MEA Identity Verification Market Outlook to 2030

Region:Africa

Author(s):Shambhavi

Product Code:KROD2202

Region:Africa

Author(s):Shambhavi

Product Code:KROD2202

December 2024

91

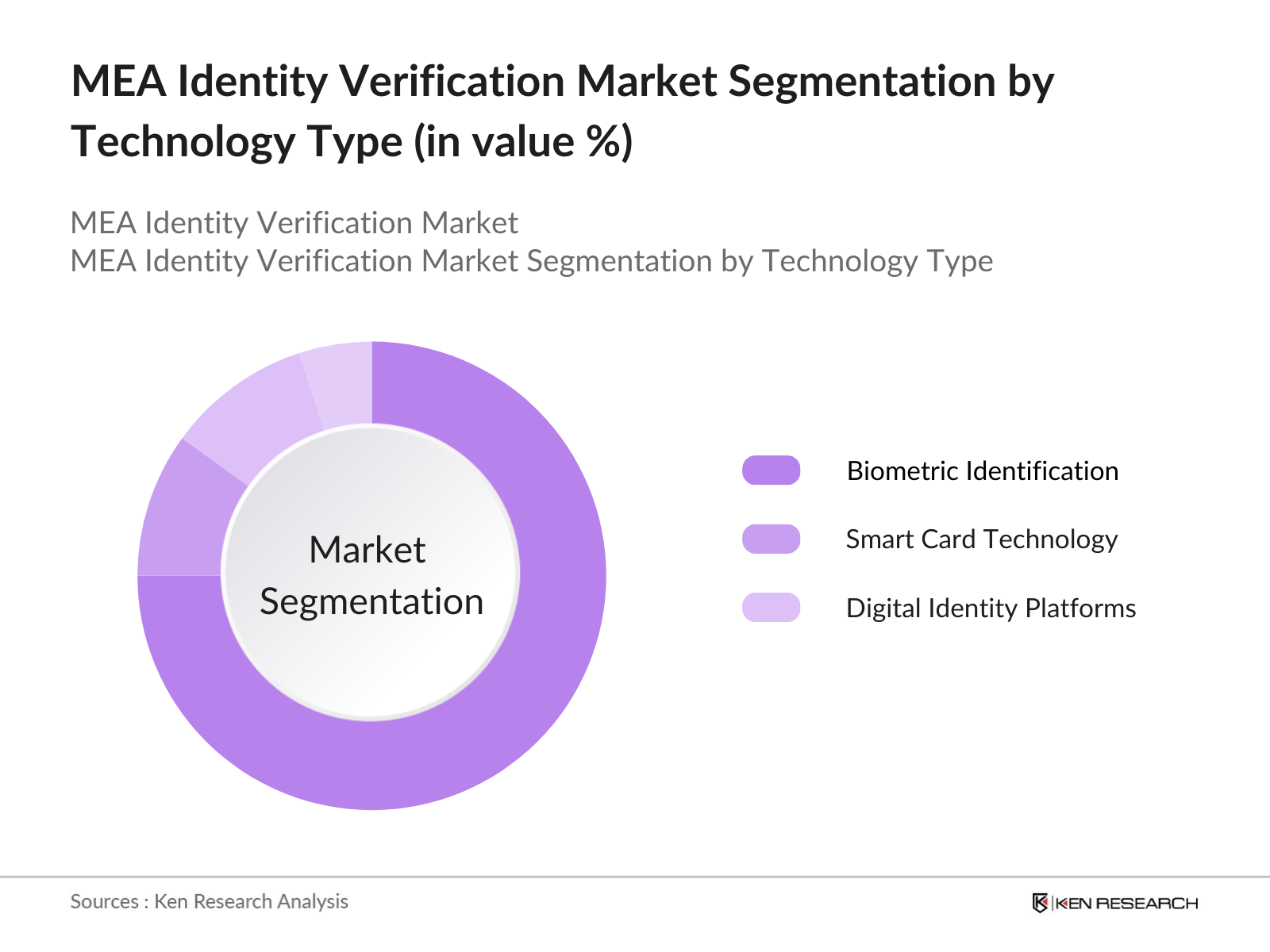

By Technology Type: The MEA identity verification market is segmented by technology type into biometric identification, smart card technology, and digital identity platforms. In 2023, biometric identification had a dominant market share due to its extensive use across various sectors such as banking, healthcare, and government services. The growing emphasis on security and the increasing prevalence of identity theft have spurred the demand for biometric technologies, particularly facial recognition and fingerprint scanning, which are seen as more secure alternatives to traditional methods of identification.

