MEA Aramid Fiber Market Outlook to 2030

Region:Africa

Author(s):Shambhavi

Product Code:KROD3041

Region:Africa

Author(s):Shambhavi

Product Code:KROD3041

November 2024

98

By Type: The MEA aramid fiber market is segmented by type into Para-Aramid and Meta-Aramid. Para-Aramid holds the dominant market share due to its high strength and heat resistance, making it ideal for use in bulletproof vests, helmets, and other military applications. Additionally, para-aramid is widely used in automotive brake pads and optical fibers, which further elevates its demand. Meta-aramid, on the other hand, is extensively used in industrial filtration, protective clothing, and electrical insulation, but has a smaller share compared to para-aramid.

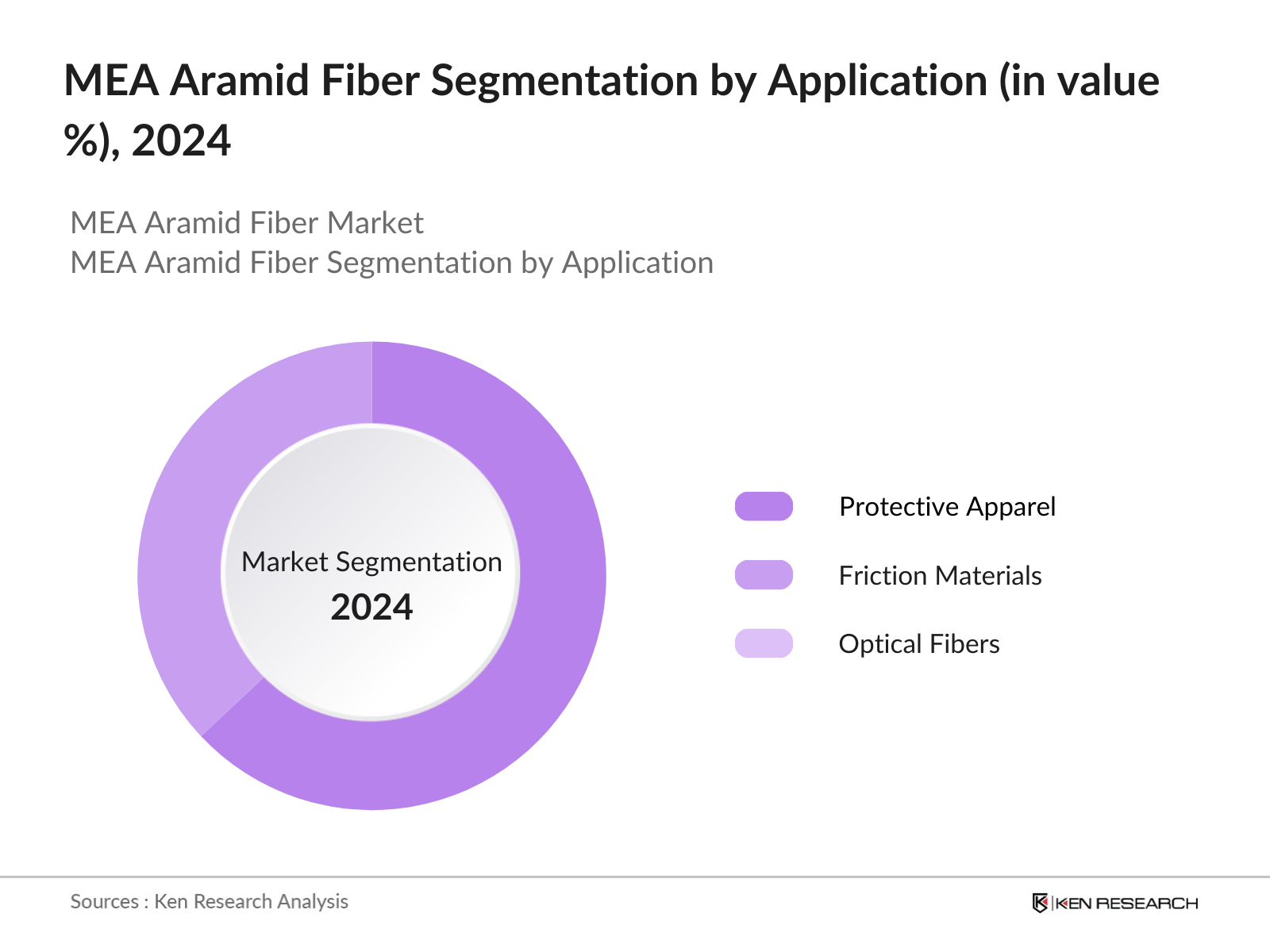

By Application: MEA aramid fiber is segmented by application into Protective Apparel, Friction Materials, and Optical Fibers. Protective apparel dominates the market as aramid fibers are commonly used in fire-resistant clothing for firefighters, military personnel, and industrial workers. Their excellent resistance to heat and chemicals makes them essential in high-risk environments. Friction materials like brake pads and clutches are also significant consumers of aramid fibers, driven by the need for durability in high-performance vehicles and heavy machinery.

