on red meat consumption, production, and import levels were compiled to establish trends in the market. Factors such as urbanization, income growth, and government policies were analyzed to understand their impact on market size. The research also included an assessment of distribution channels to determine their influence on market growth.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses, particularly around growth drivers such as premium meat demand and local production capabilities, were validated through consultations with industry experts. These consultations were conducted using computer-assisted telephone interviews (CATIs) with leading meat producers, distributors, and logistics providers.

Step 4: Research Synthesis and Final Output

The final phase synthesized insights from producers and government reports, providing a comprehensive view of the KSA Red Meat Market. By combining bottom-up data from meat processors and top-down data from government sources, the report provides accurate and actionable insights for market stakeholders.

Frequently Asked Questions

01. How big is the KSA Red Meat Market?

The KSA red meat market was valued at USD 1.3 billion, driven by increasing demand for protein-rich diets and government-led efforts to boost domestic meat production.

02. What are the challenges in the KSA Red Meat Market?

Challenges in the KSA red meat market include high dependence on meat imports, fluctuating global meat prices, and sustainability concerns regarding livestock farming practices.

03. Who are the major players in the KSA Red Meat Market?

Major players in the KSA red meat market include Almarai, National Agricultural Development Company (NADEC), Almunajem Foods, Tanmiah Food Company, and Aseer Agricultural Company.

04. What are the growth drivers of the KSA Red Meat Market?

The KSA red meat market growth is propelled by increasing disposable incomes, government initiatives to boost local meat production, and rising consumer demand for premium meat products in urban areas.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.