Why Are Indian Car Buyers Considering EVs but Still Choosing ICE?

Ken Research

June 10, 2026 - 8 min read

June 10, 2026

by Ken ResearchKey Findings from 5,000 Indian Car Buyers

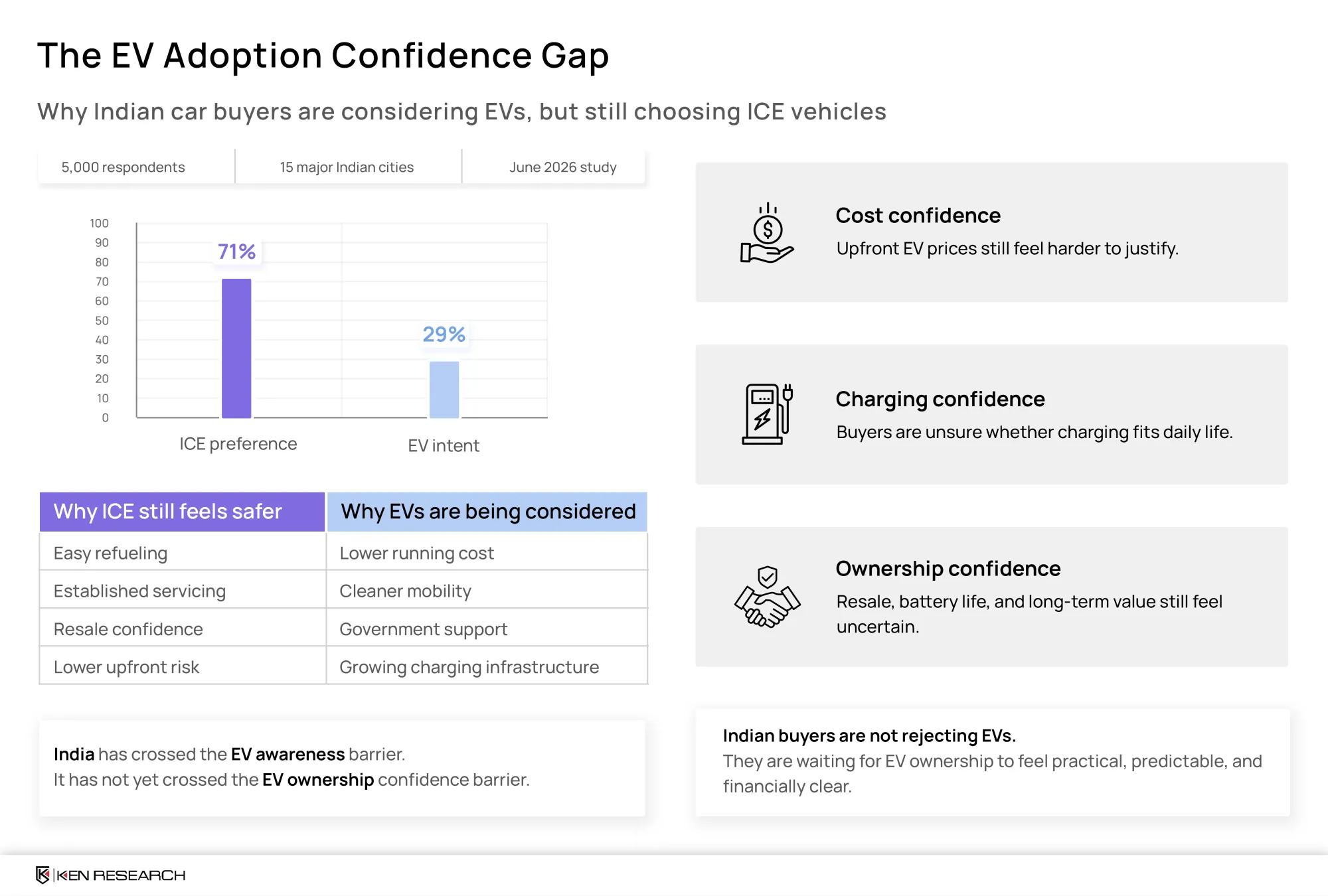

- 29% of Indian car buyers showed EV purchase intent, while 71% still preferred ICE vehicles.

- The 26-40 age group accounts for 65% of EV purchase intent.

- EVs currently carry an upfront price premium of Rs 1 lakh to Rs 4 lakh compared with comparable ICE vehicles.

