Colocation Data Centers in APAC – Market Trends, Strategic Insights & Growth Opportunities

This Point of View unpacks market trends, growth hubs, and strategic priorities shaping the 2024–2028 colocation boom.

This Point of View unpacks market trends, growth hubs, and strategic priorities shaping the 2024–2028 colocation boom.

15 Slide Report | Market Forecasts & Size Expansion | Country-Specific Leadership | Competitive Landscape

Built for Leaders Across

- Founders and strategy heads at data center operators

- Digital infrastructure investors and sovereign funds

- Cloud providers, OTT players, and enterprise IT decision-makers

- Policymakers framing data localization and infrastructure policy

Access Market Maps, Country Benchmarks, and ROI Models for Colocation Growth

Executive Summary

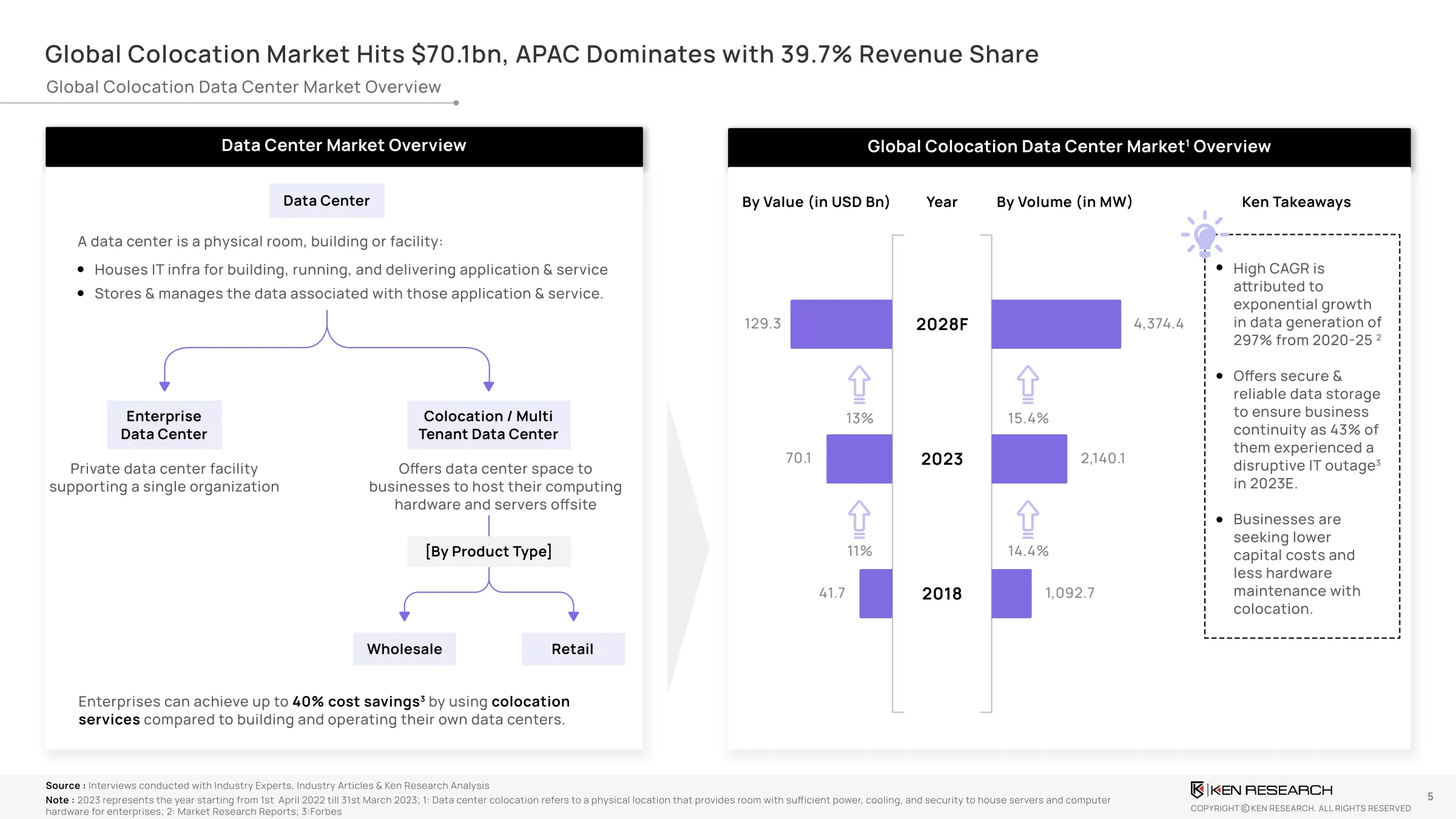

The global colocation market grew fromUSD 41.7B (2018)toUSD 70.1B (2023)and is expected to hitUSD 129.3B by 2028. APAC commands the lead with a39.7% revenue share, driven by data-intensive sectors and sovereign digital strategies.