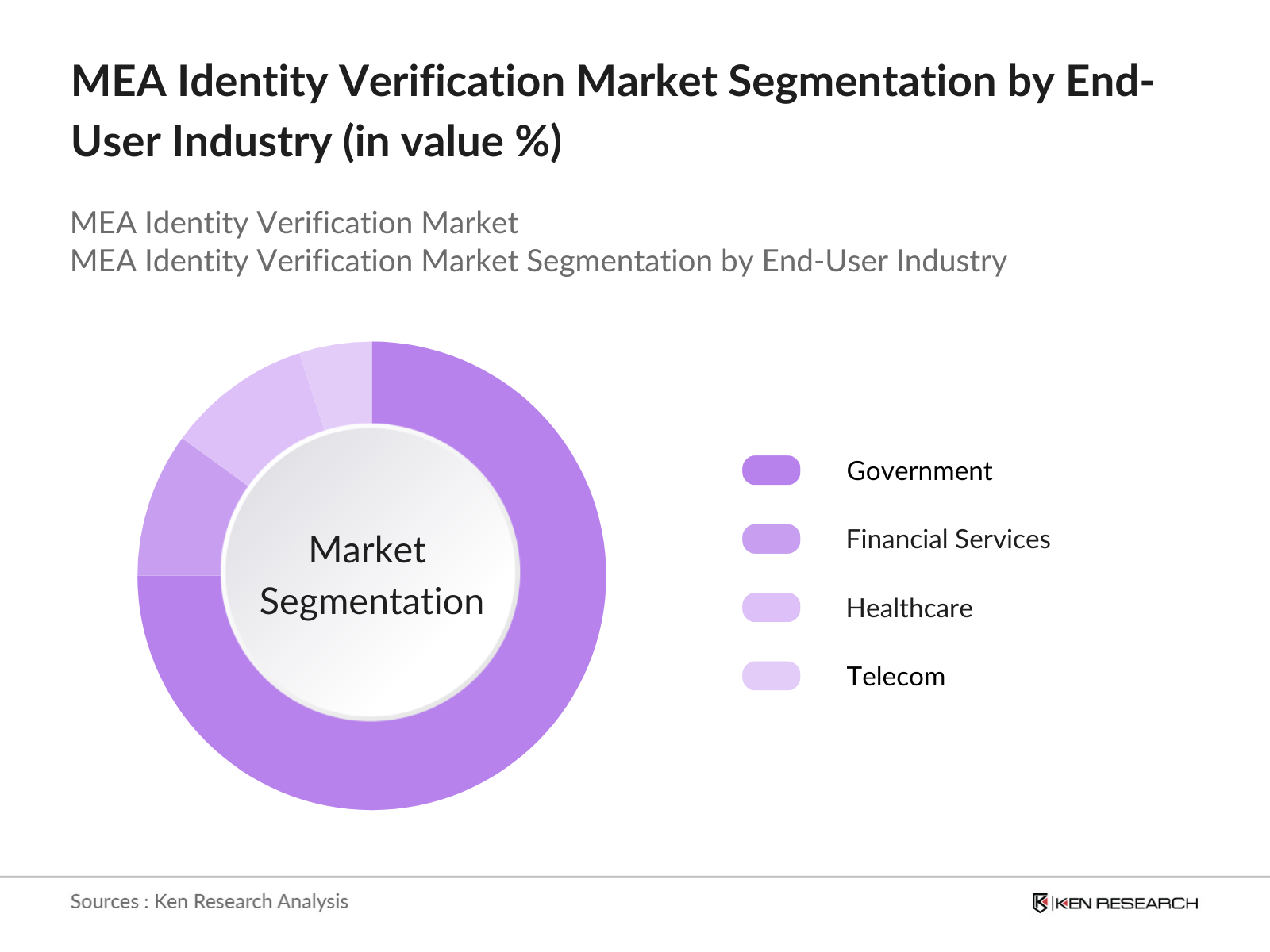

By End-User Industry: By end-user industry, the market is segmented into government, financial services, healthcare, and telecom. In 2023, the financial services industry held the largest share of the identity verification market in MEA. This is driven by the growing need for secure, seamless digital banking solutions, coupled with an increasing shift towards online and mobile banking services. Financial institutions are integrating digital identity verification systems to ensure security, streamline processes, and comply with stringent regulatory requirements. Additionally, biometric solutions are being employed for fraud prevention and customer onboarding.

