How Mechanization Can Solve the Productivity Gap in Southeast Asia’s Agriculture Sector

Download the Full Consulting POV Now

Overview

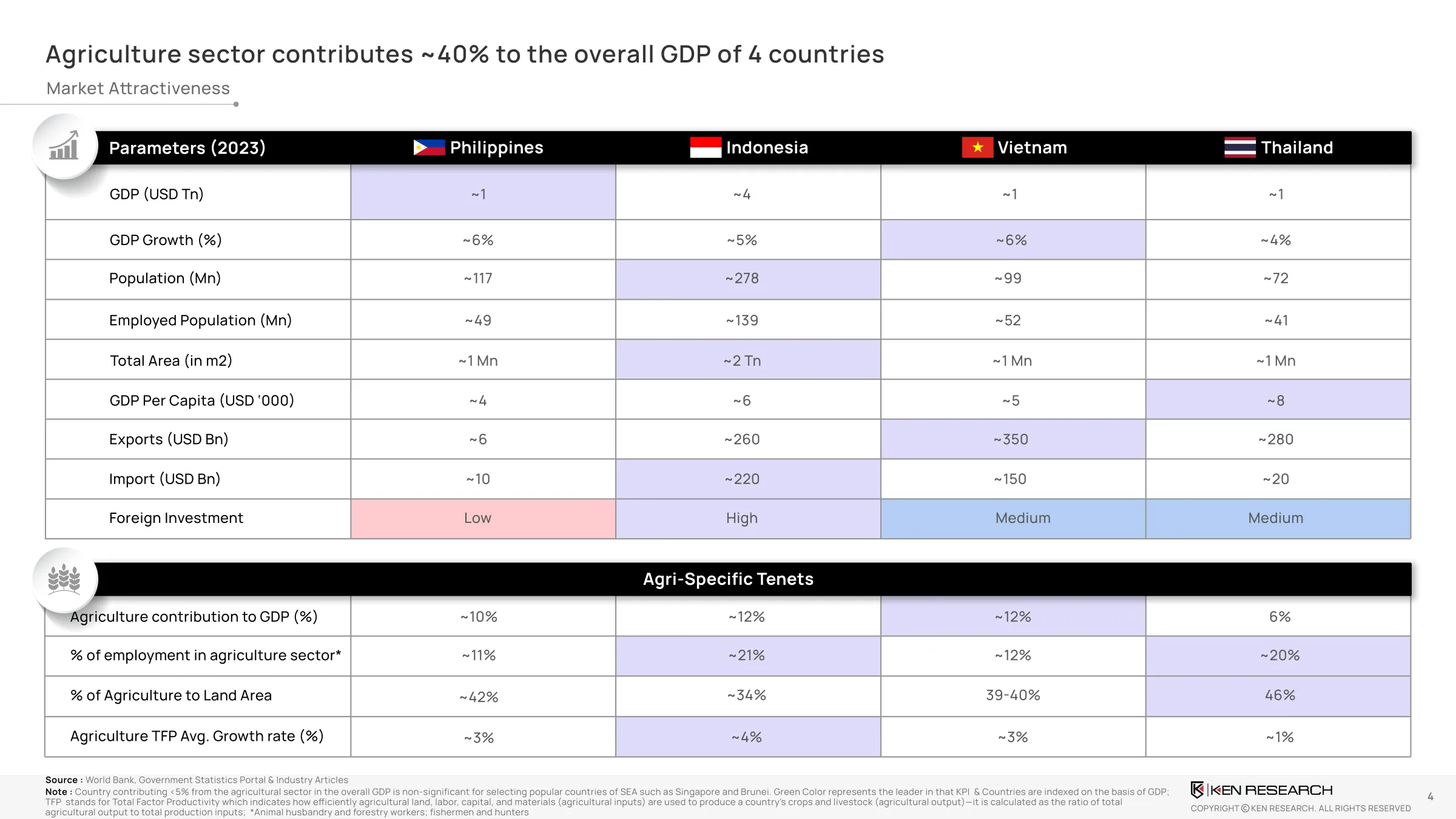

The agriculture sector contributes ~40% to the GDP of Southeast Asian countries such as Thailand, Vietnam, Indonesia, and the Philippines. Despite this, the region’s agri-equipment adoption remains limited due to fragmented infrastructure, weak capital access, and underdeveloped digital presence. While paddy remains the leading crop across all four nations, crop-specific mechanization is under-penetrated, and most farmers rely on traditional methods. This writeup highlights key operational challenges, market disparities, and a future roadmap for enhancing mechanization via rental models, R&D-driven products, and smart technologies like IoT, AI, and precision farming tools.