- Charging confidence, resale value concerns, battery-life questions, and ownership uncertainty remain key EV adoption barriers.

- SUV and sedan owners show stronger EV switching intent than hatchback owners.

- Environmental awareness is high, but ownership confidence is still significantly lower.

Executive Summary

India's four-wheeler mobility market is entering a new phase of transformation. Awareness of electric vehicles has increased substantially, and EVs are now firmly part of the purchase consideration set for urban consumers. However, despite growing interest, most buyers continue to choose internal combustion engine vehicles when making the final purchase decision.

A Ken Research field-based study of 5,000 respondents across 15 major Indian cities shows that 29% of respondents are considering EVs, while 71% continue to prefer ICE vehicles. The findings suggest that India has largely crossed the awareness stage of EV adoption. The next challenge is building confidence around ownership, charging convenience, resale value, and long-term economics. For wider market context, this article should connect to the India electric vehicle market pages.

The future of EV adoption in India will depend less on awareness campaigns and more on making ownership practical, predictable, and financially compelling.

India EV Market Has Interest, but ICE Still Feels Familiar

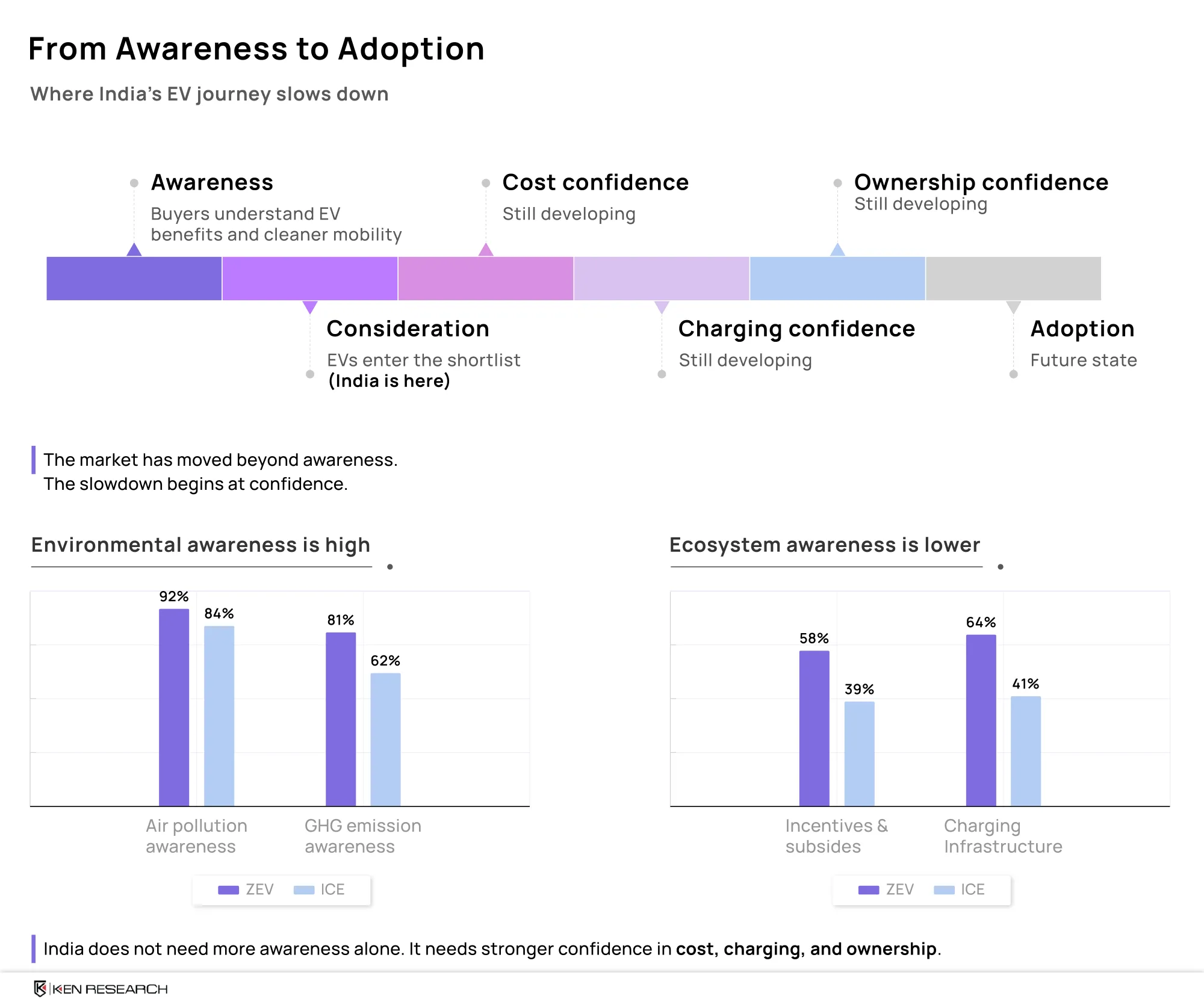

India's passenger vehicle market has moved beyond basic EV awareness. Consumers increasingly understand the environmental and operating cost benefits associated with electric mobility. However, awareness does not automatically convert into purchase.

ICE vehicles continue to offer familiarity, convenience, and predictability. Buyers understand fuel availability, maintenance requirements, servicing networks, and resale dynamics. These factors create a sense of ownership confidence that many EVs have yet to establish. The broader automotive and automotive components market continues to influence buyer trust, servicing access, component availability, and long-term ownership expectations.

