Philippines Auto Loan Market Outlook to 2029

Philippines Auto Loan Market: Growth Drivers, Trends & Future Outlook to 2030

Region:Philippines

Author(s):Harsh Saxena

Product Code:KR1527

Region:Philippines

Author(s):Harsh Saxena

Product Code:KR1527

August 2025

90

By Type: The market is segmented into various types of auto loans, including new vehicle financing, used vehicle financing, dealer/OEM captive financing programs, and loan refinancing and balance transfer. The new vehicle financing segment dominates the market, driven by the increasing preference for brand-new cars among consumers. This trend is influenced by the availability of attractive financing options from banks and captives, promotional offers from dealerships tied to sustained growth in new vehicle sales, and consumer demand for updated tech and safety features.

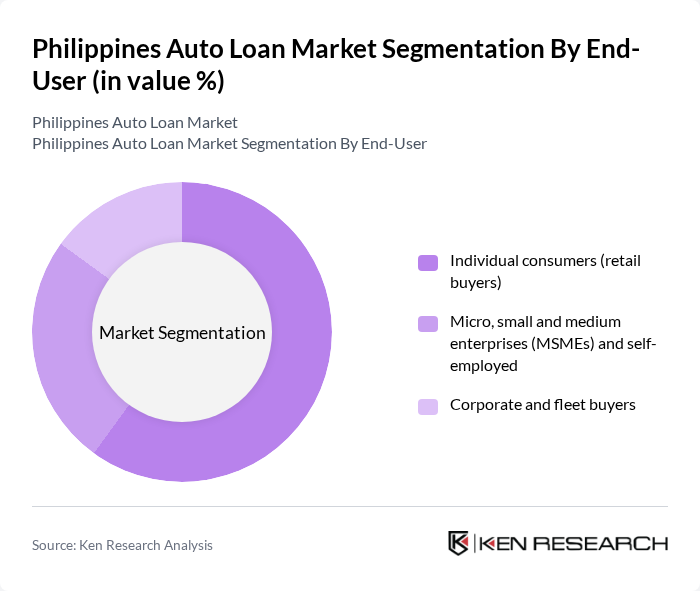

By End-User: The auto loan market is segmented by end-users, including individual consumers, micro, small, and medium enterprises (MSMEs), and corporate and fleet buyers. Individual consumers represent the largest segment in the auto loan market, driven by the increasing need for personal transportation and the growing trend of vehicle ownership among Filipinos. The rise in disposable income and the availability of flexible financing options have made it easier for individuals to purchase vehicles, aided by faster digital onboarding and online applications offered by banks and captives.

The Philippines Auto Loan Market is characterized by a dynamic mix of regional and international players. Leading participants such as BDO Unibank, Inc., Bank of the Philippine Islands (BPI), Metropolitan Bank & Trust Company (Metrobank), Security Bank Corporation, Union Bank of the Philippines (UnionBank), contribute to innovation, geographic expansion, and service delivery in this space, with digitization initiatives and EV-oriented financing products gaining traction.

| BDO Unibank, Inc. | 1968 | Makati City, Philippines | – | – | – | – | – | – |

| Bank of the Philippine Islands (BPI) | 1851 | Makati City, Philippines | – | – | – | – | – | – |

| Metropolitan Bank & Trust Company (Metrobank) | 1962 | Makati City, Philippines | – | – | – | – | – | – |

| Security Bank Corporation | 1951 | Makati City, Philippines | – | – | – | – | – | – |

| Union Bank of the Philippines (UnionBank) | 1982 | Pasig City, Philippines | – | – | – | – | – | – |

| Company | Establishment Year | Headquarters | Portfolio size (auto loans outstanding, PHP) | Disbursements (annual new auto loans, PHP) | Approval rate (%) | Average interest rate (APR or add-on, %) | Average processing time (application to release, days) | NPL ratio/default rate (%) |

|---|

The Philippines auto loan market is poised for significant transformation in the coming years, driven by technological advancements and changing consumer preferences. The rise of digital platforms will facilitate easier access to loans, while the increasing focus on sustainable financing will align with global trends. Additionally, as the automotive market shifts towards electric vehicles, lenders will need to adapt their offerings to meet the evolving demands of environmentally conscious consumers. Overall, the market is expected to evolve dynamically, presenting both challenges and opportunities for stakeholders.