The MEA aramid fiber market is characterized by a few key players, with Teijin Limited and DuPont de Nemours leading the market due to their technological advancements and strong presence in the defense sector. These companies, along with Kolon Industries and Hyosung Corporation, benefit from established supply chains and extensive R&D capabilities. The market consolidation around these key players reflects their dominance in driving innovation and addressing the region's demand for high-performance aramid fibers.

|

Company |

Establishment Year |

Headquarters |

Market Penetration |

R&D Spending |

Product Portfolio |

Strategic Partnerships |

Regional Presence |

|

Teijin Limited |

1918 |

Japan |

|||||

|

DuPont de Nemours, Inc. |

1802 |

USA |

|||||

|

Kolon Industries, Inc. |

1957 |

South Korea |

|||||

|

Hyosung Corporation |

1966 |

South Korea |

|||||

|

Yantai Tayho Advanced Materials |

1986 |

China |

Increased Defense and Aerospace Spending: Aramid fibers, widely used in defense and aerospace due to their lightweight and high-strength properties, have seen rising demand driven by increasing defense budgets across the MEA region. For example, Saudi Arabia, with a defense budget of USD 45 billion in 2023, is investing heavily in advanced materials for protective gear and aerospace applications. Aramid fibers play a crucial role in improving the performance of ballistic protection and aircraft parts, reducing weight while maintaining structural integrity. The use of aramid fibers is expanding as defense spending in the UAE and Egypt also sees growth.

High Production Costs: The production of aramid fibers involves complex processes and the use of costly raw materials, which has been a significant challenge for manufacturers in the MEA region. In 2023, the average production cost per ton of aramid fibers in the region was USD 20,000, driven by high energy and labor costs, particularly in countries like Saudi Arabia and the UAE. These high costs limit the adoption of aramid fibers in price-sensitive industries such as consumer goods and textiles, despite their superior properties.

Over the next five years, the MEA aramid fiber market is expected to grow significantly, driven by increasing demand in the defense, aerospace, and automotive sectors. The rising focus on safety regulations and the development of energy-efficient materials will further accelerate the market's expansion. Furthermore, advancements in renewable energy projects and industrial applications will contribute to sustained demand for aramid fibers. This growth will also be propelled by technological innovations and the integration of aramid fibers in new applications, such as hybrid composites used in renewable energy projects. As industrialization across the MEA region progresses, the market is poised to benefit from the increased emphasis on durable and lightweight materials that offer superior performance.

Emerging Applications in Renewable Energy: The renewable energy sector in the MEA region is rapidly expanding, offering new opportunities for the use of aramid fibers. In 2023, renewable energy projects such as wind turbines in Morocco and solar power plants in Egypt are integrating aramid fibers for their durability and resistance to environmental stress. These fibers are used in turbine blades and other components where lightweight and high-strength materials are essential for improving efficiency and longevity. The increasing investment in renewable energy projects presents a significant opportunity for aramid fiber manufacturers.