The gap between EV consideration and EV purchase highlights a critical reality: India has crossed the awareness barrier but has not yet crossed the confidence barrier.

Who Is More Likely to Consider EVs in India?

The strongest EV purchase intent is concentrated among working-age urban consumers. These buyers are more likely to compare fuel savings, daily commute patterns, ownership economics, and long-term vehicle value before making the purchase decision.

Age Profile of EV-Intent Buyers

Age Group | Share of Respondents |

18-25 | 14% |

26-32 | 34% |

33-40 | 31% |

41-50 | 15% |

50+ | 6% |

The 26-40 age group represents 65% of all EV-intent respondents. This segment typically has stable income streams, daily commuting needs, and higher exposure to mobility trends.

Gender, Occupation, and Education Profile

Profile Parameter | Respondent Split |

Gender | Male: 73%; Female: 27% |

Occupation | Private salaried: 51%; Self-employed: 16%; Business owners: 15%; Others: 18% |

Education | Above graduate: 55.0%; Graduate: 42.1%; Others: 2.9% |

For EV manufacturers, this means future growth will depend on demonstrating practical ownership benefits rather than relying only on sustainability messaging.

Why Awareness Is Not Converting into EV Adoption?

Environmental awareness among Indian consumers is already strong. The adoption challenge is not limited to whether consumers understand the benefits of EVs. The bigger challenge is whether they trust the ownership ecosystem.

Environmental Awareness Is Strong

Metric | ZEV Respondents | ICE Respondents |

Air pollution awareness | 92% | 84% |

Noise pollution awareness | 78% | 71% |

GHG emission awareness | 81% | 62% |

Perceived EV Benefits Are Also Visible

Benefit | ZEV Respondents | ICE Respondents |

Improved air quality | 88% | 70% |

GHG reduction | 74% | 55% |

Urban mobility benefits | 61% | 42% |

Ownership Ecosystem Awareness Is Weaker

The data suggests that consumers understand why EVs matter but remain uncertain about how EV ownership will fit into their daily lives. This is why this article should connect to the India EV charging infrastructure market and India automotive battery market pages when discussing charging confidence, range confidence, and battery ownership concerns.