| By Type |

New vehicle financing (brand-new passenger cars and light commercial vehicles) Used vehicle financing (pre-owned cars) Dealer/OEM captive financing programs Loan refinancing and balance transfer |

| By End-User |

Individual consumers (retail buyers) Micro, small, and medium enterprises (MSMEs) and self-employed Corporate and fleet buyers |

| By Loan Amount |

Below PHP 500,000 PHP 500,000 - PHP 1,000,000 Above PHP 1,000,000 |

| By Loan Tenure |

Short-term loans (1-3 years) Medium-term loans (4-5 years) Long-term loans (6-7 years) |

| By Interest Rate Type |

Fixed interest rates Variable interest rates |

| Scope Item/Segment | Sample Size | Target Respondent Profiles |

|---|---|---|

| Auto Loan Customers | 150 | Individuals who have taken auto loans in the last 2 years |

| Bank Loan Officers | 100 | Loan officers from major banks and financial institutions |

| Automobile Dealerships | 80 | Finance managers and sales executives at car dealerships |

| Financial Analysts | 50 | Analysts specializing in automotive finance and lending |

| Regulatory Bodies | 40 | Officials from the Bangko Sentral ng Pilipinas and other regulatory agencies |

The Philippines Auto Loan Market is valued at approximately PHP 650 billion, reflecting the scale of outstanding auto finance and disbursements, driven by a rebound in vehicle sales and financing penetration among banks and captive finance companies.

Metro Manila, Cebu, and Davao are the dominant regions in the Philippines Auto Loan Market. Metro Manila leads in auto loan credit disbursement due to its dense population and concentration of banks and dealerships, while Cebu and Davao benefit from expanding urban economies.

The market is segmented into new vehicle financing, used vehicle financing, dealer/OEM captive financing programs, and loan refinancing. Each segment caters to different consumer needs, with new vehicle financing currently dominating due to consumer preferences for brand-new cars.

The market is projected to grow significantly, driven by increasing disposable income, expanding vehicle sales, and competitive interest rates. The average household income is expected to rise, enabling more consumers to consider auto loans for vehicle purchases.

The market faces challenges such as high default rates, currently around 5.5%, and limited financial literacy among consumers. Economic uncertainties and a lack of understanding of loan terms can hinder consumer engagement and increase default risks.

The Philippine government supports the automotive industry through policies like the Electric Vehicle Industry Development Act (EVIDA), which promotes electric vehicle adoption and related financing products. These initiatives aim to enhance sustainable transport and stimulate the auto loan market.

The average interest rate for auto loans in the Philippines is around 8.0%. This competitive rate is maintained by the Bangko Sentral ng Pilipinas' stable monetary policy, encouraging consumers to finance vehicle purchases through loans.

Key players in the Philippines Auto Loan Market include BDO Unibank, Bank of the Philippine Islands (BPI), Metropolitan Bank & Trust Company (Metrobank), and Security Bank Corporation. These institutions contribute to innovation and service delivery in auto financing.

The shift towards digitalization has led to a 35% increase in online auto loan applications. Consumers prefer the convenience of applying online, prompting financial institutions to enhance their digital platforms to capture this growing segment effectively.

Partnerships between lenders and automotive dealers facilitate seamless financing options at the point of sale, enhancing the purchasing experience for consumers. Over 45% of auto loans are now originated through these dealer partnerships, making them crucial for market growth.

The Philippines Auto Loan Market is expected to undergo significant transformation, driven by technological advancements and a focus on sustainable financing. The rise of electric vehicles and digital platforms will shape the market, presenting both challenges and opportunities for stakeholders.

Auto loans in the Philippines include new vehicle financing, used vehicle financing, dealer/OEM captive financing programs, and loan refinancing. Each type caters to different consumer needs, reflecting the diverse landscape of auto financing in the country.

Factors contributing to the rising demand for auto loans include increasing disposable income, expanding urbanization, competitive interest rates, and a growing middle class. These elements enable more consumers to finance vehicle purchases, driving market growth.

Limited financial literacy among Filipinos, with only 30% understanding basic financial concepts, affects auto loan uptake. This gap can lead to poor financial decisions regarding loans, resulting in higher default rates and reluctance to engage with financial institutions.

The Electric Vehicle Industry Development Act (EVIDA) is significant as it promotes the adoption of electric vehicles in the Philippines. It provides incentives for EV financing, aligning with global trends towards sustainable transport and enhancing the auto loan market's growth potential.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.