|

Segment |

Sub-Segments |

|

By Type |

Para-Aramid, Meta-Aramid |

|

By Application |

Protective Apparel, Friction Materials, Optical Fibers |

|

By End-User |

Defense and Aerospace, Automotive, Industrial, Electrical & Electronics |

|

By Form |

Fiber, Pulp, Paper, Fabrics |

|

By Region |

North Africa, GCC, Sub-Saharan Africa, Rest of MEA |

1.1. Definition and Scope

1.2. Market Taxonomy (By Type, Application, End-User, Region)

1.3. Market Growth Rate (CAGR, Year-on-Year Growth)

1.4. Market Segmentation Overview

2.1. Historical Market Size (In Value, By Type, By Application, By End-User, By Region)

2.2. Year-On-Year Growth Analysis (Volume and Value, Market Share)

2.3. Key Market Developments and Milestones (Partnerships, Mergers, Technology Innovations)

3.1. Growth Drivers

3.1.1. Increased Defense and Aerospace Spending

3.1.2. Rise in Automotive Production

3.1.3. Advancements in Safety Equipment

3.1.4. Rising Demand for Lightweight and Durable Materials

3.2. Market Challenges

3.2.1. High Production Costs

3.2.2. Limited Raw Material Availability

3.2.3. Lack of Recycling Infrastructure

3.3. Opportunities

3.3.1. Emerging Applications in Renewable Energy

3.3.2. Growing Demand in the Automotive and Aerospace Sectors

3.3.3. Expansion of Industrial Applications

3.4. Trends

3.4.1. Shift Toward Sustainable and Eco-Friendly Products

3.4.2. Increased Usage in Oil & Gas Sectors

3.4.3. Adoption of Hybrid Aramid Products

3.5. Government Regulations (Compliance With Safety Standards, Emission Norms, Export Regulations)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Manufacturers, Suppliers, Distributors, End-Users)

3.8. Porters Five Forces Analysis

3.9. Competitive Ecosystem

4.1. By Type (In Value %)

4.1.1. Para-Aramid

4.1.2. Meta-Aramid

4.2. By Application (In Value %)

4.2.1. Protective Apparel

4.2.2. Friction Materials

4.2.3. Optical Fibers

4.3. By End-User (In Value %)

4.3.1. Defense and Aerospace

4.3.2. Automotive

4.3.3. Industrial

4.3.4. Electrical & Electronics

4.4. By Form (In Value %)

4.4.1. Fiber

4.4.2. Pulp

4.4.3. Paper

4.4.4. Fabrics

4.5. By Region (In Value %)

4.5.1. North Africa

4.5.2. GCC

4.5.3. Sub-Saharan Africa

4.5.4. Rest of MEA

5.1. Detailed Profiles of Major Companies (Competitors)

5.1.1. Teijin Limited

5.1.2. DuPont de Nemours, Inc.

5.1.3. Kolon Industries Inc.

5.1.4. Hyosung Corporation

5.1.5. Toray Industries, Inc.

5.1.6. Yantai Tayho Advanced Materials Co., Ltd.

5.1.7. Kermel

5.1.8. Huvis Corporation

5.1.9. FibrTec Inc.

5.1.10. SRO Aramid (JSC Kamenskvolokno)

5.1.11. JSC Sintez-Kauchuk

5.1.12. Aramid HPM LLC

5.1.13. Suzhou Zhaoda Special Fiber Co., Ltd.

5.1.14. China National Bluestar (Group) Co., Ltd.

5.1.15. Indian Technical Textiles Co.

5.2. Cross Comparison Parameters (Annual Revenue, Production Capacity, Regional Presence, Product Portfolio, Innovation Pipeline, Employee Strength, Manufacturing Facilities, Strategic Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Product Launches, Collaborations, Supply Chain Enhancements)

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Capex, R&D Spending)

5.7. Venture Capital Funding

5.8. Government Grants and Subsidies

5.9. Private Equity Investments

6.1. Environmental Regulations (Sustainability Standards, Emission Norms)

6.2. Compliance and Certification (ISO, ASTM, REACH Compliance)

6.3. Safety Standards (Industrial and Consumer Protection Norms)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-User (In Value %)

8.4. By Form (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis (End-User Preferences, Product Usage Patterns)

9.3. Marketing Initiatives (Target Market Strategies, Branding Efforts)

9.4. White Space Opportunity Analysis

The first phase involved identifying the critical variables driving the MEA aramid fiber market. Comprehensive desk research was conducted to map the competitive landscape, identify major stakeholders, and assess the influence of macroeconomic factors.

In this phase, historical market data was gathered to understand market penetration and revenue trends. The data was analyzed to identify key growth drivers, challenges, and opportunities across different market segments.

Industry experts were consulted through telephonic interviews to validate the market hypotheses. These consultations helped refine the data and provided additional insights into the markets operational dynamics.

In the final step, the data was synthesized to create a comprehensive market report. Industry players were consulted to verify the accuracy of the findings and to ensure a holistic analysis of the market.

The MEA aramid fiber market was valued at USD 1.3 billion in 2023, driven by the rising demand in defense, aerospace, and industrial applications across the region.

Challenges include high production costs and the lack of a well-established recycling infrastructure. Limited availability of raw materials also hampers the growth potential of the market.

Key players in the market include Teijin Limited, DuPont de Nemours, Kolon Industries, Hyosung Corporation, and Yantai Tayho Advanced Materials. These companies dominate due to their strong technological capabilities and extensive product portfolios.

The market is driven by increasing demand for durable, heat-resistant materials in sectors such as defense, aerospace, and automotive. The growth of infrastructure projects and safety regulations also fuels market expansion.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.