Why Cost Still Pulls Buyers Toward ICE Vehicles

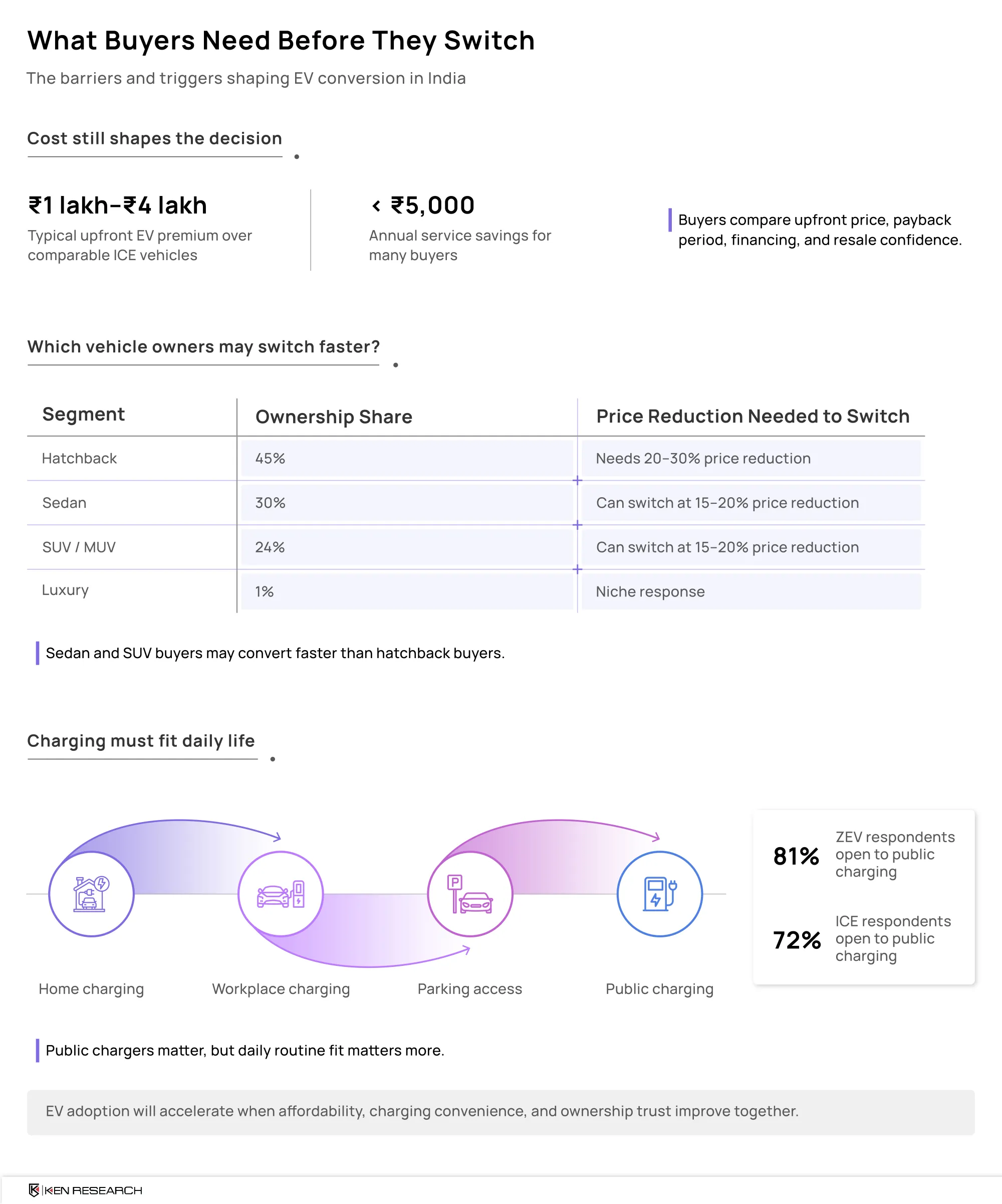

Vehicle affordability remains one of the strongest barriers to EV adoption. Most EVs currently carry an upfront premium ranging from Rs 1 lakh to Rs 4 lakh compared with equivalent ICE vehicles.

While EVs typically offer lower running and maintenance costs, the savings are distributed over several years. Buyers experience the purchase price immediately. Financing also becomes central to the EV adoption conversation, which makes the India car finance and leasing market and India car loan market.

For many consumers, the decision becomes a comparison between immediate upfront expenditure, long-term operating savings, resale uncertainty, battery questions, and financing considerations. As a result, ICE vehicles continue to feel like the safer financial choice despite the long-term economic advantages of EV ownership.

EV vs ICE in India: What Buyers Are Comparing

Factor | EV | ICE |

Purchase price | Higher | Lower |

Running cost | Lower | Higher |

Maintenance cost | Lower | Higher |

Fueling or charging convenience | Developing | Established |

Resale confidence | Lower | Higher |

Ownership familiarity | Lower | Higher |

Environmental impact | Better | Lower |

Government incentives | Available | Limited |

This comparison explains why many consumers continue to prefer ICE vehicles despite increasing interest in EVs.

How Vehicle Segment Shapes EV Switching Behaviour

Current ownership patterns significantly influence conversion potential. Segment-level pricing sensitivity determines how quickly consumers may switch from ICE vehicles to EVs.

- SUV and sedan owners are more likely to switch at a 15-20% price reduction threshold.

- Hatchback owners typically require a 20-30% price reduction before considering a switch.

- Hydrogen remains structurally weaker in buyer preference, with meaningful response improving only beyond a 50% reduction threshold.