By Region: The MEA identity verification market is also segmented by regions, including Israel, United Arab Emirates, Jordan, Morocco, South Africa, and the rest of MEA. In 2023, the United Arab Emirates held the dominant market share due to its advanced digital infrastructure and government initiatives aimed at improving identity verification services. The UAE government has made significant investments in digital identity systems, including the Emirates Digital Identity System, which simplifies access to e-government services and ensures secure digital transactions.

|

Company |

Establishment Year |

Headquarters |

|

Thales Group |

2000 |

Paris, France |

|

IDEMIA |

2007 |

Courbevoie, France |

|

HID Global |

1991 |

Austin, Texas, USA |

|

NEC Corporation |

1899 |

Tokyo, Japan |

|

Gemalto |

2006 |

Meudon, France |

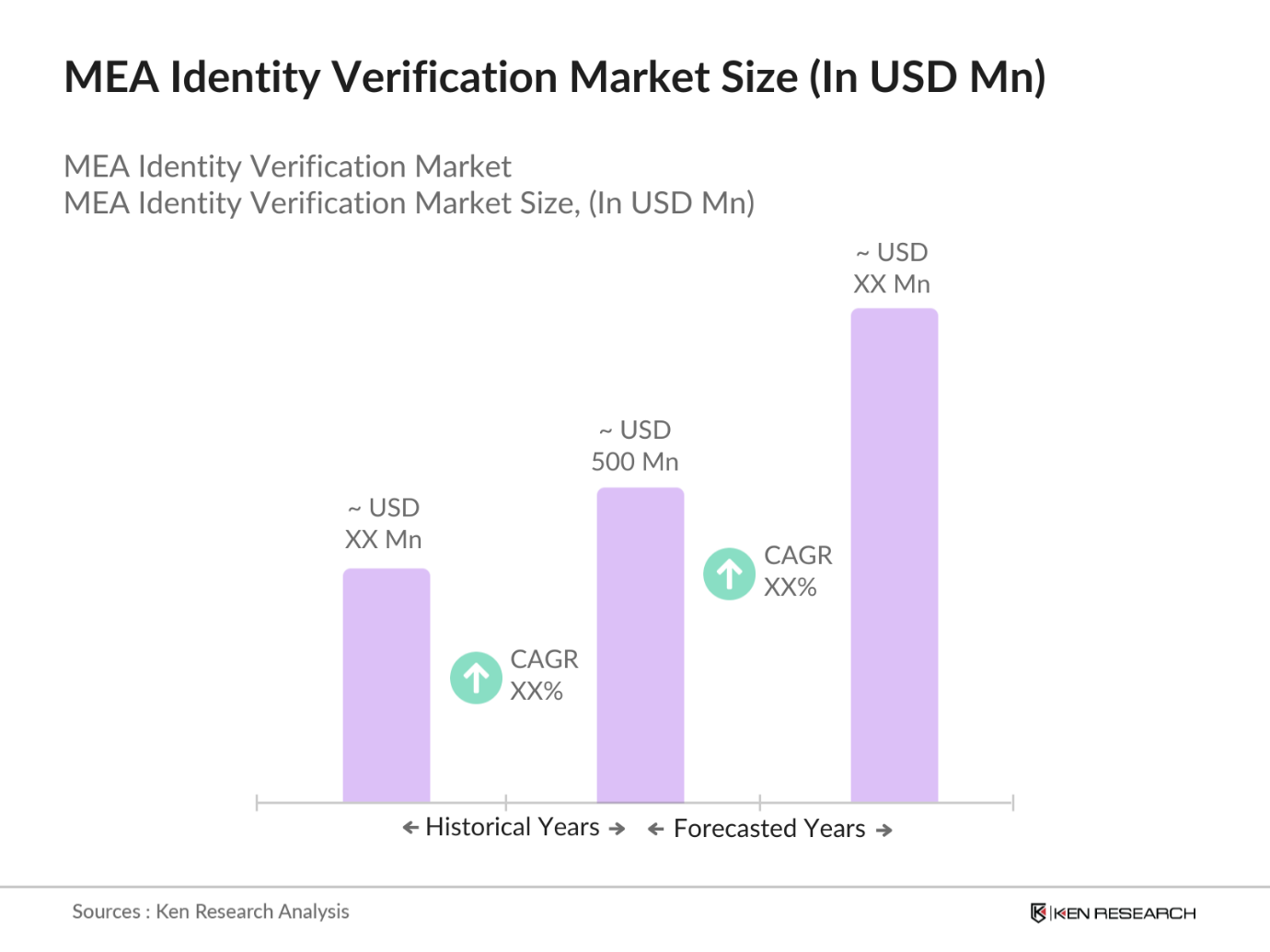

The MEA identity verification market is set to experience rapid expansion over the next five years, driven by a combination of government initiatives, the proliferation of biometric technologies, and rising demand for secure digital transactions. Governments in the region, particularly in the UAE and Saudi Arabia, are leading the charge with large-scale national identity programs that aim to bring digital services to their populations, improving public sector efficiency and security. Additionally, the growing need for identity verification in sectors such as financial services, healthcare, and e-commerce is expected to continue propelling the market forward.