Key catalysts include:

- 5G and OTT demandfueling rack densification and cross-border edge computing

- $570B+FDI inflows into APAC targeting digital infrastructure

- 1.4 trillion USDin projected IT spend in APAC (2024)

Market Structure & Segmentation

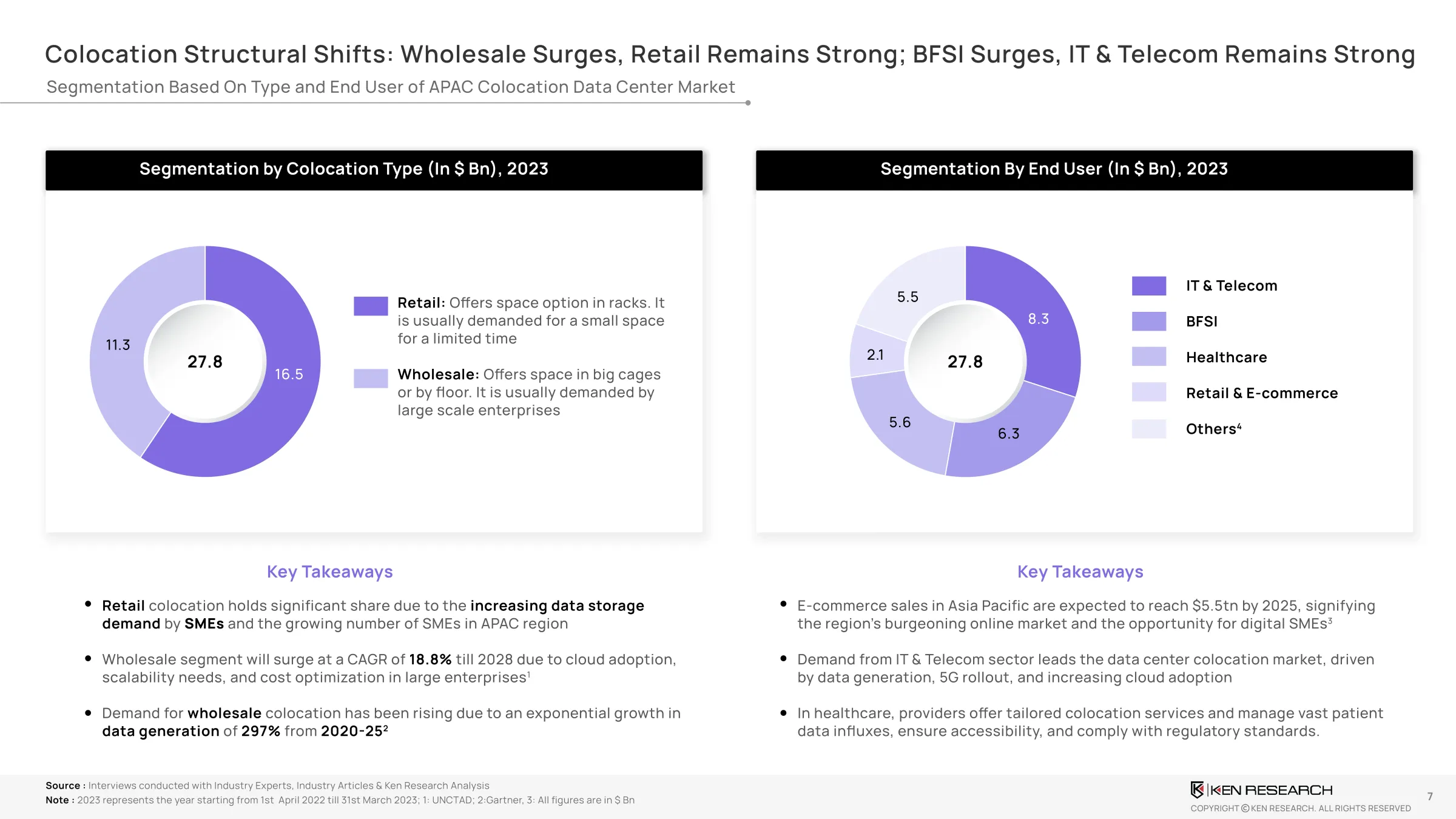

By Colocation Type:

- Retail Colocation (USD 16.5B, 2023): Dominated by SMEs and decentralized operations

- Wholesale Colocation (USD 11.3B, 2023): Fastest-growing at18.8% CAGR, driven by hyperscalers

By End-Use Sector:

- IT & Telecom (USD 8.3B): 5G expansion, cloud-native deployments

- BFSI (USD 6.3B): Regulatory compliance, disaster recovery

- Healthcare, Retail, E-Commerce: AI processing, real-time logistics, and video streaming

Access Segment-Level Growth Maps and Sector Demand Snapshots

Country Snapshot – Growth & Competitive Landscape

Country | 2023 Share | CAGR (2023–28) | Key Drivers |

China | 30.3% | 13.4% | Alibaba/Tencent infra, Made in China 2025 |

India | 12.4% | 21.7% | OTT growth, Digital India, FDI-led DC investments |

Japan | 16.1% | 17.6% | Global connectivity hub, submarine cable investments |

Indonesia | 5.5% | 16.9% | Startups, e-commerce, tax incentives |

Singapore | 7.4% | 13.9% | Data governance leadership, smart grid integration |

Download Country-Specific Colocation Benchmarks & Opportunity Grids

Opportunity Zones – Where to Invest & Scale

- India Tier II Cities: Noida, Hyderabad, Pune emerging as cost-effective DC hubs

- Indonesia & Vietnam: Underserved SME market, low penetration, high margin

- Singapore Edge Nodes: Smaller, energy-efficient DC formats for urban deployment

Explore Emerging Cities, Power Zones, and Land Cost Grids for Buildouts

Strategic Moves by Industry Leaders

- Equinix: Acquired GPX India DCs for USD 161M, 100% renewable APAC coverage

- Digital Realty: 250MW DC in Sydney, USD 250M expansion in Mumbai

- NTT: USD 2B invested in India; built 45MW Jakarta site, expanded to Noida

- China Telecom: Operates450+ on-net DCs, deploying 40,000 HPC racks in Shanghai

Future-Ready Strategies For Operators

- Retail Colocation Customization: Modular service tiers to capture SME & fintech demand

- Certified Government Workloads: Launch domestic-compliant DCs with EDB/IMDA partnerships (SG)

- Sustainable Cooling: Shift to Direct Liquid Cooling and AI-driven airflow for power density optimization

- OEM Co-Development: Launch cloud-native colocation blueprints with AWS, GCP, or Azure

Download Operator Playbook with Margin Benchmarks and Tiered Offerings

Roi Metrics & Financial Modeling Insights

- Colocation ROI timeline: 3.2–4.5 years (median); up to25–30% EBITDA marginfor efficient rack scaling

- Power-efficient DCswith PUE < 1.5 outperform older facilities by35% cost savingsannually

- Land + Power Capex recoveryaccelerates with multi-tenant layering and SLA optimization

Access ROI Calculator and Margin Sensitivity Templates for Operators and Funds

The Next Five Years In Colocation

Colocation is no longer optional—it is foundational to APAC’s cloud-first, data-resilient, and AI-enabled future. Operators that align with national priorities, offer modular scalability, and build for green power and AI workloads will dominate the region’s USD 55B+ opportunity by 2028.

Get the Full APAC Colocation Strategy Brief for 2024–2028 Planning

FAQ's

Still Got Questions? Connect Via Mail

What is APAC’s share in the global colocation data center market (2023)?

With 39.7%, APAC region is leading global colocation data center market.

Which segment is growing fastest?

Wholesale colocation (CAGR 18.8%), fueled by hyperscaler expansions

Which country offers highest CAGR potential?

India, expected to grow at 21.7% CAGR till 2028, driven by cloud & OTT traffic

What’s the ROI horizon for new builds?

3–4 years in core and Tier II cities with optimized utilization and power contracts

What makes colocation attractive over in-house data centers?

Up to 40% cost savings, rapid deployment, and zero maintenance burden for clients