This suggests that EV adoption may accelerate faster in premium and mid-segment categories before reaching highly price-sensitive hatchback segments. For premium adoption context, this section can naturally link to the India luxury car market page.

Why Charging Confidence Is Still Incomplete

Charging concerns remain one of the most important ownership barriers. Public charging acceptance is already relatively high, but charging confidence extends beyond public charging availability.

Group | Public Charging Acceptance |

ZEV respondents | 81% |

ICE respondents | 72% |

Consumers evaluate home charging access, apartment parking infrastructure, workplace charging facilities, public charging accessibility, charging reliability, and charging time. For most buyers, the question is not whether charging stations exist. The question is whether charging can seamlessly fit into daily routines.

This section should link directly to the India EV charging infrastructure market because charging availability is one of the strongest adoption enablers.

What EV Brands Need to Solve Next

Indian consumers are not rejecting EVs. They are evaluating them more seriously than ever before. However, ICE vehicles continue to win because they feel familiar, financially predictable, operationally convenient, and lower-risk.

1. Cost Confidence

Buyers must clearly understand ownership economics, payback periods, financing options, and long-term operating savings.

2. Charging Confidence

Charging infrastructure must become accessible, reliable, and convenient across home, workplace, apartment, and public environments.

3. Ownership Confidence

Consumers need stronger assurance around battery life, resale value, maintenance support, service network availability, and long-term ownership outcomes.

The next phase of India's four-wheeler mobility transformation will not be driven by awareness alone. It will be driven by brands that make EV ownership practical, predictable, and financially sensible.

Frequently Asked Questions

What percentage of Indian car buyers are considering EVs?

According to Ken Research field data, 29% of respondents showed EV purchase intent, while 71% still preferred ICE vehicles.

Why do Indian buyers still prefer ICE vehicles?

Indian buyers still prefer ICE vehicles because they feel familiar, financially predictable, easier to refuel, easier to service, and lower-risk in terms of resale and long-term ownership.

What is the biggest barrier to EV adoption in India?

The biggest barriers are upfront price premium, charging convenience, resale uncertainty, battery-life concerns, and limited confidence in the complete EV ownership ecosystem.

Which age group is most interested in EVs in India?

The 26-40 age group shows the strongest EV intent, accounting for 65% of EV-intent respondents.

Are EVs cheaper to maintain than ICE vehicles?

EVs can have lower running and servicing costs, but annual service savings of less than Rs 5,000 may not be enough to offset the higher upfront price for many buyers.

How much more expensive are EVs compared to ICE vehicles in India?

Comparable EVs currently carry an upfront price premium of around Rs 1 lakh to Rs 4 lakh over ICE vehicles.

Why is charging infrastructure important for EV adoption?

Charging infrastructure matters because buyers need charging to fit into daily routines through home charging, workplace charging, parking access, and reliable public charging.

Are Indian buyers aware of EV environmental benefits?

Yes. Awareness of air pollution, GHG emissions, and improved air quality is high, especially among ZEV-intent respondents.

Which vehicle segment may switch to EVs faster?

Sedan and SUV/MUV buyers may switch faster because they show stronger conversion potential at a 15-20% price reduction trigger.

Why are hatchback buyers harder to convert to EVs?

Hatchback buyers are more price-sensitive and typically require a deeper 20-30% price reduction trigger before switching to EVs.

Will EV adoption continue to grow in India?

Yes. EV adoption is expected to grow as affordability improves, charging access expands, and buyers gain stronger confidence in battery life, resale value, and ownership economics.

Research Methodology

This article is based on Ken Research's field-based consumer survey insights focused on India four-wheeler mobility decision-making.

- Sample size: 5,000 respondents

- Geography: 15 major Indian cities

- Vehicle category: Four-wheeler mobility market

- Research approach: Field-based consumer survey

- Focus areas: EV purchase intent, consumer awareness, charging infrastructure perception, ownership behavior, cost sensitivity, switching triggers, and mobility preferences

The findings provide directional insight into the evolving EV adoption landscape and consumer decision-making patterns within India's passenger vehicle market.

Relevant Ken Research market intelligence includes the following:

India Electric Vehicle Market

India EV Charging Infrastructure Market

India Automotive Battery Market

India Car Finance Market

India Car Leasing Market

India Connected Car Market

Get started

We've helped companies around the world future-proof

their businesses - and we can do the same for you.