|

By Technology Type |

Biometric Identification Smart Card Technology Digital Identity Platforms |

|

By End User |

Government Financial Services Healthcare Telecom |

|

By Region |

Israel United Arab Emirates Jordan Morocco South Africa Rest of MEA |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics Overview

1.4. MEA Identity Verification Market Ecosystem

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing demand for biometric verification in banking and financial services

3.1.2. Government-led national identity programs

3.1.3. Rise of e-commerce and digital payments requiring secure identity verification

3.2. Market Challenges

3.2.1. High implementation costs

3.2.2. Data privacy concerns

3.2.3. Lack of digital infrastructure in rural areas

3.3. Market Opportunities

3.3.1. Expansion to small and medium-sized enterprises

3.3.2. Adoption of biometric technologies in healthcare and e-government services

3.3.3. Potential for international collaborations

3.4. Market Trends

3.4.1. AI integration in biometric verification

3.4.2. Mobile-based identity verification solutions

3.4.3. Blockchain for enhanced security

3.5. Government Regulations

3.5.1. UAEs Emirates Digital Identity System (2023)

3.5.2. Saudi Arabias National Digital Transformation Program (2023)

3.5.3. South Africas Biometric National ID Program (2022)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

4.1. By Technology Type (in value %)

4.1.1. Biometric Identification

4.1.2. Smart Card Technology

4.1.3. Digital Identity Platforms

4.2. By End-User Industry (in value %)

4.2.1. Government

4.2.2. Financial Services

4.2.3. Healthcare

4.2.4. Telecom

4.3. By Solution Type (in value %)

4.3.1. Identity Verification Solutions

4.3.2. Authentication and Access Management

4.3.3. Biometric Data Capture Solutions

4.4. By Deployment Type (in value %)

4.4.1. On-premise

4.4.2. Cloud-based

4.5. By Region (in value %)

4.5.1. Israel

4.5.2. United Arab Emirates

4.5.3. Jordan

4.5.4. Morocco

4.5.5. South Africa

4.5.6. Rest of MEA

5.1. Detailed Profiles of Major Companies

5.1.1. Thales Group

5.1.2. IDEMIA

5.1.3. HID Global

5.1.4. NEC Corporation

5.1.5. Gemalto

5.1.6. Accenture

5.1.7. Cognitec Systems

5.1.8. Suprema Inc.

5.1.9. Veridos

5.1.10. BioID

5.1.11. FaceTec

5.1.12. Innovatrics

5.1.13. Iris ID Systems

5.1.14. Smartmatic

5.1.15. ZKTeco

5.2. Cross-Comparison Parameters (number of employees, headquarters, inception year, revenue)

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants and Investments

6.4.3. Private Equity Investments

7.1. Identity Verification Standards

7.2. Compliance Requirements

7.3. Certification Processes

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9.1. By Technology Type (in value %)

9.2. By End-User Industry (in value %)

9.3. By Solution Type (in value %)

9.4. By Deployment Type (in value %)

9.5. By Region (in value %)

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

Ecosystem creation for all major entities and referring to multiple secondary and proprietary databases to perform desk research around the market to collate market-level information.

Collating statistics on the MEA Identity Verification Market over the years, analyzing the penetration of MEA Identity Verification technologies, and computing the revenue generated for the market. This step also involves reviewing technology adoption rates and application effectiveness to ensure accuracy behind the data points shared.

Building market hypotheses and conducting CATIs with market experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Our team will approach multiple MEA Identity Verification companies to understand the nature of technology segments, consumer preferences, and other parameters. This supports validating statistics derived through a bottom-to-top approach from these MEA Identity Verification companies, ensuring accuracy and reliability in the report.

The MEA identity verification market was valued at USD 500 million in 2023, driven by increasing government-led initiatives for digital transformation, the proliferation of biometric technologies, and growing demand for secure digital transactions across various sectors.

Key challenges include data privacy concerns, high implementation costs, and the lack of digital infrastructure in rural areas. Additionally, regulatory hurdles and the high cost of biometric technologies pose significant barriers to market expansion, especially in less economically developed regions.

Major players in the MEA identity verification market include Thales Group, IDEMIA, HID Global, NEC Corporation, and Gemalto. These companies lead the market due to their advanced biometric solutions, strong government partnerships, and extensive technological expertise.

Growth is driven by the increasing adoption of biometric authentication in financial services, national digital identity programs in countries like the UAE and Saudi Arabia, and the rise in e-commerce activities that require secure digital verification systems. These factors contribute to the growing demand for advanced identity solutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.