What Are the Core Challenges

- Low Equipment Penetration:Despite high agricultural output, countries like Vietnam and Indonesia still face low farm-level equipment availability. Thailand is currently leading the region in adoption, but even here, smallholder farmers find it difficult to access modern tools.

- Limited Access to Capital:Agricultural equipment ownership is skewed due to affordability issues. In markets like the Philippines, annual farmer income is ~$3,600, making direct equipment purchase challenging. Hence, rental penetration remains low and informal.

- Digital Fragmentation:Equipment OEMs lack digital discoverability in rural areas, and localized after-sales service is poor. Digital rental platforms and maintenance support are nearly non-existent across Tier 2–3 towns.

- Operational Gaps:Maintenance costs and lack of crop-specific variants prevent adoption. Most available tools are not aligned to soil and crop types prevalent in SEA countries.

Root Cause Analysis

- Affordability Mismatch:Farmer income ranges between $3,000–$9,000 annually, while quality agri equipment typically costs 3–5x that amount. Even with leasing models, financial penetration is low.

- Lack of Rental Infrastructure:There is a critical absence of rental models such as pay-per-use, lease-to-own, or seasonal leasing. Existing infrastructure is fragmented, with no aggregation model to serve rural markets.

- Technology Underuse:Technologies like autonomous tractors (Kubota), smart harvesters (AGCO), and cloud-based diagnostic tools exist, but adoption remains limited due to complexity and lack of awareness among smallholders.

- Low R&D Spend:Product development is not aligned to SEA's crop diversity. Countries such as Indonesia and Vietnam lack localized machinery for cassava, maize, and rubber production.

The Southeast Asia Advantage & Potential Solutions

- Strong Agricultural Base:Thailand, Vietnam, Indonesia, and the Philippines collectively represent over 61% of SEA’s agricultural output. These countries have significant land allocation to farming (35–46%) and high workforce participation (12–21%).

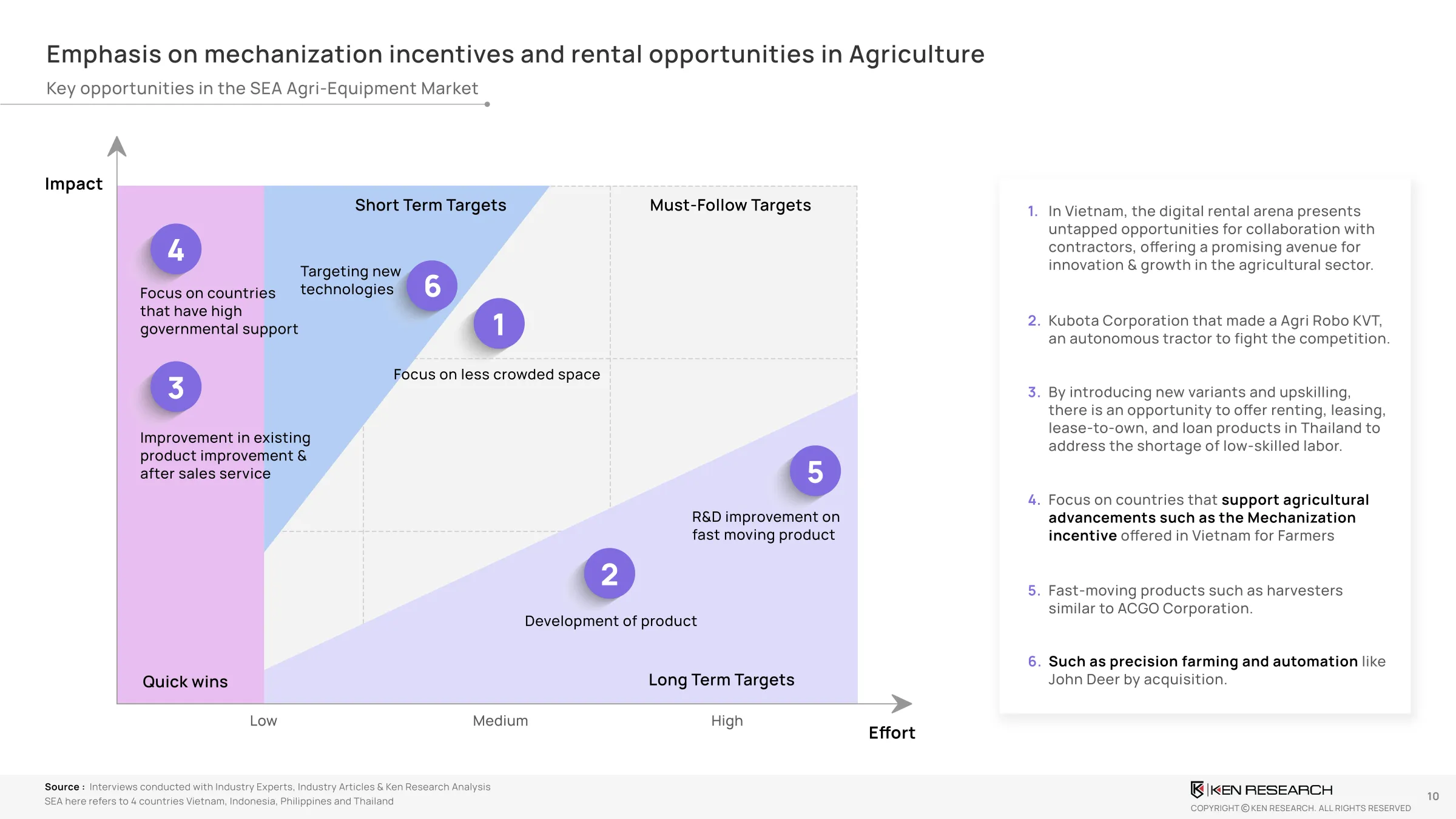

- Government Support:Vietnam offers mechanization incentives for smart harvesters. Thailand supports lease-to-own models to offset labour shortages.

- Emerging Rental Opportunities:Vietnam is emerging as a target market for digital rental platforms. Cloud-based equipment leasing integrated with contractor networks can address current accessibility barriers.

- Tech Stack Expansion:Integration of IoT sensors, satellite mapping, precision farming tools, and AI-based crop planning is gaining traction across SEA. Government initiatives now include agri-sensor networks, drone integration, and agri-cloud adoption.

Roadmap for Execution

Short-Term (0–1 Year) – Awareness & Pilot Models

- Launch government-OEM awareness campaigns in rural districts to promote basic mechanization.

- Initiate public-private pilots for equipment leasing via cooperatives and local contractors.

- Promote digital visibility of OEMs via mobile-first listings, service apps, and vernacular campaigns.

Mid-Term (1–3 Years) – Integration & Product Localization

- Develop country-specific rental models (lease-to-own, subscription-based) with embedded service.

- Incentivize product development for cassava, sugarcane, and multi-crop use.

- Enable cloud platforms for diagnostics, maintenance tracking, and remote advisory.

Long-Term (3–5 Years) – Smart Mechanization Infrastructure

- Scale autonomous tools like robotic tractors and harvesters with AI-backed systems.

- Expand cross-border tech cooperation for R&D on SEA crop-specific solutions.

- Establish a regional digital agri-equipment registry for usage, uptime, and asset tracking.

What is the Future Agri-Tech?

The future of agriculture in Southeast Asia hinges on smart, affordable mechanization. By solving for cost, reach, and product-market fit, the region has the potential to unlock a USD 50 billion opportunity in digital agri-equipment services by 2030. Policymakers, OEMs, fintech platforms, and R&D institutes must act together to make mechanization inclusive, data-driven, and scalable across the region.